Economy

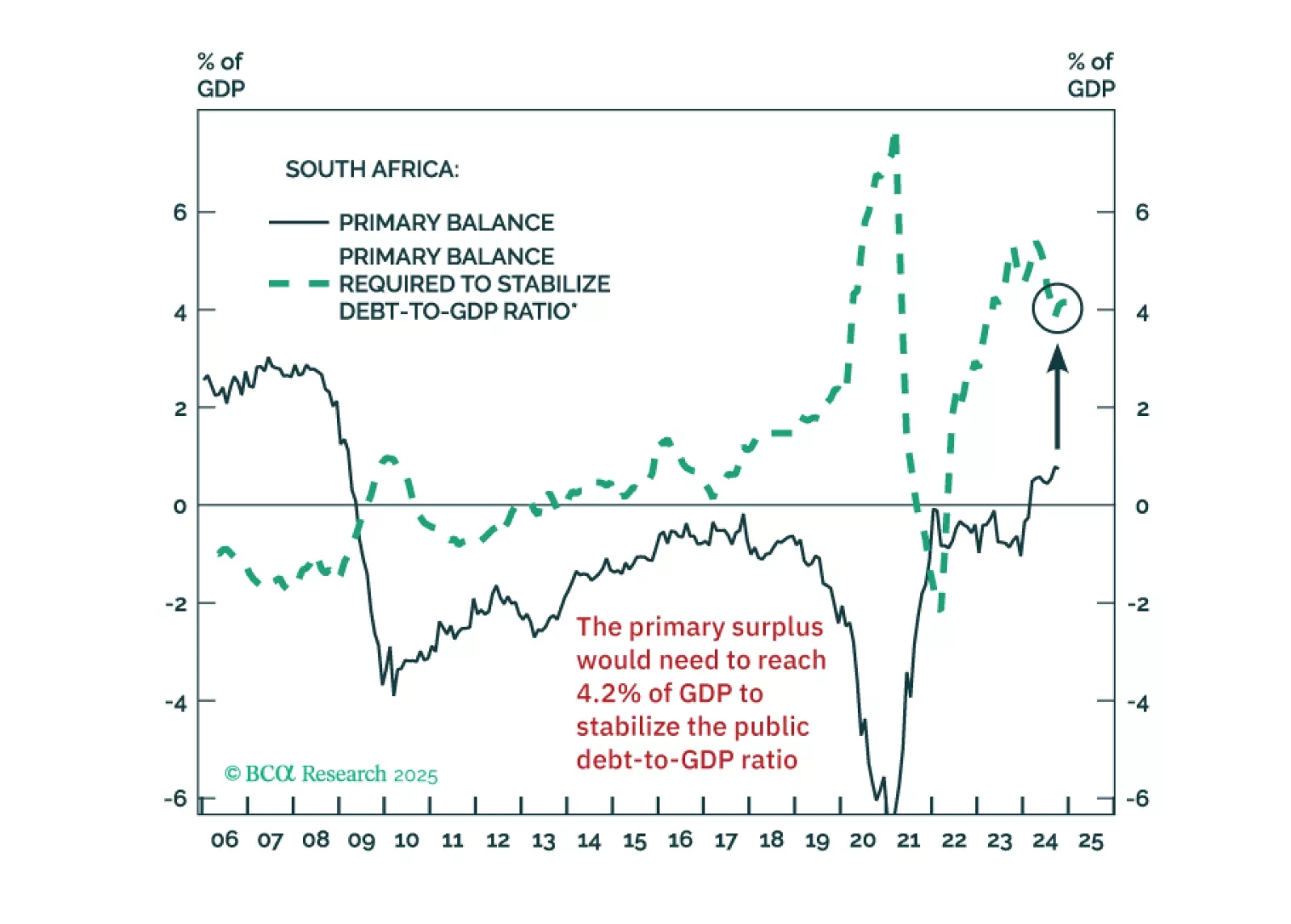

The South African government seems to believe that some fiscal retrenchment can stabilize the public debt-to-GDP ratio. But that’s a misconception. The country will need draconian spending cuts to achieve this.

