Global

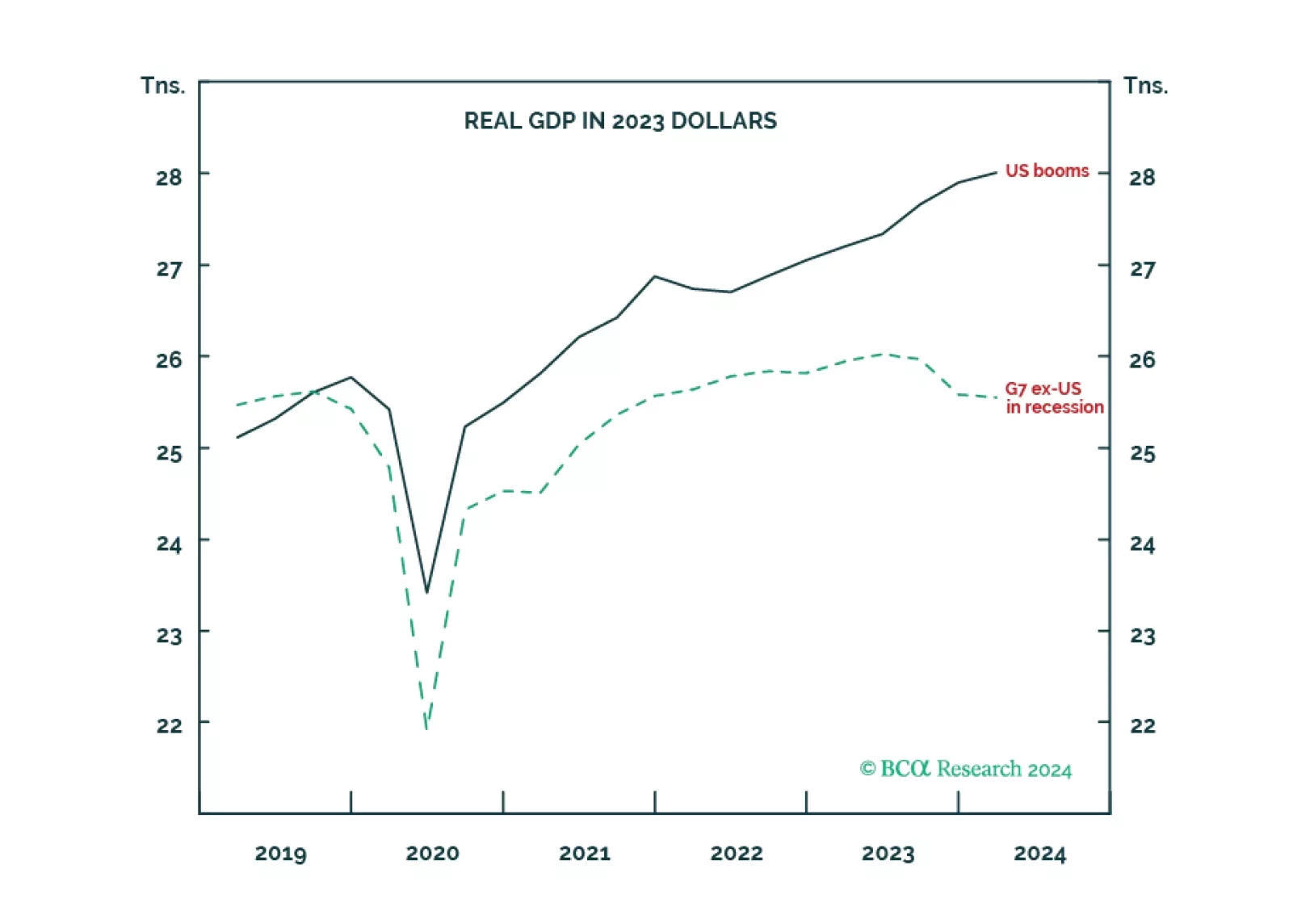

The economic schism in the world economy, between the non-US developed economy in recession and the US in strong growth, is unprecedented during our lifetimes. Now the schism will continue in reverse, as the non-US developed economy rebounds while the US fades. There are important implications for rates, the dollar, and sector and regional equity allocation which we discuss. Plus: base metals are a tactical short.

