Fixed Income

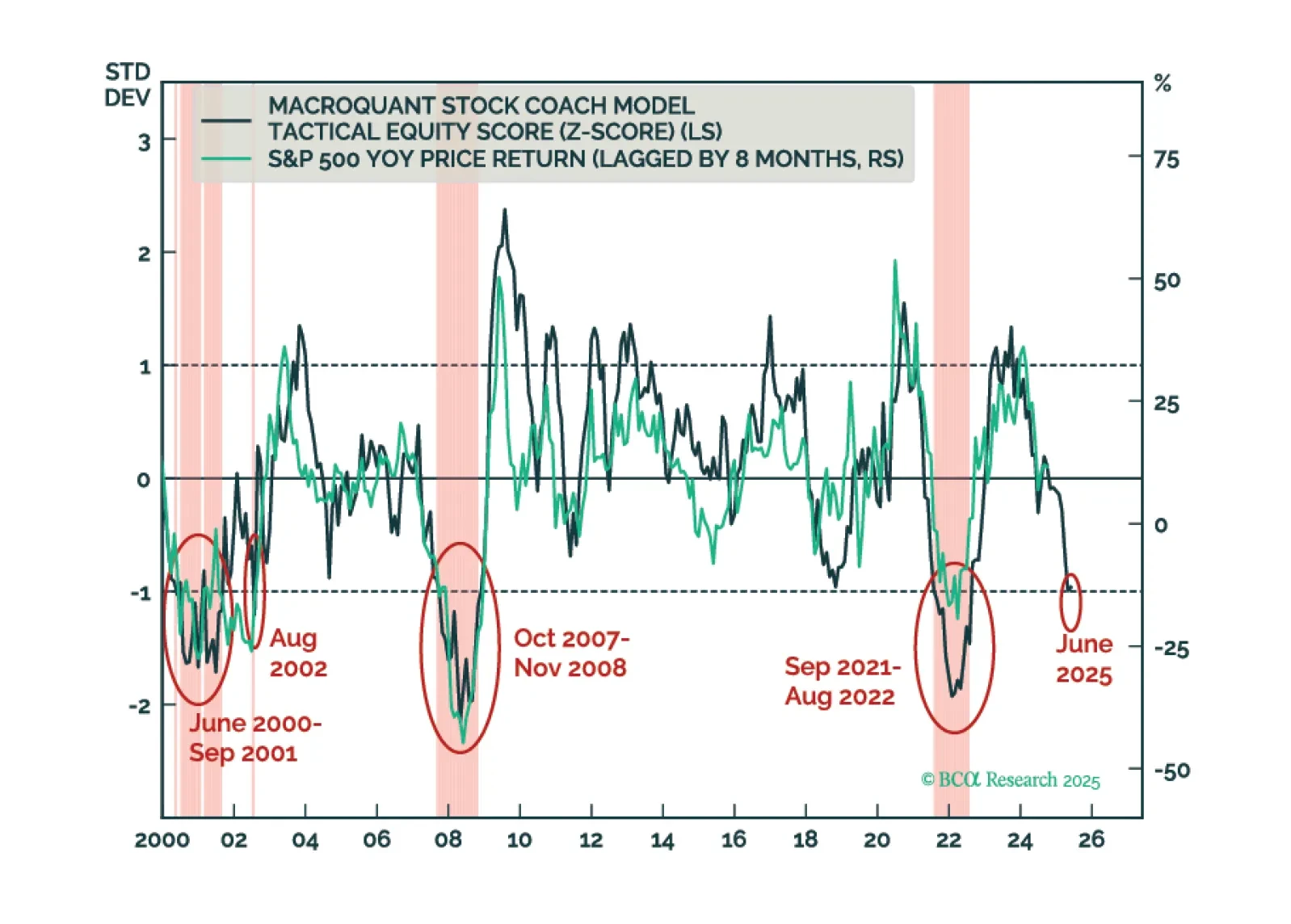

Investors should modestly underweight equities in their portfolios and look to turn more aggressively defensive once the whites of the recession’s eyes are visible. We think that will happen within the next few months.

