Fixed Income

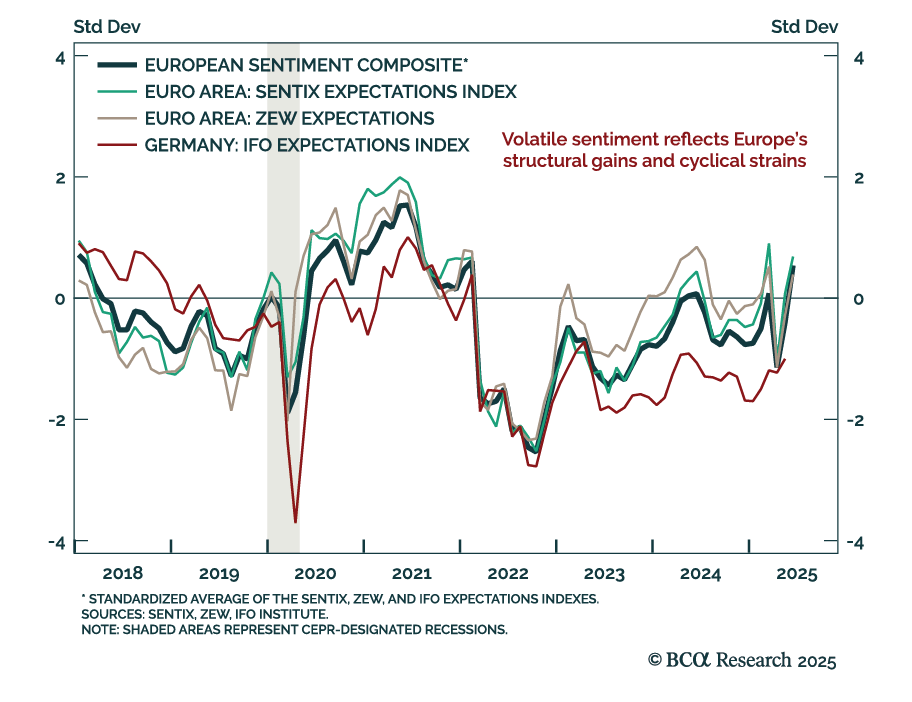

ZEW expectations jumped in May, but underlying macro fragility supports a cautious stance on eurozone assets. The ZEW expectations index for the euro area rose to 35.3 from 11.6, with Germany also beating expectations. The current situation component improved…

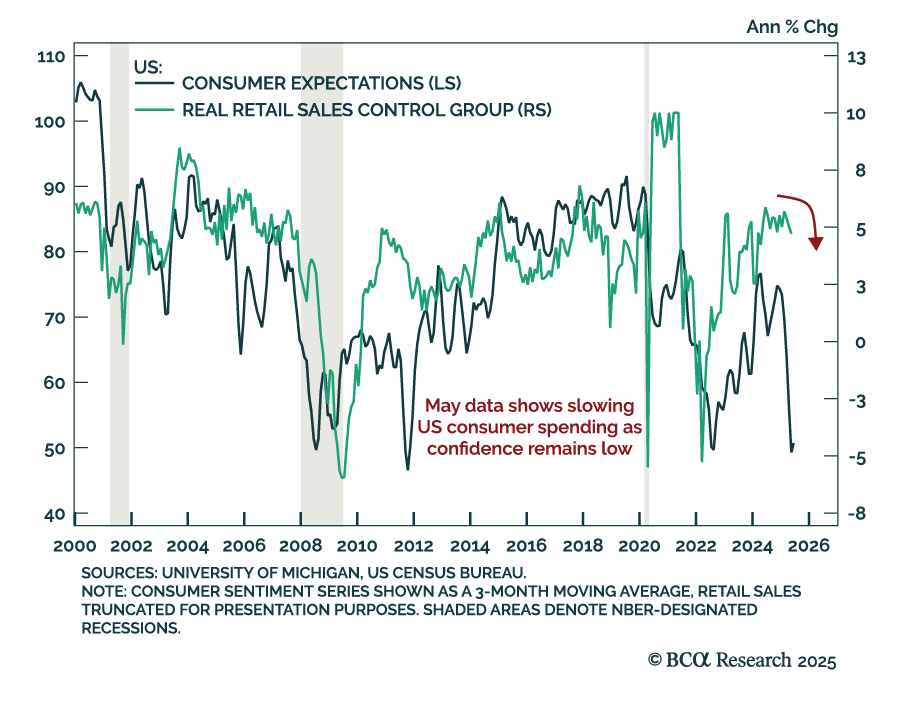

US May retail sales missed expectations, reinforcing our defensive allocation stance. Headline sales fell 0.9% m/m from a downwardly revised -0.1%. Core sales dropped 0.1%, while the control group rose 0.4%, beating estimates. Auto sales were especially weak…

