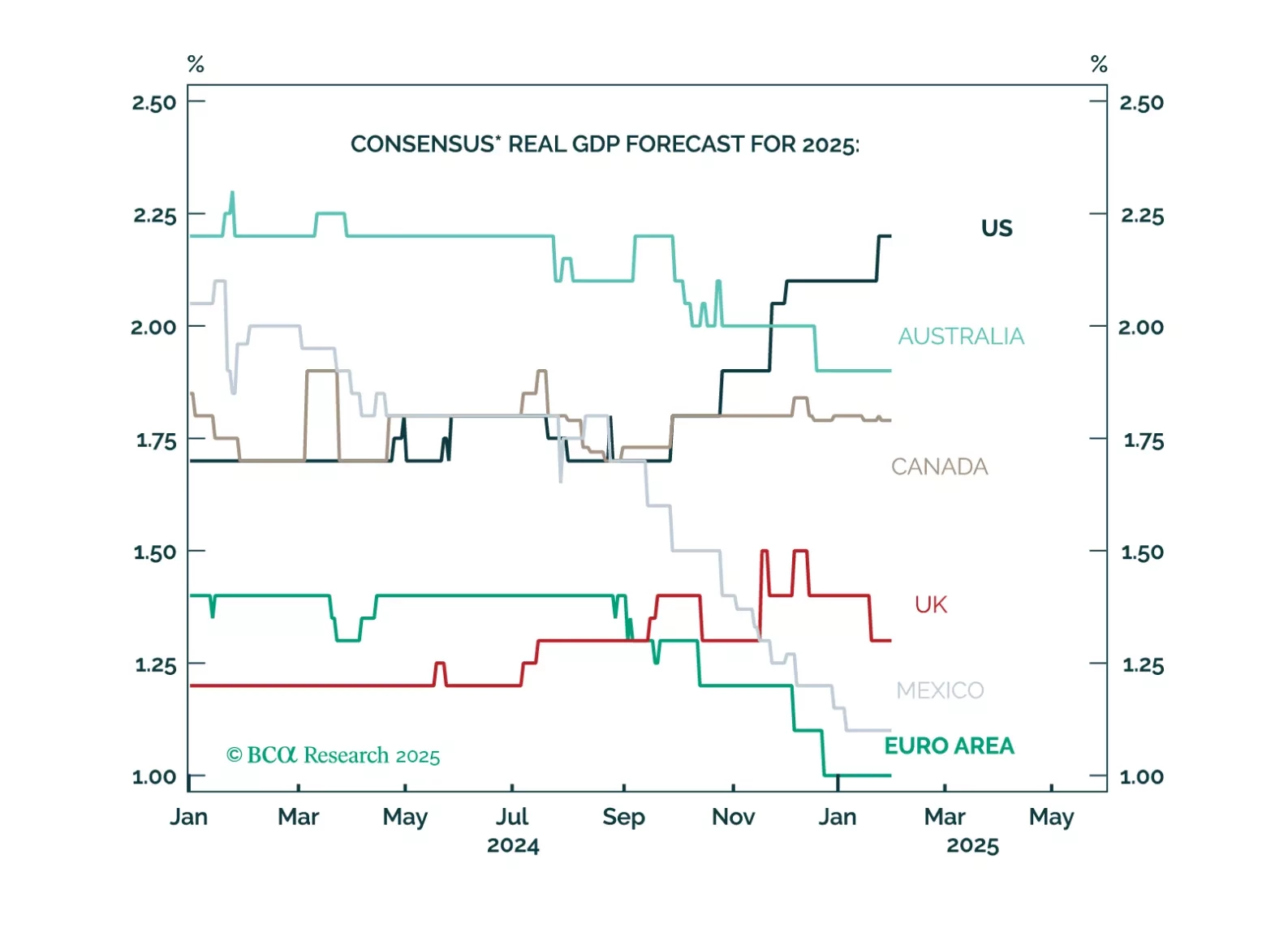

Economy

Markets and forecasters anticipate a “Golden Age” for Trump’s America, with US growth expectations soaring while the rest of the world lags. However, this extreme optimism means that there is a lot of room for disappointment. Cooling income growth, weak housing and less deficit spending than expected will result in US growth underperforming expectations. Maintain a modest underweight to equities and modest overweight to fixed income. US markets have become more expensive relative to the rest of the world even as quality differentials have stabilized. Prepare to downgrade US equities to underweight and to upgrade Euro Area and China to overweight. We will wait to pull the trigger until we have more clarity on trade policy and when the dollar's momentum turns negative.

