Economy

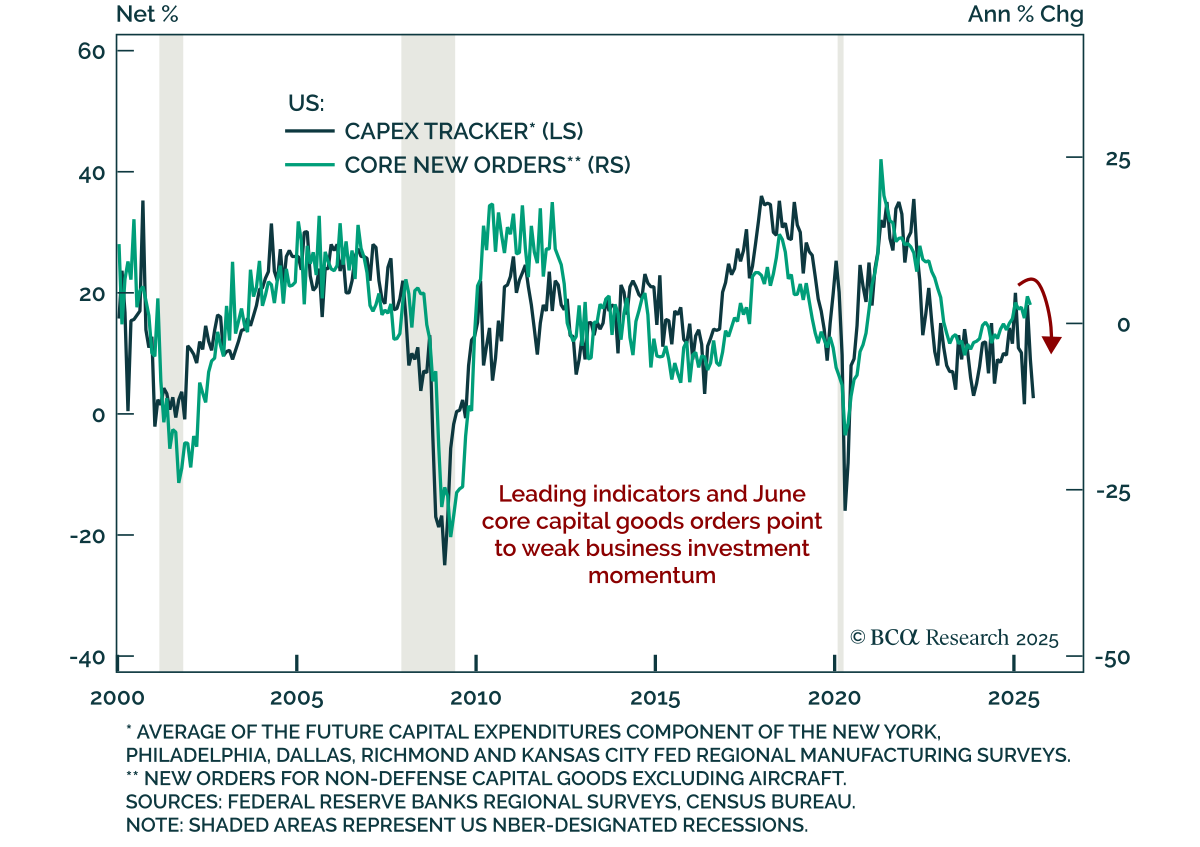

June core capital goods orders missed, confirming subdued capex momentum and reinforcing our defensive stance and long duration bias. Orders fell 0.7% m/m, below expectations, while shipments rose 0.4%. Headline durable goods dropped 9.3%, reversing…