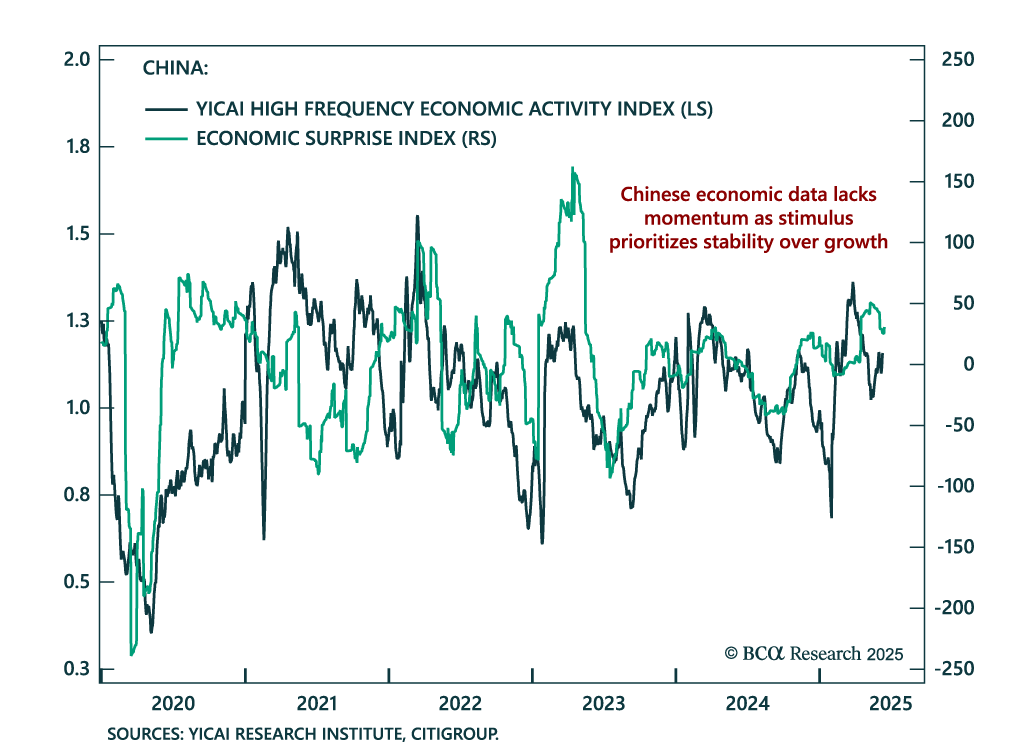

Household data beat in May, but China’s macro story remains fragile, reinforcing our overweight in local government bonds. Traditional supply-side activity decelerated, with industrial production and fixed asset investment both weaker, while retail sales and…

