Energy

Stay overweight US equities versus world, long US energy sector versus Middle East stocks, and long Canada and Mexico versus global-ex-US stocks.

Fears of a hard landing are abating as growth has been surprising to the upside. New worries are emerging, such as the trajectory of disinflation, and the pace and timing of rate cuts. In this environment, it is important to build a resilient all-weather portfolio, which protects against a correction, rising rates, or stubborn inflation but also has exposure to the AI theme.

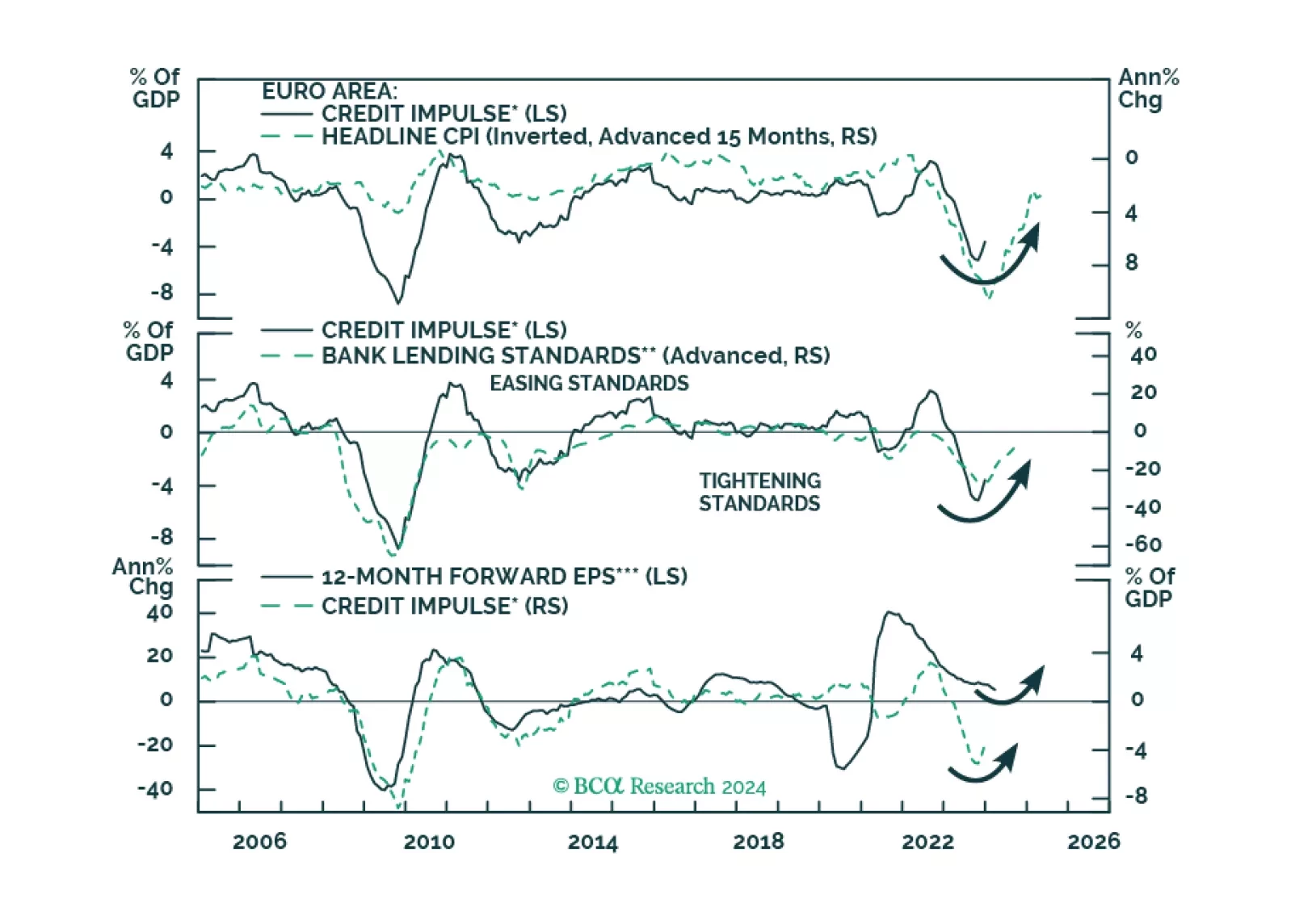

Europe credit flows are stabilizing, hence a major drag on the region’s growth will dissipate. What does this development imply for European equities?