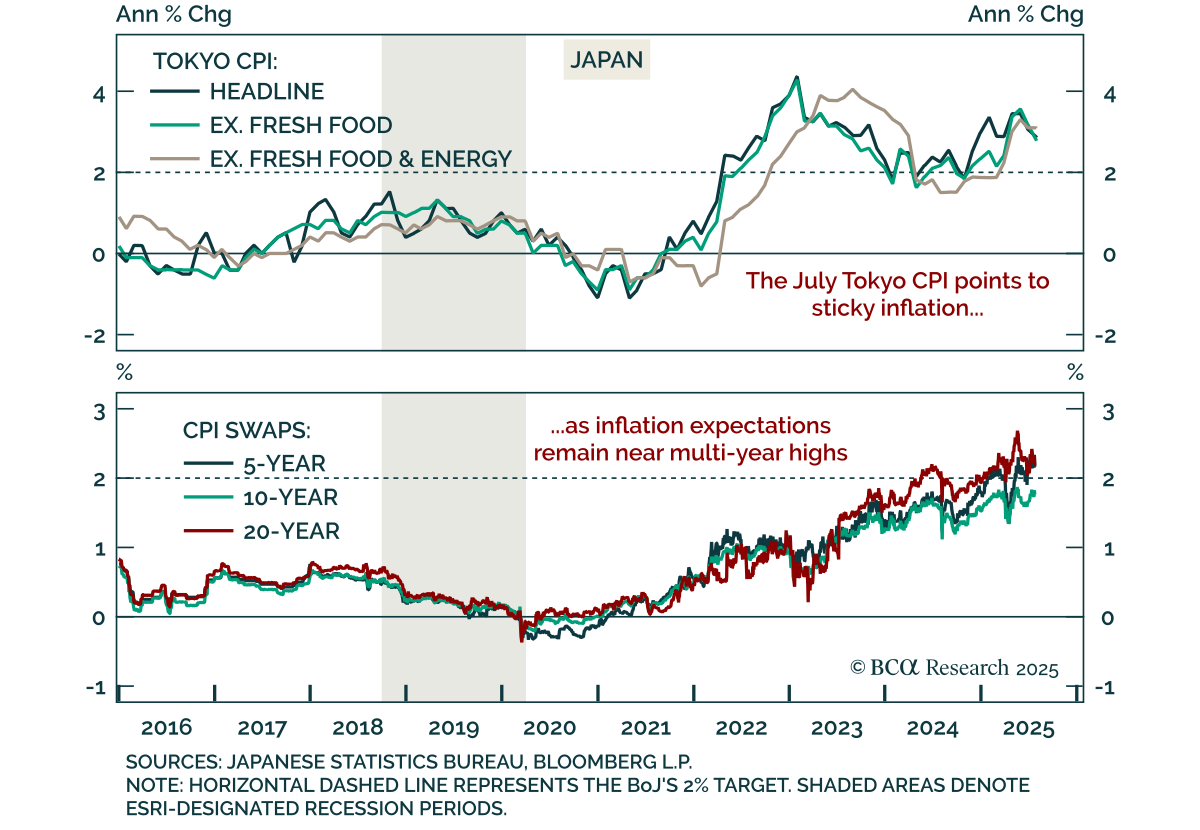

Tokyo CPI data confirms persistent inflation pressures in Japan, keeping the BoJ on a hawkish footing and reinforcing our underweight in JGBs and bullish stance on the yen. July Tokyo CPI came in broadly in line, falling to 2.9% y/y from 3.1%, with core and…

