Economic Growth

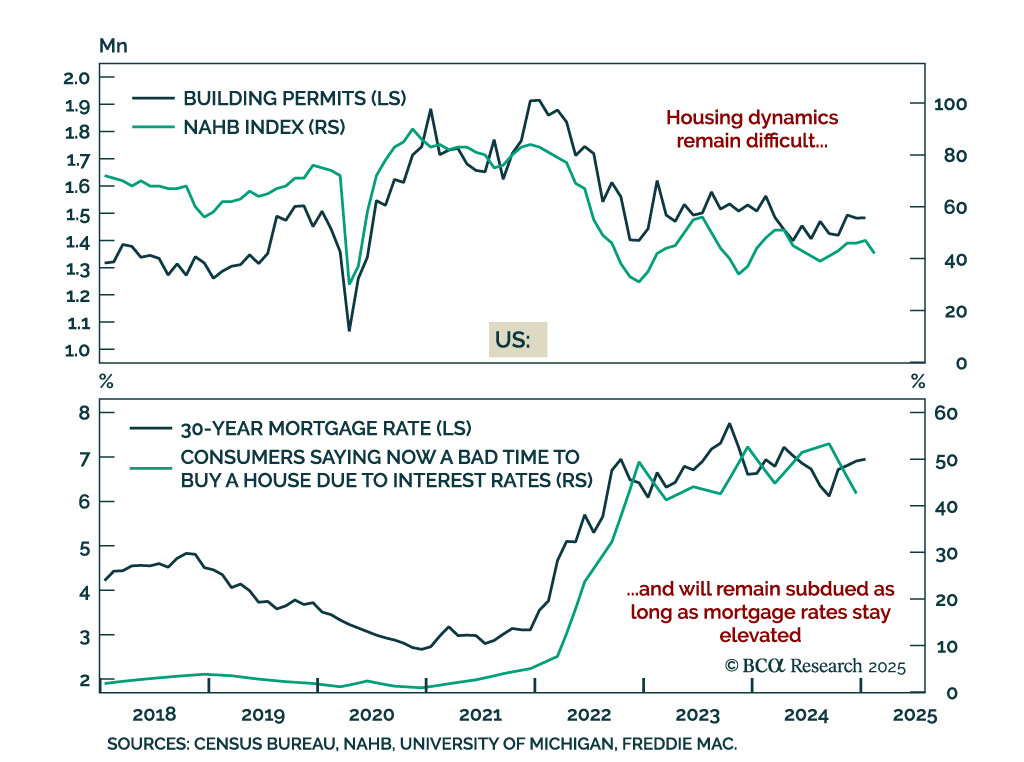

US January housing data disappointed, with housing starts falling 9.8% m/m after expanding 16.1% in December. The February NAHB Housing Market Index also weakened, falling to 42 from 47 in February. Building permits were the one positive surprise, growing…

