Internet Retail

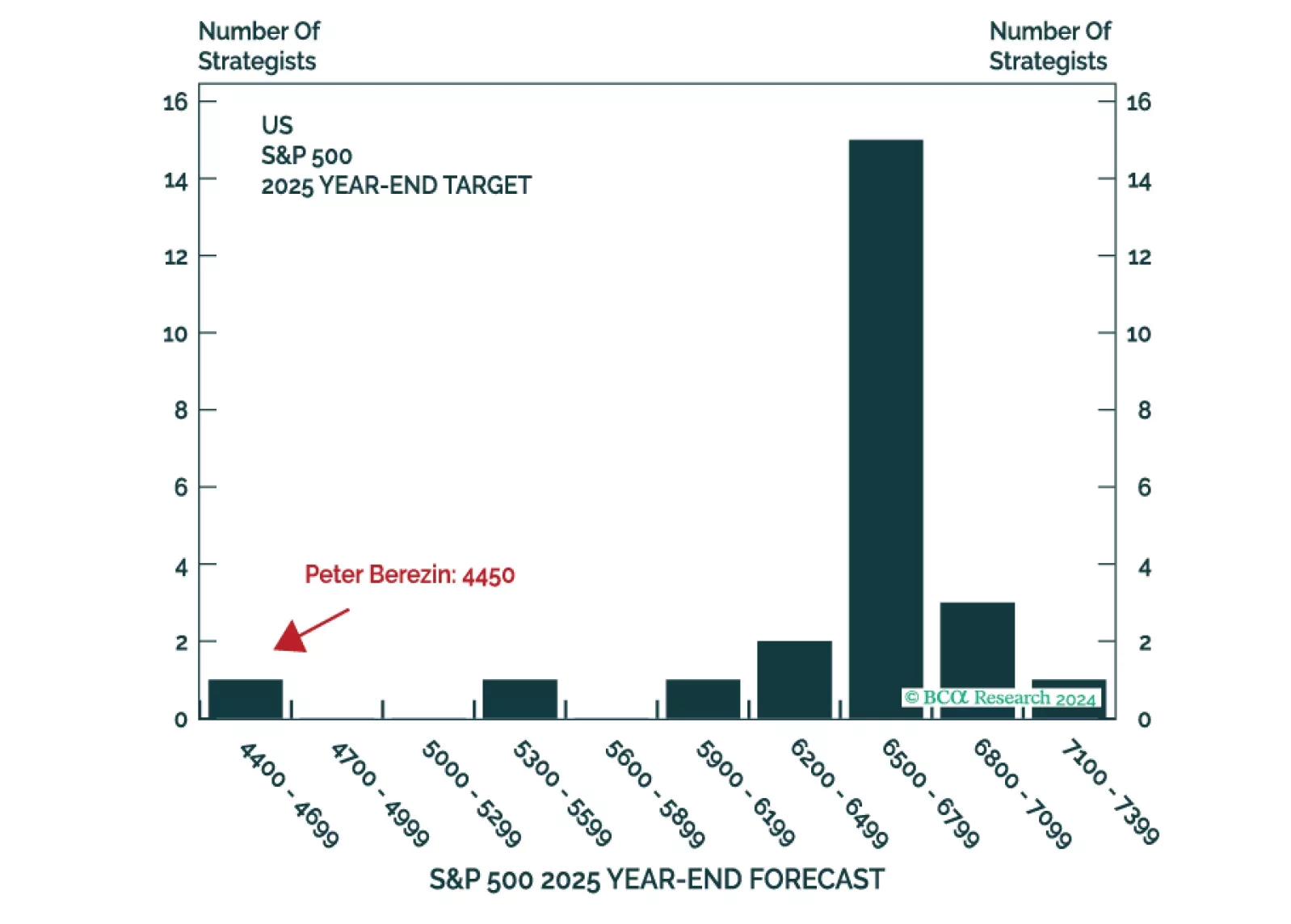

This is the time of the year when strategists are busy sending out their annual outlooks. Here on the Global Investment Strategy team, we decided to go one step further. Rather than pontificating about what could happen in 2025, we decided to harness the power of the multiverse to tell you what did happen (in at least one highly representative timeline).

