Currencies

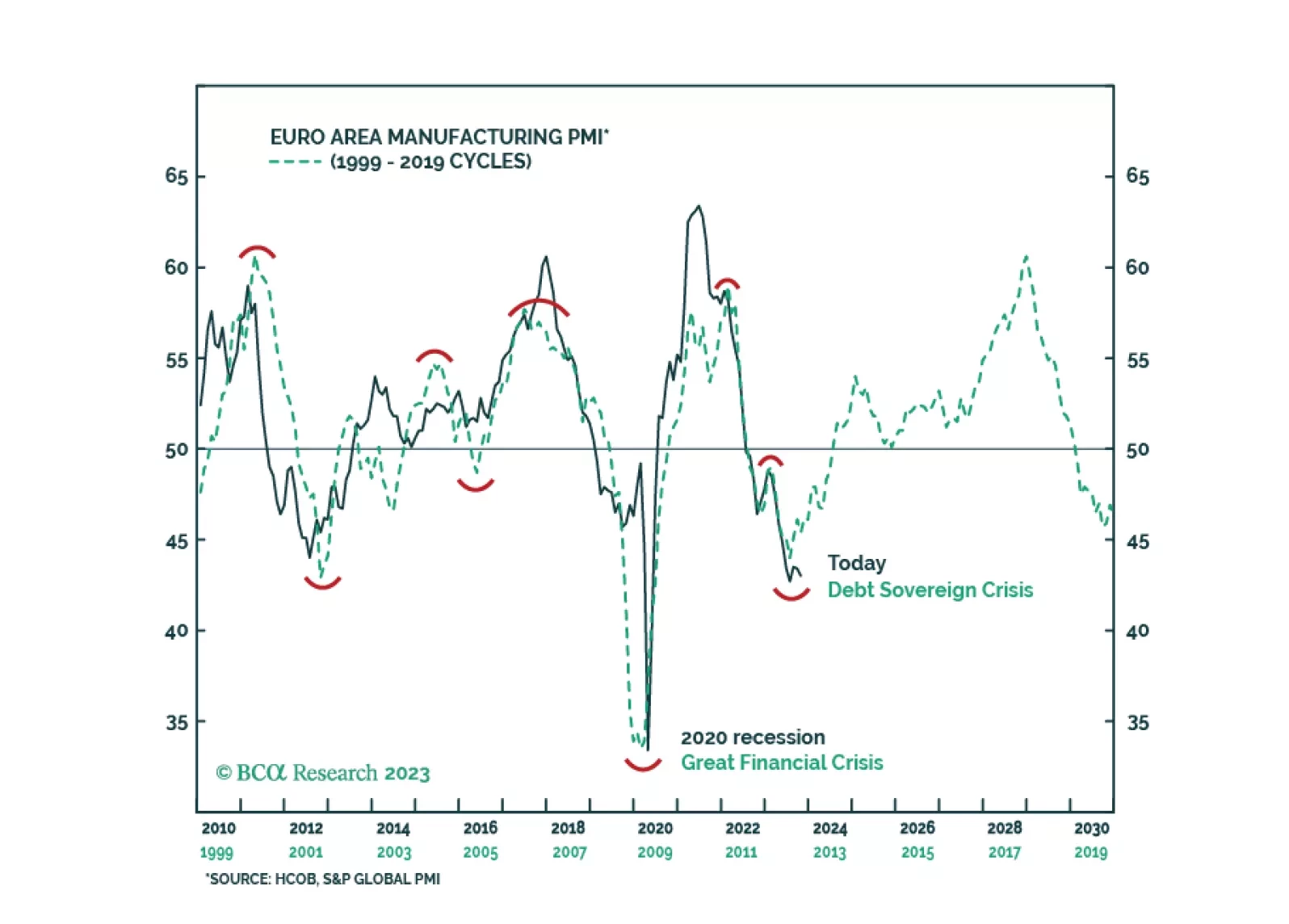

What will the next manufacturing cycle look like in Europe and how will risk assets perform? Lessons from the recent past.