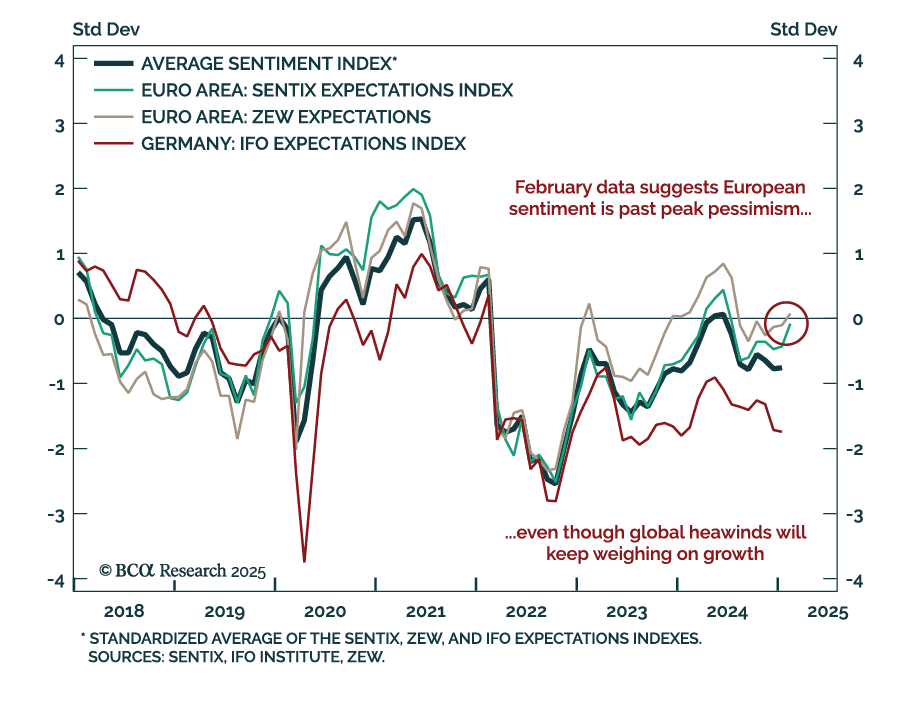

The February ZEW index for Germany and the eurozone beat estimates, with the expectations component rising to 26.0 from 10.3 a month prior. The current situation assessment also improved, although it remains deeply negative at -88.5. The improvement…

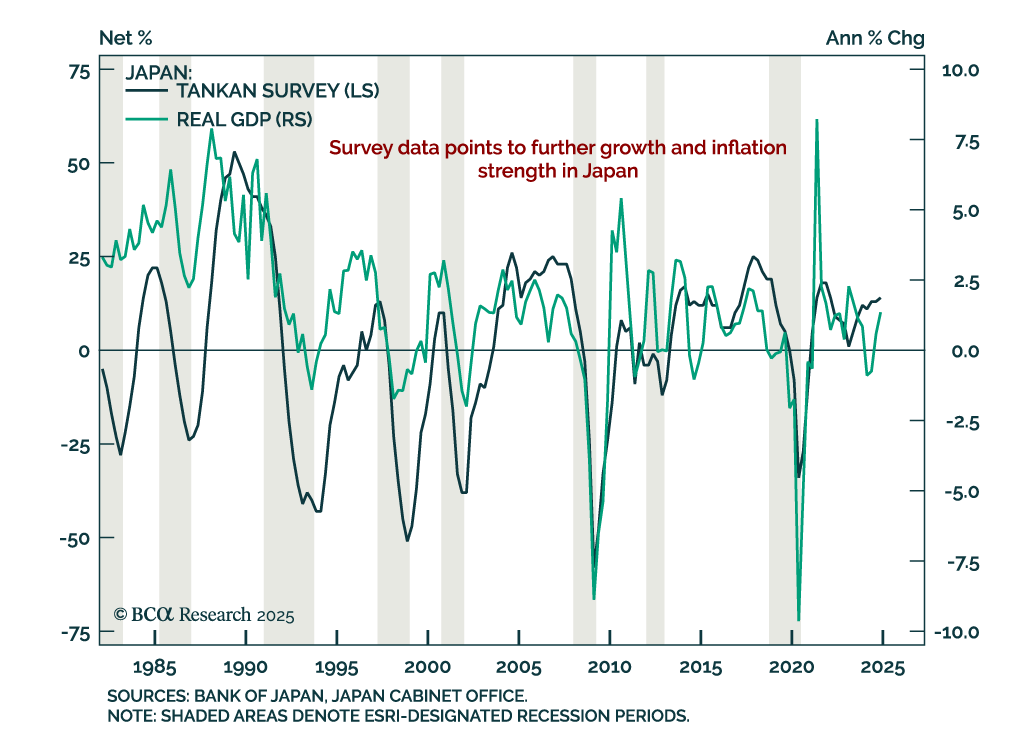

Preliminary estimates of Q4 real GDP growth in Japan was stronger than expected, rising to 2.8% q/q annualized from 1.7% in Q3. Domestic demand remained strong, and the GDP deflator increased to 2.8% y/y. Japan’s economy is running hot, sustaining price…