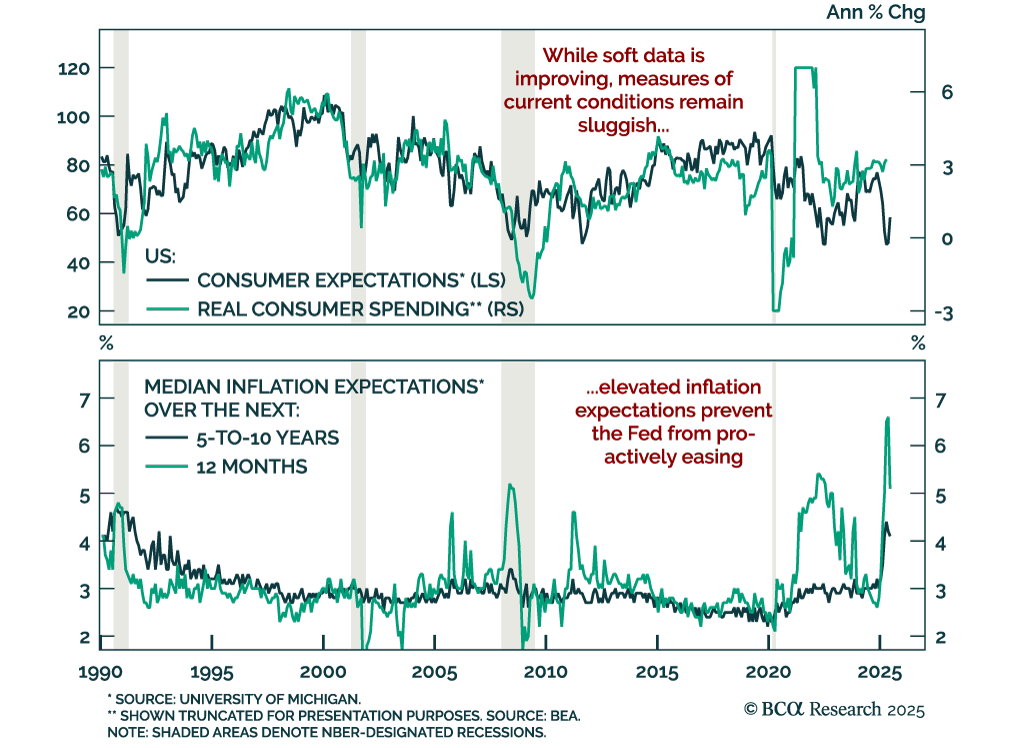

While consumer sentiment is rebounding, sticky inflation expectations and slowing growth warrant staying long duration and steepeners. The preliminary June University of Michigan Consumer Sentiment Index surprised to the upside, rising to 60.5 from 52.2.…

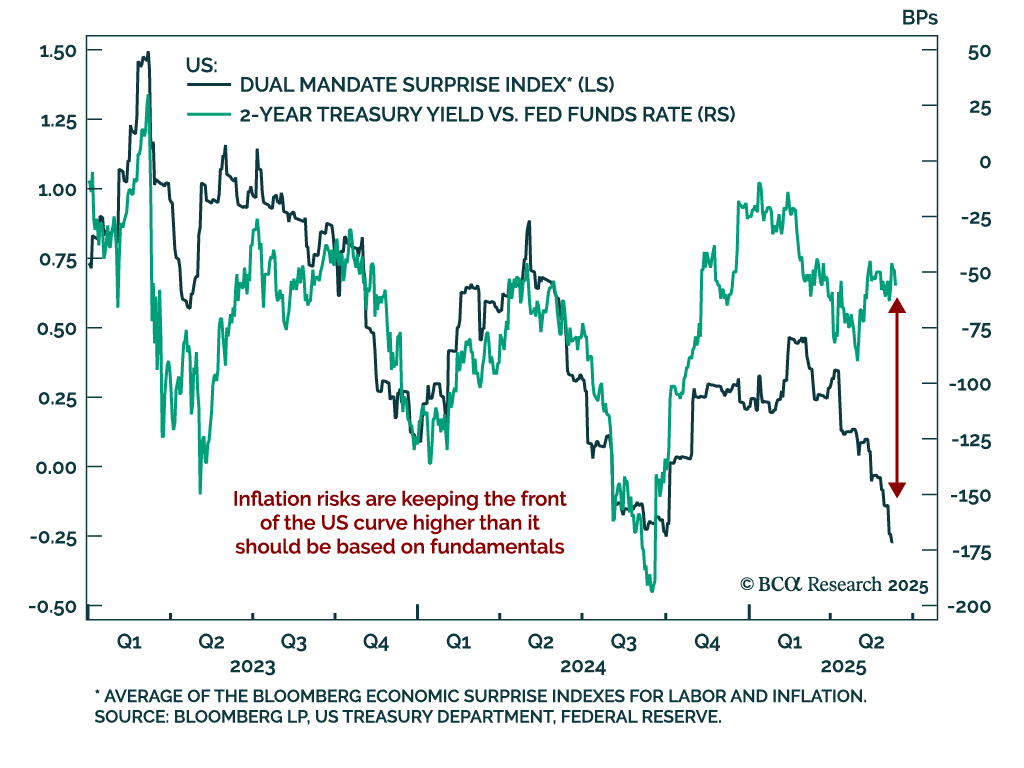

Elevated inflation expectations are keeping the Fed sidelined, reinforcing our long-duration and steepener bias in US rates. The US May CPI would have normally supported cuts, but the Fed cannot risk elevated short-term inflation expectations feeding…