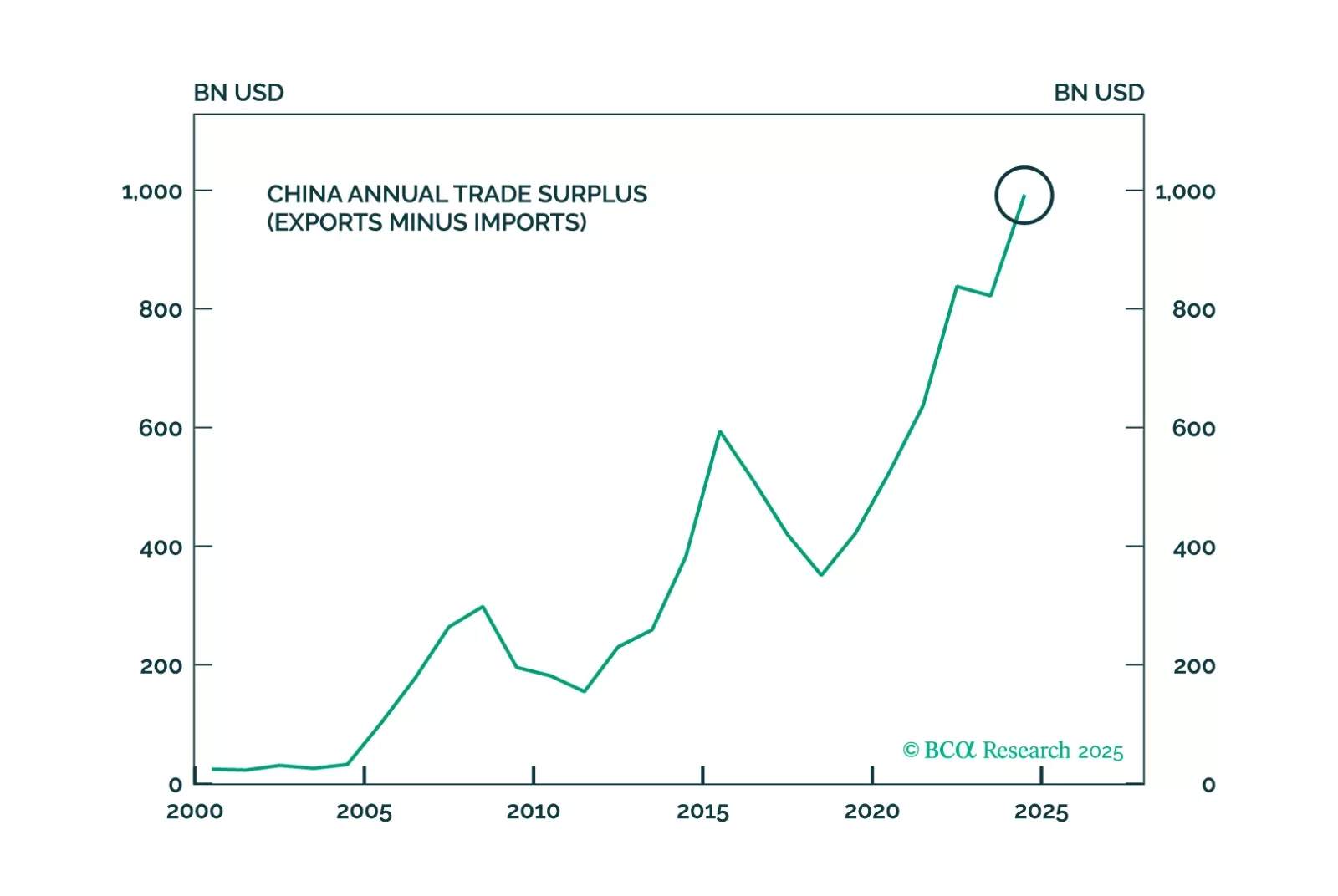

China barely hit its growth target in 2024 by shifting back to its old model of exports, racking up a record trade surplus with the world – right as Donald Trump walks back into the White House. Tariffs will elicit larger fiscal stimulus even as China rolls out innovations such as DeepSeek to meet its 2025 industrial goals, creating a volatile mix this year.