Next week, please join me for a Webcast on Tuesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets.

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2025. We will be back in the first week of January with our MacroQuant Model Update.

Neutral In mid-April we moved the S&P consumer discretionary sector to the overweight column via upgrading the internet and home improvement retail sub-sectors. While the home improvement retailers hit our stop earlier this month resulting into 15% relative gains, last Friday internet retailers followed suit. We are obeying our previously instituted stop in the S&P internet retail index and crystalizing gains at the 20% relative return mark and downgrade to neutral. This move also pushes the overall S&P consumer discretionary sector to a benchmark allocation, locking in profits of 15% in excess of the broad market over the past five months. Bottom Line: Downgrade the S&P internet retail index to neutral which also pushes our S&P consumer discretionary sector allocation to benchmark for 20% and 15% relative gains, respectively, since the mid-April inception.

In mid-April we boosted the S&P internet retail index to overweight as it was poised to benefit from the shifting consumer spending habits due to the COVID-19 outbreak. True, the “amazonification” of the economy is not a new phenomenon, but COVID-19 acted as an accelerant to an already powerful uptrend in online retail sales (see chart). Today, our overweight in the S&P internet retail index surpassed the 29% relative return mark since the mid-April inception, which compels us to protect profits by instituting a stop at the 20% mark. Bottom Line: We remain overweight the S&P internet retail index, but from a portfolio risk management perspective today we add a stop at the 20% relative return mark in order to protect profits.

Overweight In our April 14 Weekly Report we executed our upgrade alert and boosted the S&P internet retail index to overweight – a call that has since produced handsome relative gains of 14%. The most recent Advance Monthly Retail Trade (AMRT) report also suggests that the path of least resistance remains up for relative share prices. In fact, non-store retailers were the only category that reported an increase in activity on a month-on-month basis, while other categories such as clothing & accessories contracted nearly 80%. Bottom Line: We heed the message from the most recent AMRT report and continue to recommend an above benchmark allocation for the S&P internet retail index. The ticker symbols for the stocks in this index are: BLBG: S5INRE - AMZN, BKNG, EBAY, EXPE.

Overweight In the most recent Weekly Report, we boosted the S&P consumer discretionary index to overweight via upgrading its heavy-weight internet retail sub-index to an above benchmark allocation. E-commerce has been garnering a rising market share of total retail sales uninterruptedly for over two decades. In fact, this juggernaut accelerates during recessions not only because overall retail sales level off, but also because internet sales prove resilient during downturns (see chart). AMZN dominates the internet retail space and by extension the broad consumer discretionary index, especially ever since the media complex migrated to the newly formed S&P communications services index in October 2018. Therefore, as AMZN goes, so goes the rest of the consumer discretionary sector. Time and again we have stressed that when growth is scarce investors flock to industries that exemplify growth. The inevitable rise in online retail sales as a percent of total due to the ongoing pandemic will underpin demand for e-commerce services. Bottom Line: Boost the S&P internet retail index to overweight. The ticker symbols for the stocks in this index are: BLBG: S5INRE - AMZN, BKNG, EBAY, EXPE.

