Financial Markets

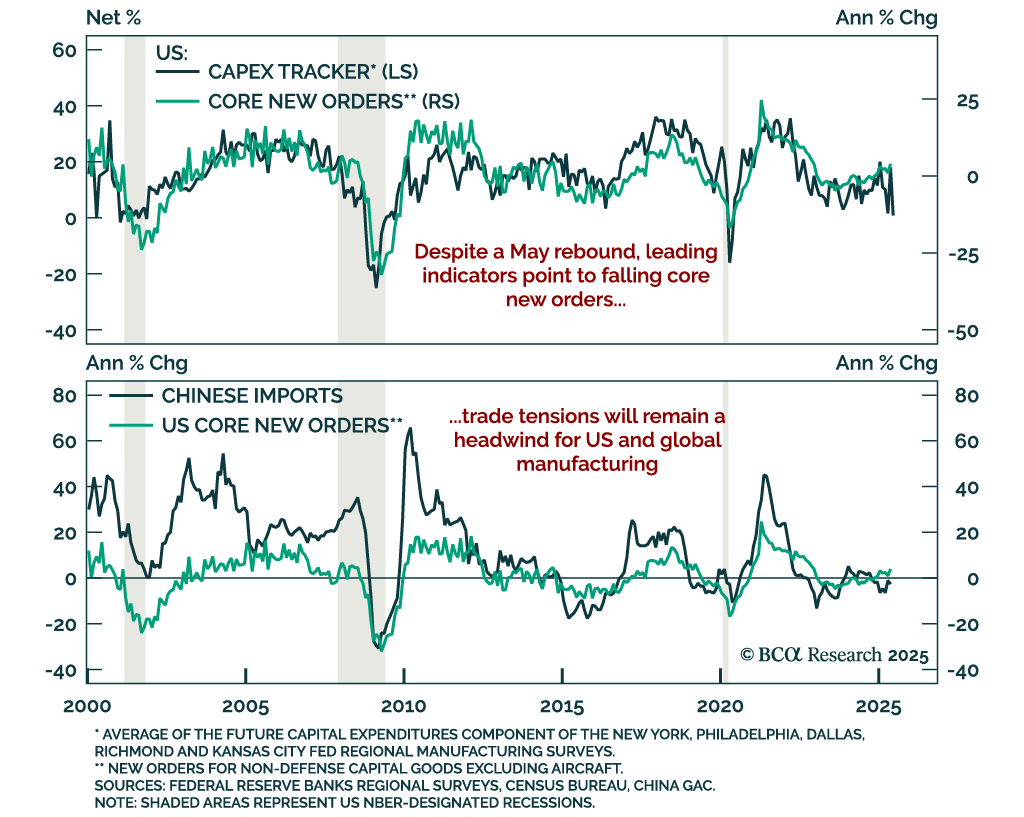

Headline strength in US capital goods orders is unlikely to last, reinforcing our defensive stance and preference for steepeners. New orders for core capital goods (nondefense ex-aircraft) rose 1.7% m/m in May, beating expectations after a 1.5% drop in April.…

