Fixed Income

Our Portfolio Allocation Summary for September 2025.

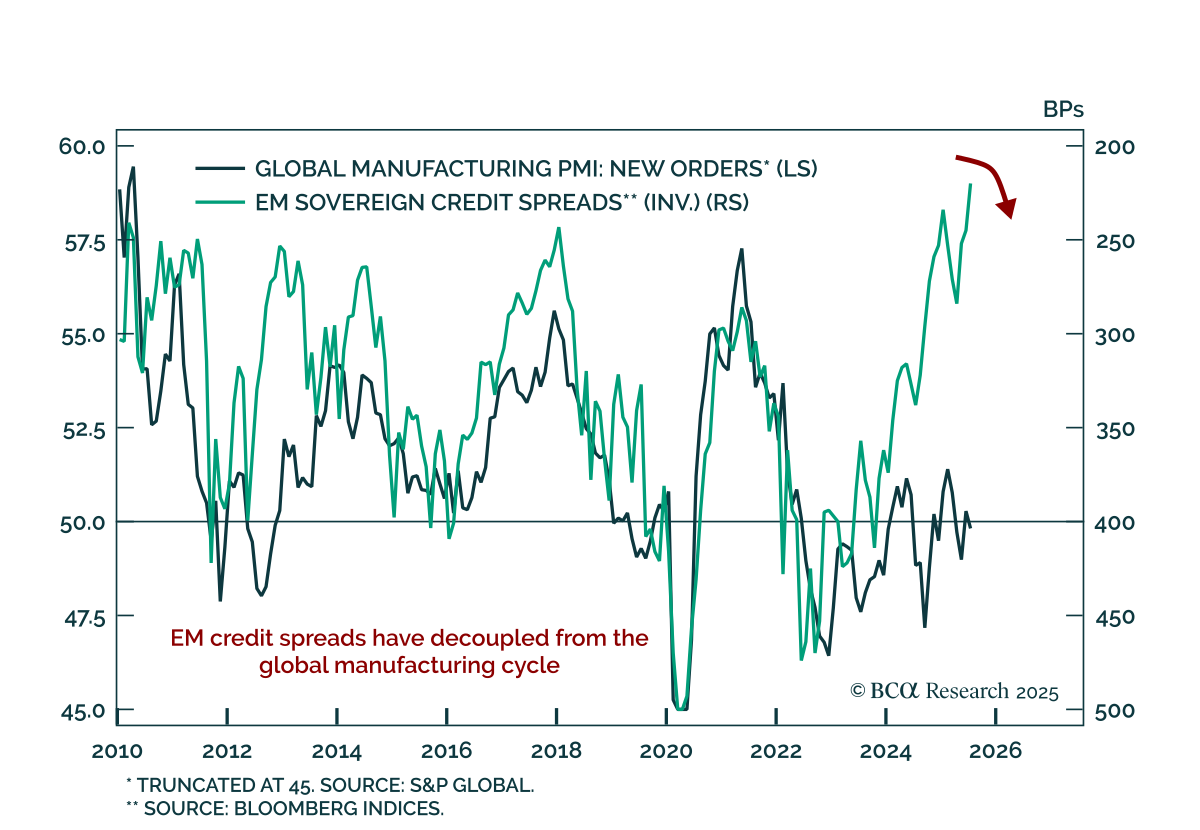

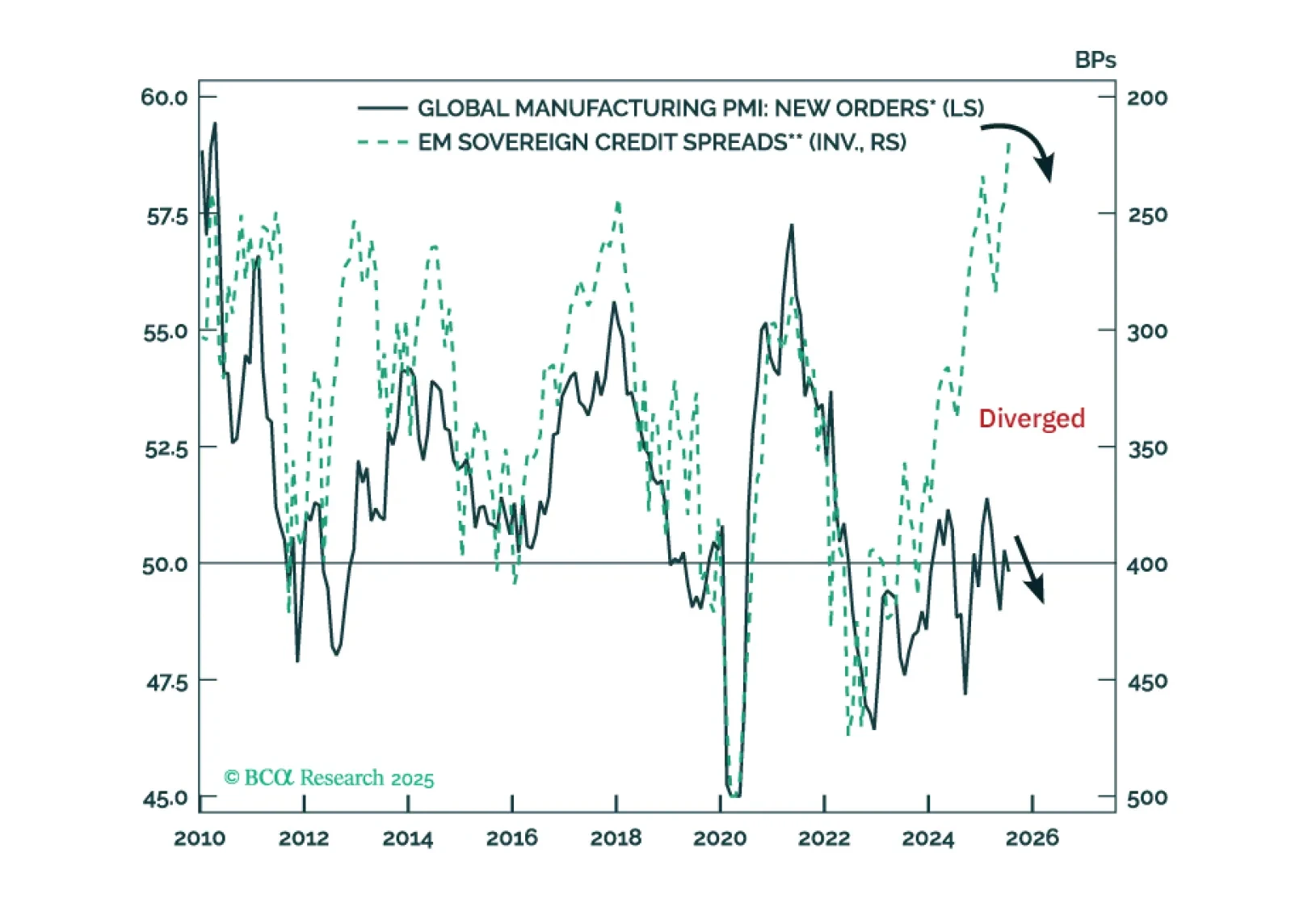

Our Emerging Markets strategists expect EM sovereign and corporate credit spreads to widen as global trade slows and domestic demand weakens, despite a softer US dollar. USD depreciation alone will not drive a sustained rally in EM credit, and tentative…

EM sovereign and corporate credit spreads are set to widen. Within a global credit portfolio, maintain a neutral allocation to EM credit markets versus US corporate credit. Favor EM local currency bonds over EM USD bonds.