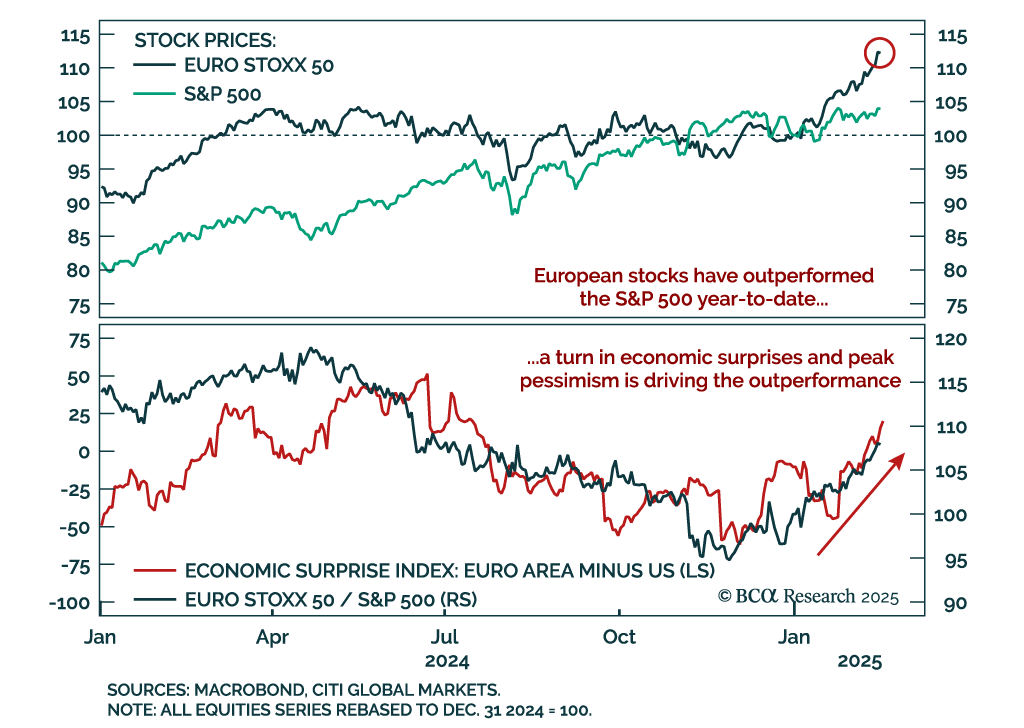

While the main Q1 2025 theme has been “America First”, the year-to-date market story has been more nuanced. “America First” would suggest an outperformance of US assets, but it is European assets that have started the year on a strong footing: The EURO STOXX…