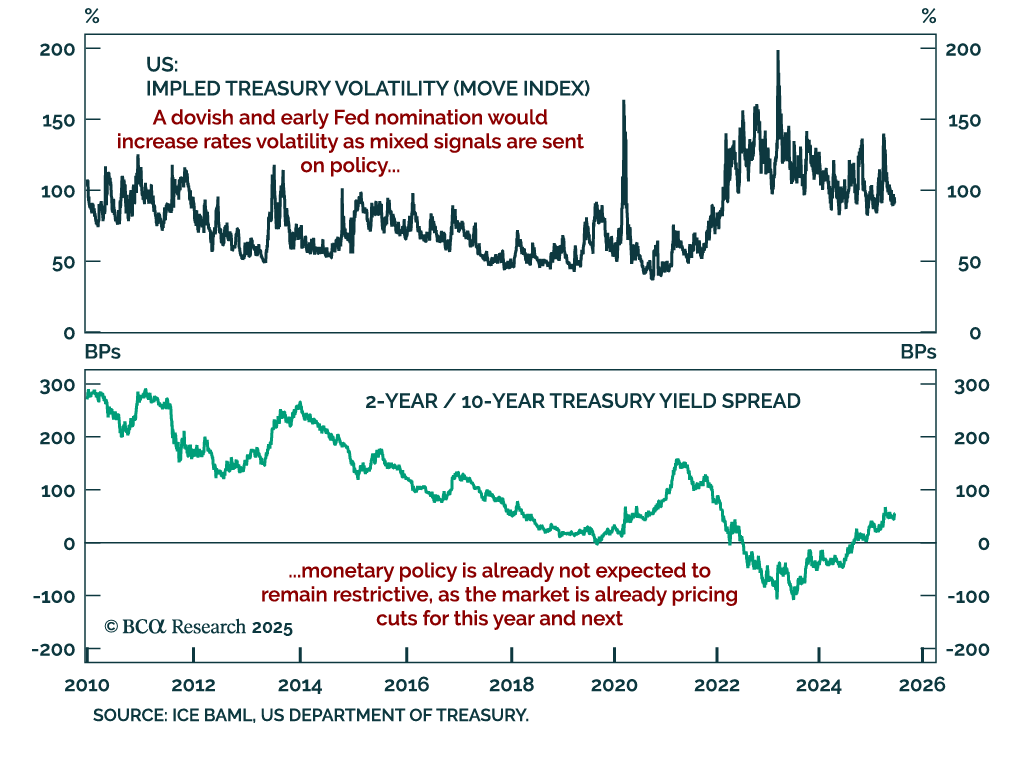

A dovish early Fed nominee would increase volatility in rates and FX as markets reassess the credibility of US monetary policy. News reports indicate the Trump administration is considering nominating a Fed successor ahead of the end of Chairman Powell’s…

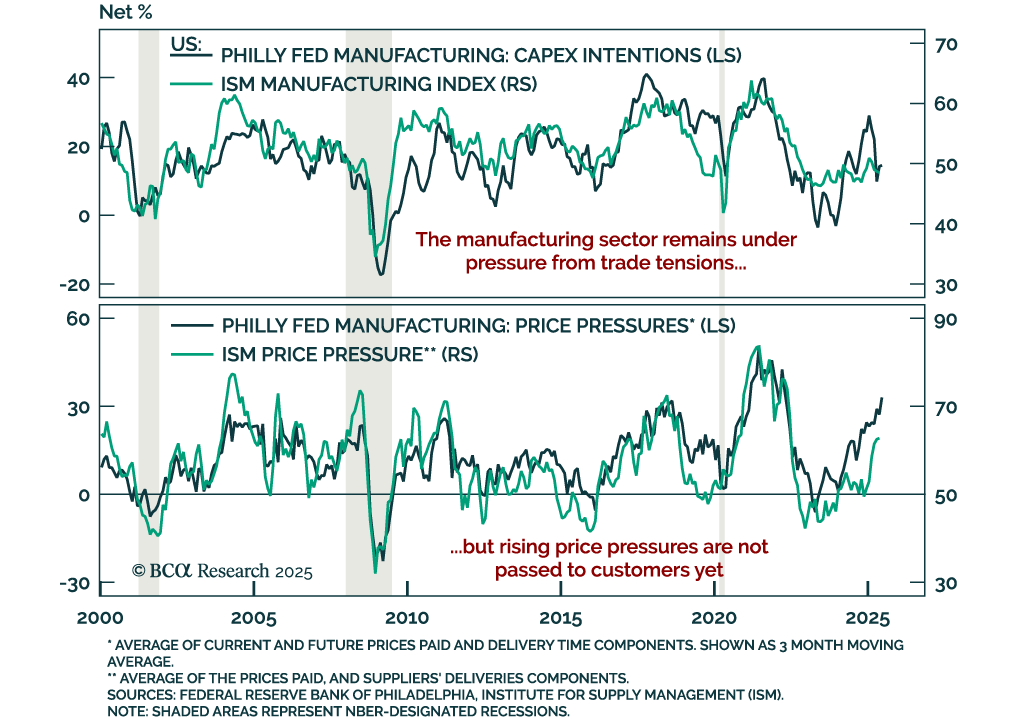

Worsening manufacturing momentum supports a long duration stance as recession risks remain elevated. The June Philly Fed survey came in below expectations, unchanged at -4.0. While shipments increased, new orders decelerated and employment measures fell.…

