Fixed Income

This Special Report introduces a framework for assessing the relative importance of slope change and initial yield in curve trade performance. The yield penalty for curve steepeners has fallen significantly since the beginning of the year, and we recommend shifting out of Treasury curve flatteners and into Treasury curve steepeners in US bond portfolios.

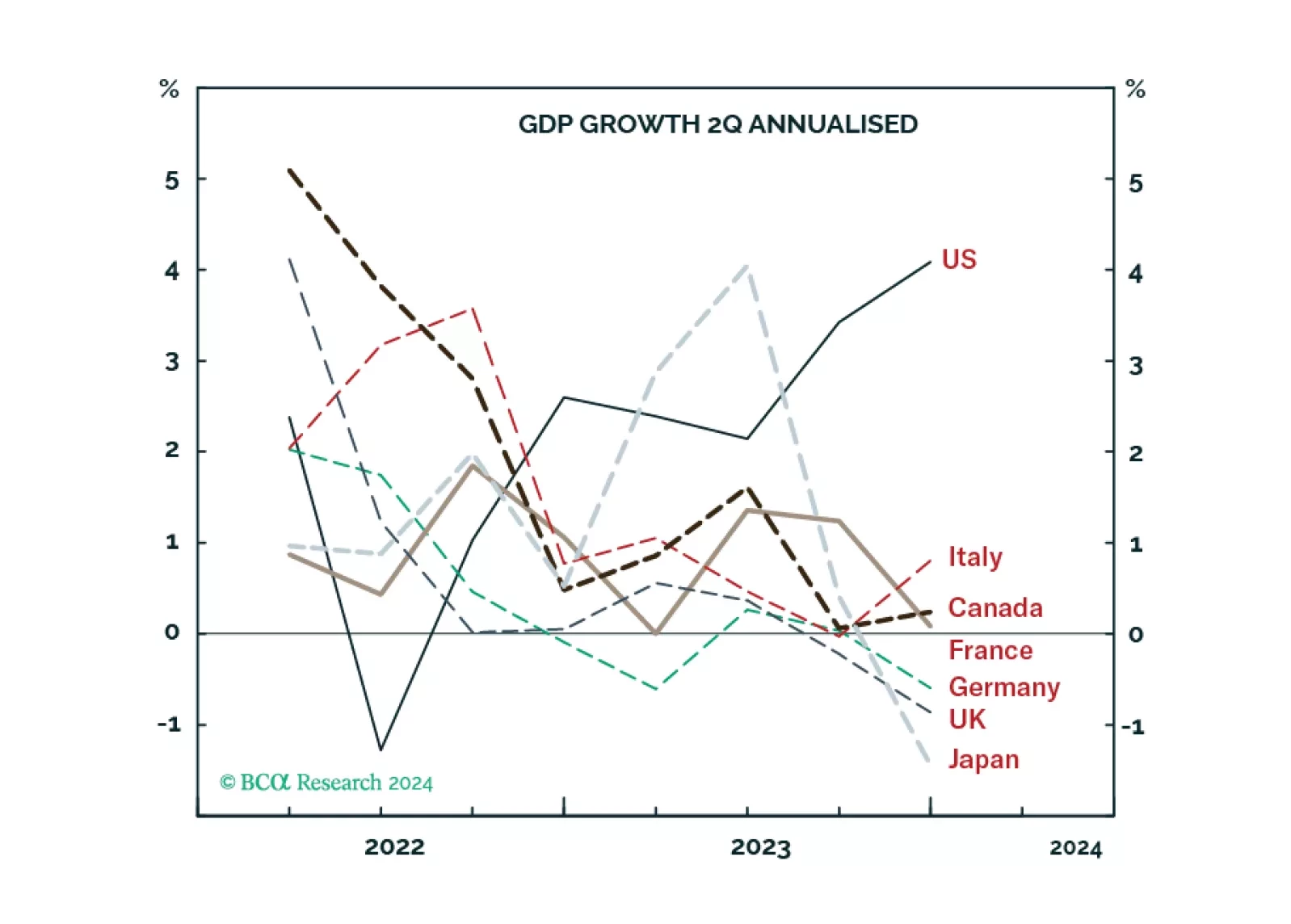

Unlike most advanced economies that are flirting with recession due to weak demand, the ‘inverted’ US economy is motoring along due to strong supply, from a combination of surging labour participation and surging immigration. We go through the implications for stocks, bonds, interest rates, and the dollar. Plus: IXJ, PEP, and MCD are good tactical outperformance candidates.