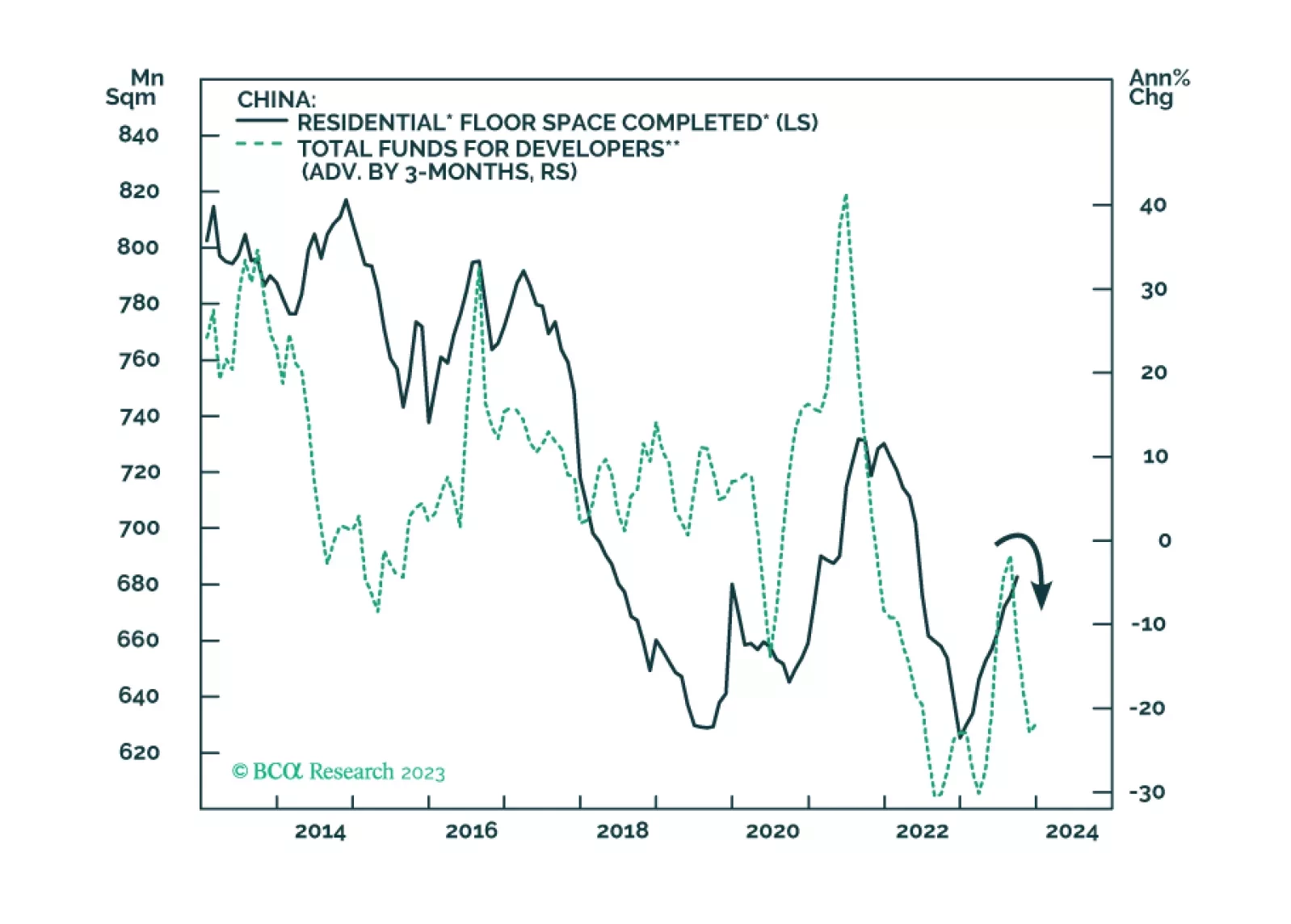

China’s economic growth will stagnate, at best, rather than revive. Lower valuations of Chinese equities are justified, and share prices have more downside. The RMB will continue to depreciate versus the US dollar.