Highlights Portfolio Strategy The Fed’s QE and ZIRP, the collapse in gasoline prices and extremely depressed breadth readings that are contrarily positive, all signal that it no longer pays to be bearish consumer discretionary stocks. A boost in demand for e-commerce, the high-growth profile of internet retailers along with neutral valuations and technicals, all compel us to trigger our upgrade alert and lift the S&P internet retail index to overweight. The rising gap between house price inflation and mortgage rates, the looming increase in residential investment’s contribution to GDP growth and firming industry operating metrics, all argue for an above benchmark allocation in the S&P home improvement retail index. Recent Changes Boost the S&P consumer discretionary sector to overweight today. Execute the upgrade alert and lift the S&P internet retail index to overweight today. Augment exposure to the S&P home improvement retail index to above benchmark today. Table 1 Feature The SPX oscillated violently last week, and a glimmer of good news on the coronavirus fight front, the Fed’s newly announced bazooka and a tick down in unemployment insurance claims all signaled that the bulls have the upper hand. We first showed the Google Trends’ worldwide searches for “coronavirus” series in our early-March Weekly Report,1 when stocks were unhinged and we were still bearish. Now, the most recent update of this indicator suggests that the recessionary lows are likely in for the SPX – this search term peaked a week prior to the overall stock market’s bottom (Google Trends shown inverted, Chart 1) – and we therefore reiterate our cyclically sanguine equity market view.2 Moreover, two weeks ago we highlighted that market internals were confirming the SPX recessionary lows.3 Not only did the SOX versus NDX and small caps versus large caps bottom in advance of the S&P 500, but also transports along with the Value Line Geometric and Arithmetic Indexes relative ratios all led the broad market’s trough.4 Chart 1Joined At The Hip Chart 2Dr. Copper... Importantly, Dr. Copper is also sending a bullish signal for the broad equity market. Economically sensitive copper tends to trough prior to the SPX especially in recessions. Copper collapsed below $2/lb recently leading the SPX by a few days (Chart 2). Similarly, in the recent late-2015/early-2016 manufacturing recession, the 2007/09 and 2001 recessions, copper sniffed out the bottom before the overall equity market troughed (Chart 3). Turning over to the macro backdrop, keep in mind that the Fed first cut rates this year on March 3, 2020, a mere nine trading days following the SPX peak when it fell just below the 10% correction mark. Then, on Sunday March 15, 2020 the Fed cut rates to zero, as the SPX had fallen another 10% into a bear market. Chart 3...Tends To Lead Just to put these moves into perspective, the last time the SPX fell roughly 20% from its peak was on Christmas Eve 2018, and it took the Fed seven months to cut interest rates. While a retest of the 2174 ES futures lows is possible, we would rather not fight the Fed. Instead, we continue to recommend investors deploy cyclically oriented capital in the broad equity market with a 9-12 month time horizon. Chart 4 shows that the Fed is on track to balloon its balance sheet over $11tn in the coming year, i.e. almost trebling it, and soaring to over 50% of GDP. Chart 4Follow The… Beyond the Fed’s QE5 liquidity injection and skyrocketing bank credit, in response to firms tapping existing credit lines, money seems to be growing on trees. M2 money supply growth spiked to 14.8% of late, the highest rate since WWII! This breakneck pace of M2 growth translates into $2tn created versus last year. In the past two weeks alone, M2 grew by $805bn. Deposits and money market funds’ assets are surging, driving the money supply to unprecedented levels. While we have sympathy to some investors’ view that very little of this money and credit will flow to the real economy, such flush liquidity is likely to spillover from the banking system. Asset prices will be the primary beneficiaries of that flood, albeit with a slight lag (Chart 5). Chart 5…Money Trail Meanwhile, we have heeded our research of how to prepare a portfolio from the SPX peak to the recessionary trough highlighted in the Special Report penned in May 2018, and we have been overweight health care and consumer staples (please refer to Table 5 in that Special Report).5 We are now building on the research from that report. Table 2 shows the (unweighted) average relative sector performance six, twelve and eighteen months out from the SPX recessionary troughs, using market cycles since the 1960s. Table 2Sector Winners From Recessionary Recoveries Early cyclicals financials and consumer discretionary along with tech are clear winners in all three periods we analyzed. This empirical evidence confirms the theoretical backdrop that early cyclicals are the first to sniff out a recovery during a recession. At the opposite end of the spectrum, defensive utilities, consumer staples and telecom services fare poorly in the three time frames we examined. Impressively, health care (we are overweight), which is the defensive sector with the largest market cap weight, manages to eke out modest relative gains. Charts 6 & 7 depict these time series profiles for the ten GICS1 sectors (we use telecom services instead of communication services due to lack of historical data). Chart 6Early