In the short run, global risk assets are vulnerable due to rising oil prices and bond yields. Cyclically, a global economic downturn will weigh on global risk assets.

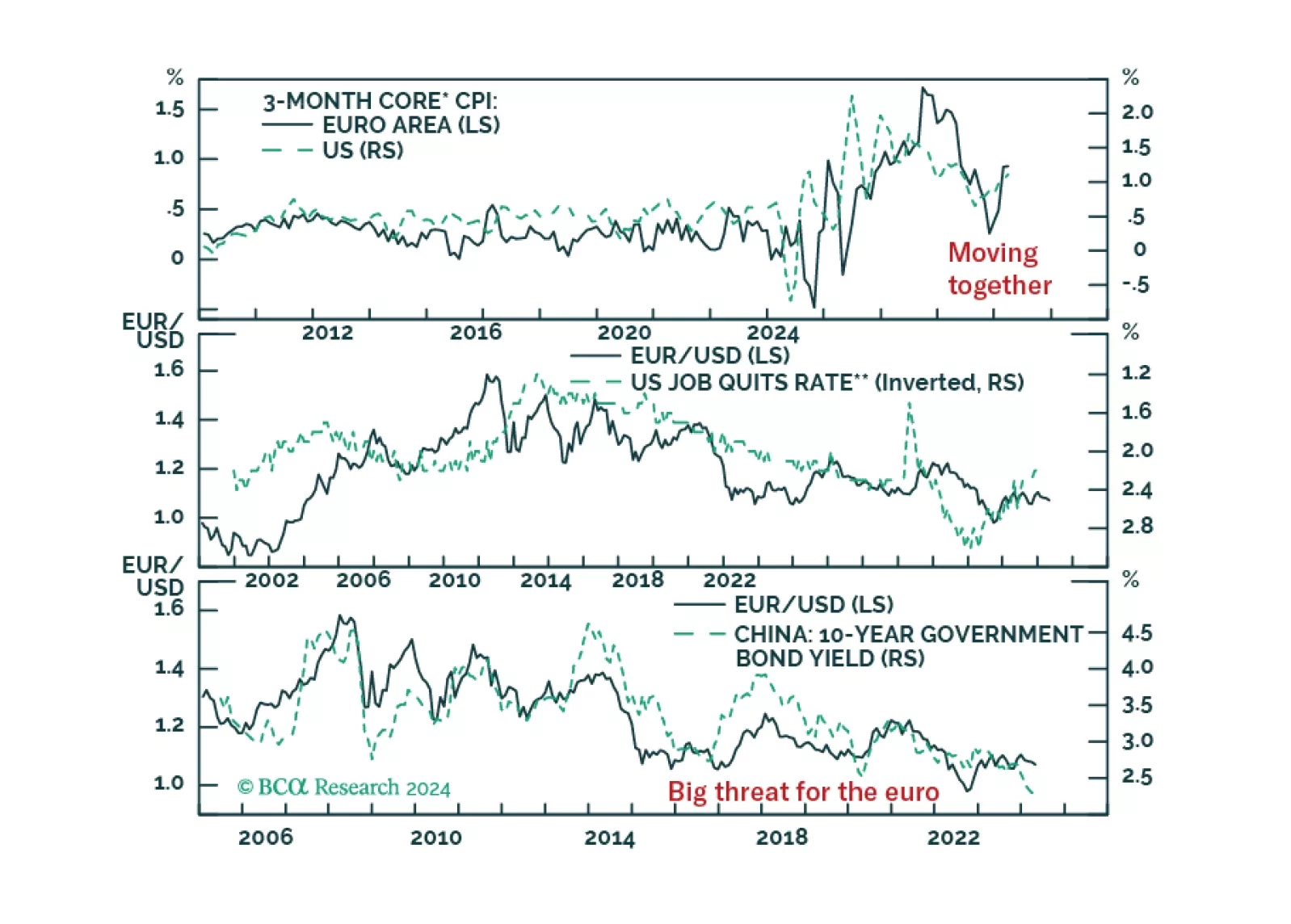

EUR/USD collapsed in the wake of last week’s hotter-than-expected US CPI report. Is this pessimism warranted and will the euro’s trading range that has prevailed since 2023 breakdown?

