Global

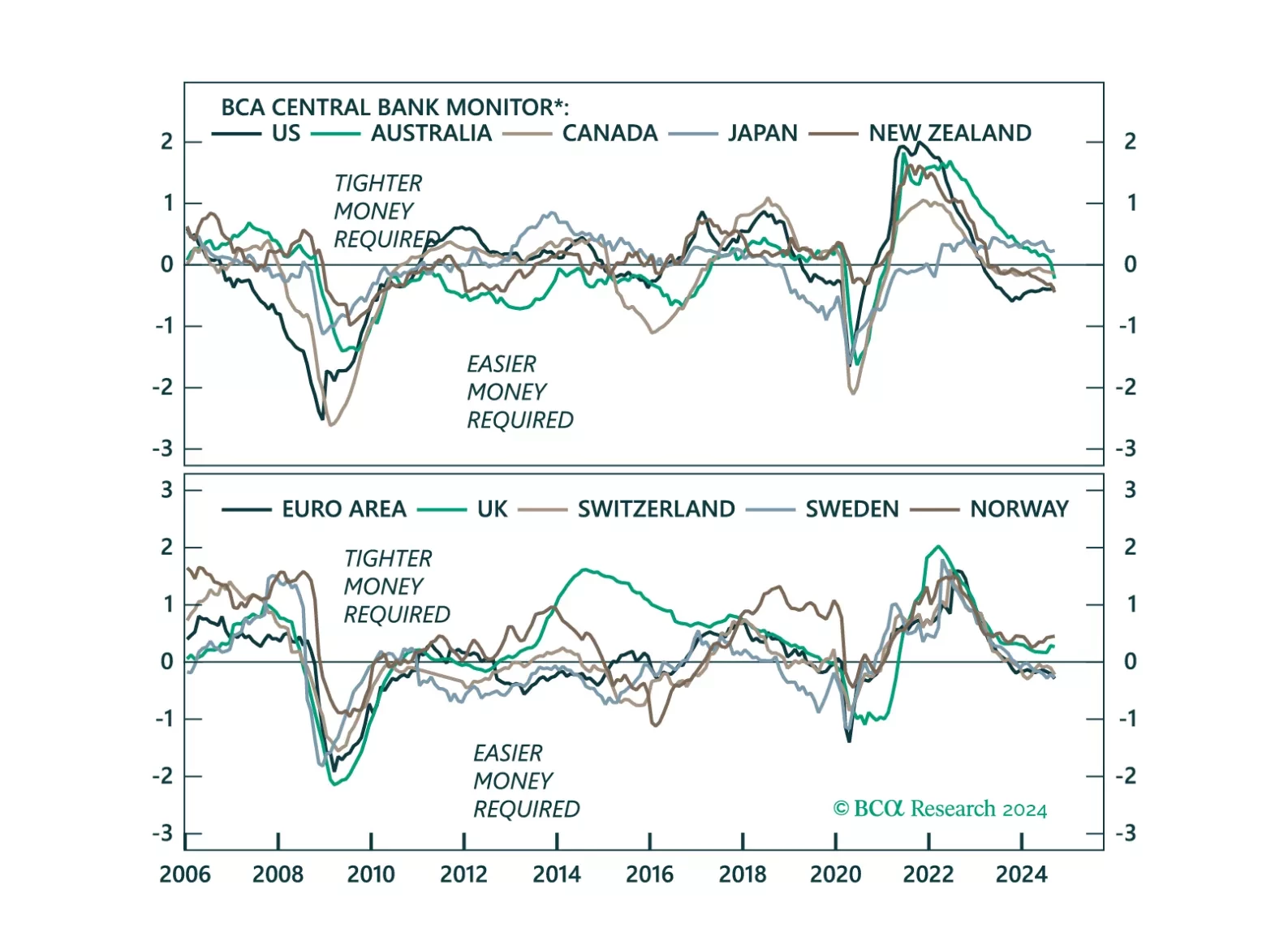

This week, we update our Central Bank Monitors (CBMs), that help us calibrate how monetary policy should be adjusted in developed-market economies. Our conclusion is that while overall, easier monetary settings are required, there a few trade ideas that arise from the divergences in signals amongst G10 countries.