Cyclicals Rise To The Occasion... Chart 7...But Defensives Lag We are already overweight financials, hence, this week we heed this empirical evidence and are upgrading the S&P consumer discretionary sector to overweight via executing the upgrade alert on the S&P internet retail index and also via augmenting the S&P home improvement retail (HIR) index to an above benchmark allocation. Boost Consumer Discretionary To Overweight… While we may be a bit early, we recommend investors augment exposure to the S&P consumer discretionary index to overweight, today. The Fed really cares about household net worth (HNW). It is a key pillar of consumer spending, which powers over 70% of the US economy. Greenspan in the late 1990s eloquently described this relationship between HNW and the economy. In Q1/2020 HNW will take a beating, but the Fed is making sure it recovers in Q2, and is doing everything in its power to keep the stock and residential real estate markets afloat (roughly 50% of HNW). Granted employment and income are also currently of paramount importance, and the Main Street Fed programs along with the massive fiscal easing package should partially cushion the blow from the looming surge in the unemployment rate. We are therefore comfortable with lifting consumer discretionary to an above benchmark allocation. Chart 8 highlights the inverse correlation between consumer discretionary relative performance and the fed funds rate dating back to the 1980s. Now that the Fed has returned to ZIRP and is on track to expand its balance sheet to over $11tn, the risk/reward tradeoff favors consumer discretionary stocks. Keep in mind household balance sheets have been repaired since the Great Recession with both debt/income and debt/GDP ratios plumbing multi-year lows as the GFC hit the consumer (and financial sector) hardest (bottom panel, Chart 8). Chart 8Buy Consumer Discretionary Stocks Our consumer drag indicator comprising interest rates and oil prices also signals that the path of least resistance for this early cyclical sector is higher (Chart 9). Not only will consumers eventually take advantage of ultra-low interest rates to buy big ticket items on credit, but also a wave of mortgage refinancing at lower rates translates into more cash in consumers’ wallets. Keep in mind that $20/bbl oil also saves US consumers money as retail gas at the pump has now plunged to $1.8/gallon from a recent high of $2.8/gallon. If we are correct and the US economy avoids a Great Depression/Recession, then the swift economic collapse will likely prove transitory as the authorities will have to slowly reopen the economy in early May, and the US consumer will come roaring back in the back half of the year. Finally, sentiment is bombed out toward consumer discretionary equities. Earnings breadth is as bad as it gets, technicals are washed out and a lot of damage has already been done to these interest rate-hypersensitive stocks (Chart 10). True, valuations are a bit extended, but were our thesis to pan out, these early cyclical stocks will grow into their expensive valuations. Chart 9Tailwinds Netting it all out, the Fed’s QE and ZIRP, the collapse in gasoline prices and extremely depressed breadth readings that are contrarily positive, all signal that it no longer pays to be bearish consumer discretionary stocks. Chart 10As Bad As It Gets Bottom Line: Boost the S&P consumer discretionary sector to overweight today from previously underweight, for a modest loss of 1.4% since inception. …Via Executing The Upgrade Alert On Internet Retail To Overweight… E-commerce has been garnering a rising market share of total retail sales uninterruptedly for over two decades. In fact, this juggernaut accelerates during recessions not only because overall retail sales level off, but also internet sales prove resilient during downturns. We are thus compelled to boost the bellwether S&P internet retail index to overweight by executing our upgrade alert to take advantage of the ongoing explosion of internet sales in the face of the coronavirus pandemic (Chart 11). AMZN dominates the internet retail space and by extension the broad consumer discretionary index, especially ever since the media complex migrated to the newly formed S&P communications services index in October 2018. Therefore, as AMZN goes so goes the rest of the consumer discretionary sector. Chart 11Market Share Gains As Far As The Eye Can See AMZN is a retail category killer and the “amazonification” of the economy is not something new as evidenced by the shopping mall evisceration and the dampening of retail sales price inflation. Nearly every segment AMZN has entered it has dominated. The Whole Foods acquisition has also positioned this internet retail behemoth to benefit from an online push for groceries. All of these forces were ongoing prior to the current recession. Now we deem they will accelerate and disproportionately benefit internet retailers at the expense of bricks and mortar retailers: the howling out of the latter is best evidenced by the recent double demotion of Macy’s from the big leagues to the S&P 600 small cap index. Related to the inevitable rise in demand for e-commerce owing to social distancing, growth is a highly sought after attribute that this index enjoys. Time and again we have stressed that when growth is scarce investors flock to industries that exemplify growth (Chart 12). AMZN’s cloud business, AWS, represents another aspect of significant