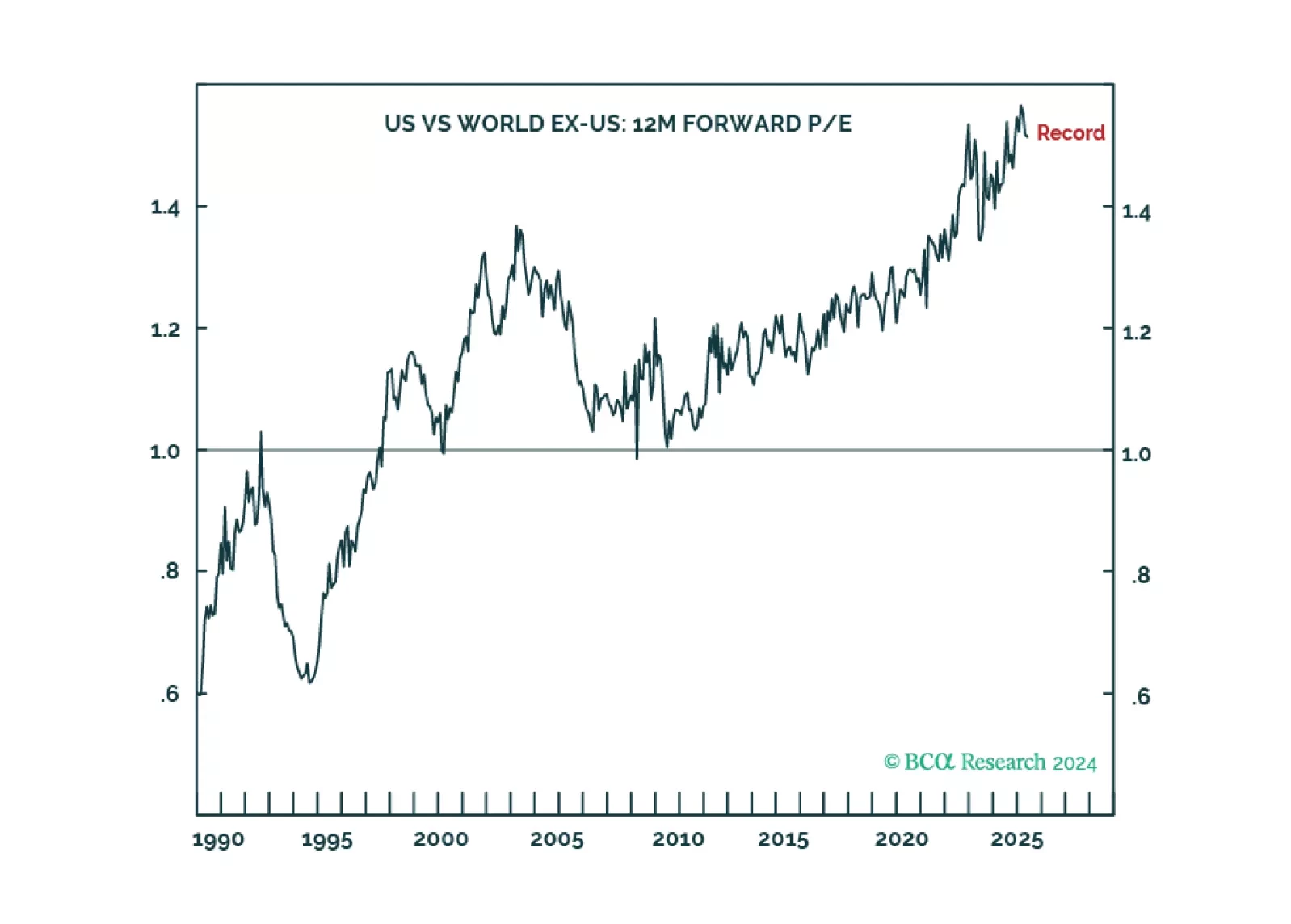

The US stock market’s record 50 percent valuation premium versus the non-US stock market is pricing generative AI to do through the next decade what the Web 2.0 network effect did through the last decade. But this is a huge ask, as it will be very difficult for the Web 2.0 superstar companies to become generative AI superstar companies, assuming there are indeed any lasting generative AI superstar companies. We go through the main long-term investment implications.