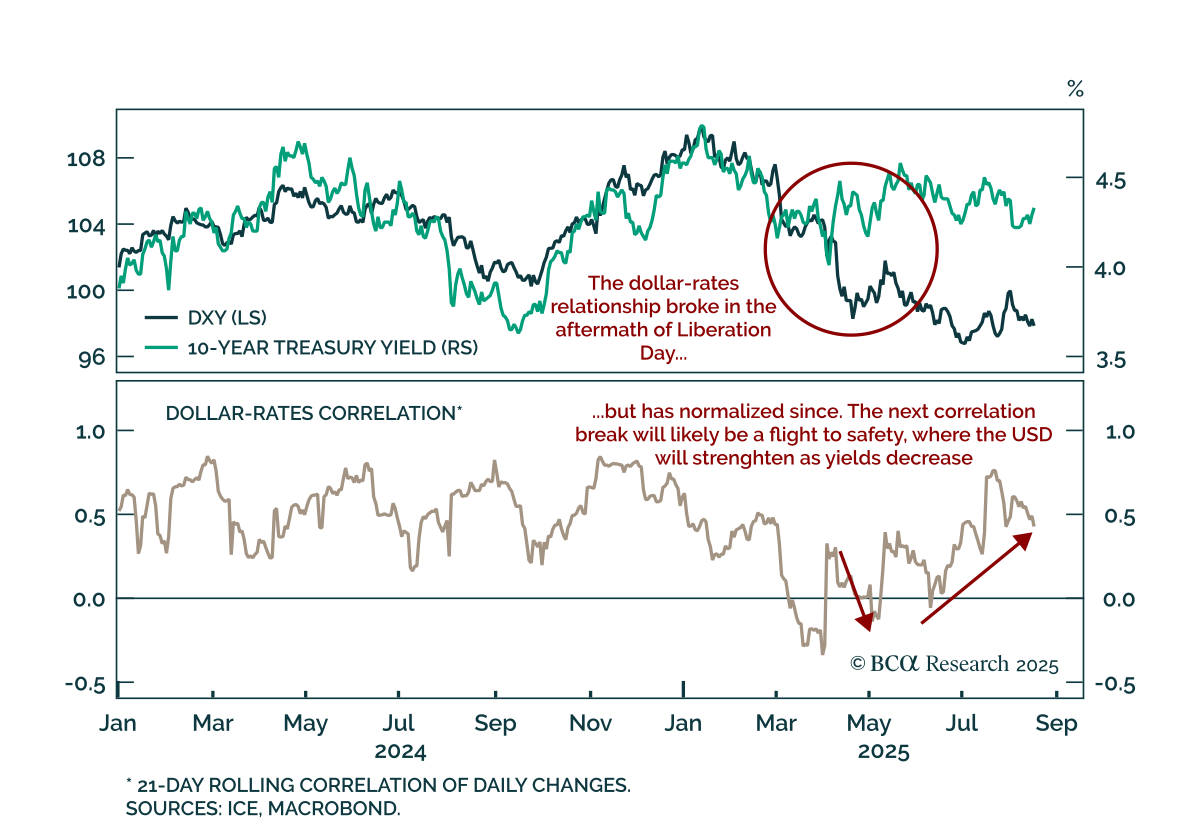

Trade tensions briefly broke the USD-rates link, but the dollar will remain a countercyclical currency for the near future. A key 2025 trend has been USD depreciation, driven by foreign investors reducing exposure to US assets. At the peak of stress,…

