Financial Markets

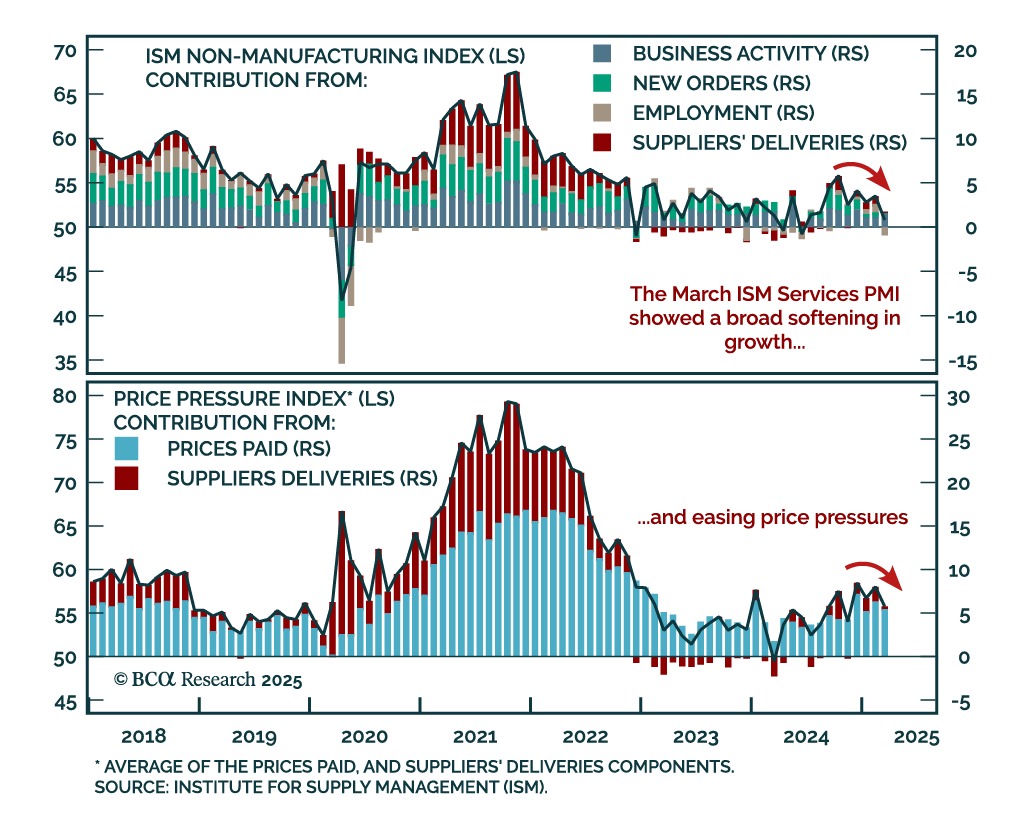

The March ISM Services report sent a recessionary signal, supporting our defensive positioning. The headline index fell sharply to 50.8 from 53.5, missing expectations. New orders dropped to 50.2, while employment collapsed to 46.2 from 53.9. Prices paid also…