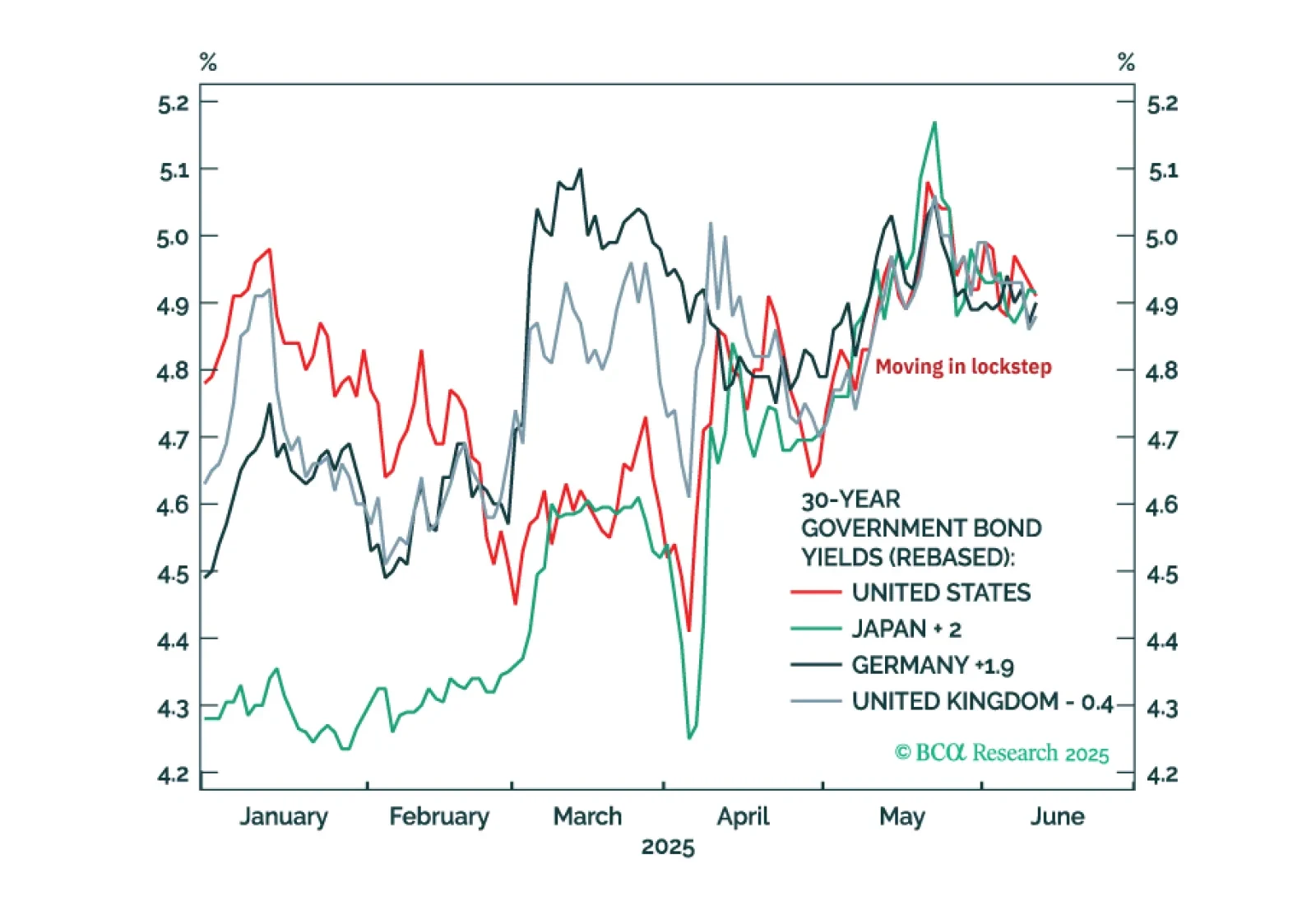

The perfectly synchronised moves in US, Japanese, German, and UK 30-year bond yields through the past two months are odd… and irrational. These irrational moves present compelling investment opportunities.