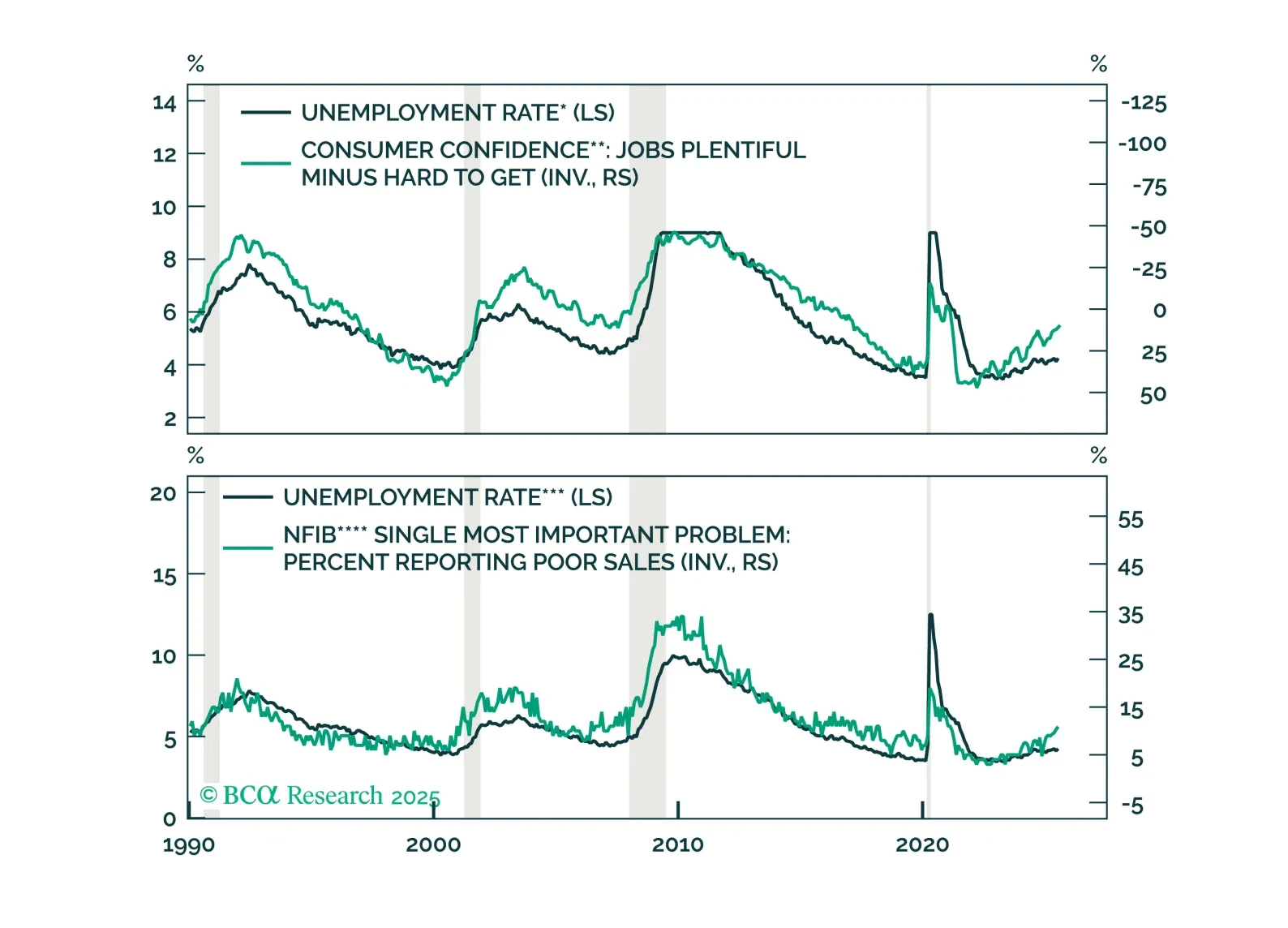

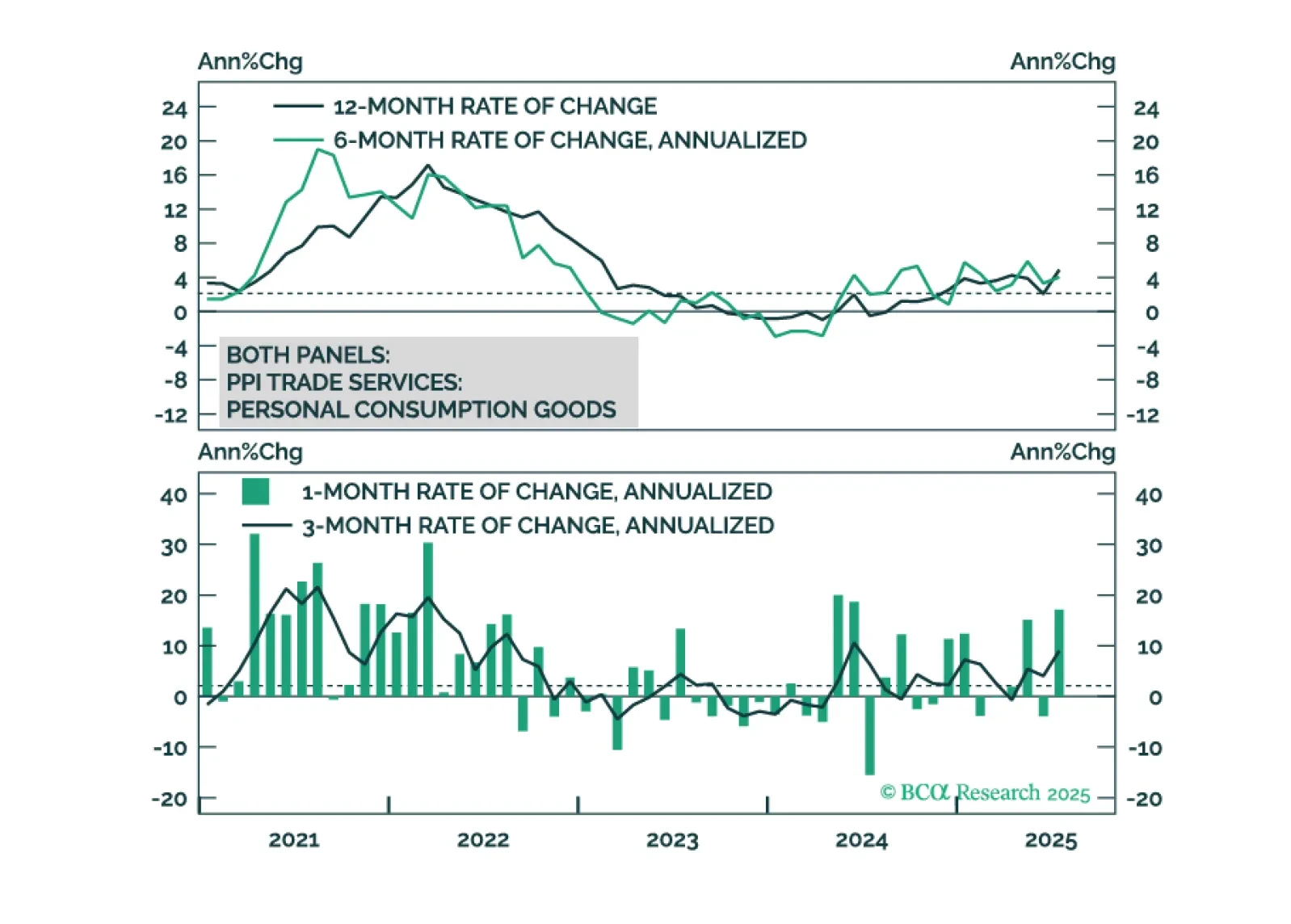

The cost of tariffs is falling on the US consumer, not foreign exporters or US firms.