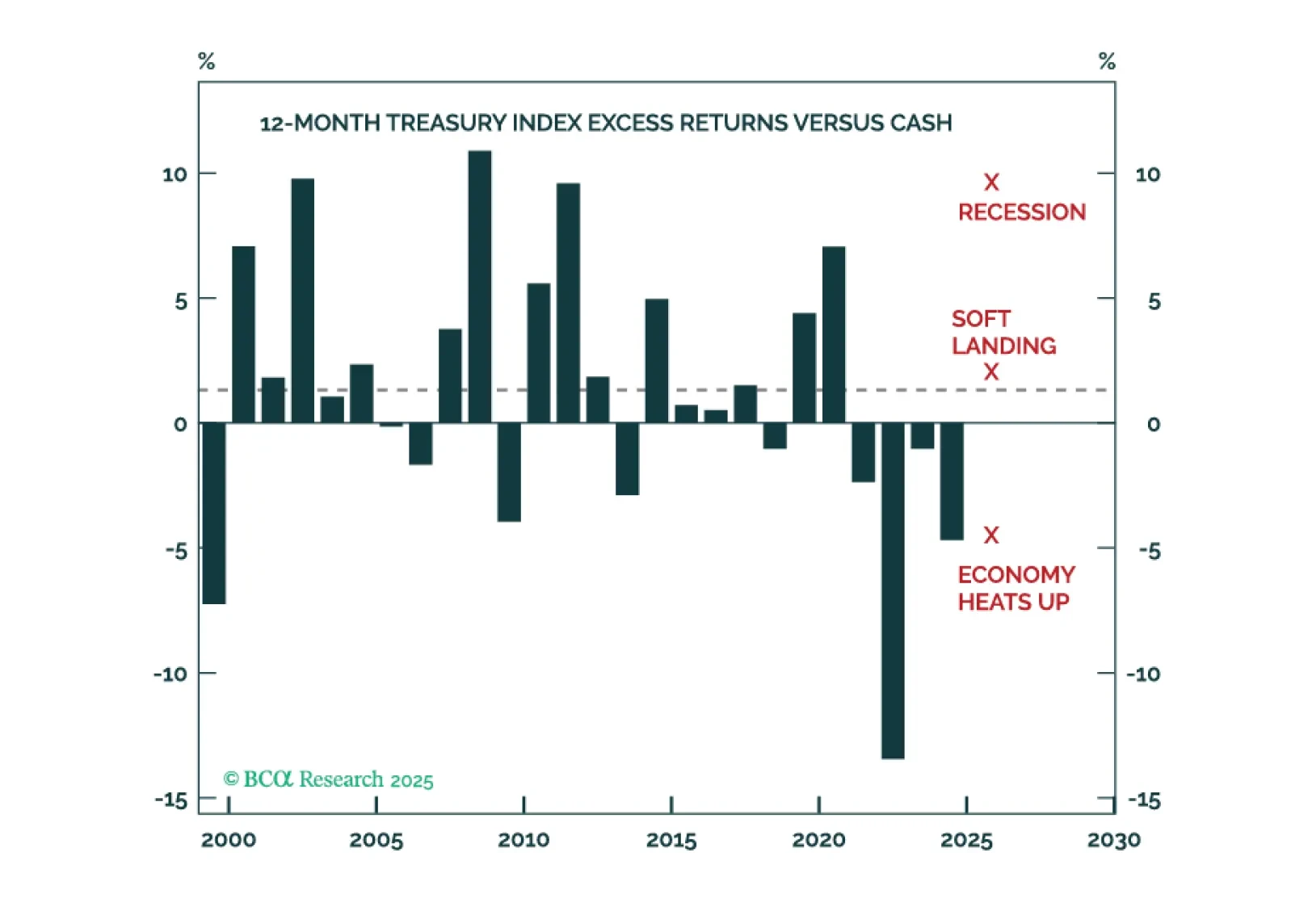

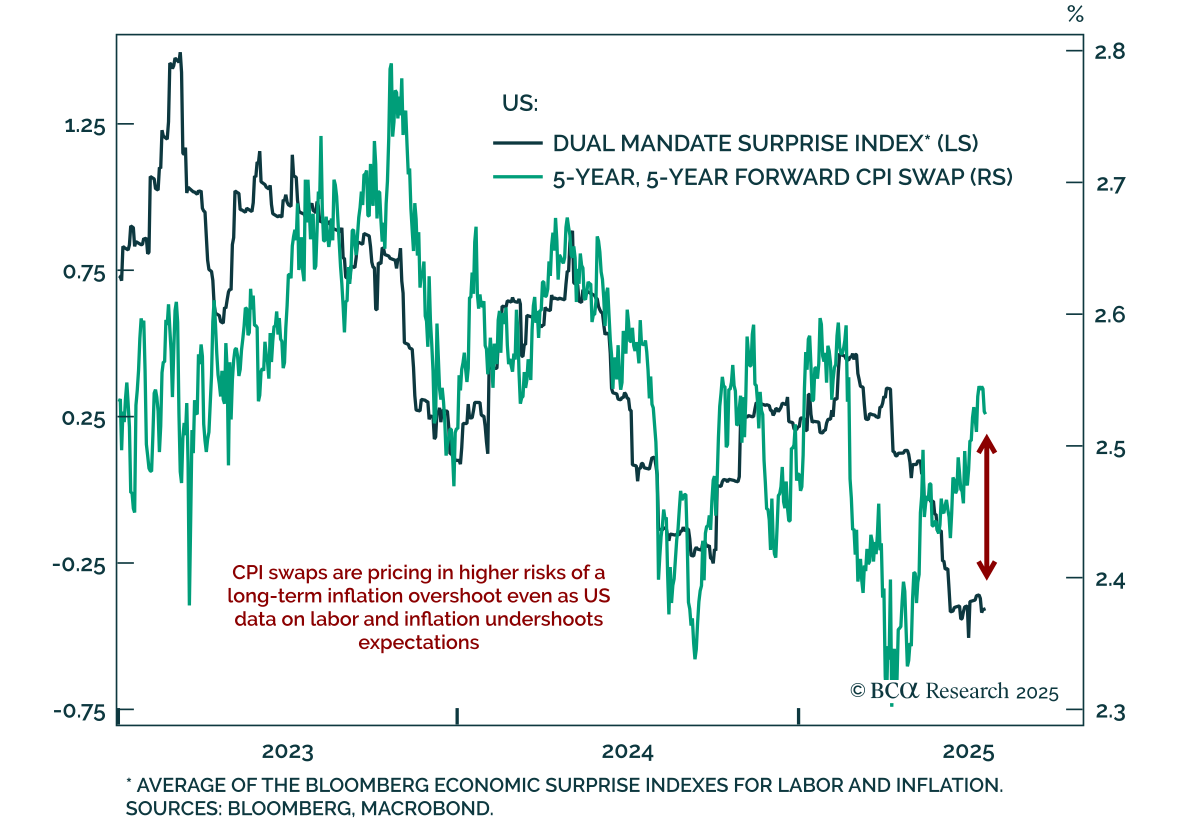

Investors should anticipate above average Treasury returns during the next 12 months, and curve steepeners will continue to profit.

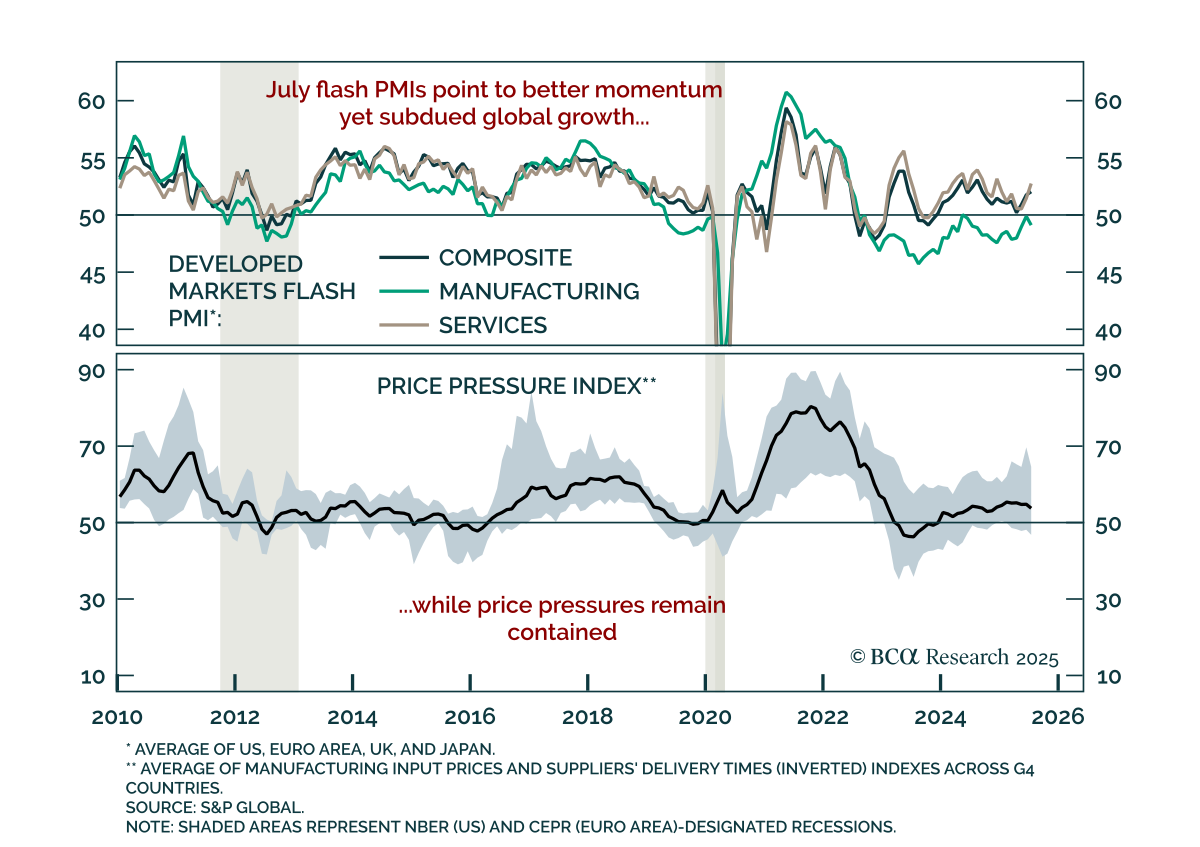

July DM flash PMIs point to improving global growth momentum led by services, but manufacturing remains weak and upside is limited, reinforcing our defensive stance. Services PMIs improved in the US, Europe, and Japan, but slowed in the UK. Manufacturing…