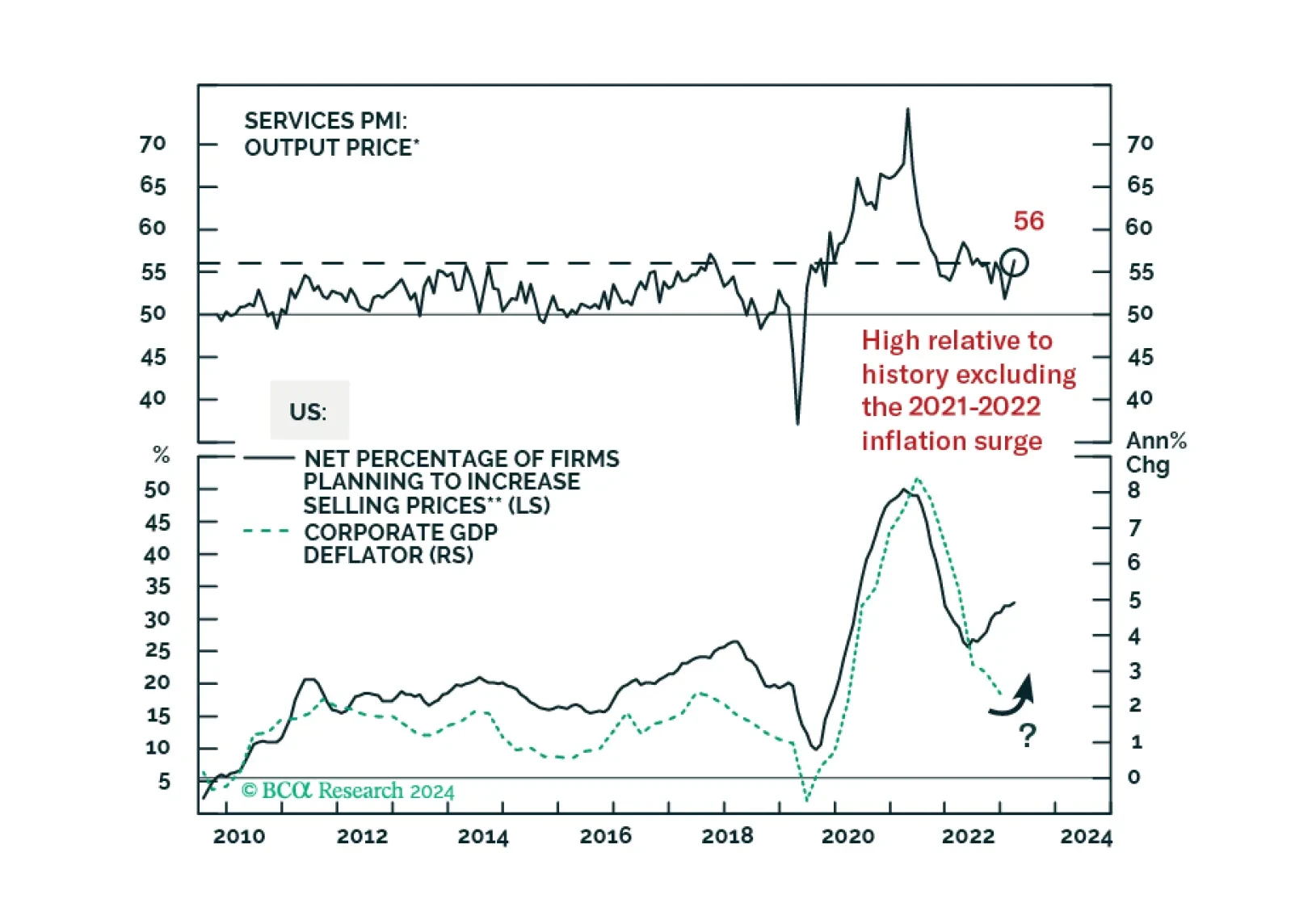

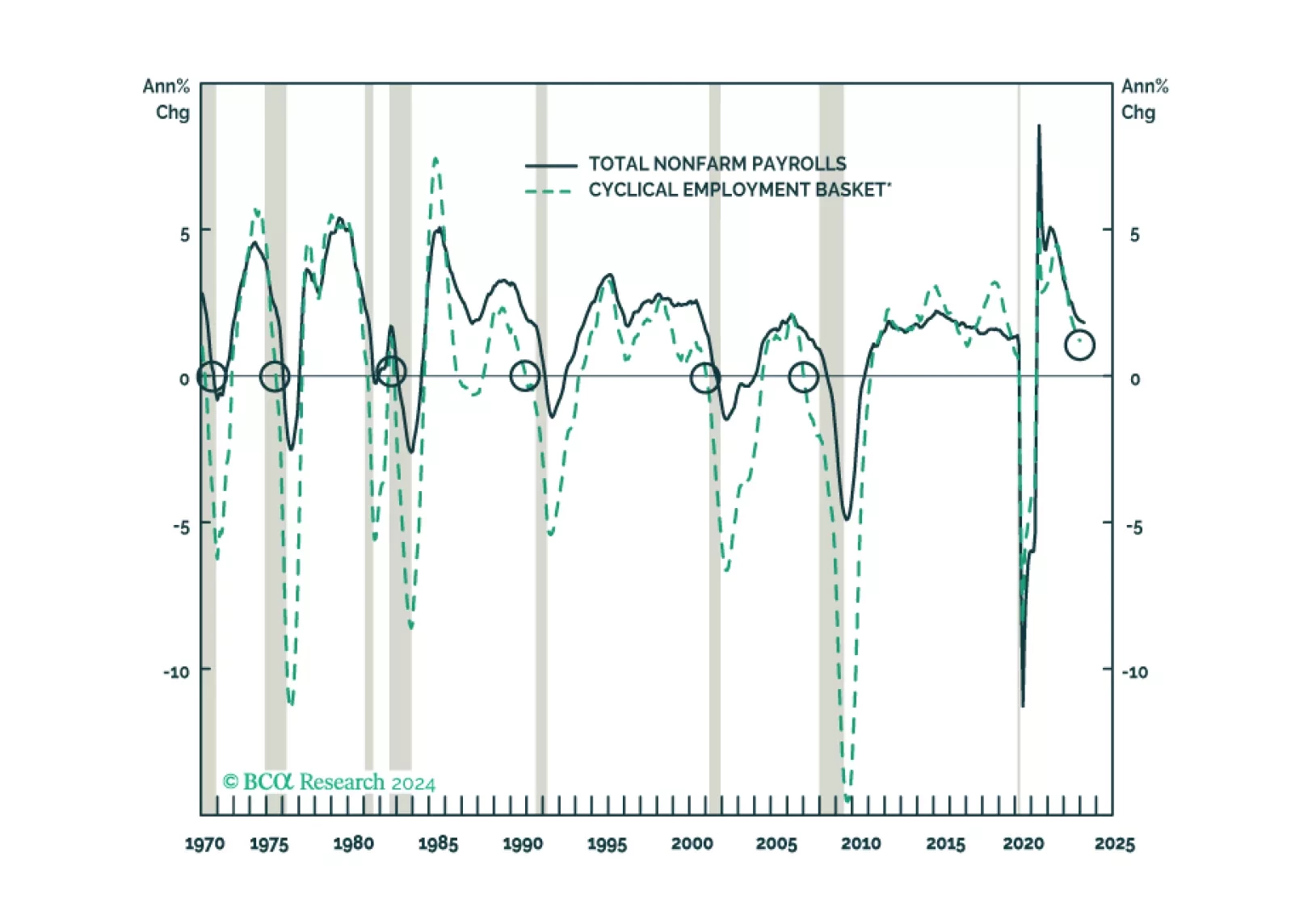

We look beneath headline data to assess the state of the labor market in cyclical goods-producing industries that have previously led overall nonfarm payrolls and in the services segments that have recently been leading the charge. The bottom-up view looks a lot like the top-down view: the labor market is softening, but very slowly, and offers no indications that a recession is at hand.