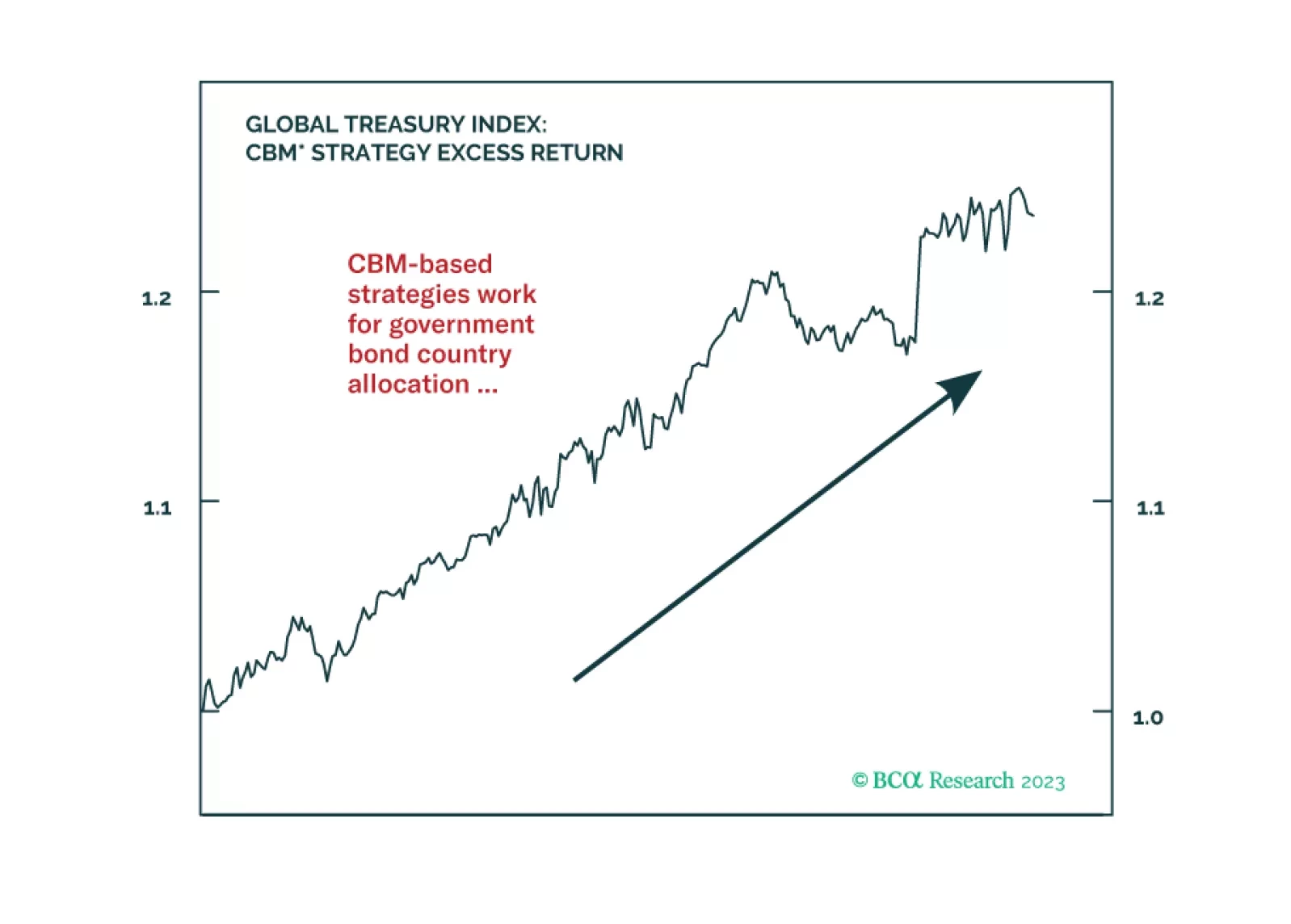

In this Special Report, we introduce two strategies that use our Central Bank Monitors for global fixed income country allocations and currency trades. We find that using the Monitors in country selection helps improve the performance of a developed markets government bond portfolio. The CBMs can also help substantially minimize the drawdowns on a standard FX carry strategy.