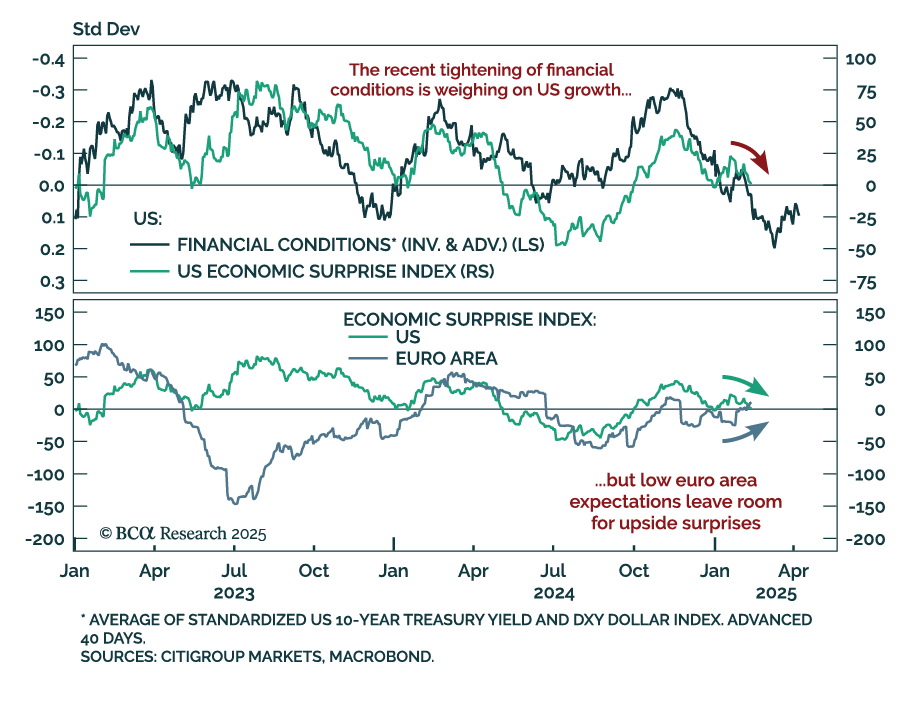

While geopolitics captured the latest headlines, Eurozone economic surprises have turned positive, while those in the US are on the verge of turning negative. Global economic surprises hinge on expectations and realized data, and they play a…

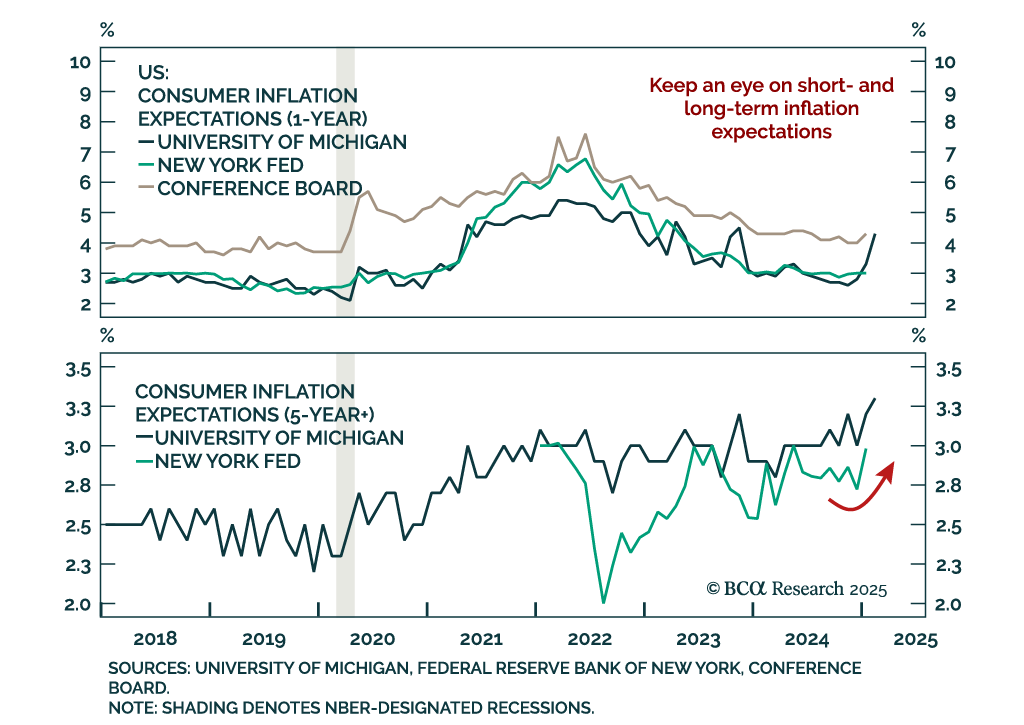

The New York Fed’s Survey of Consumer Expectations’ 1-year and 3-year inflation expectations were unchanged in January. Five-year ahead expectations however increased, as did expectations for staples inflation, while spending expectations…

Europe is about to become President Trump’s next target. The good news: a US/EU trade war will be short as common ground to achieve a deal exists. The bad news: European assets remain at the mercy of heightened uncertainty. How should investors position themselves in this tricky context?