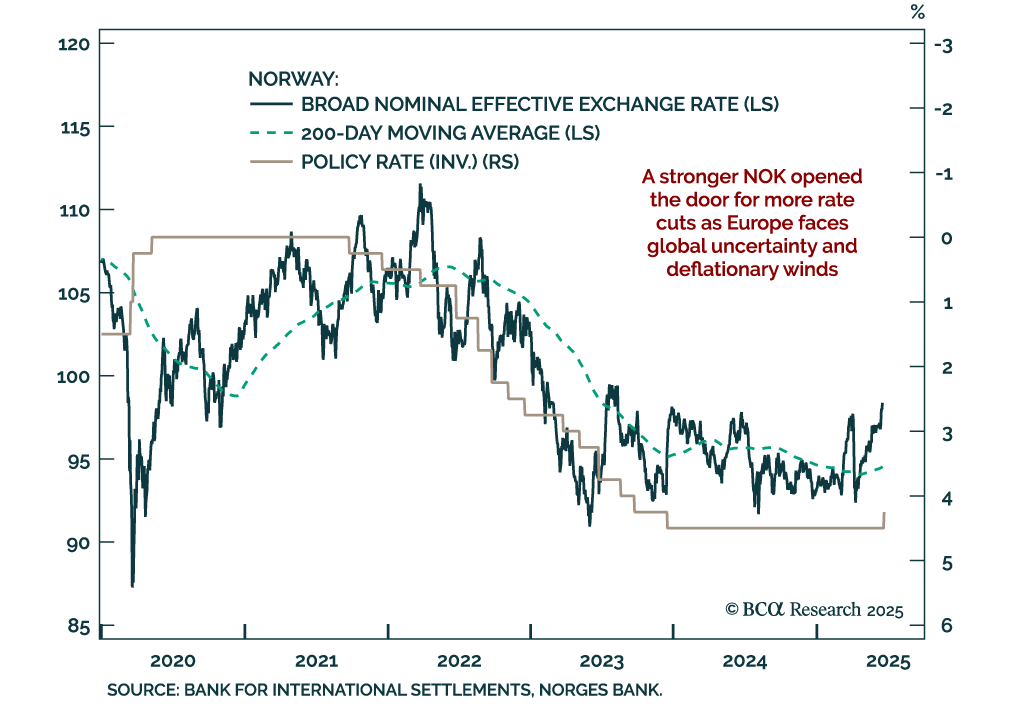

A stronger Norwegian krone has opened the door to more rate cuts, making Norwegian government bonds more attractive. Our Chart Of The Week comes from Jeremie Peloso, European Strategist. With its surprise 25 basis point cut, the Norges Bank made its first…

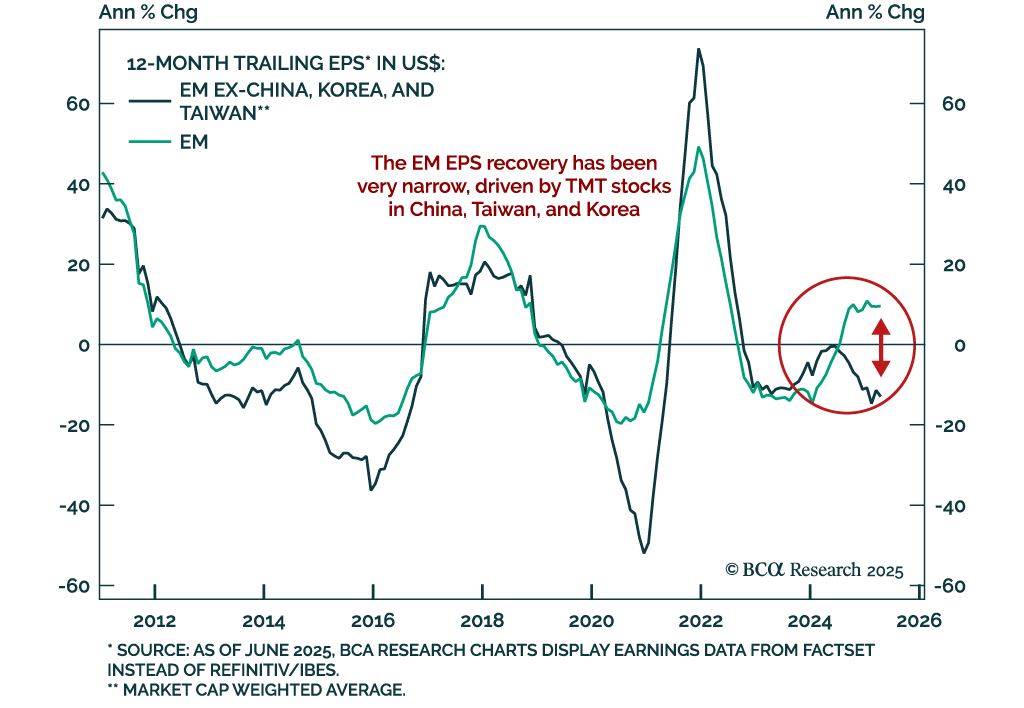

BCA’s EM strategists remain downbeat on EM equities despite a bearish US dollar view, citing profit headwinds and limited valuation support. The ongoing EM earnings recovery has been narrowly concentrated in TMT sectors across China, Taiwan, and Korea,…