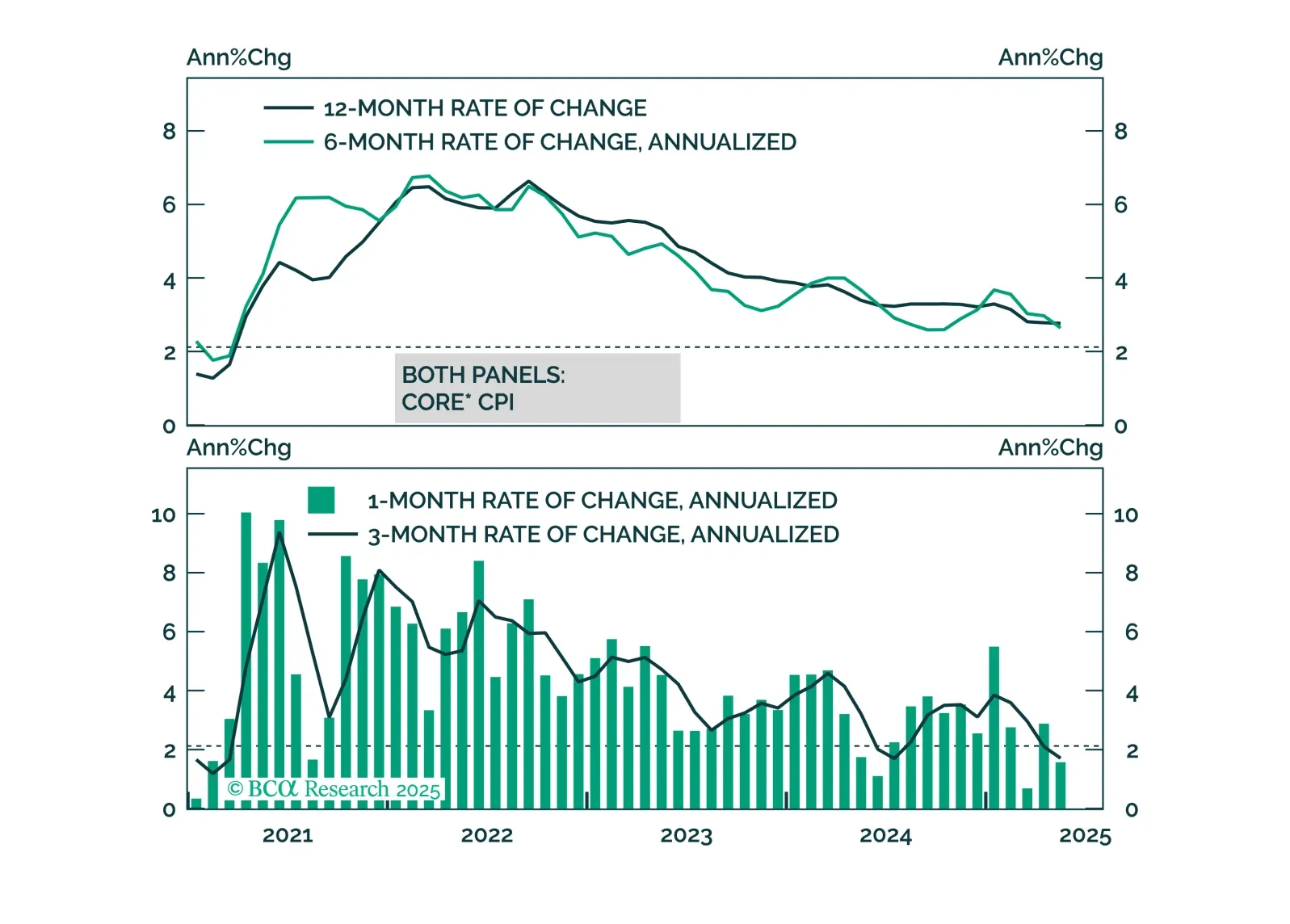

While we anticipate higher inflation in June, it looks increasingly likely that the price impact from tariffs will be less aggressive and long-lasting than many feared.