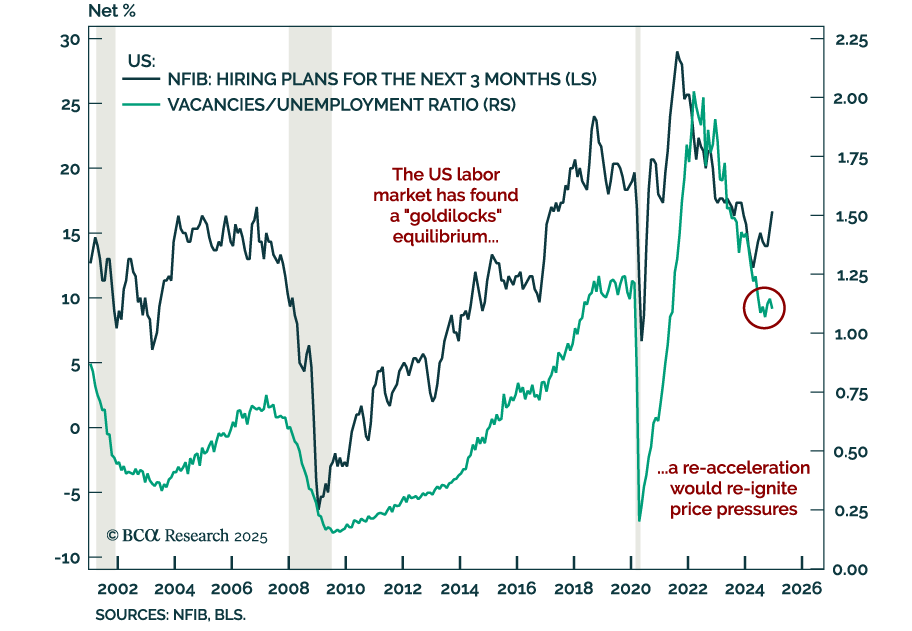

December job openings missed estimates, decreasing to 7.6m from an upwardly revised 8.2m in November. Quits, hires, but also layoffs all ticked up marginally, leaving the general “slowing-but-not-collapsing” direction of the labor market…