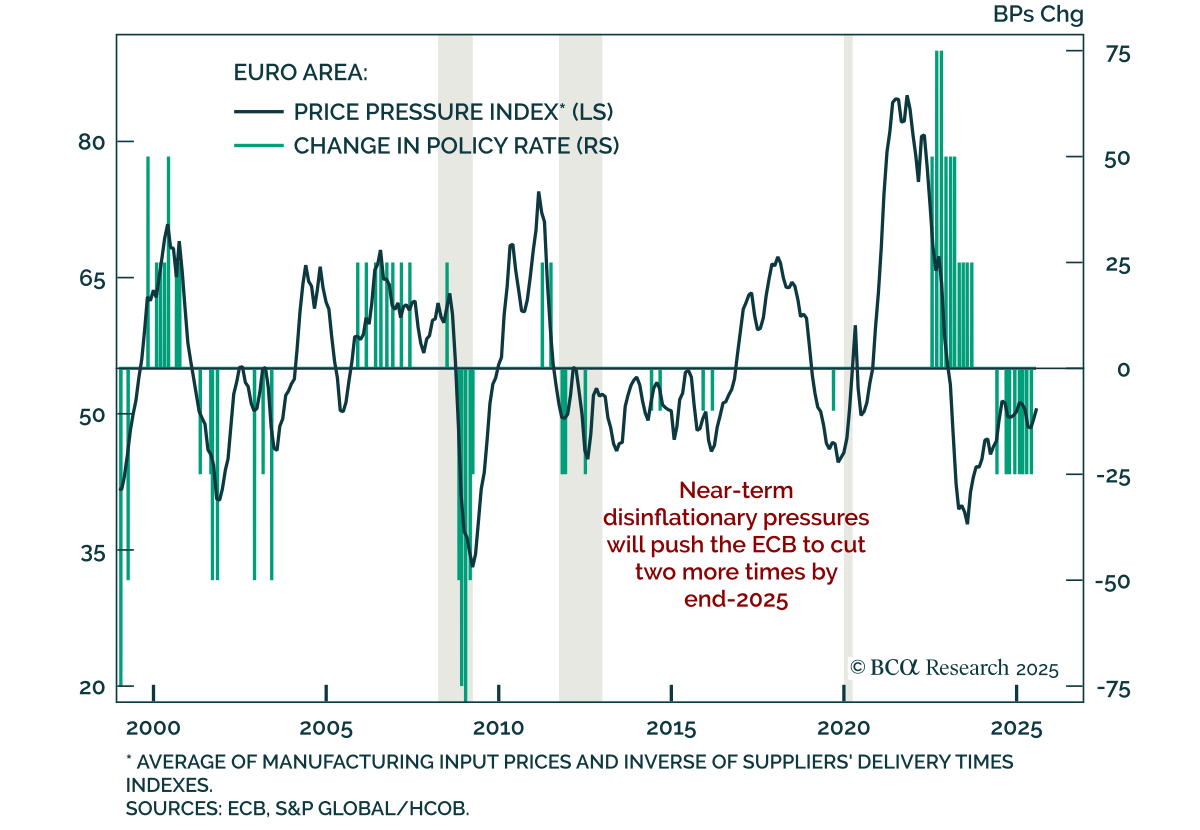

The ECB held rates steady for the first time in eight meetings, signaling a slower pace of easing while downside risks and entrenched disinflation support positioning for further cuts. The deposit facility rate remains at 2.0%, with the ECB adopting a…