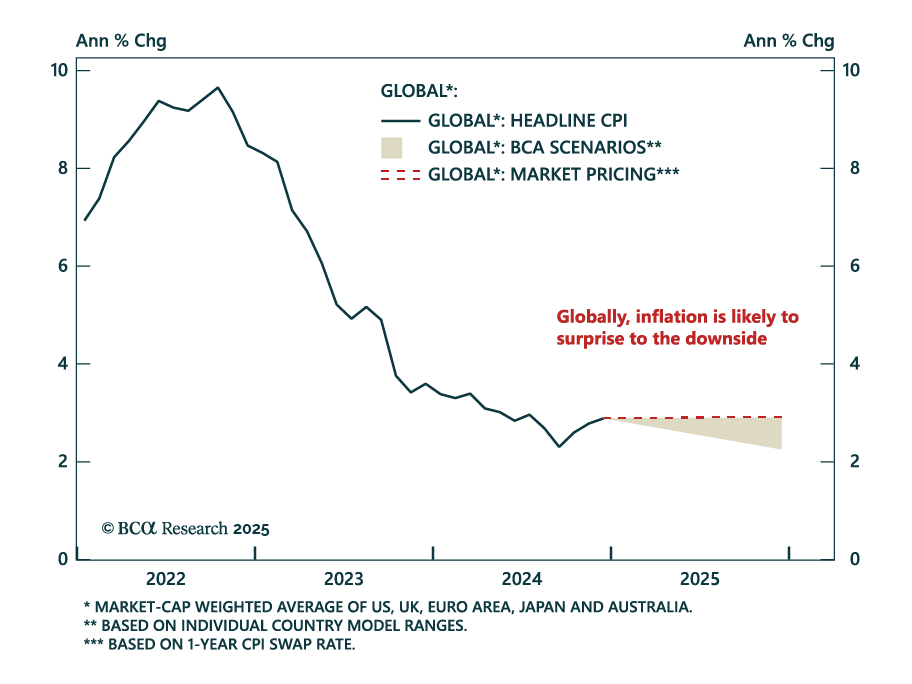

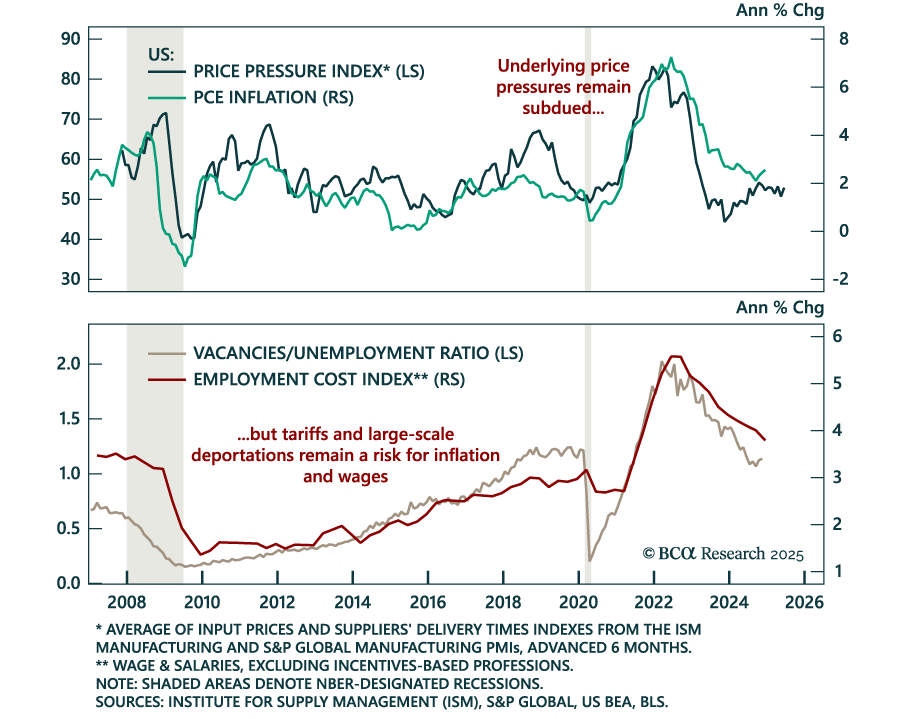

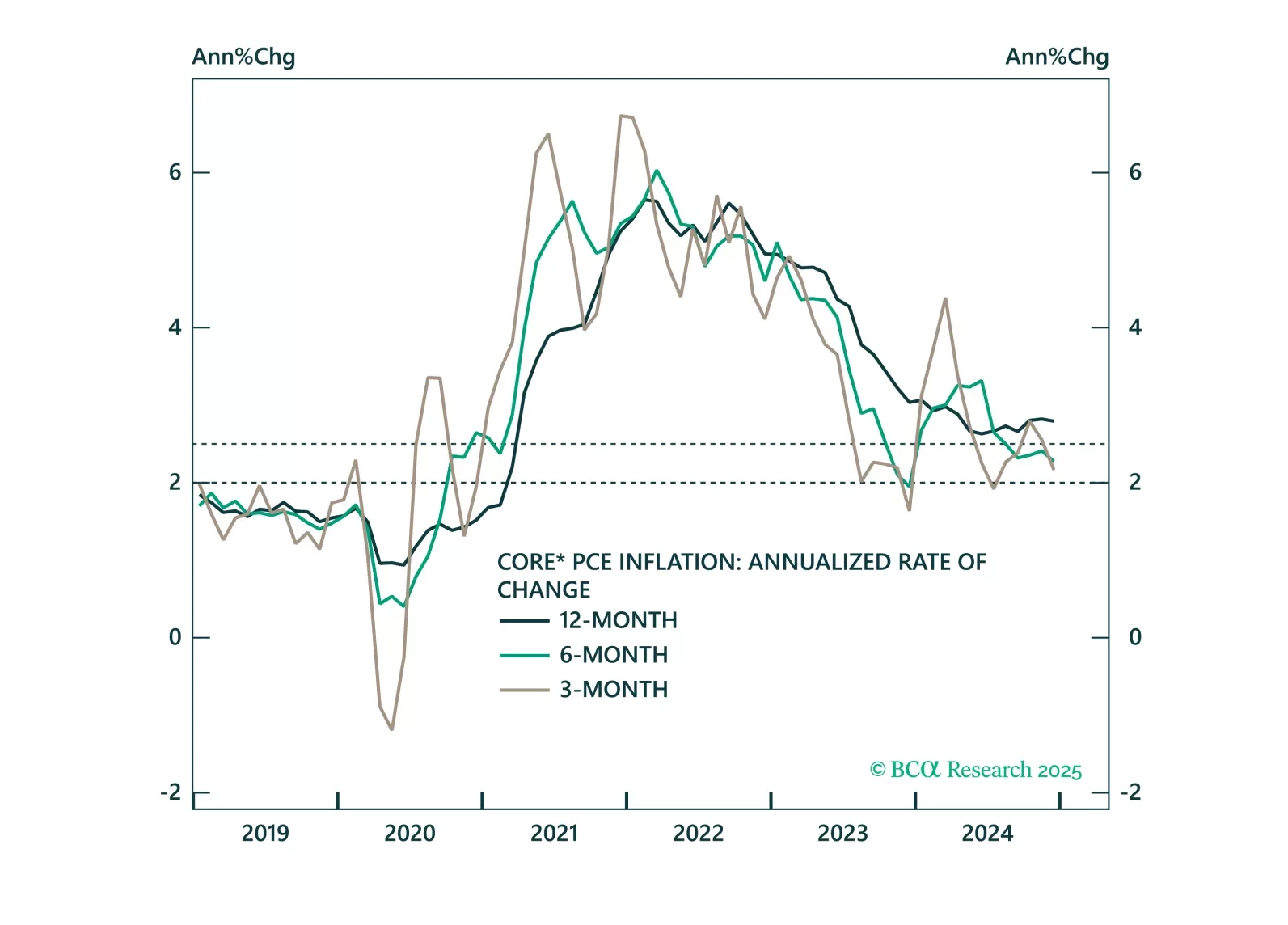

Core PCE inflation came in soft this morning and is tracking well below the Fed’s 2025 forecast. We highlight three upside risks to inflation and preview next week’s employment report.