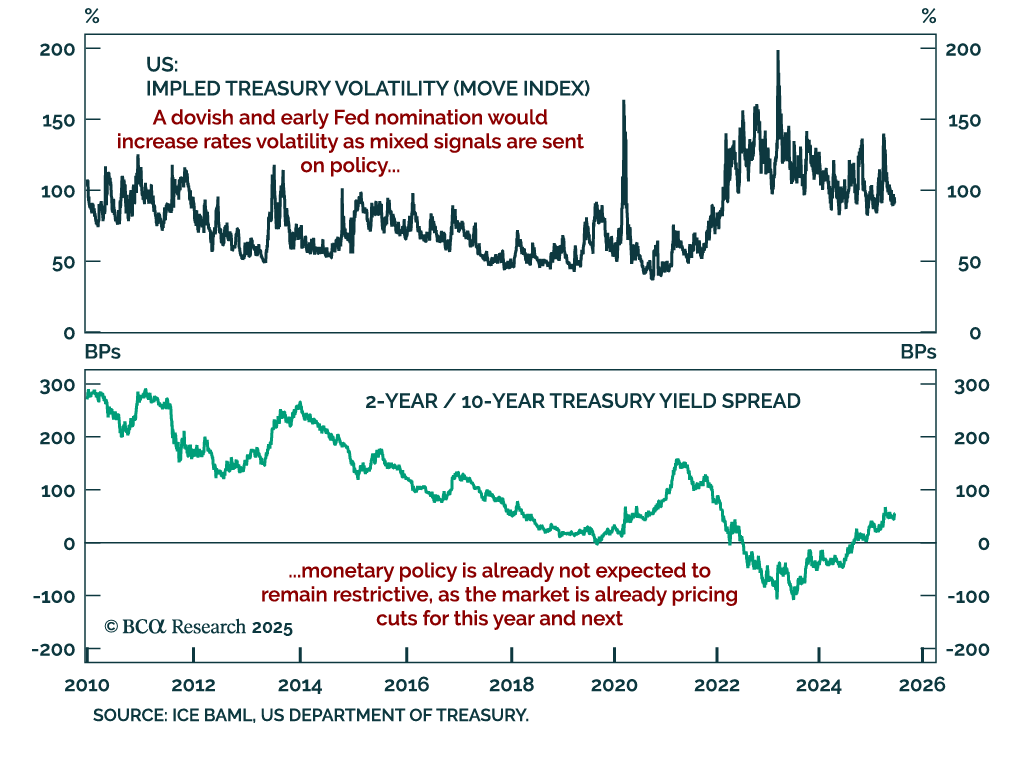

A dovish early Fed nominee would increase volatility in rates and FX as markets reassess the credibility of US monetary policy. News reports indicate the Trump administration is considering nominating a Fed successor ahead of the end of Chairman Powell’s…

