Fixed Income

The undercurrents of global financial markets signal deteriorating global growth conditions. There is little cash on the sidelines in the US, the Euro Area, and Japan. If the budding bear market resembles the 2000-2003 one, EM stock prices are unlikely to outperform global equities in the initial leg but could outperform in the latter stage of the global selloff.

The Swedish economy’s cyclicality and sensitivity to global trade make it a reliable bellwether for global growth. Sweden is facing significant domestic weakness. Employment growth declined by 0.14% y/y in July and households’ debt burden stands at 155% of…

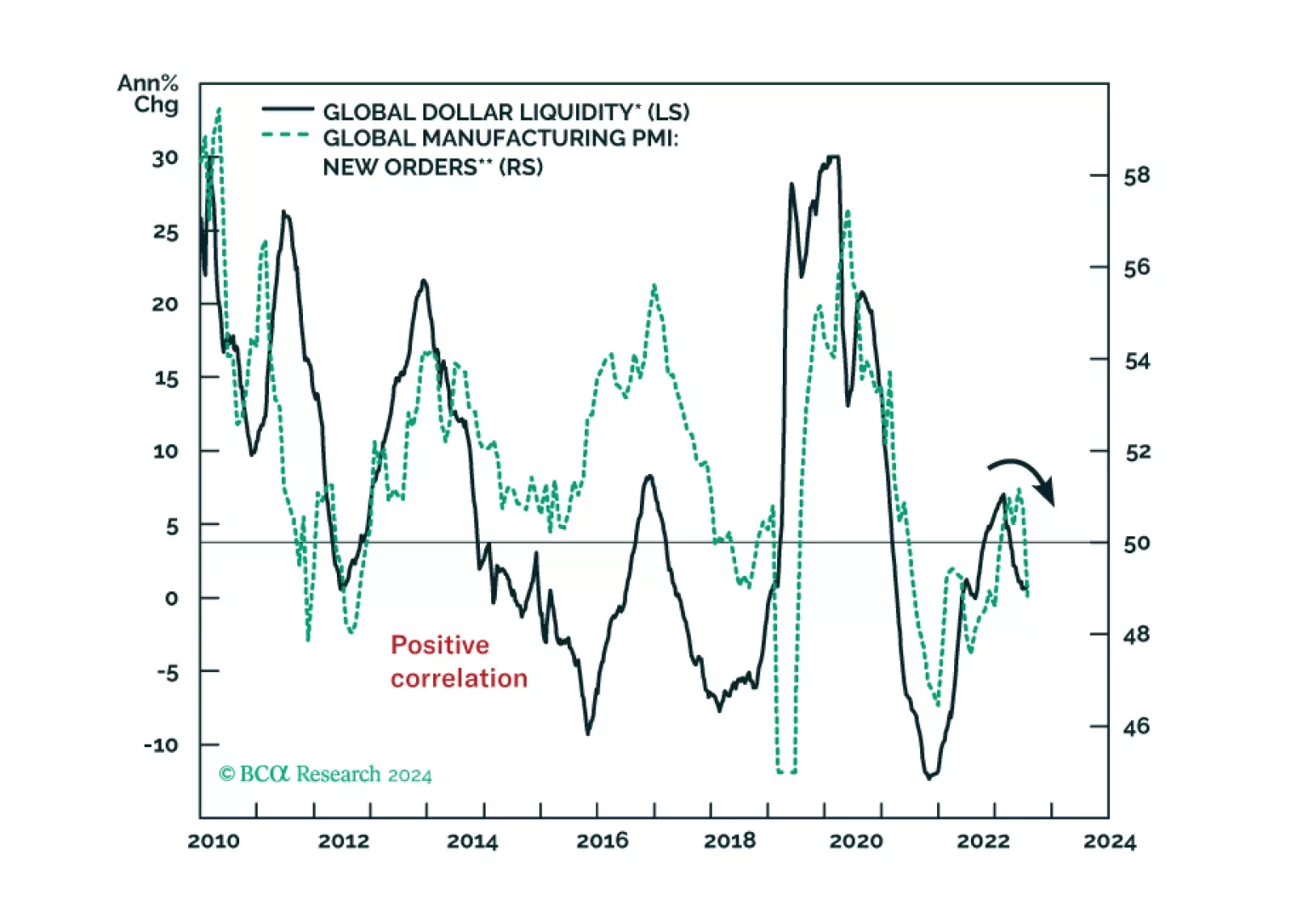

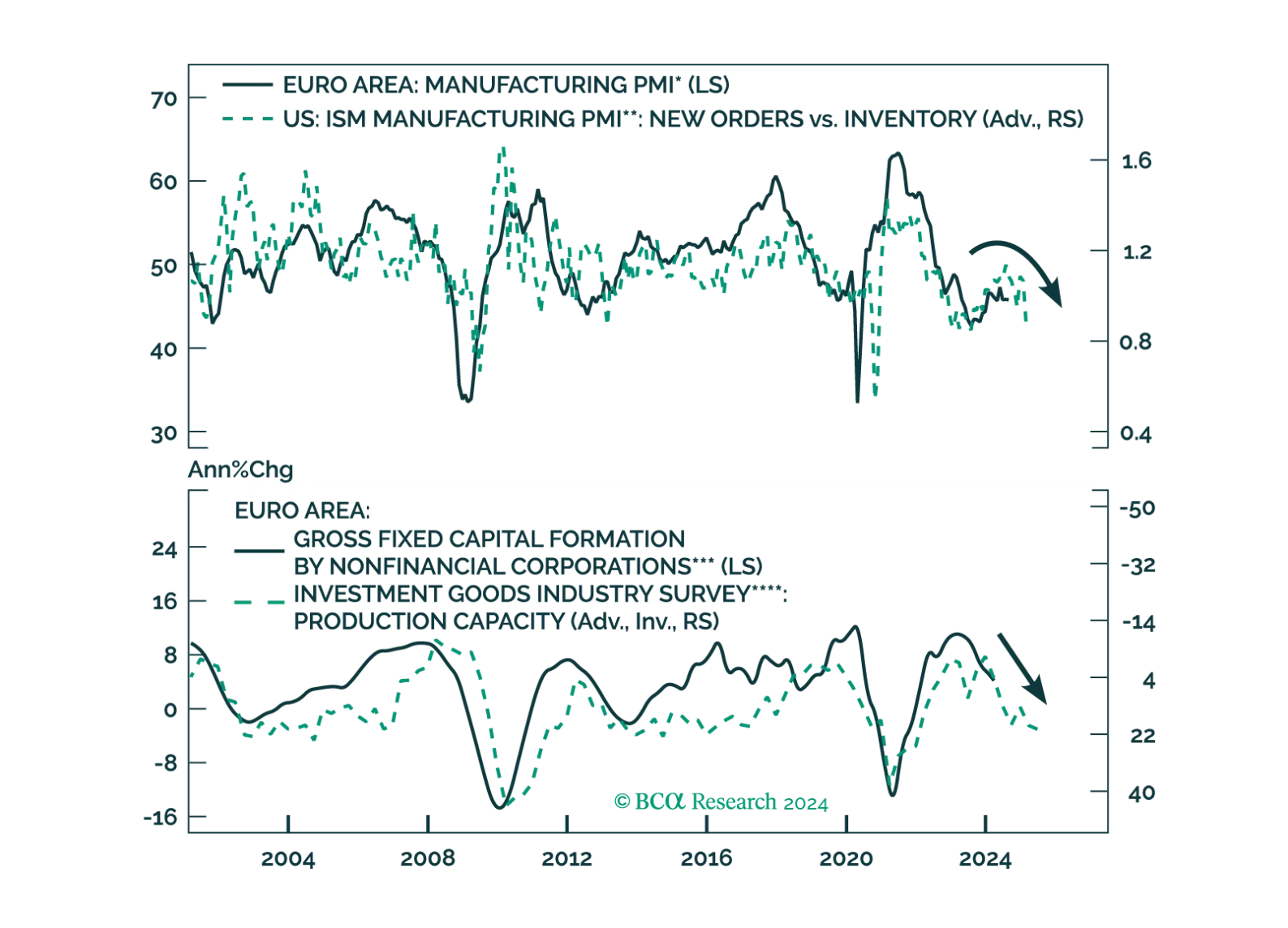

Crucial leading indicators of the global and European economies continue to deteriorate. How should investors position their European portfolios to benefit from these trends?