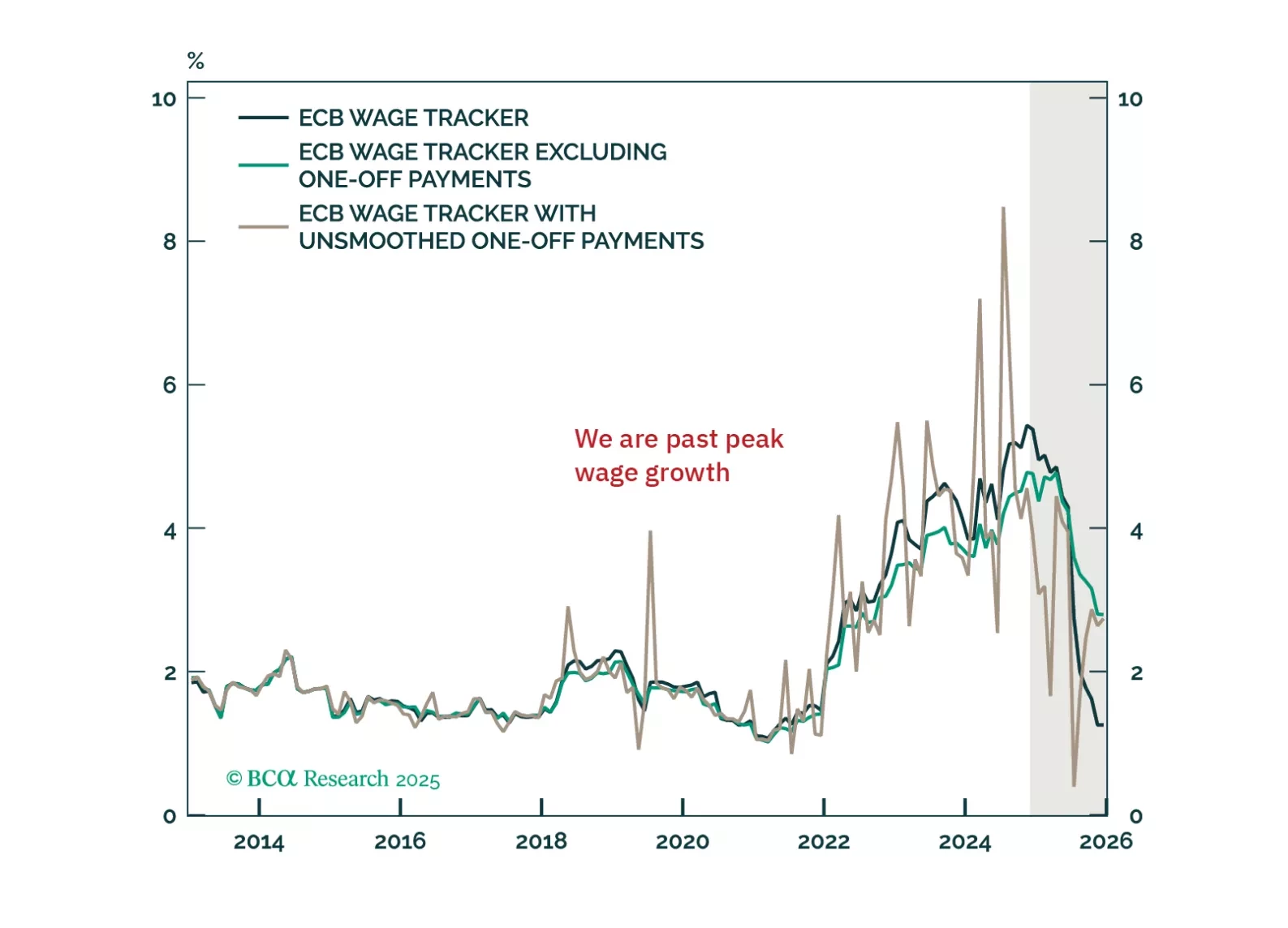

The ECB cut its deposit rate to 2.75%, as was widely anticipated. President Christine Lagarde did not provide any fireworks, but the Governing Council’s message was clear: Policy is restrictive, and inflation will fall further. As a result, if we combine our economic forecasts for the Eurozone with Frankfurt’s data dependency, we continue to expect the ECB’s deposit rate to settle below 2%. Consequently, German bond yields have downside, and the euro has yet to bottomed.