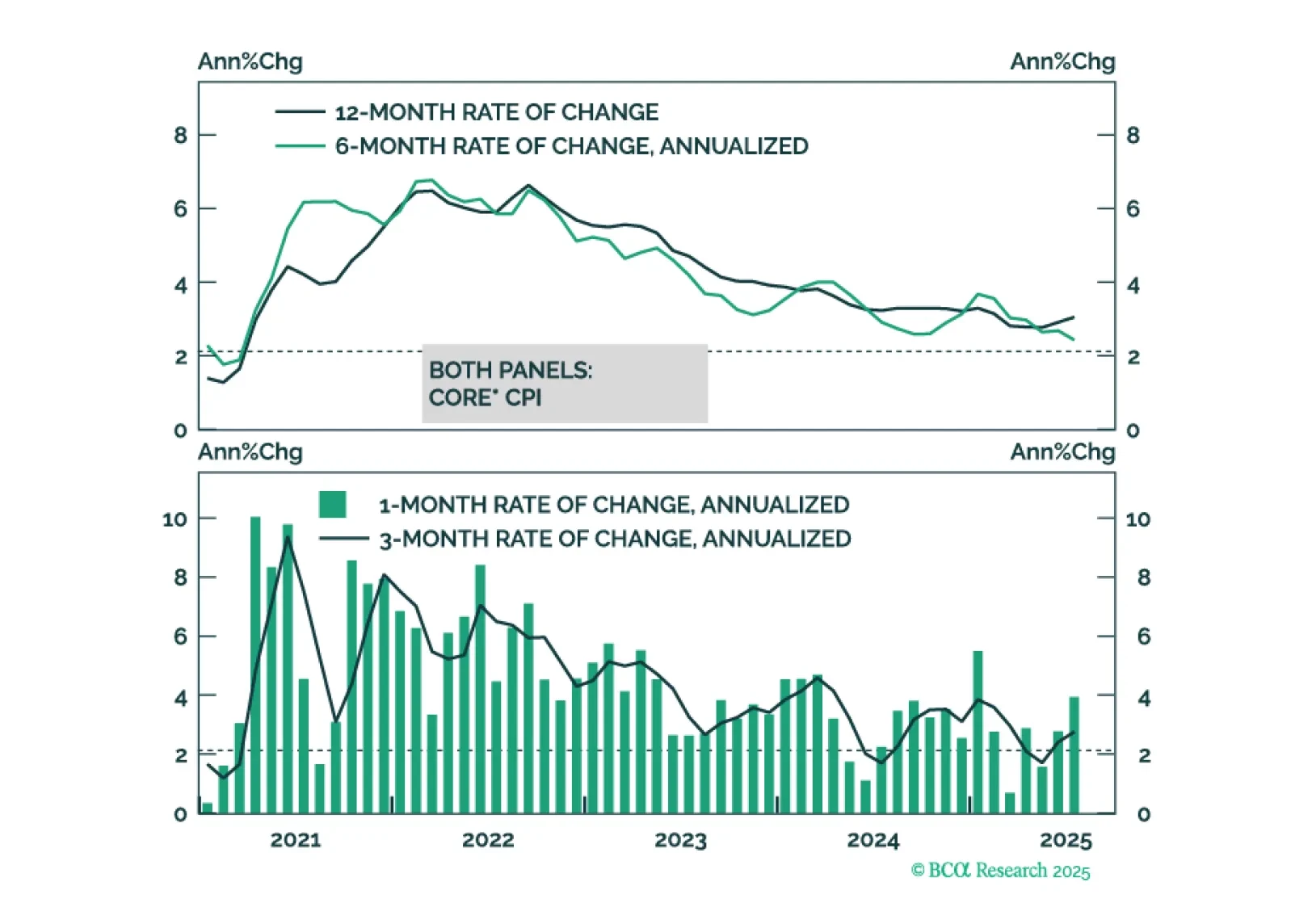

This morning’s CPI report marginally tips the scales in favor of a September rate cut.