growth, that will remain on an exponential trajectory as more and more businesses move to the SaaS model catalyzed by the current recession. While at first sight this index appears expensive, versus its own history it has worked off previously extreme valuation readings. In more detail, our relative Valuation Indicator has fallen from three standard deviations above the mean back to the historical average. Similarly, despite the recent run-up in prices, relative technicals are only back up to the neutral zone (Chart 13). Chart 12Seek Out Growth… Chart 13...At A Reasonable Price Adding it all up, a boost in demand for e-commerce, the high-growth profile of internet retailers along with neutral valuations and technicals, all compel us to trigger our upgrade alert and lift the S&P internet retail index to overweight. Bottom Line: Execute the upgrade alert and boost the S&P internet retail index to overweight, today. The ticker symbols for the stocks in this index are: BLBG: S5INRE - AMZN, BKNG, EBAY, EXPE. …And Upgrading Home Improvement Retailers To Overweight Home improvement retailers (HIR) were the first consumer discretionary stocks to sniff out the end of the Great Recession, troughing even prior to the China-sensitive materials and industrials equities (Chart 14). As such we believe these economically hyper-sensitive stocks will once again showcase their early cyclical status, and we recommend augmenting exposure to above benchmark. ZIRP along with the rising gap between house price inflation and mortgage refinancing rates are a tonic for home improvement retailers (fed funds rate shown inverted, Chart 14). While the residential real estate market will remain in the doldrums for a few months (we recently monetized impressive gains in our underweight stance in the S&P homebuilding index and lifted to neutral), mortgage holders that retain their jobs will be quick to benefit from lower refinancing rates, and boost their savings. Some of these savings will likely flow into home improvement activities courtesy of the recent quarantine rules. One big assumption is that these retailers remain open during the coronavirus induced lockdown. Chart 14Overweight Home Improvement Retailers… If our thesis pans out, then given the looming drubbing in Q2 GDP, residential investment/GDP should jump and provide a relative boost to the S&P HIR index (second panel, Chart 15). None of this positive news is priced in relative forward sales or profits that are flirting with the zero line (third panel, Chart 15). Importantly, relative valuations have dropped below par and are 30% below the historical mean, offering a compelling entry point for fresh capital with a 12-18 month time horizon (bottom panel, Chart 15). Turning over to industry operating metrics, there is a budding recovery in a number of the indicators we track. Chart 15...As A Play On A Relative Rise In Fixed Residential Investment Chart 16Firming Operating Metrics While it is not very visible in Chart 16, lumber prices have bounced from $275/tbf to over $338/tbf of late, signaling gains for industry relative profits. As a reminder, HIR make a set margin on lumber sales, thus earnings tend to move with the ebb and flow of lumber prices. Moreover, the Fed is resolute to keep the residential real estate market afloat, as we aforementioned, owing to the HNW effect and all these new and old Fed QE policies should underpin the US residential market and by extension lumber prices (Chart 16). Meanwhile, the HIR price deflator has made an effort to exit deflation recently and should also contribute to the sector’s profitability in the coming quarters (Chart 16). Tack on the V-shaped recovery in the HIR sales-to-inventories ratio, albeit from depressed levels, and factors are falling into place for an earnings-led rebound in relative share prices (Chart 16). In sum, the Fed’s ZIRP and QE5, the rising gap between house price inflation and mortgage rates, the looming increase in residential investment’s contribution to GDP growth and firming industry operating metrics, all argue for an above benchmark allocation in the S&P home improvement retail index. Bottom Line: Lift the S&P HIR index to overweight, today. The ticker symbols for the stocks in this index are: BLBG: S5HOMI – HD, LOW. Anastasios Avgeriou US Equity Strategist anastasios@bcaresearch.com Footnotes 1 Please see BCA US Equity Strategy Weekly Report, “From "Stairway To Heaven" To "Highway To Hell"?” dated March 2, 2020, available at uses.bcaresearch.com. 2 Please see BCA US Equity Strategy Weekly Report, ““The Darkest Hour Is Just Before The Dawn”” dated March 23, 2020, available at uses.bcaresearch.com. 3 Please see BCA US Equity Strategy Weekly Report, “What Is Priced In?” dated March 30, 2020, available at uses.bcaresearch.com. 4 Please see BCA US Equity Strategy Daily Report, “Watch The Value Line Geometric Index” dated April 1, 2020, available at uses.bcaresearch.com. 5 Please see BCA US Equity Strategy Special Report, “Portfolio Positioning For A Late Cycle Surge” dated May 22, 2018, available at uses.bcaresearch.com. Current Recommendations Current Trades Strategic (10-Year) Trade Recommendations Size And Style Views June 3, 2019 Stay neutral cyclicals over defensives (downgrade alert) January 22, 2018 Favor value over growth May 10, 2018 Favor large over small caps (Stop 10%) June 11, 2018 Long the BCA Millennial basket The ticker symbols are: (AAPL, AMZN, UBER, HD, LEN, MSFT, NFLX, SPOT, TSLA, V).