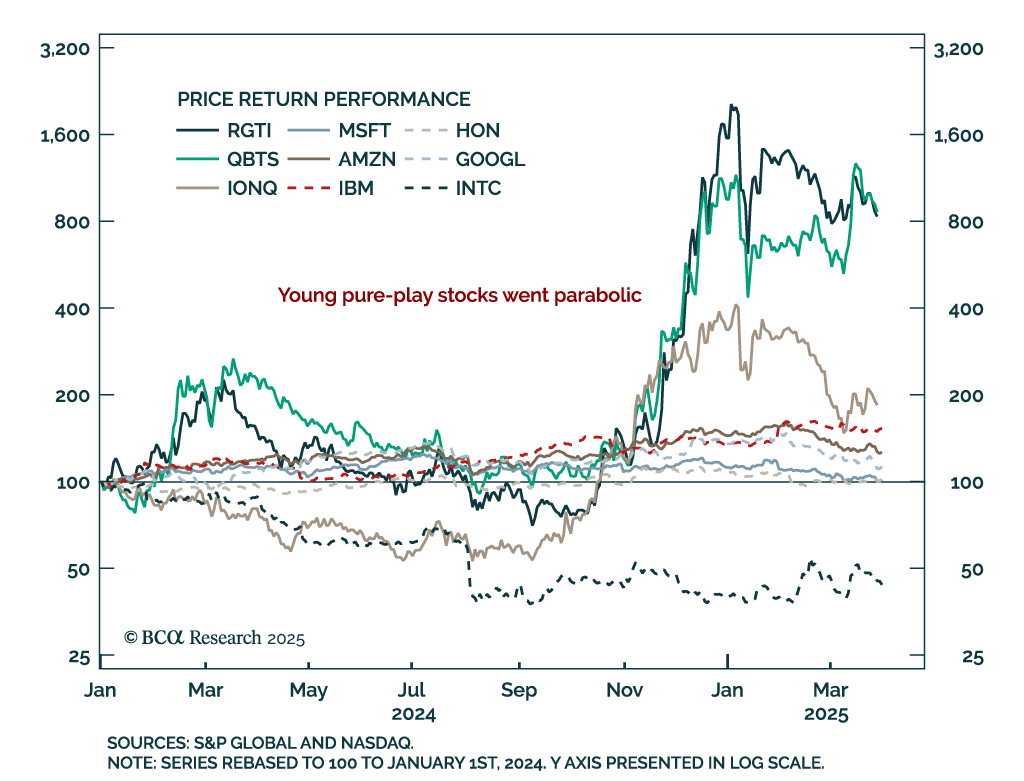

Our US Equity strategists recommend caution on quantum computing, as the industry is still too early-stage for reliable investment exposure. Although quantum computing (QC) is on the verge of major breakthroughs, pure-play QC stocks remain unprofitable and…

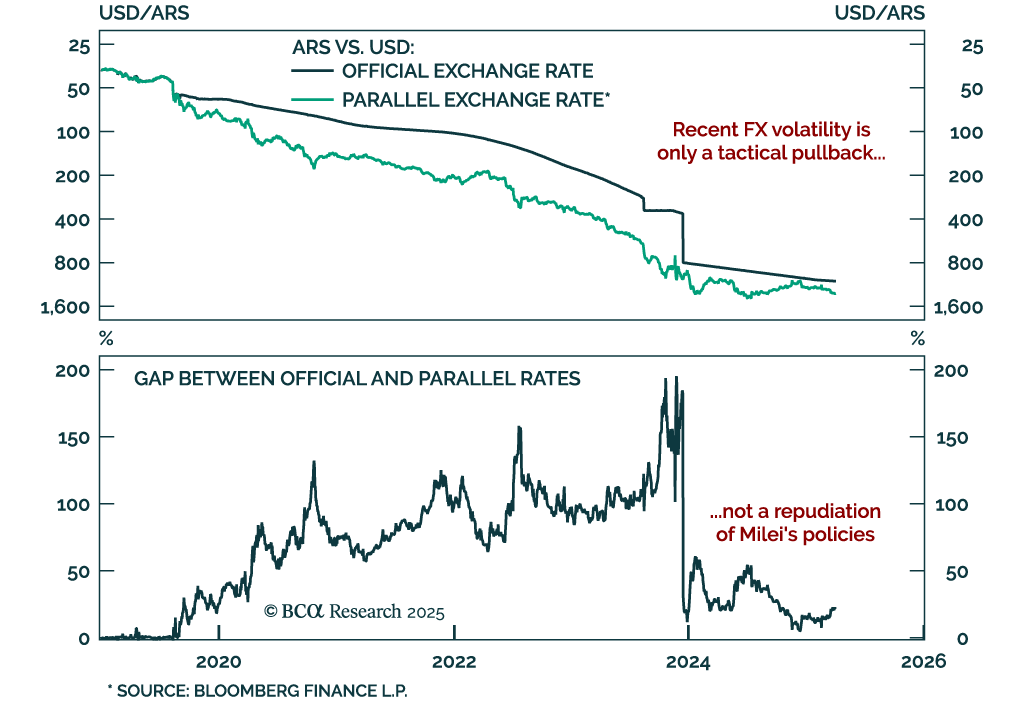

Remain constructive on Argentine assets as recent market moves are a tactical pullback, not a loss of confidence. The gap between official and parallel exchange rates has widened, prompting concerns that markets are questioning President Milei’s liberalizing…