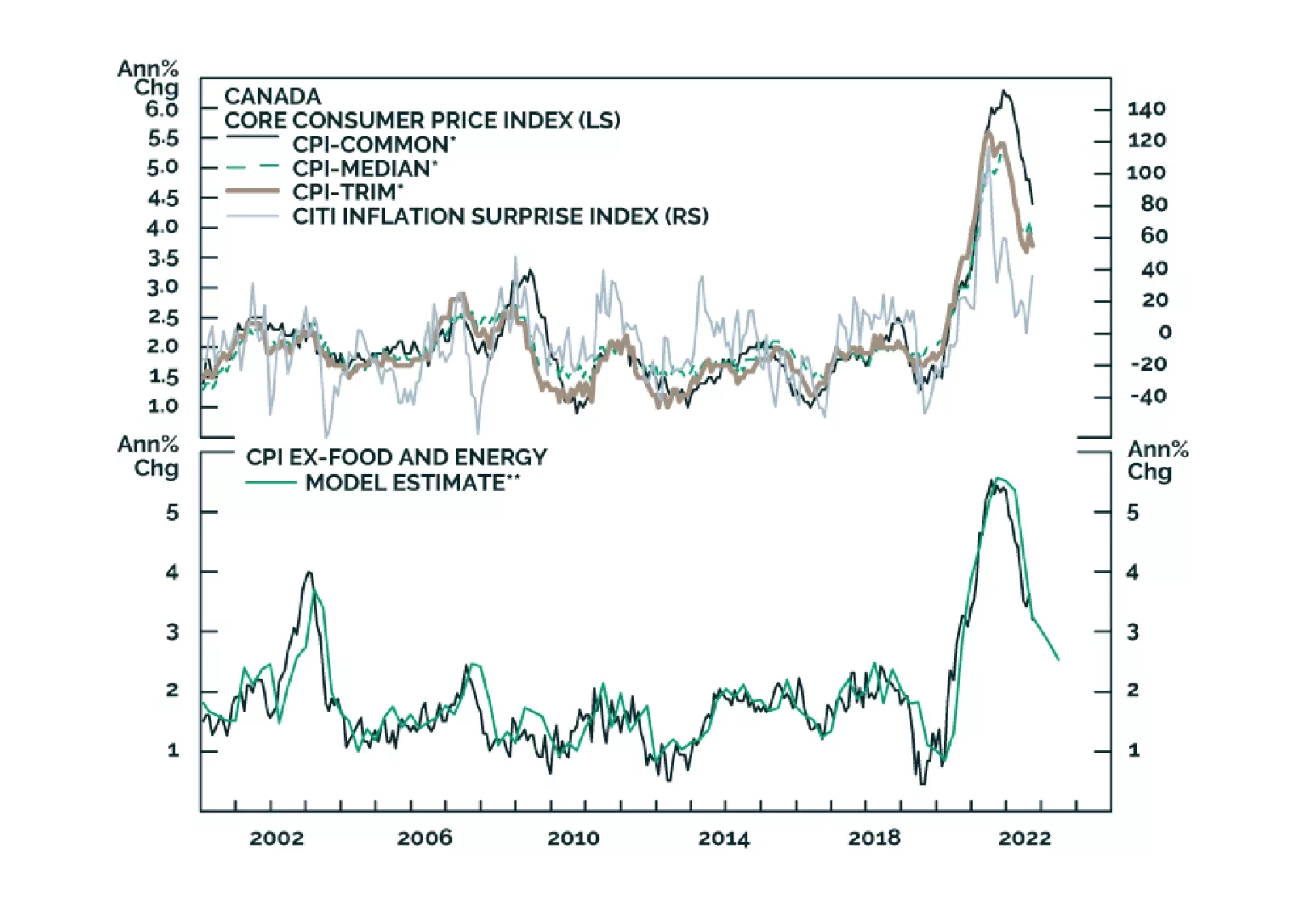

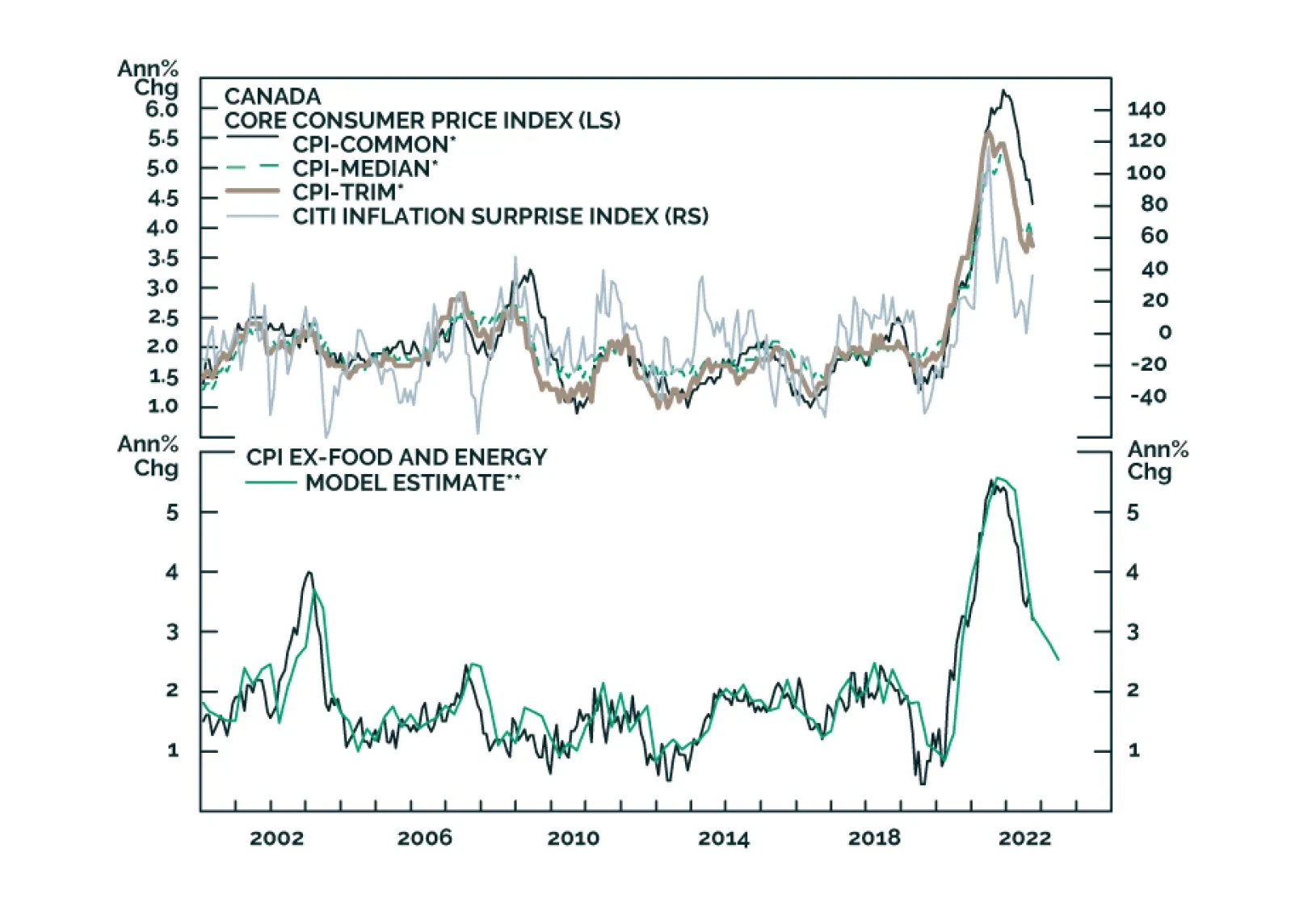

In this insight, we look at whether the recent data justifies a shift by the BoC, and some potential trades.

In this insight, we look at whether the recent data justifies a shift by the BoC, and some potential trades.