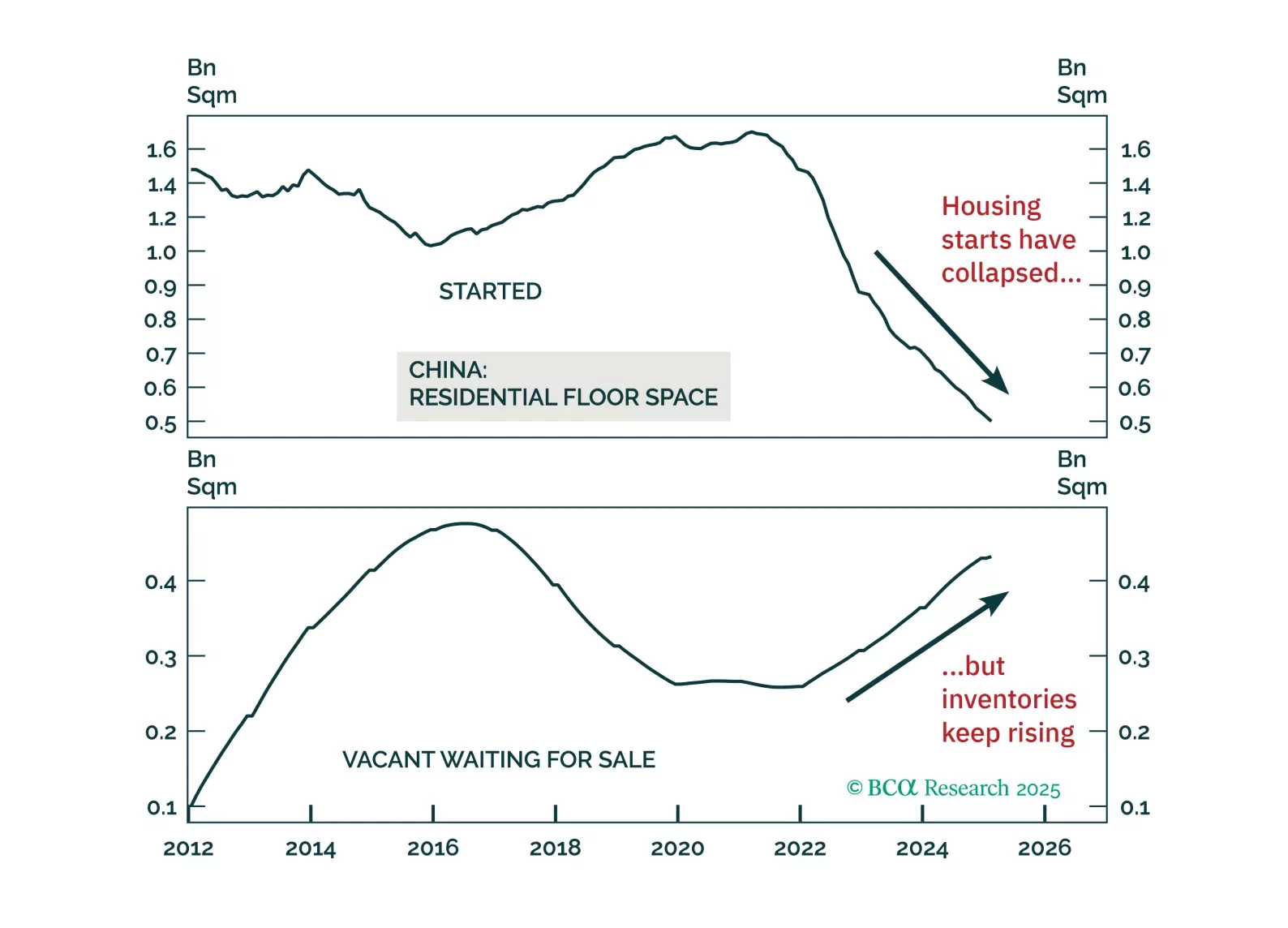

Data released this Monday suggests that while China’s housing market is no longer worsening, the secular adjustment remains ongoing. Although aggregate housing demand may be stabilizing at a low level, supply will continue to significantly outpace demand, indicating that home price deflation will persist. Additionally, property developers’ poor financing will hinder new project initiations, leading to a further decline in housing starts over the next six to 12 months.