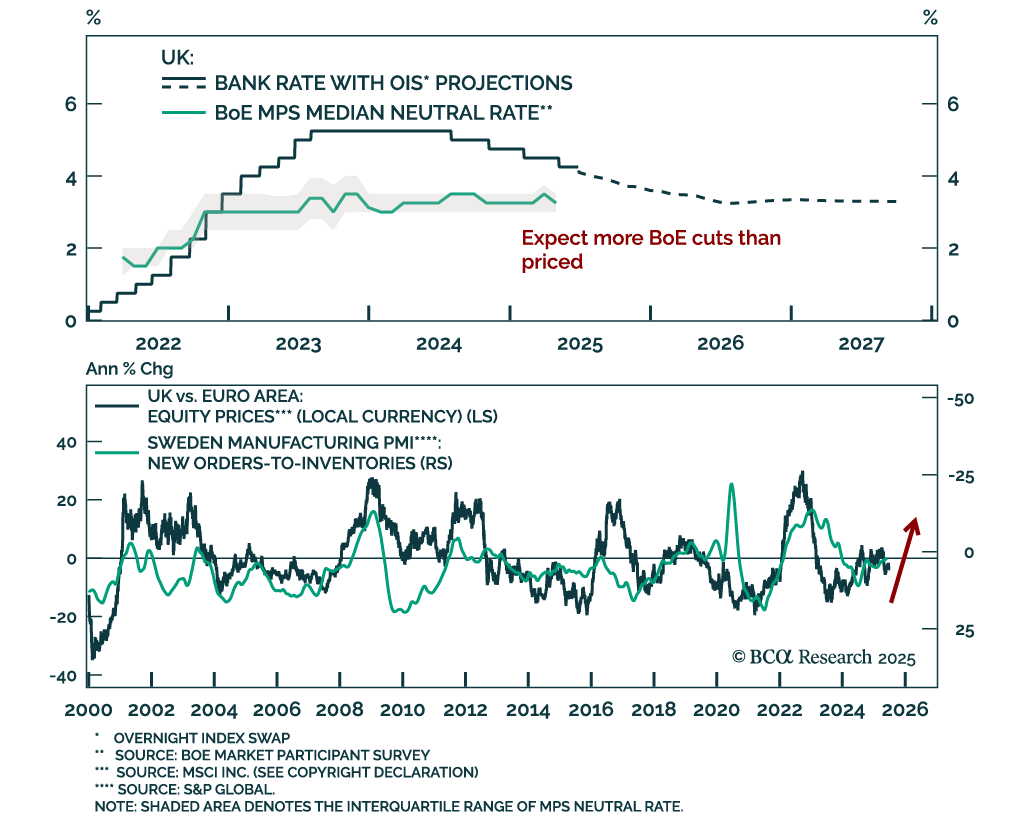

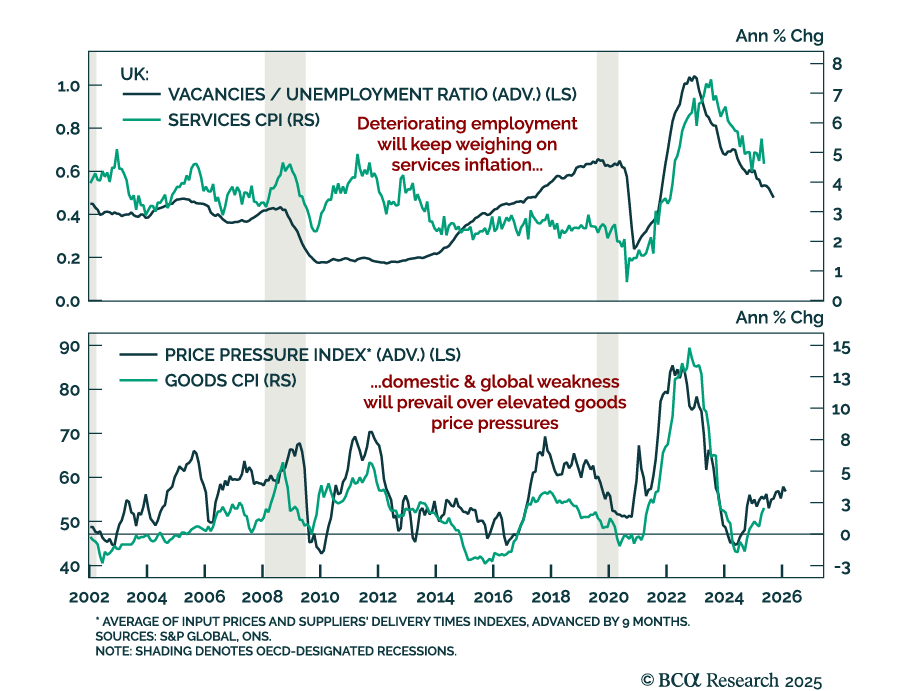

Our Global Fixed Income, FX, and European strategists expect aggressive BoE easing amid disinflation and labor market weakness, supporting an overweight in Gilts and UK equities versus the euro area. While UK productivity remains sluggish, a recovery in labor…