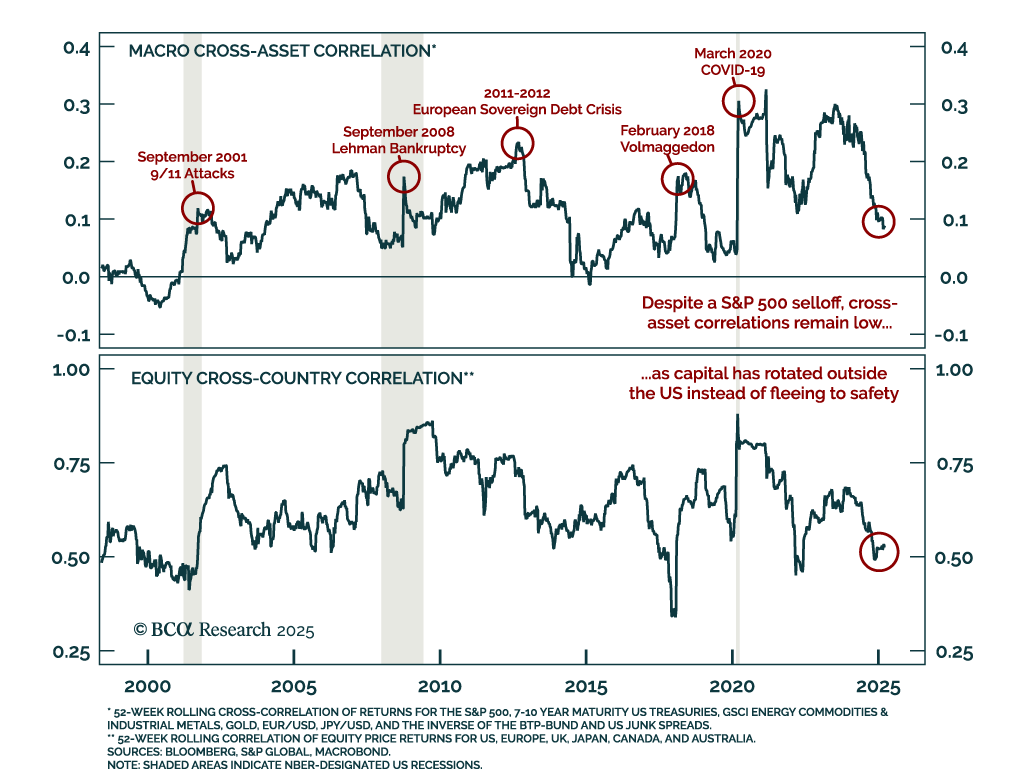

Low correlations and regional dispersion are shaping market dynamics, creating selective opportunities outside the US even as near-term risks remain. Asset classes tend to become highly correlated during crisis episodes, limiting diversification when it is…