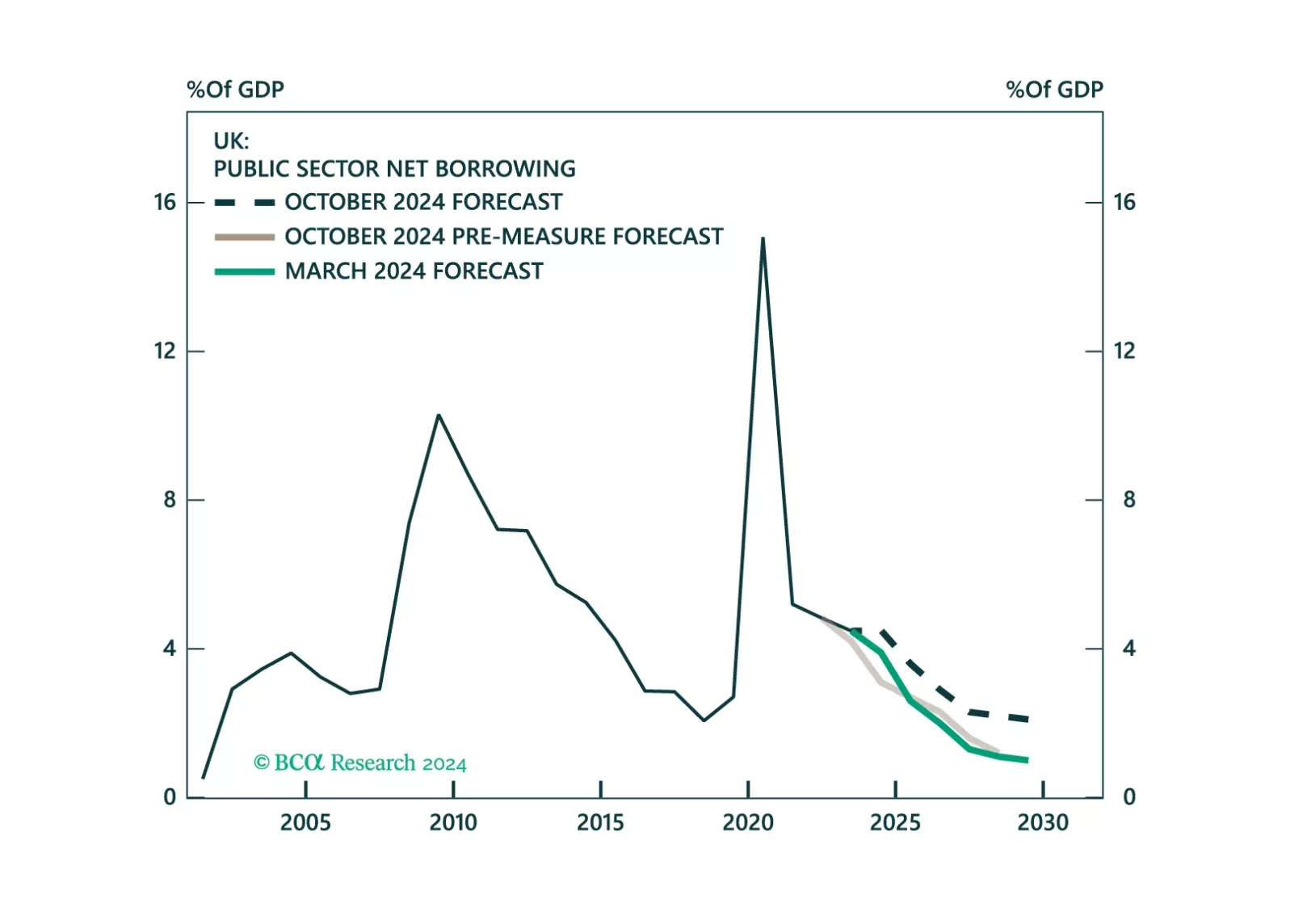

This Strategy Insight presents our view on today’s rate cut by the Bank of England as well as the budget announced by the UK government last week.