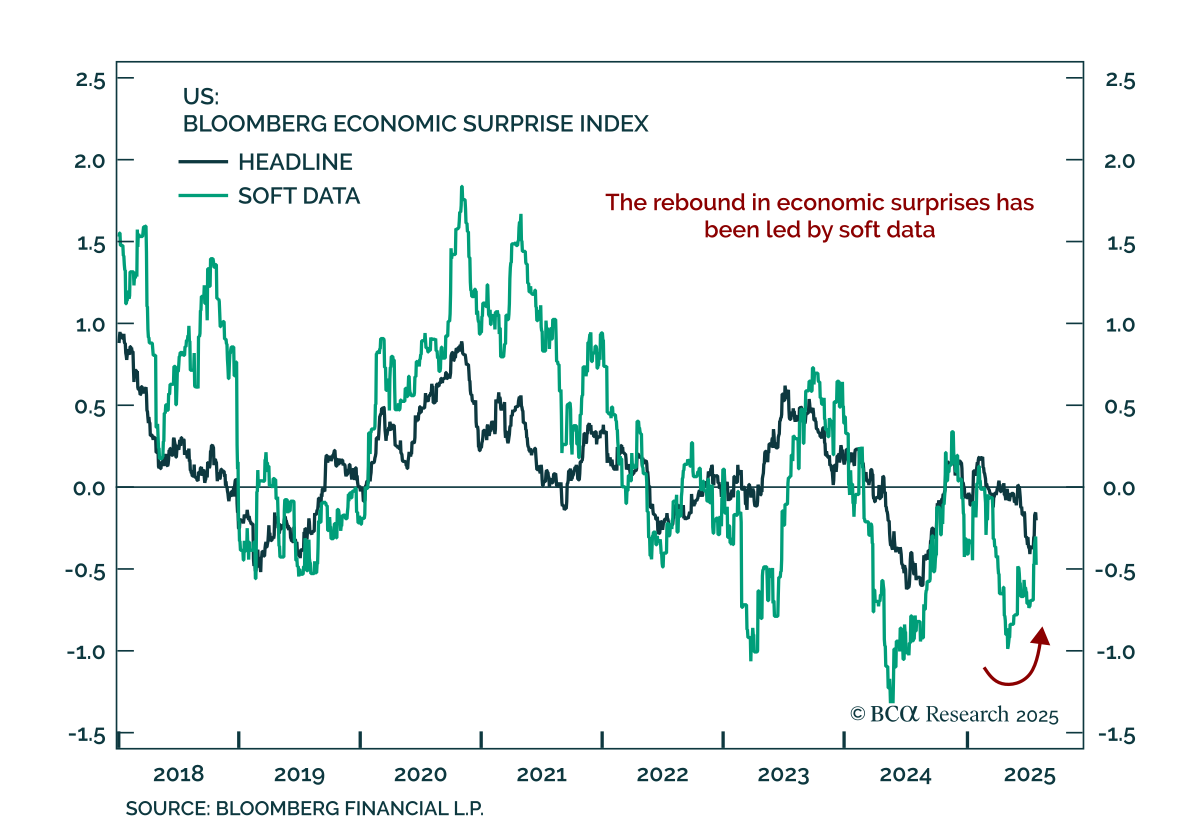

The post-Liberation Day dichotomy between improving soft data and worsening hard data points to an uneven recovery, keeping us positioned for downside risk. Soft data cratered post-Liberation Day as policy uncertainty and market volatility surged, with…