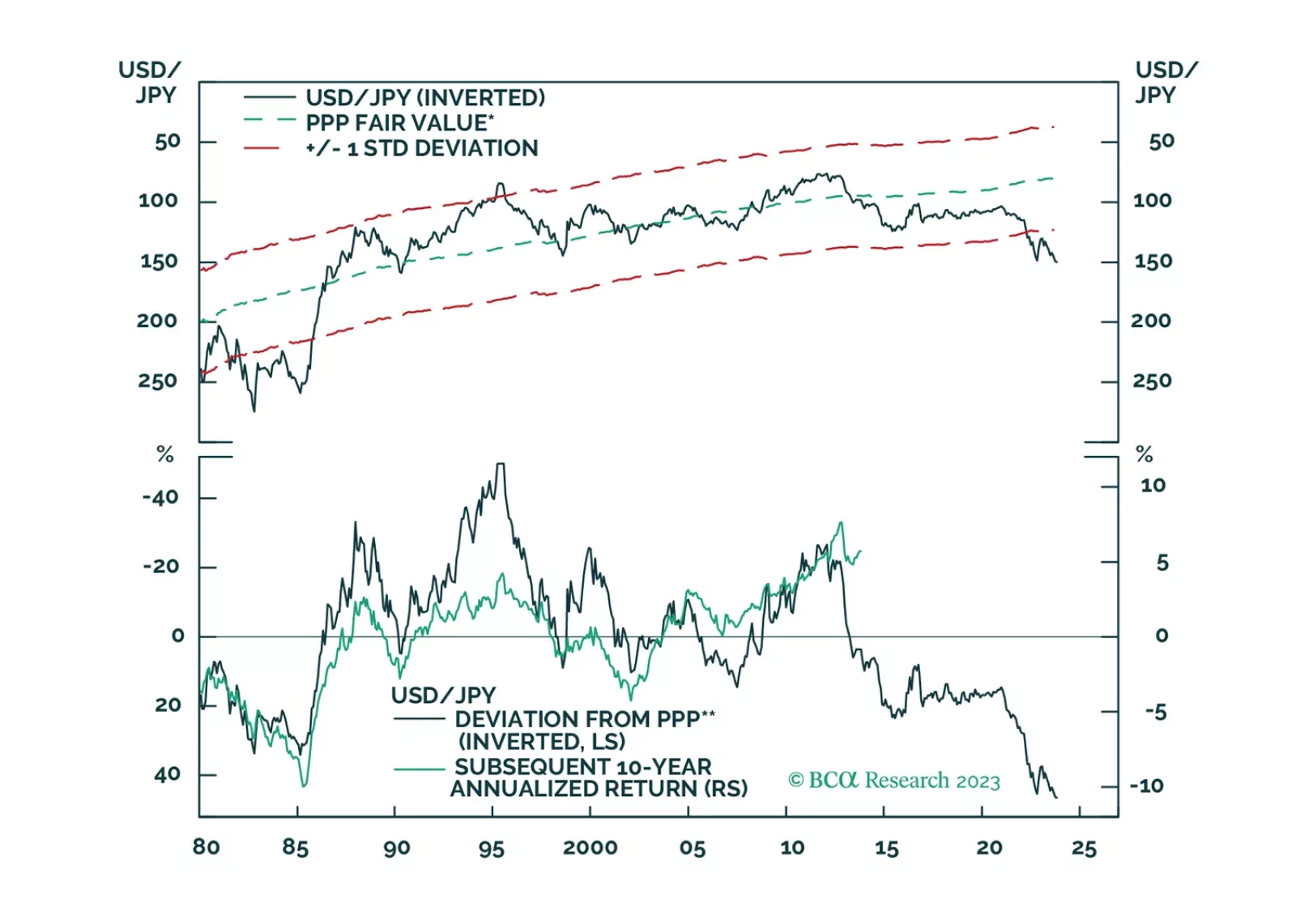

There is a high probability that the global economy will tip into recession in the second half of 2024. A long yen position is an excellent hedge against that risk.