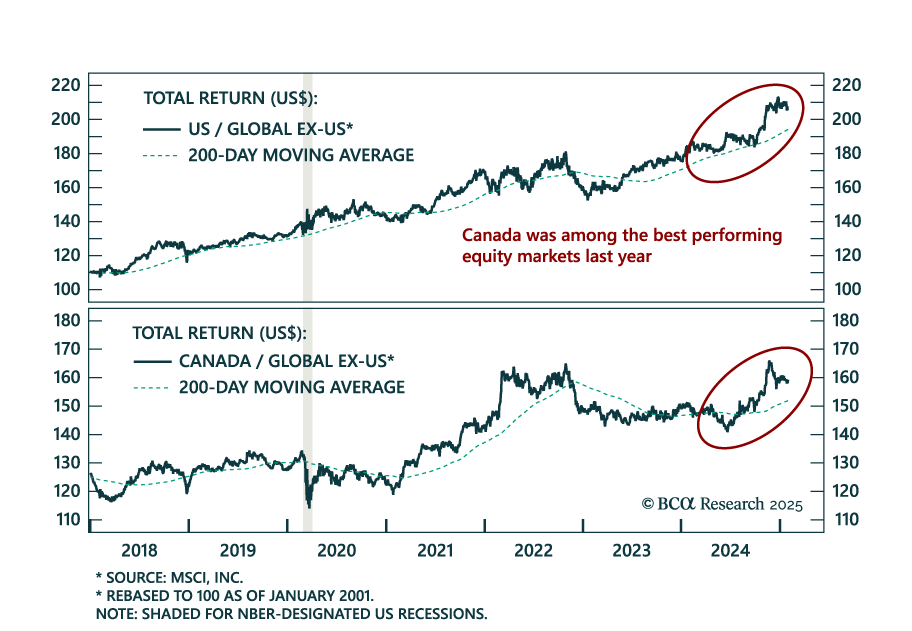

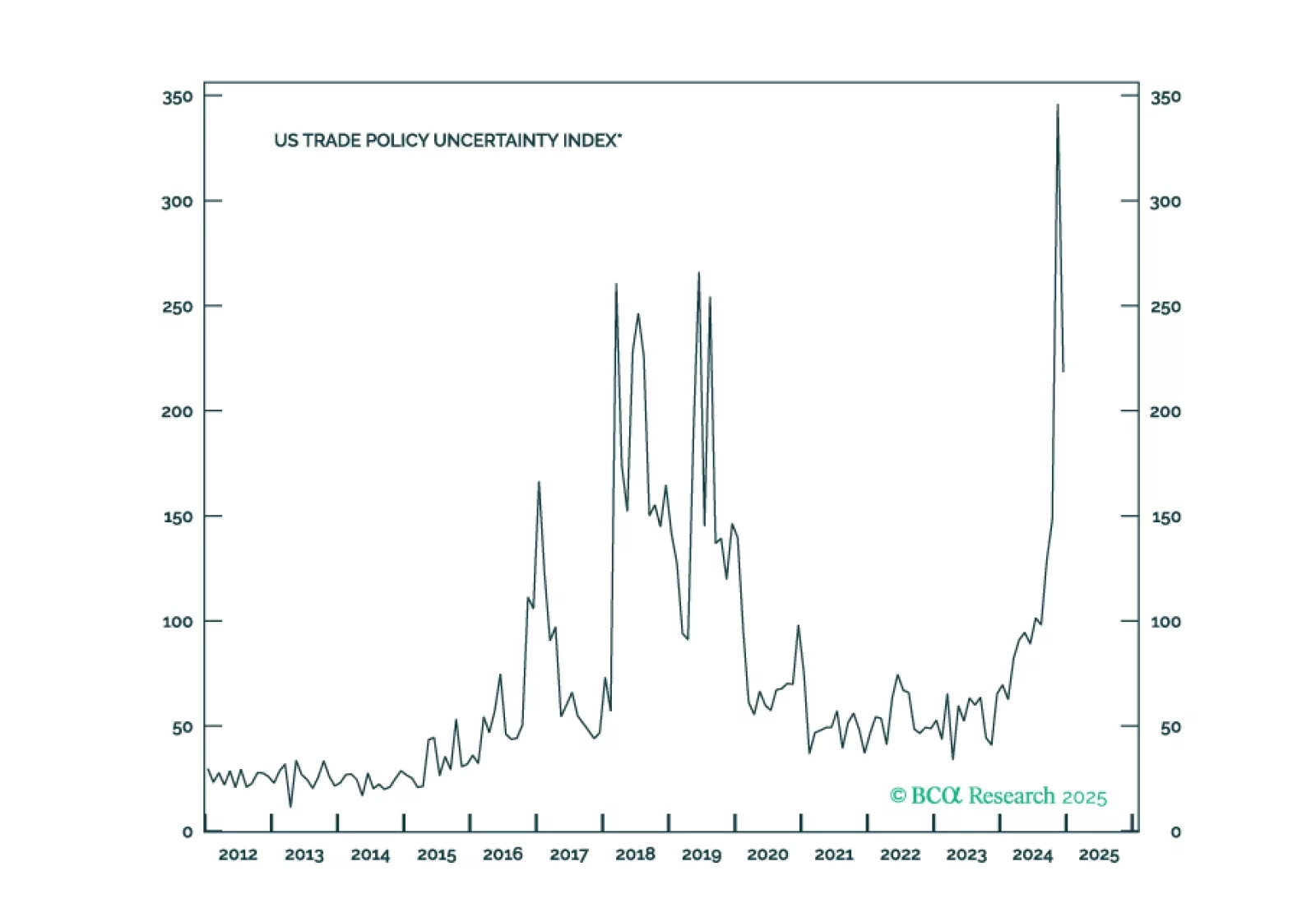

In Section I, Doug highlights that recent trade developments and news from the AI space are both consistent with a conservative investment stance. US final demand was robust in Q4, but the economy is still walking a tightrope as cracks in the labor market emerge. It is possible that an unorthodox set of policy prescriptions will cause US growth to inflect higher, but that is not yet our base case view. We recommend downgrading global growth stocks to underweight versus value. In Section II, Jonathan provides an update on Canada following strong performance from Canadian stocks last year. On a tactical basis, underweight Canada versus global ex-US on the expectation of tariffs targeting Canada and Mexico. Following a sell off, or if a trade war is avoided, investors should place Canadian stocks on upgrade watch with the goal of moving to a modest overweight versus global ex-US.