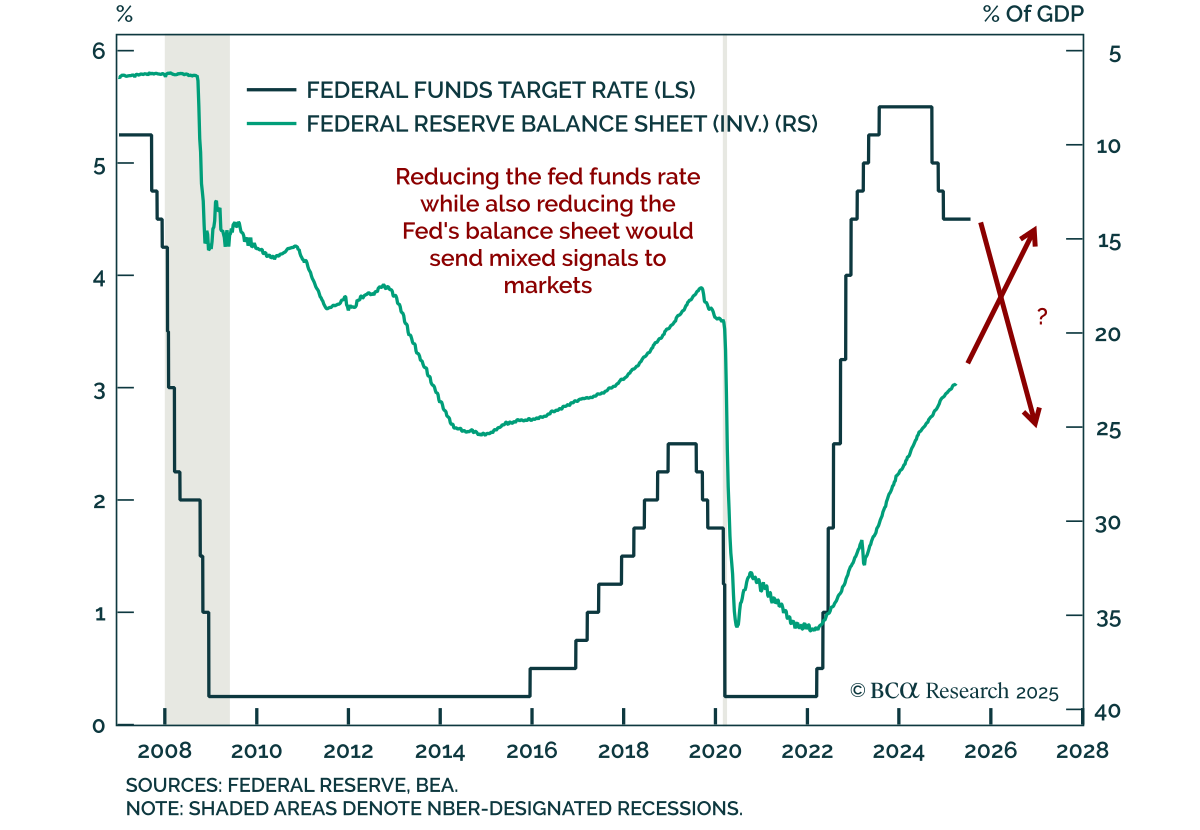

Recent criticism of the Fed centers on post-GFC policy, but proposed solutions would risk policy incoherence and higher long-end yields. Criticism covers the Fed’s reliance on balance sheet policies aimed at easing financial conditions after hitting the…

Rising political pressure on the Fed risks undermining policy credibility, risking a de-anchoring of long-term inflation expectations. The Trump administration keeps escalating attacks on Fed Chair Powell. While the Fed cannot ease proactively amid…