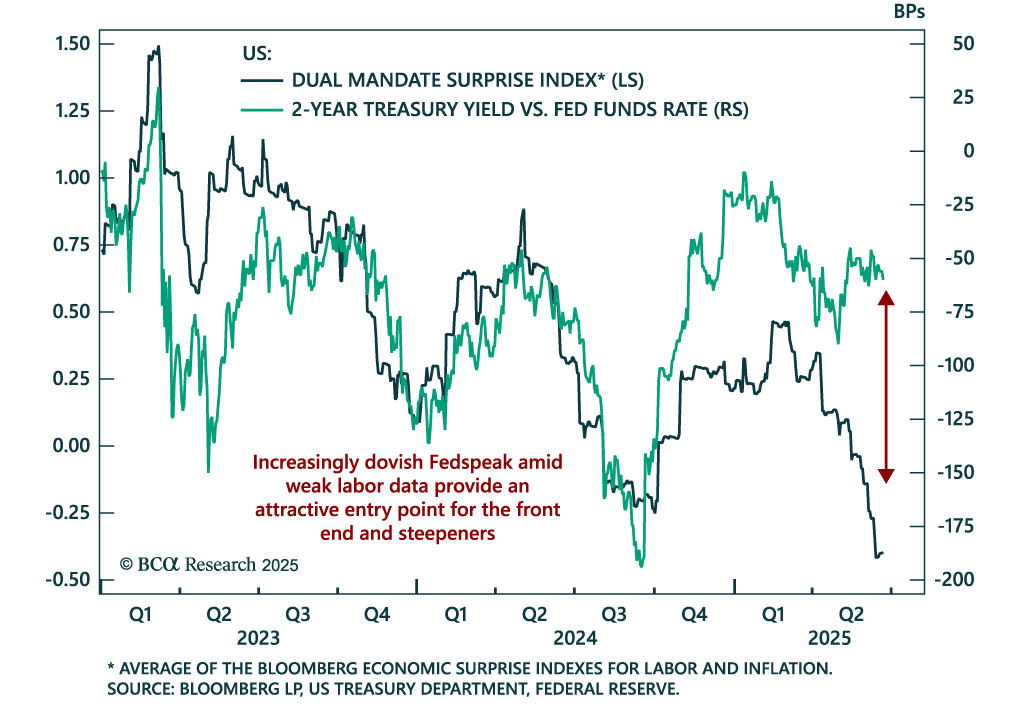

Dovish signals from Fed Governors Waller and Bowman increase the likelihood of a rate cut as early as July, supporting long front-end positions and steepeners. Last week’s FOMC meeting revealed a split between hawkish participants focused on the inflationary…