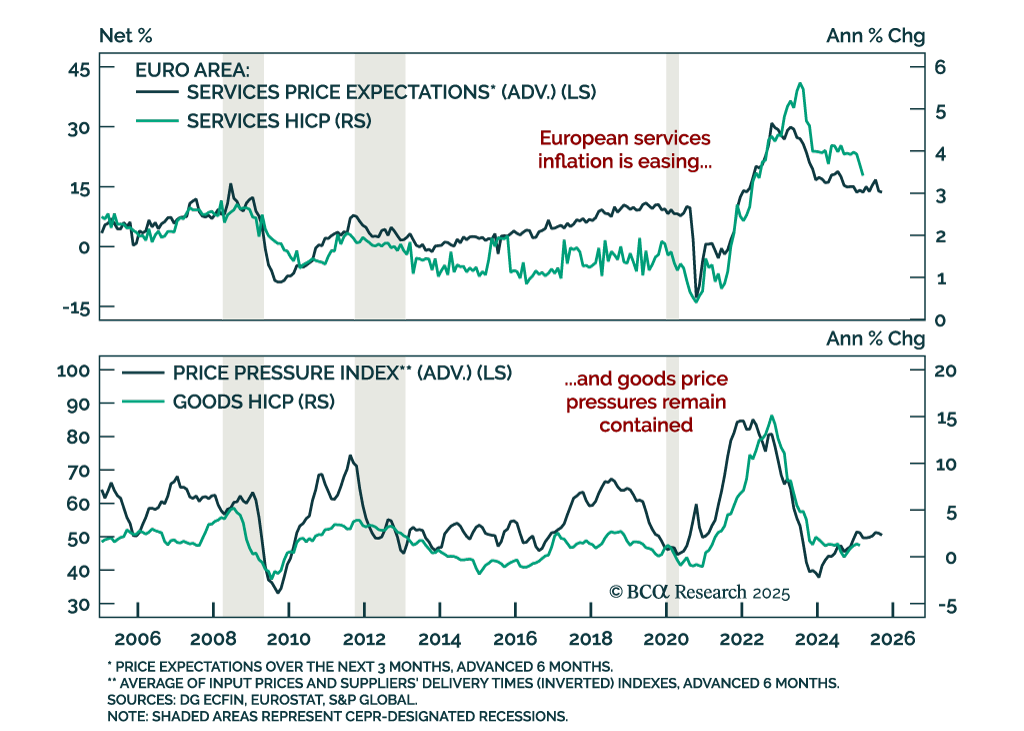

Eurozone inflation is cooling steadily, supporting our tactical overweight in German bunds versus European equities and increasing the odds of an April ECB cut. Headline HICP eased to 2.2% y/y in March from 2.3%, while core came in cooler than expected at…

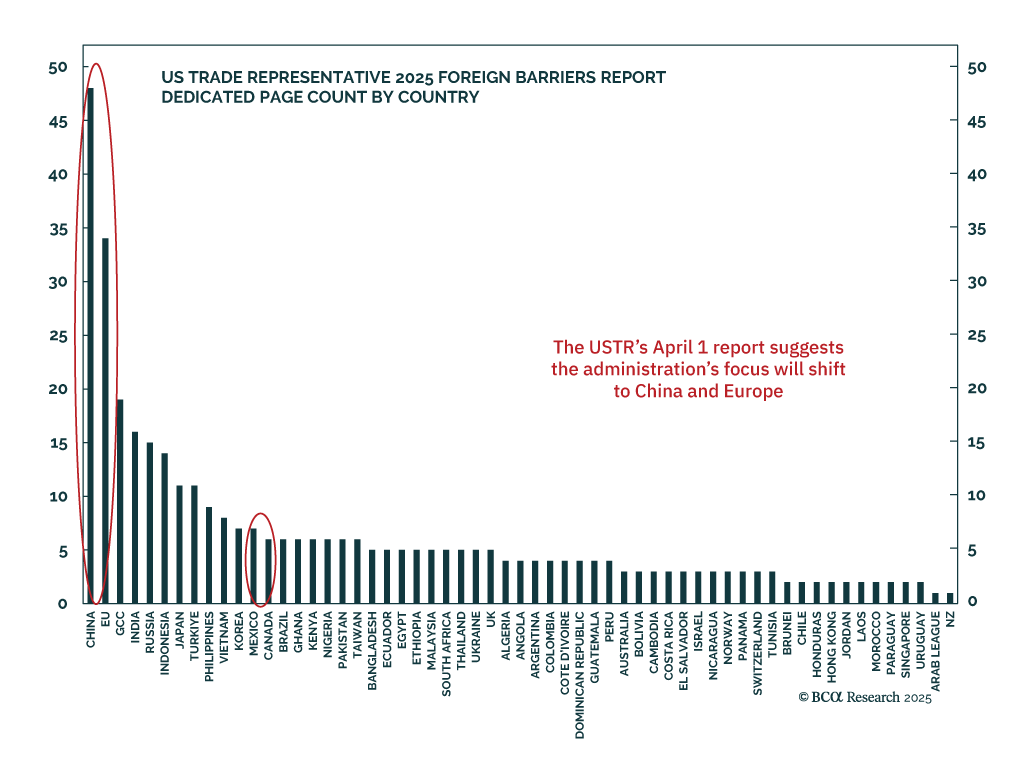

April 2 may mark peak trade tensions, but the path forward remains highly uncertain, supporting our underweight on risk assets and industrial commodities. The USTR’s long-awaited report on trade barriers will guide the next phase of US trade policy. While the…