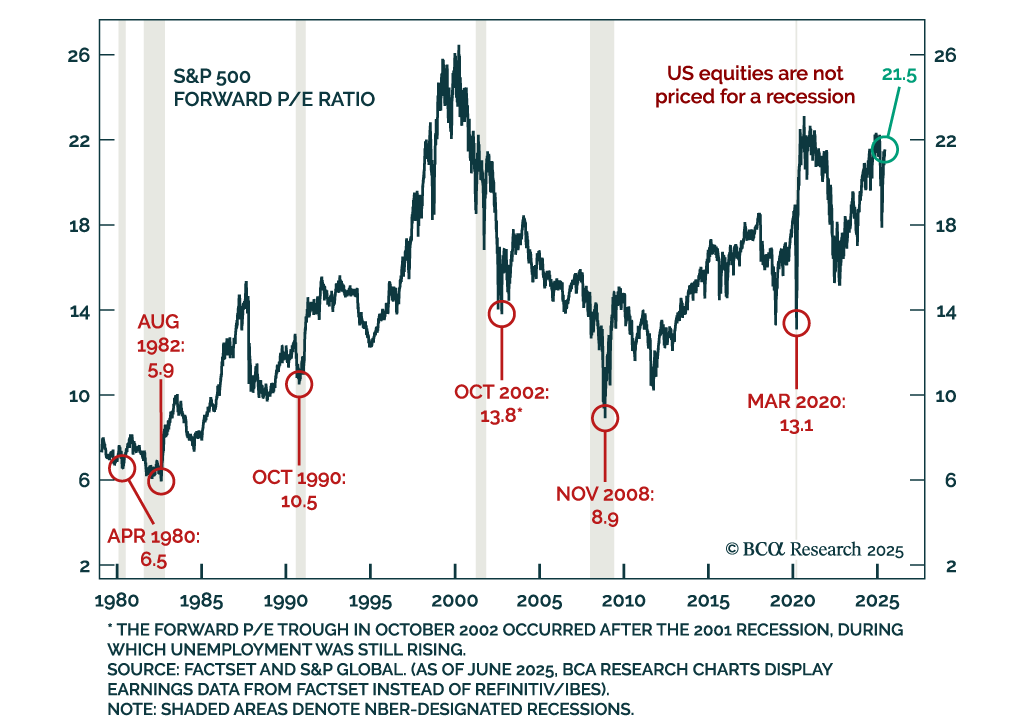

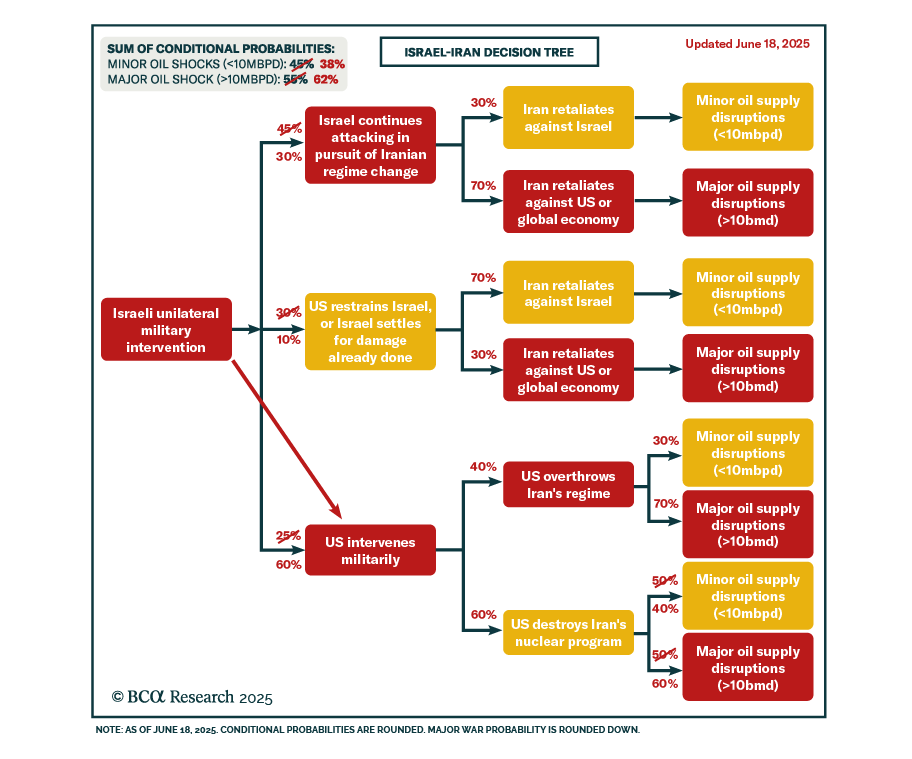

Geopolitical risks and fragile margins reinforce a defensive allocation stance, as oil shocks and high US equity valuations pose growing downside risks. At this month’s Views Meeting, our strategists discussed the potential fallout from an Iran-Israel…