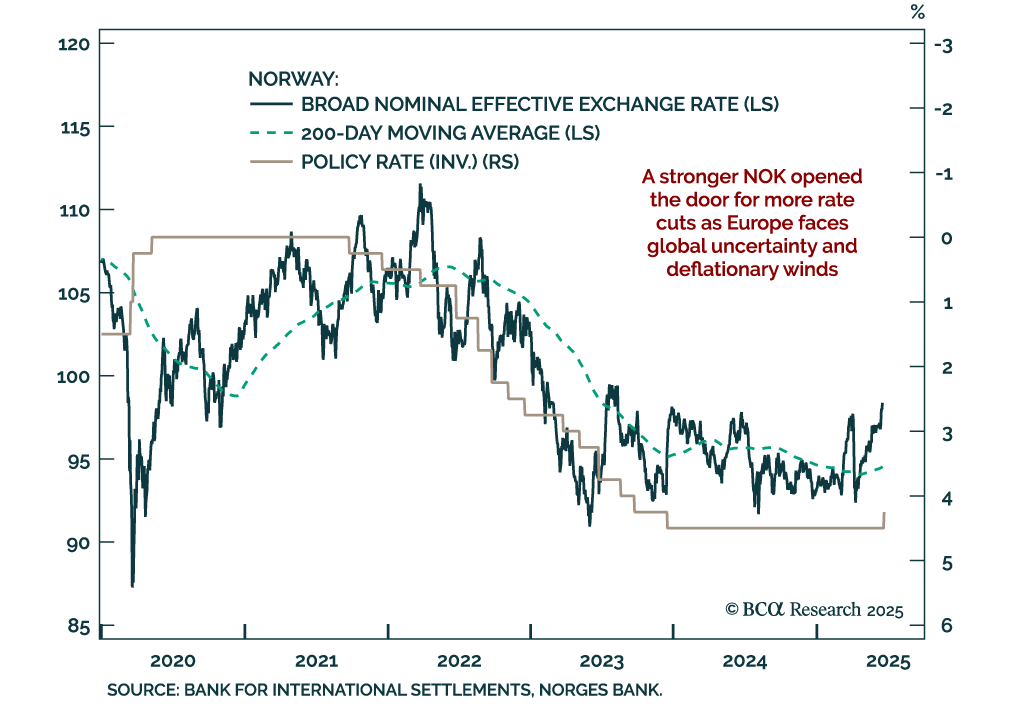

A stronger Norwegian krone has opened the door to more rate cuts, making Norwegian government bonds more attractive. Our Chart Of The Week comes from Jeremie Peloso, European Strategist. With its surprise 25 basis point cut, the Norges Bank made its first…

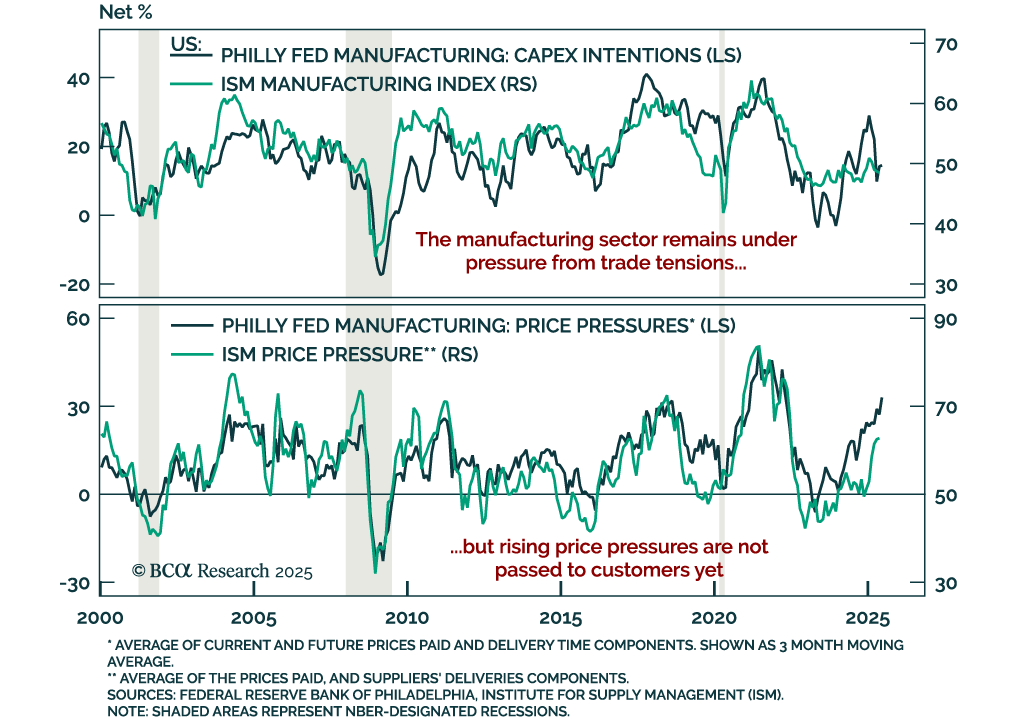

Worsening manufacturing momentum supports a long duration stance as recession risks remain elevated. The June Philly Fed survey came in below expectations, unchanged at -4.0. While shipments increased, new orders decelerated and employment measures fell.…

UK disinflation and labor market softening support our overweight in Gilts and short GBP trade. UK CPI came in slightly hotter than expected in May, with headline inflation at 3.4% y/y (vs. 3.5% in April) and core CPI meeting expectations at 3.5%, down from…