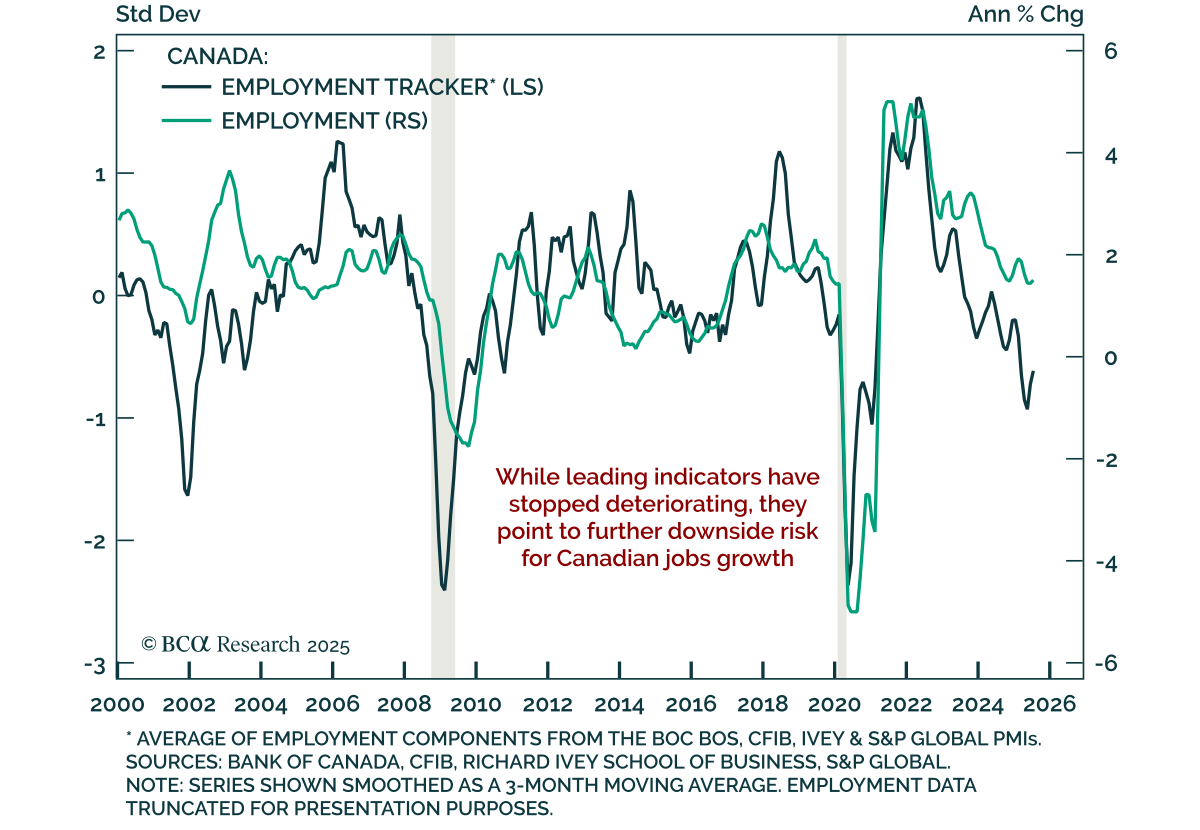

Canada’s July jobs report was mixed, but persistent slack and trade headwinds support our overweight in Canadian bonds and preference for 5s10s steepeners. Employment fell by 40.8k, driven by a 51k drop in full-time jobs, yet the unemployment rate held…

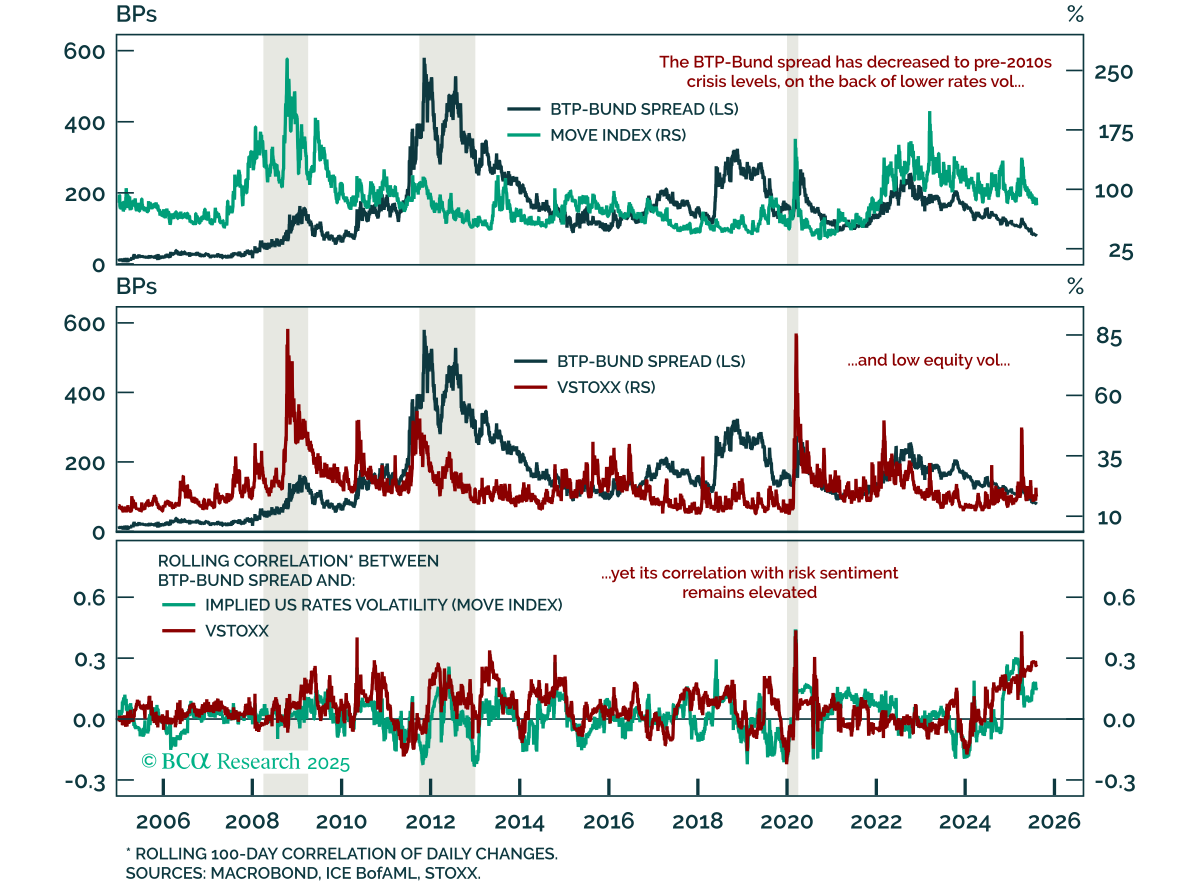

The BTP-Bund spread has tightened to pre-2010s levels, but with global growth risks we favor Gilts over Bunds and prefer BTPs over credit. While the EURO STOXX 50 remains rangebound since the Liberation Day recovery, European financial stress remains low. The…