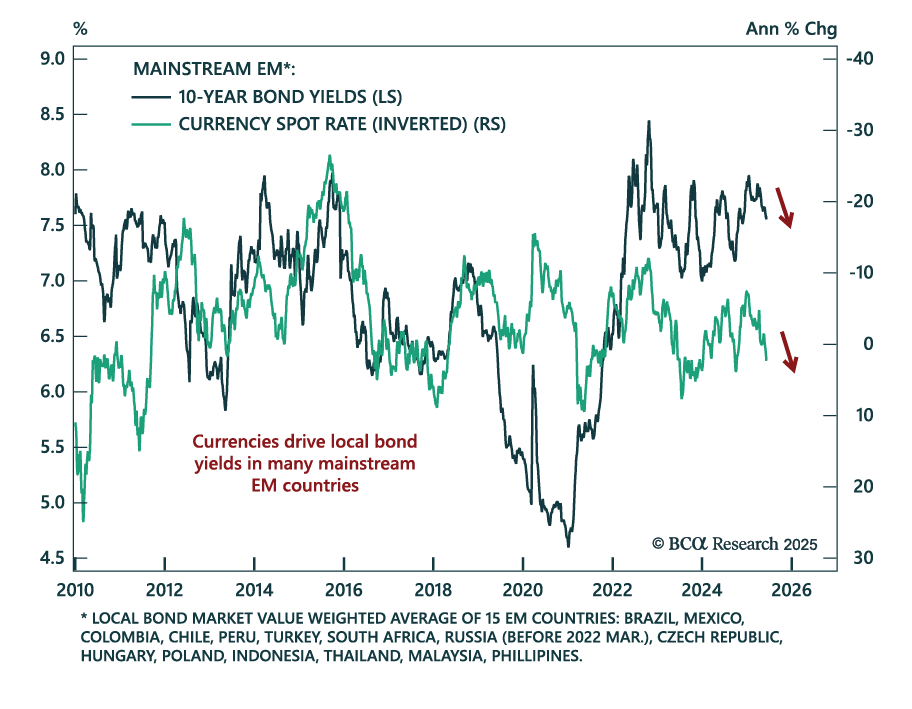

BCA’s EM strategists argue that a global macro shift is underway: A weaker US dollar will drive a retrenchment in US domestic demand and imports. Unlike previous cycles, dollar depreciation will be deflationary for the rest of the world rather than…