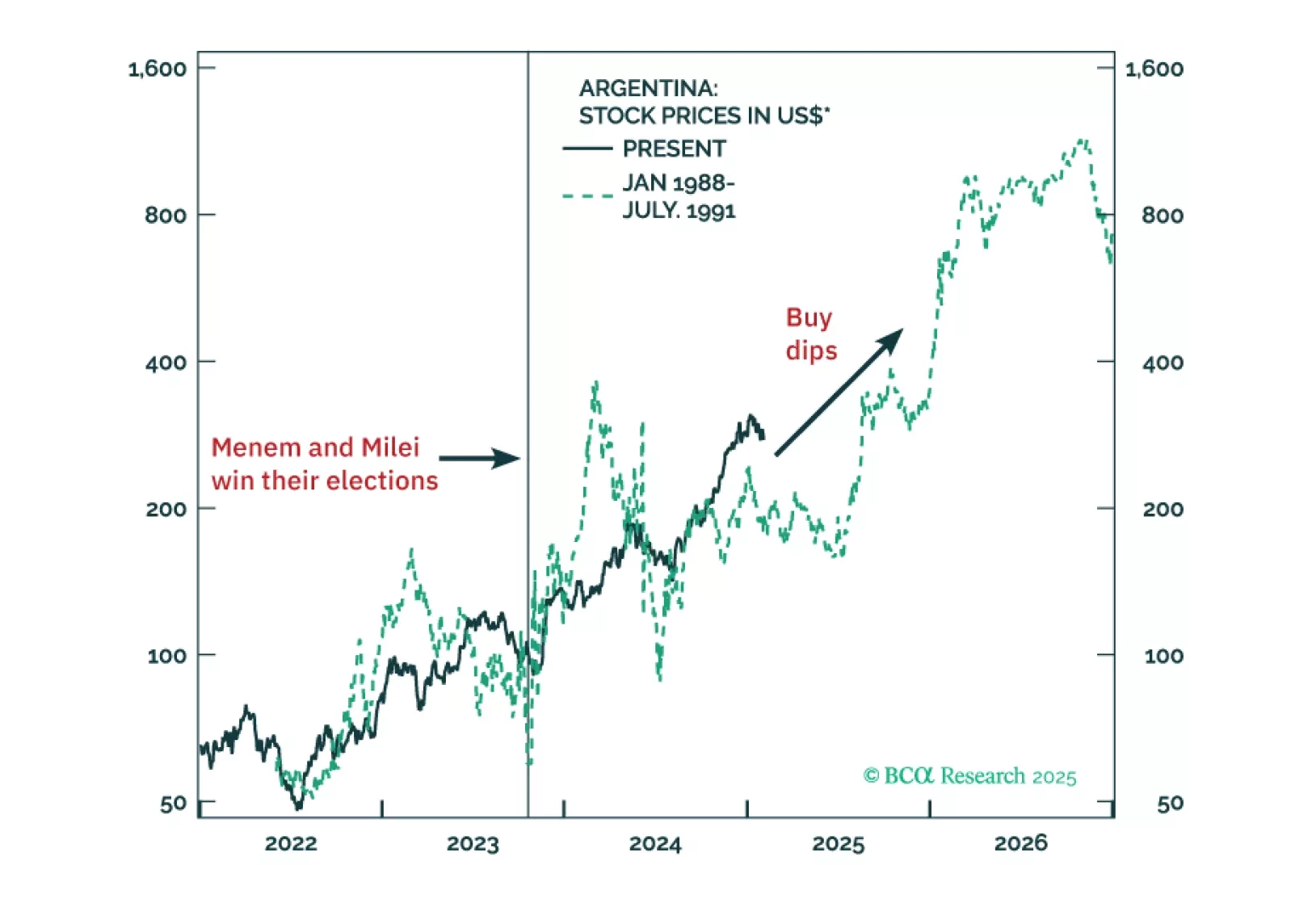

Argentina is entering a regime shift from the traditional short boom-bust cycles of the past 50 years. Profound structural reforms will result in a productivity boom, leading to a more durable economic expansion while keeping with the disinflation trend. Authorities will likely lift capital and currency controls in the second quarter of this year. All in all, odds are that Argentinian assets have entered a multi-year bull market.

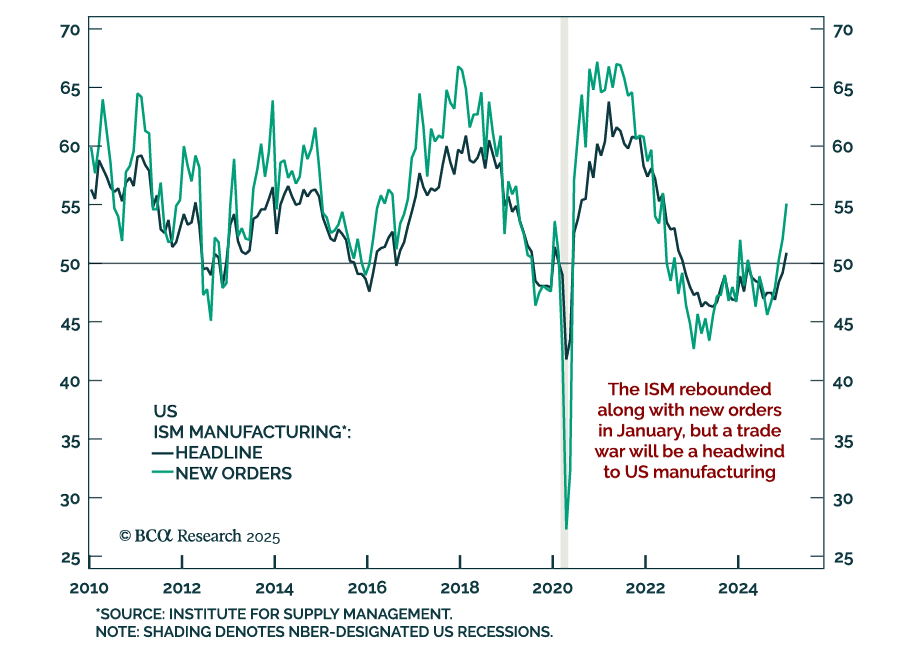

The January ISM Manufacturing index beat estimates, increasing to 50.9 to end a 26-month streak of manufacturing contraction. New orders rose to 55.1 from 52.1. Employment is also back in expansion. Prices paid strengthened as well, rising to 54.9 from…