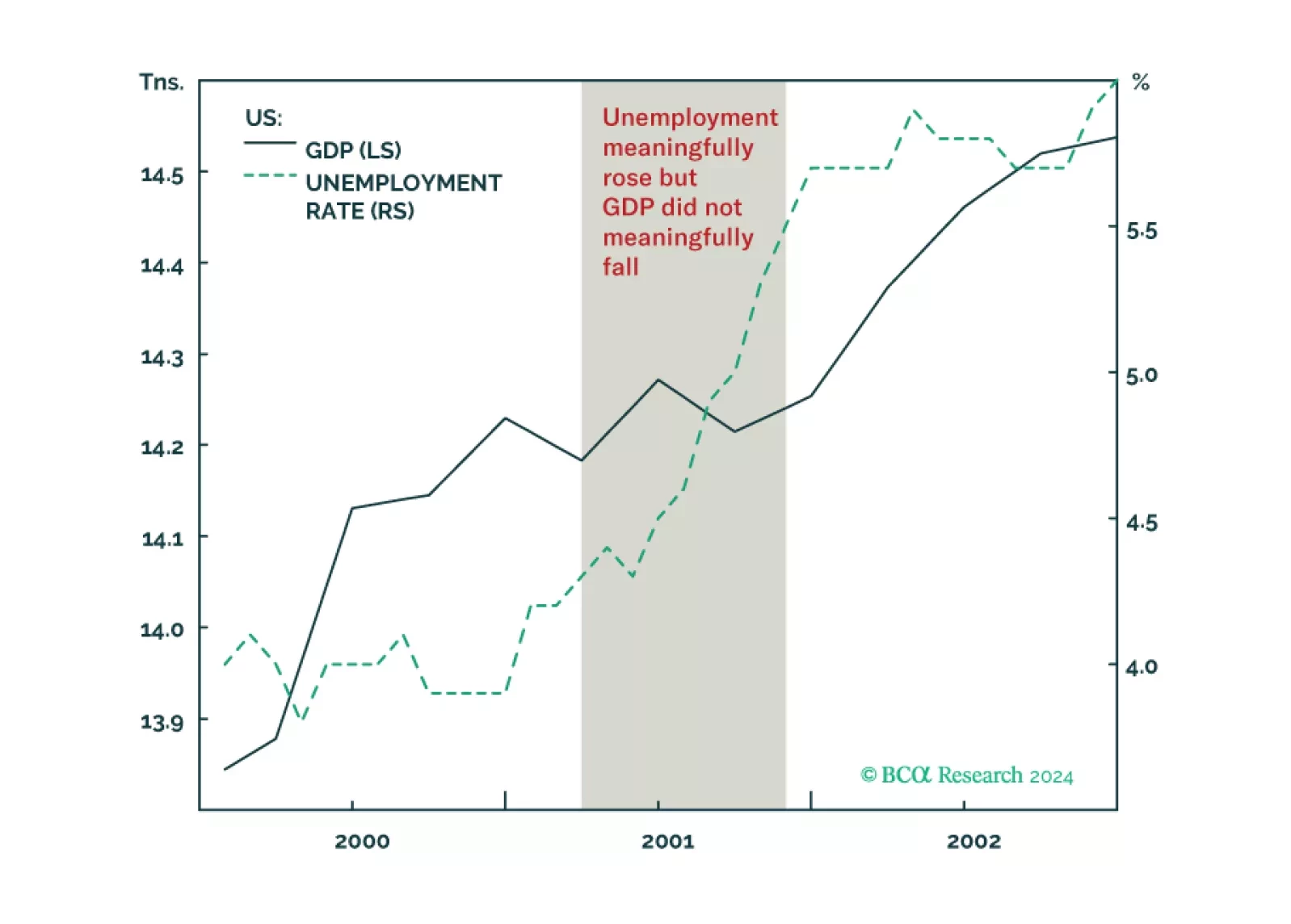

Why the US could get a jobs recession without a GDP recession, as happened in 2001, and what it means for stocks and bonds. Plus, an update on the Joshi rule.