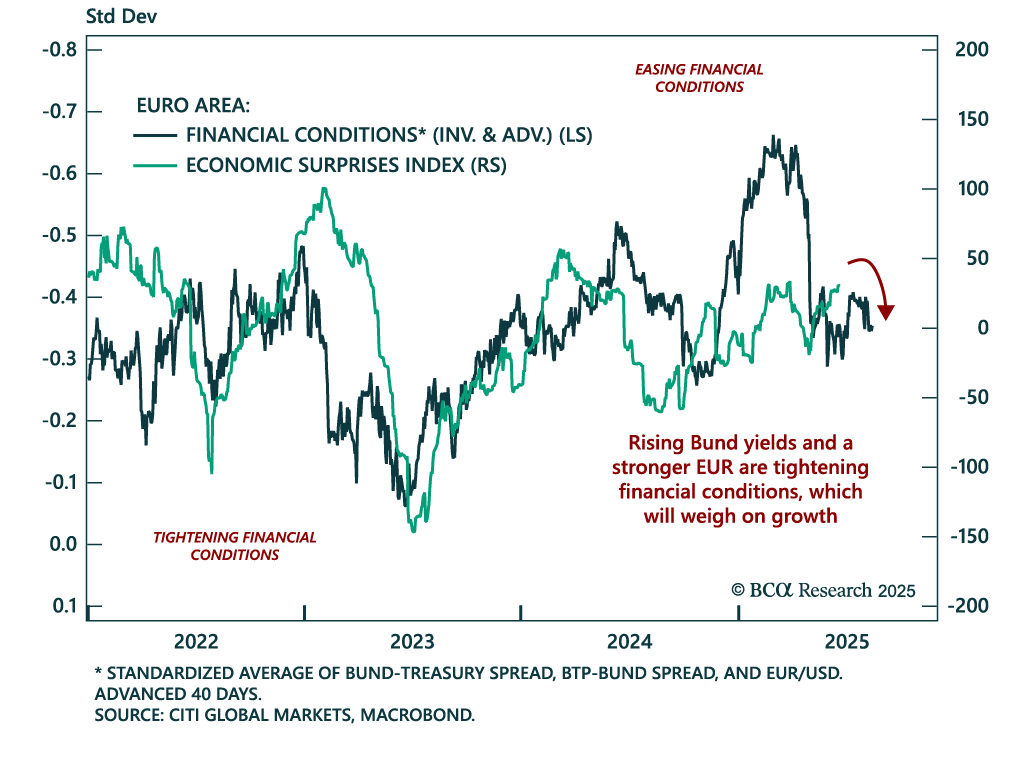

Tightening financial conditions, deflationary headwinds, and rising geopolitical risks argue for short-term caution on European assets. European equities have outperformed in 2025, with the EURO STOXX 50 beating the S&P 500 and EUR/USD moving higher. This…