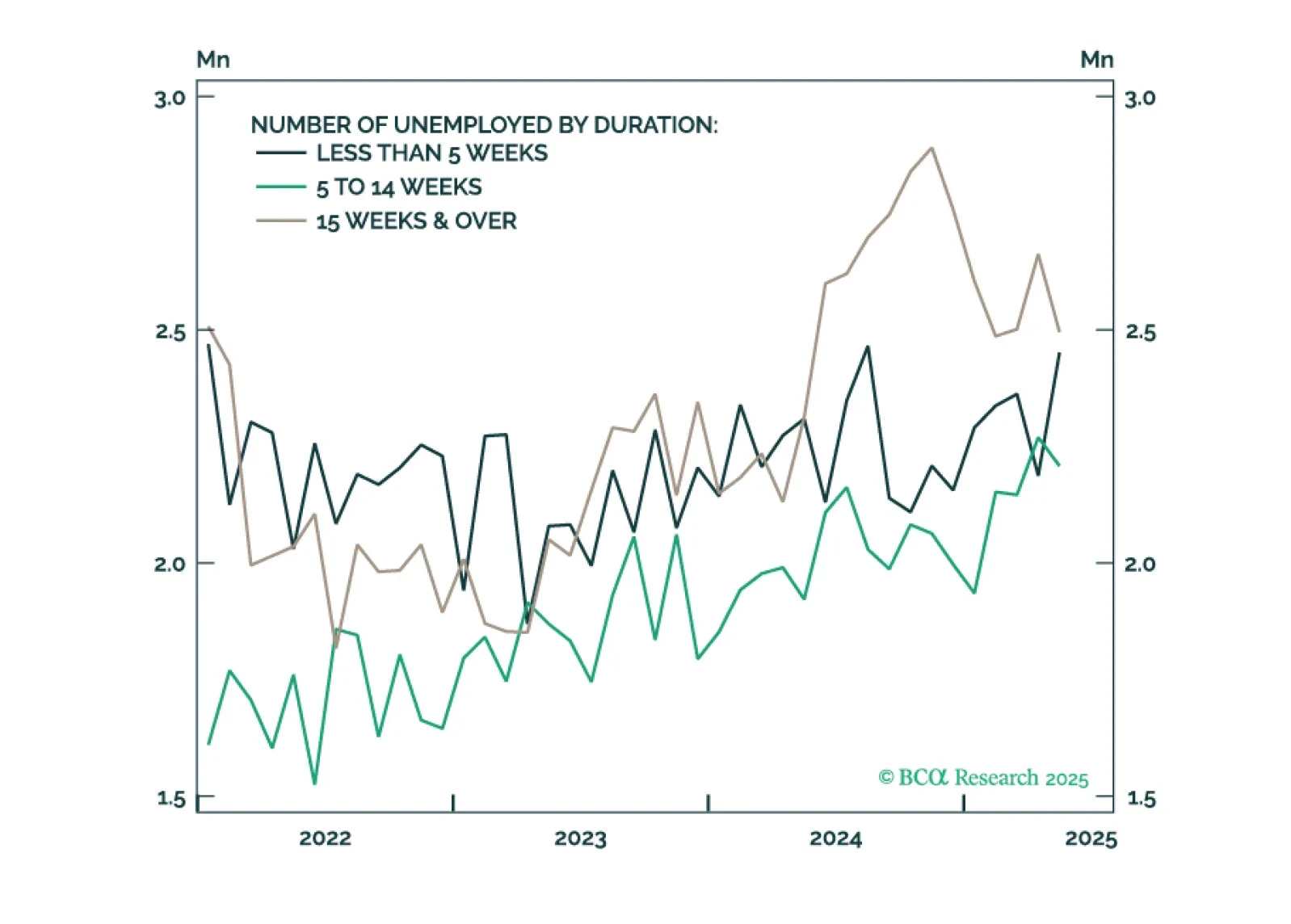

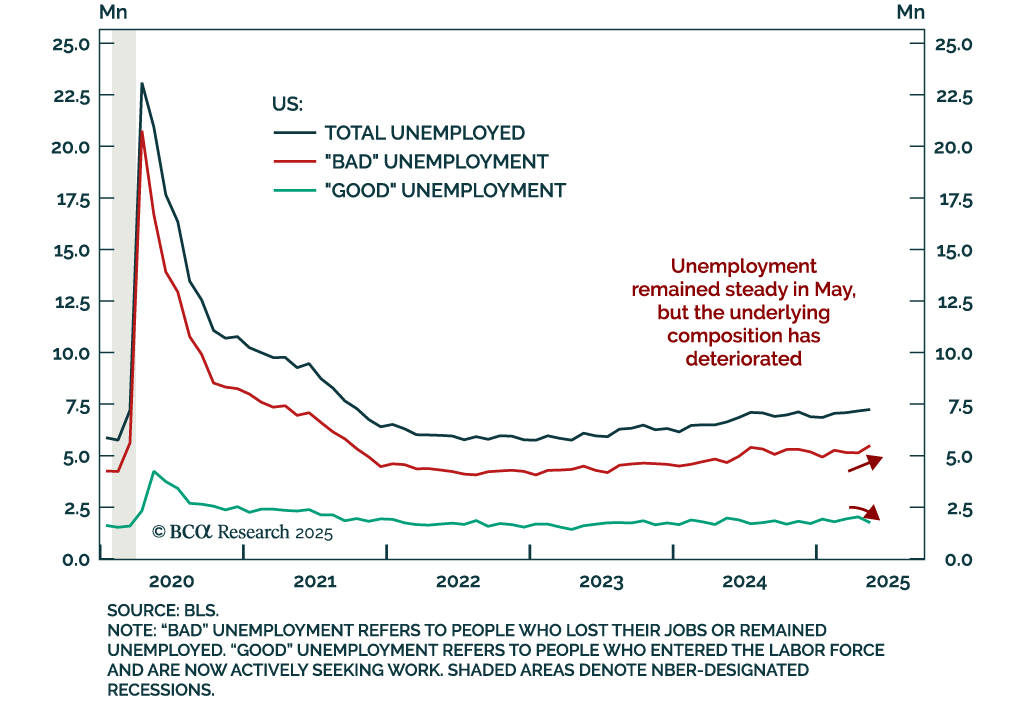

For now, measures of labor market utilization (like the unemployment rate) are only gradually weakening. But we know from history that these trends have a habit of quickly accelerating in advance of recession.

The May US jobs report reinforces our defensive stance as labor momentum is slowing even if not collapsing. Payrolls rose 139k, beating estimates, but decelerating from a downwardly revised 147k. Two-month revisions cut 95k jobs, again signaling that initial…