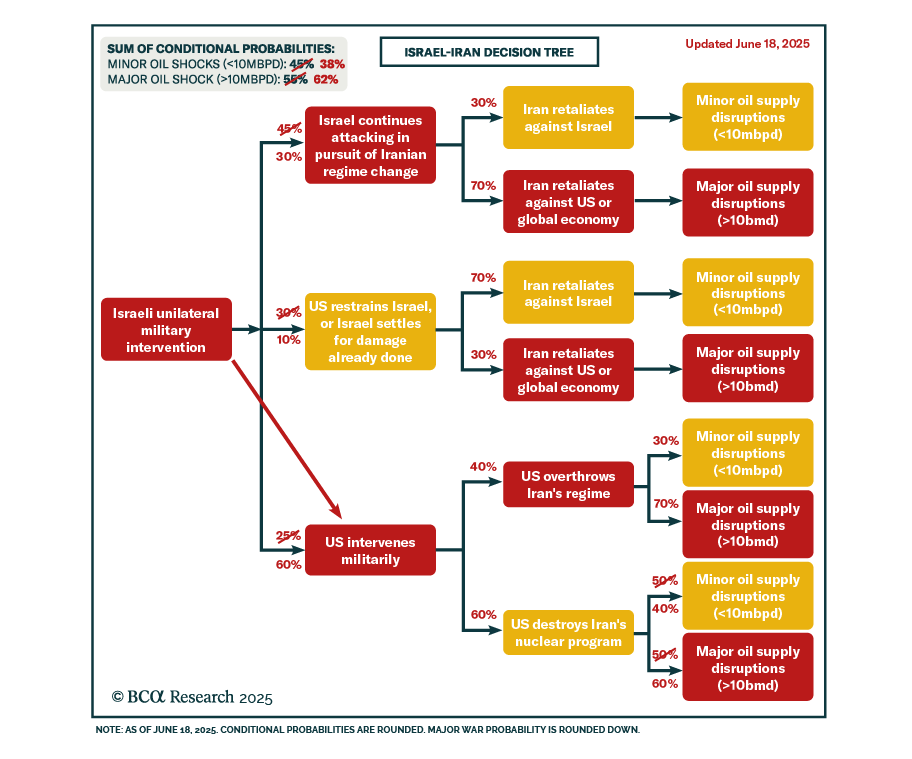

Our Geopolitical strategists expect US involvement in Israel’s military campaign against Iran, raising near-term risks to oil supply and market stability. Iran is likely to retaliate by targeting regional oil production and transport infrastructure,…

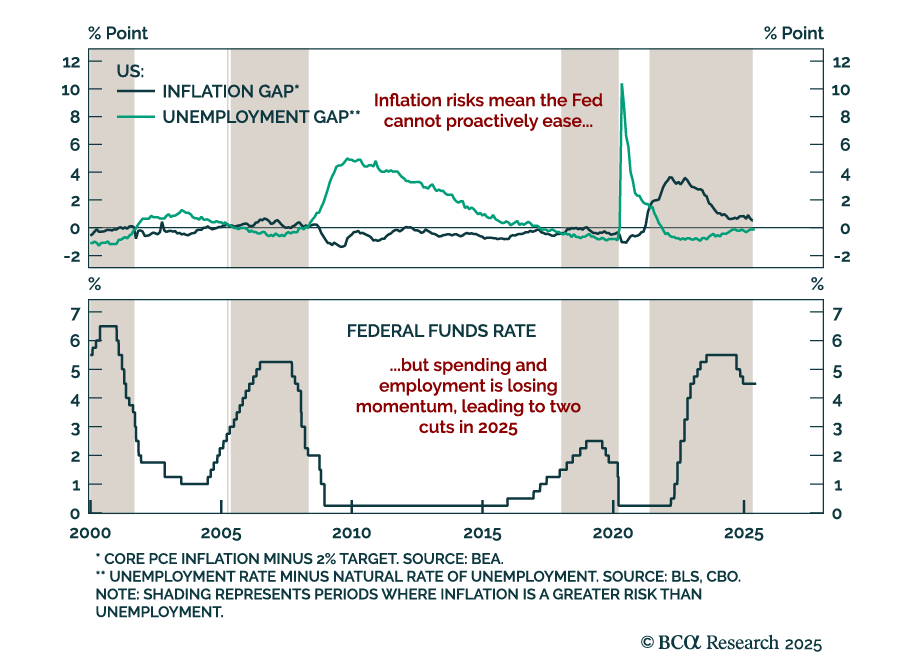

The Fed held rates steady between 4.25% to 4.5% and maintained a hawkish tilt despite soft data, reinforcing our long-duration and steepener trades. The updated dot plot showed upward revisions to both inflation and unemployment projections, as well as to…