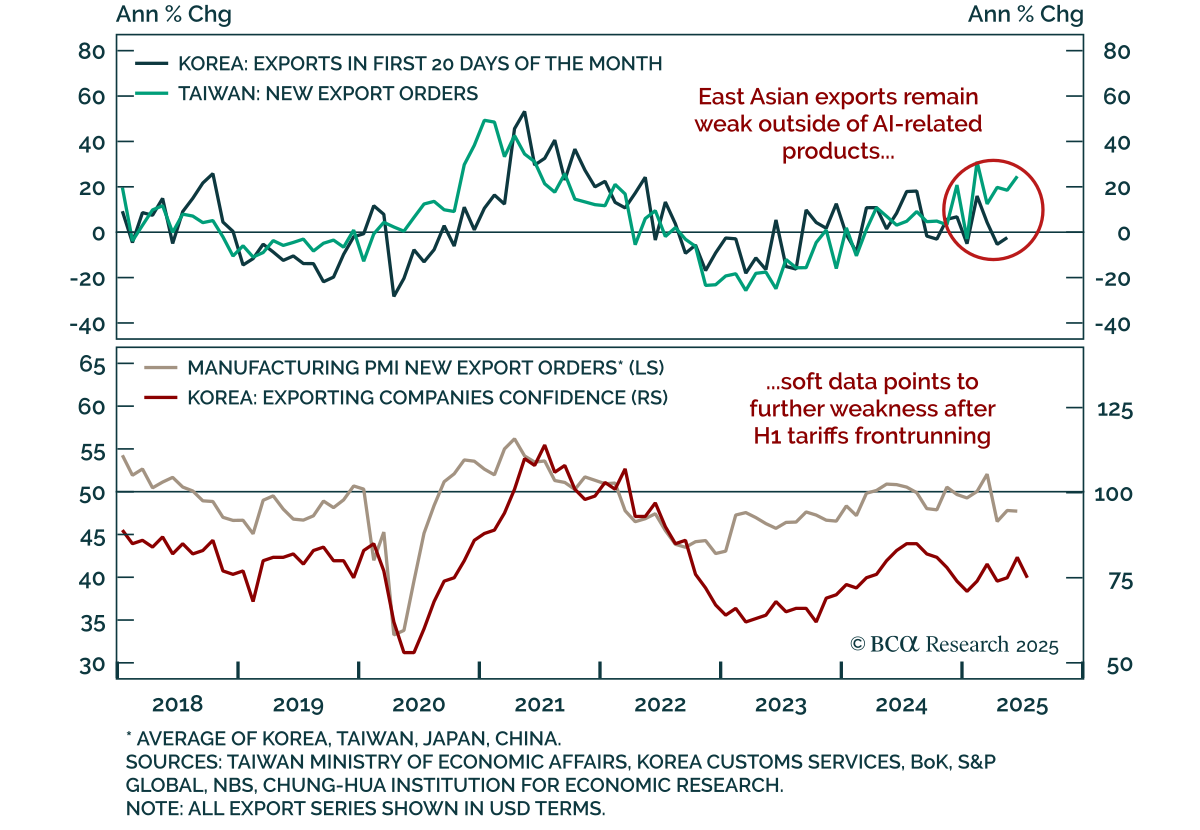

June Taiwanese export orders surprised to the upside, but weakness in non-tech trade and in broader East Asian exports underscores the narrowness of the global recovery. Orders rose 24.6% y/y, accelerating from 18.5% in May, though m/m US-bound orders fell…

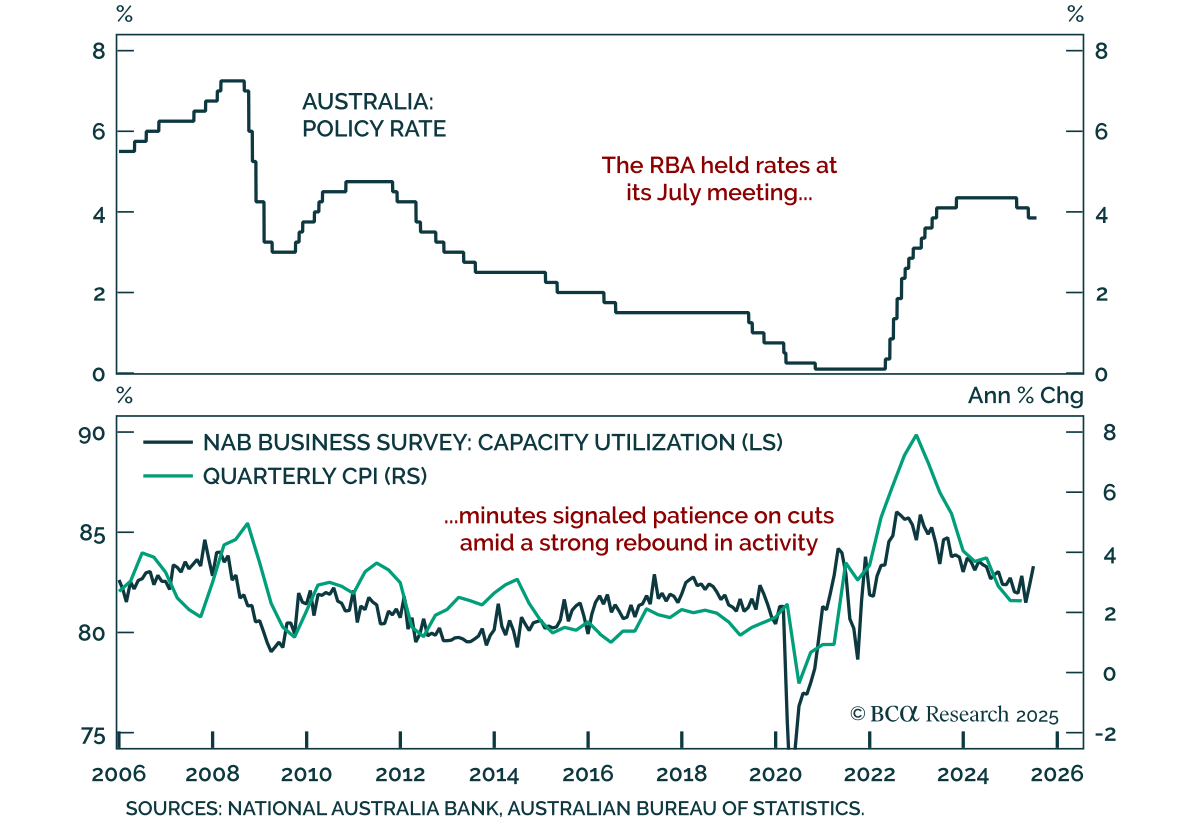

RBA minutes confirmed a cautious approach to easing, reinforcing our underweight in ACGBs and long AUD/NZD stance. The decision to hold at 3.85% surprised markets expecting a 25 bps cut. Governor Bullock had framed the decision as one of timing, but…