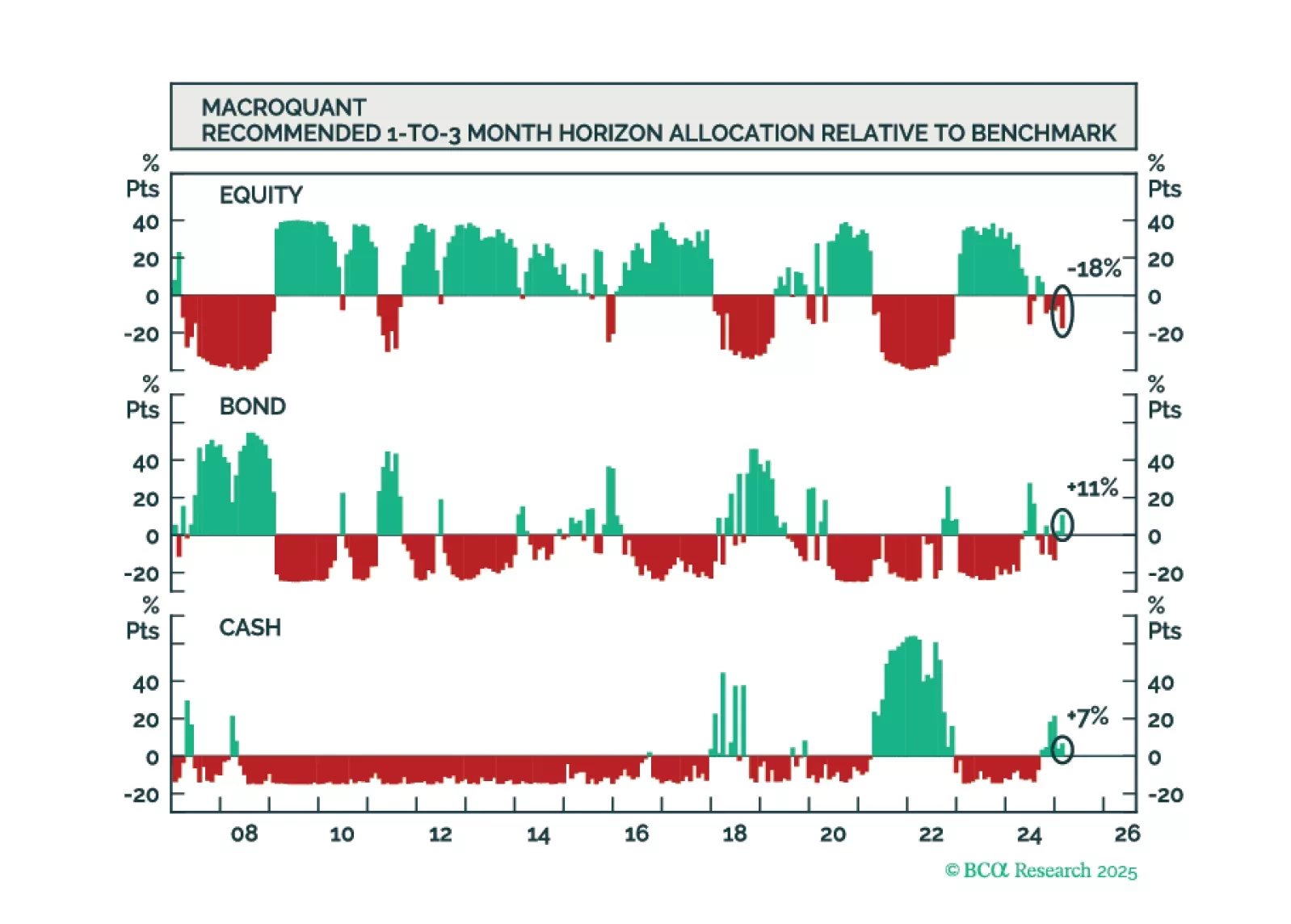

Going into April, MacroQuant recommends a modest underweight on stocks, offset by an overweight on bonds and cash. While MacroQuant is modestly bearish on stocks, we suspect that the downside risks to equities may be greater than what the model assumes.

Going into April, MacroQuant recommends a modest underweight on stocks, offset by an overweight on bonds and cash. While MacroQuant is modestly bearish on stocks, we suspect that the downside risks to equities may be greater than what the model assumes.