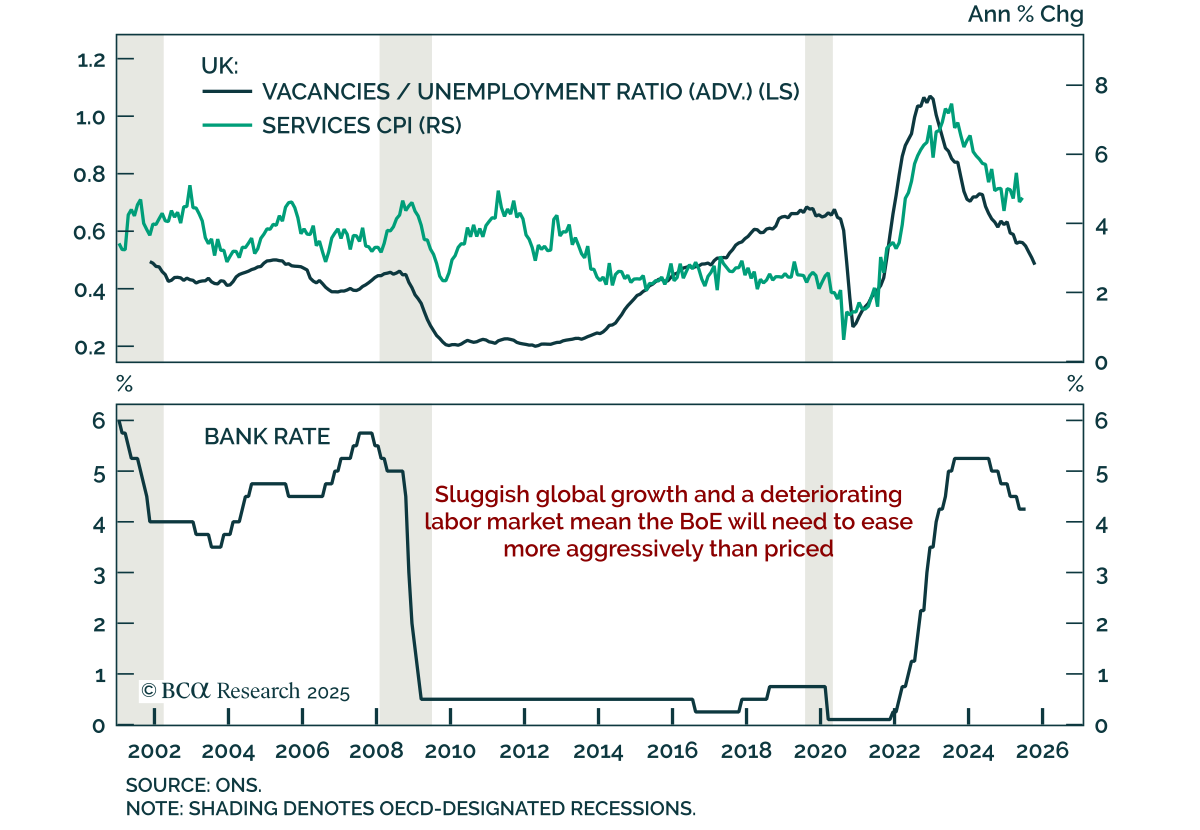

The BoE delivered a narrow rate cut to 4%, but a divided vote and fading growth momentum suggest markets are underpricing further easing. Stay overweight UK Gilts. The 5-4 split reflected concerns among dissenters about a stalling disinflation process as…

Expectations for US inflation at 3.3 percent are inconsistent with expectations for the Fed to slash rates, so one of these expectations is likely wrong. We describe how to play this mispricing. Plus, a new position is to go overweight global consumer discretionary (RXI).