The pro-cyclical Eurozone economy is highly exposed to a global downturn, which we expect will materialize by early 2025. The ECB is behind the curve and we thus expect it to ease more aggressively than markets expect next year. A dovish surprise in 2025…

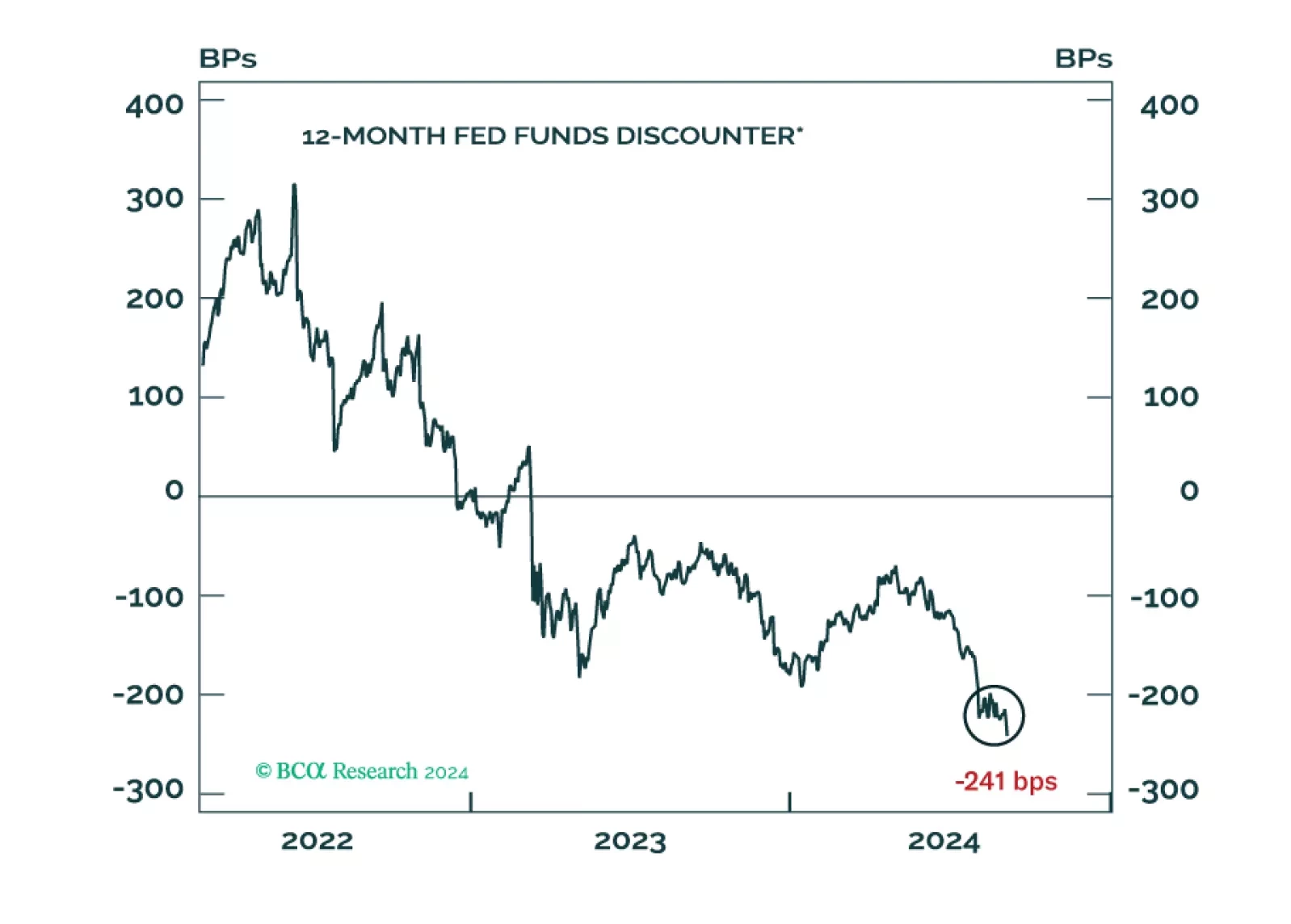

This morning's employment report, particularly the downward revisions to prior months, strengthens our conviction that the US economy is headed for recession.

Our Portfolio Allocation Summary for September 2024.

The Fed’s Beige Book compiles qualitative input sourced from business and other organizational contacts in each of its 12 Districts. It precedes FOMC meetings by a couple of weeks and is meant to help participants trace the evolution of economic conditions. …

The risk-on soft-landing narrative dominated investors’ psyche last month and pro-cyclical assets topped the August return ranking. Asian currencies led the pack by a wide margin, while the dollar was the largest laggard. Markets pricing in an upcoming Fed…

The 2Y/10Y segment of the yield curve is flirting with un-inversion. Aggressive rate cut expectations have largely driven its steepening, with the 2-year Treasury yields falling nearly 100 bps over the past couple of months. Our colleagues at the Bank…

According to BCA Research’s European Investment Strategy service, an increase in borrowing costs will further weaken vulnerable corporate balance sheets. As suggested by their Corporate Health Monitors (CHMs), the health of High-Yield corporate balance sheets…