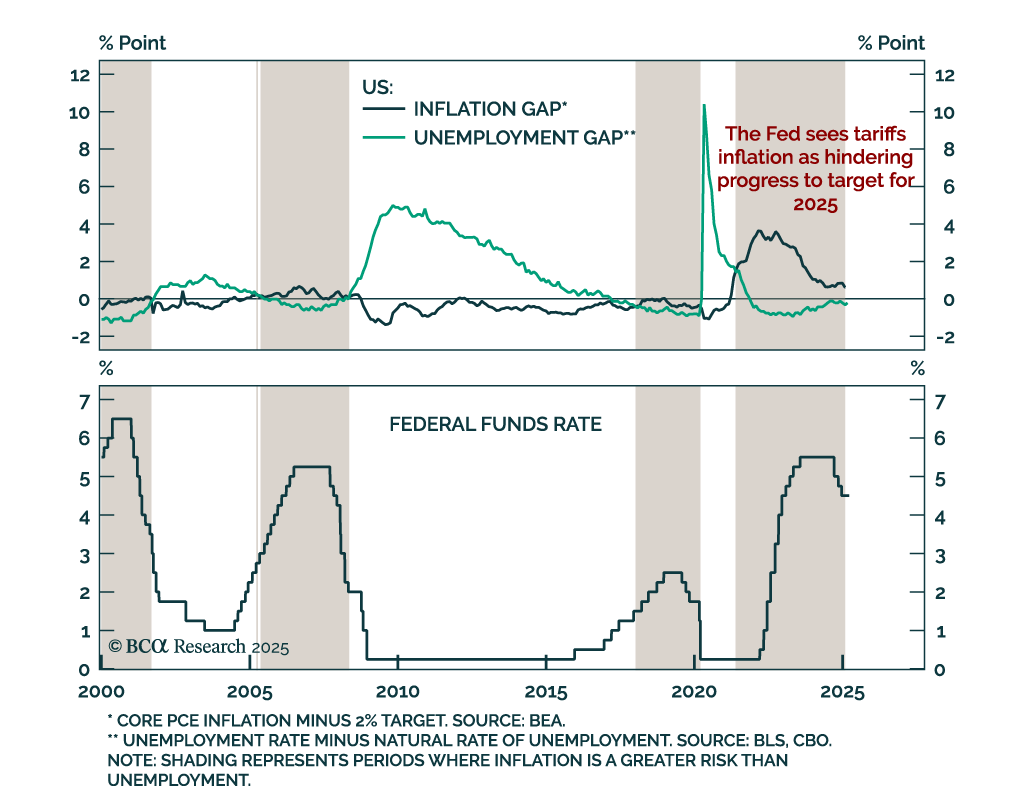

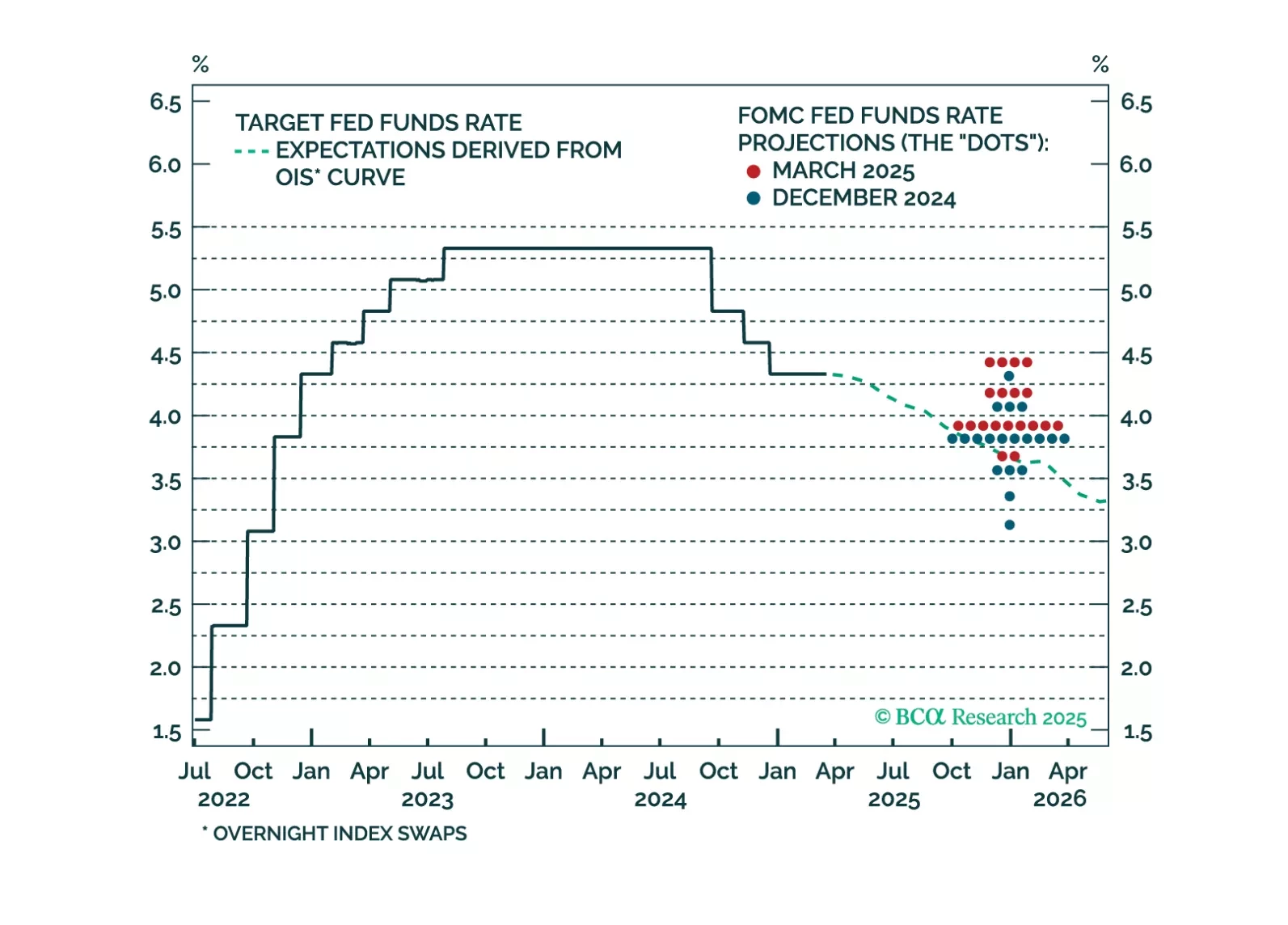

The market reaction to this afternoon’s Fed meeting looks overdone. Investors could be in for a hawkish surprise when it becomes apparent that the Fed won’t ease policy into higher tariff-driven inflation prints.