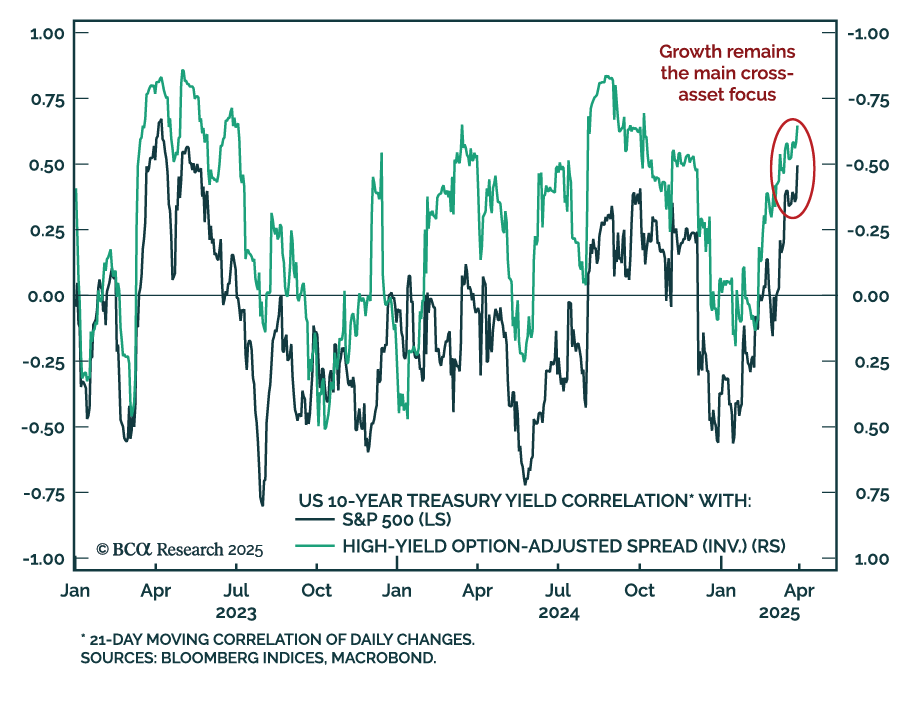

Markets are responding to the growth drag of stagflation, not the inflation impulse, reinforcing our defensive stance. Despite rising short-term inflation pressures in the US, risk assets and bond yields continue to move together, with the stock–bond yield…

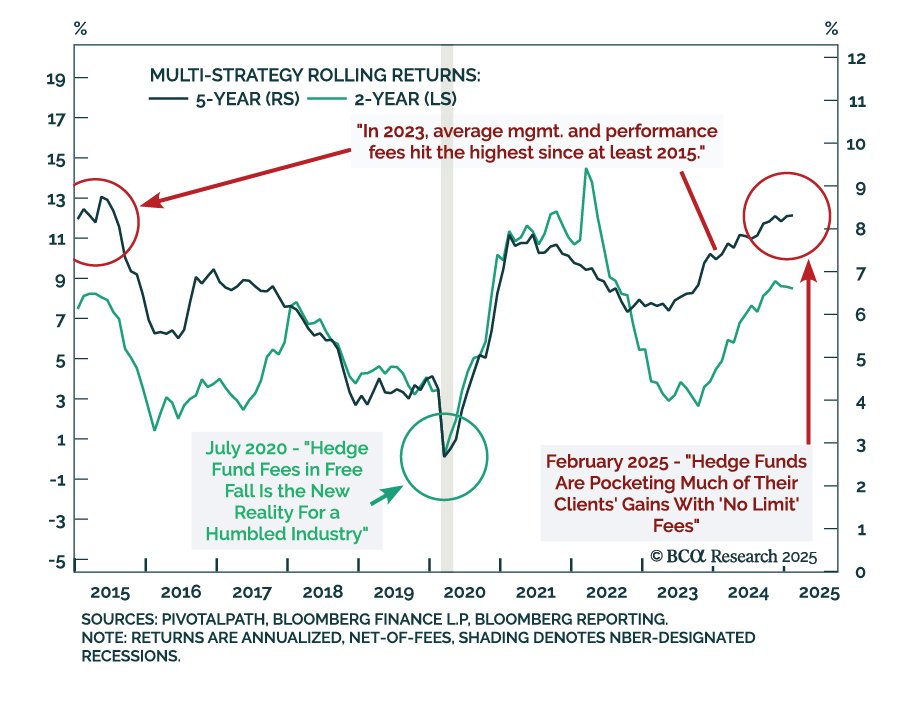

Our Private Markets & Alternatives strategists remain structurally positive but cyclically underweight on Multi-Strategy Hedge Funds. While these funds have delivered consistent alpha and valuable diversification, current market conditions offer more…