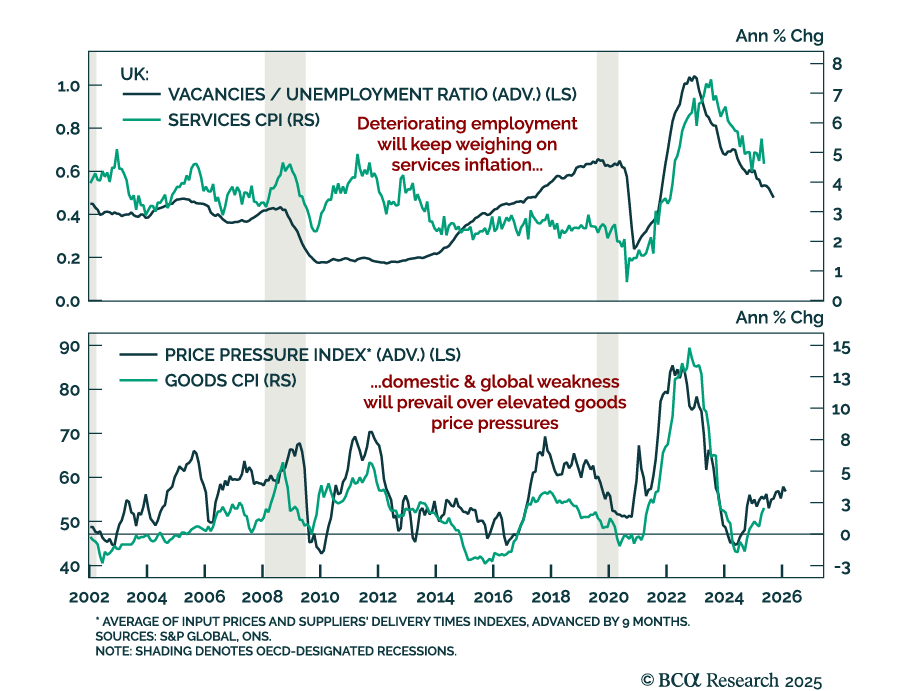

UK disinflation and labor market softening support our overweight in Gilts and short GBP trade. UK CPI came in slightly hotter than expected in May, with headline inflation at 3.4% y/y (vs. 3.5% in April) and core CPI meeting expectations at 3.5%, down from…

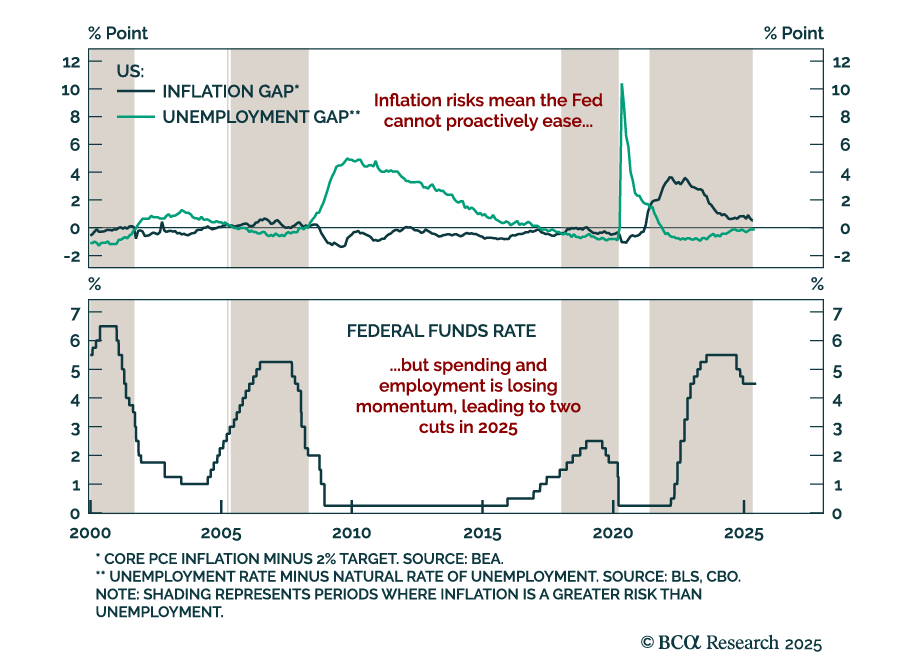

The Fed held rates steady between 4.25% to 4.5% and maintained a hawkish tilt despite soft data, reinforcing our long-duration and steepener trades. The updated dot plot showed upward revisions to both inflation and unemployment projections, as well as to…

Our Geopolitical strategists expect US involvement in Israel’s military campaign against Iran, raising near-term risks to oil supply and market stability. Iran is likely to retaliate by targeting regional oil production and transport infrastructure,…