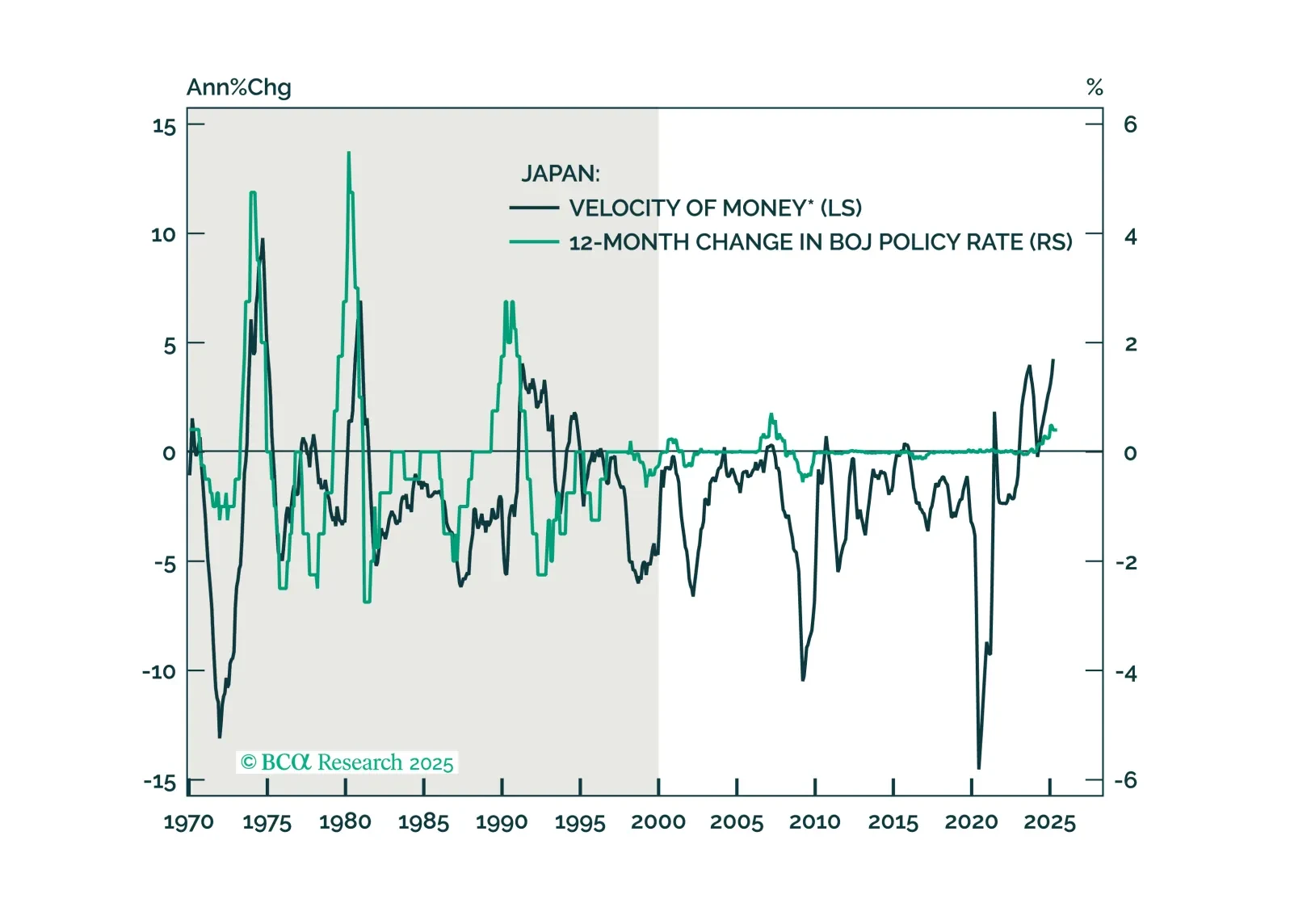

In this note, we reaffirm our underweight position in JGBs and long yen positions given the BoJ’s meeting overnight.