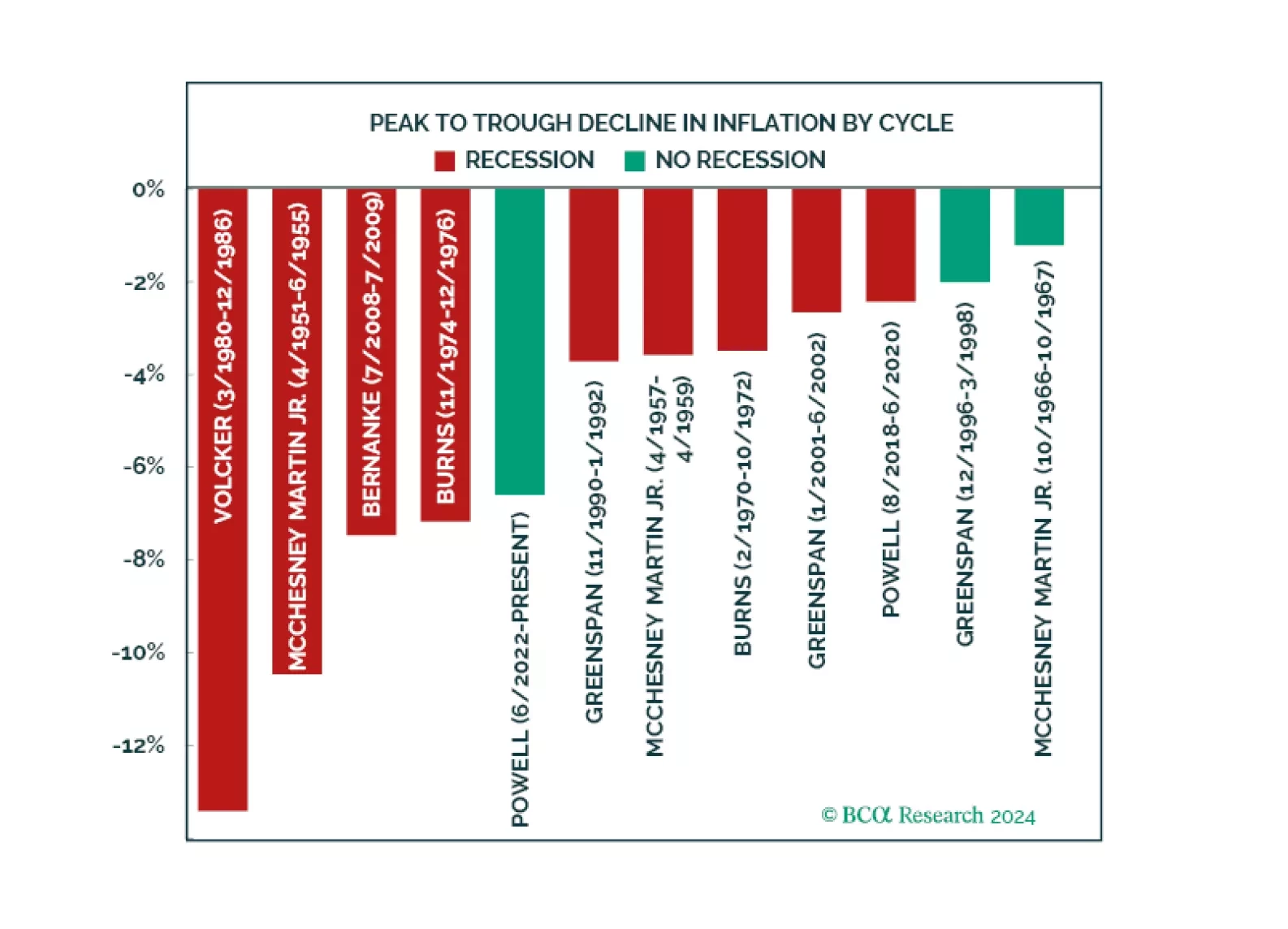

Can Powell achieve a soft landing? There are some indications he is doing it. We examine why our negative stance was wrong and analyze the four growth engines that kept recession at bay. Half of these forces remain while the other half have run out of juice. While this might be enough to keep the economy going, we maintain our defensive positioning. Equities have priced a very benign outcome. Meanwhile, rising rates in anticipation of a Trump win are pushing the economy away from the soft-landing path. We hedge the possibility of further upside in yields in case Trump gets elected by downgrading duration to neutral.