In this Strategy Outlook we examine why, contrary to popular perception, the odds of a global recession over the next 12 months are rising not falling.

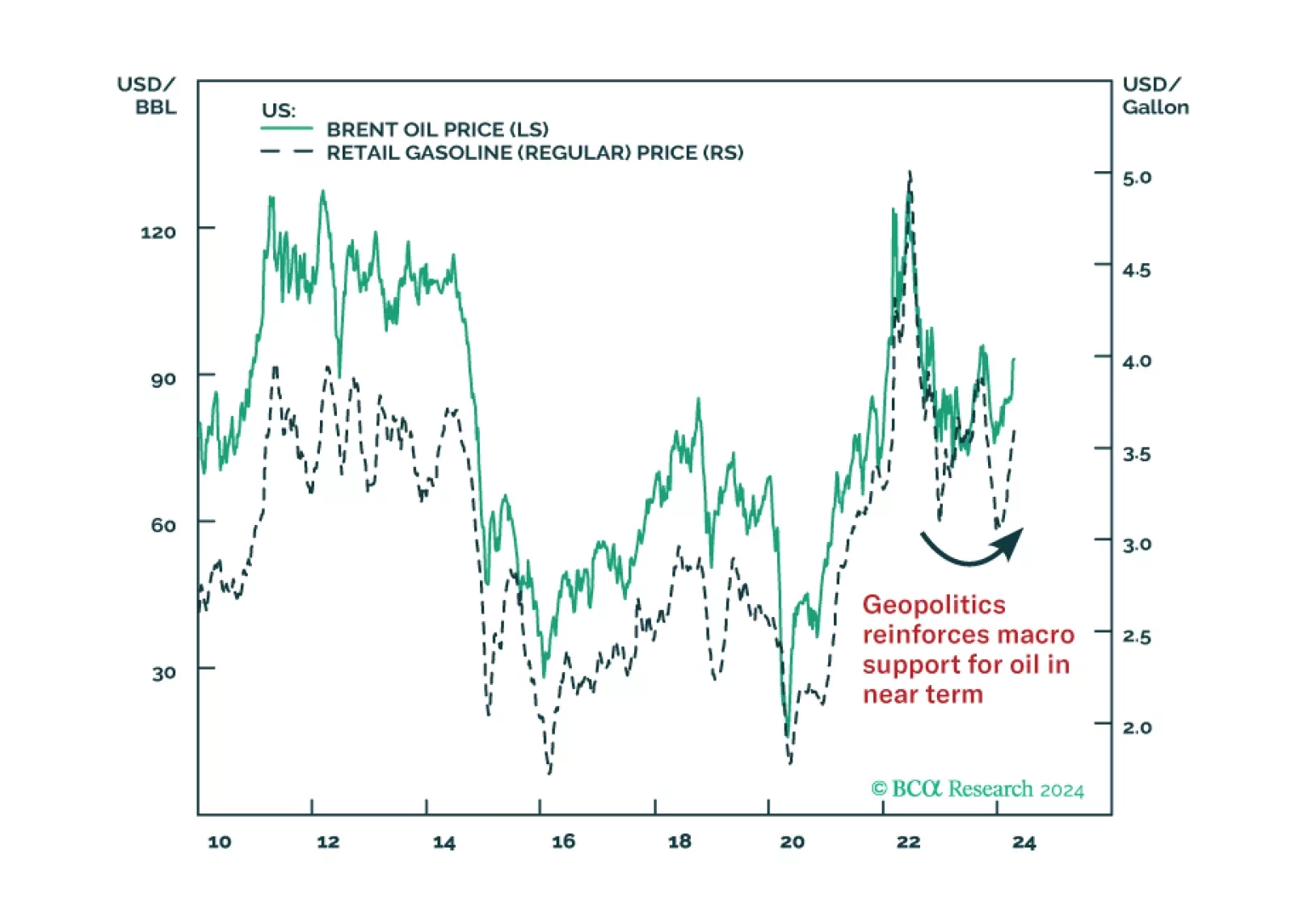

We expect oil-demand growth to increase this year – to 1.7mm b/d from 1.4mm b/d (0.30% of total demand) – and anticipate tighter supply at the margin. Our balances estimates are unchanged, leaving our Brent price forecasts for 2024 and ’25 at $95/bbl and $105/bbl. We expect the US to deploy warships if Venezuela makes a move on Guyanese territory in a bid to grab deep-water oil production.