In a recent Insight Report ,1 we highlighted the collapse in valuations that were making us grow more constructive on the S&P internet retail index. In fact, sky high valuations were what kept us on the sidelines in the first place in our early-2018 initiation of coverage on the sector.2 That trend has continued into 2019 (second and third panels) and we are compelled to add an upgrade alert to the sector. The timing of such a move may be surprising as for a brief time last week, Amazon (representing roughly 85% of the index) overtook Microsoft as the most valuable public company in the world. However, that title was largely due to Apple’s fall, rather than an Amazon rally; importantly, Amazon’s stock is off roughly 20% from when it breached the $1 trillion market cap mark in September, 2018. However, as we have noted in the past, the dominance of one stock in this index introduces a greater degree of specific risk and hence volatility in our valuation measures, which we view as less reliable than usual. Accordingly, we would wait until valuations deliver a more convincing narrative before catalyzing our upgrade alert. The ticker symbols for the stocks this index are: BLBG: S5INRE - AMZN, BKNG, EBAY, EXPE. 1 Please see BCA U.S. Equity Strategy Weekly Report, “The Amazonification Of Internet Retail,” dated October 17, 2018, available at uses.bcaresearch.com. 2 Please see BCA U.S. Equity Strategy Special Report, “ Internet Retail: Dialed Up” dated February 26, 2018, available at uses.bcaresearch.com.

Neutral In our recent initiation of coverage on the newly minted Communication Services sector, we examined the impact of a variety of technology and consumer discretionary stocks being pulled together to form a new GICS1 sector.1 One sector that saw some important changes was the S&P internet retail index, a sub-sector of consumer discretionary, with Netflix and TripAdvisor moving out and eBay moving in. Our thesis of continued elevated profit growth being offset by sky-high valuations is unchanged by these moves, though there are two important developments. First, the moves are not equal from a market cap perspective and the stocks moving out are much larger than the one moving in. The upshot is that Amazon goes from 75% of the index to 85% now, meaning that little else matters than that sole equity to an even greater extent. Thus, the second development is Amazon’s 12% share price pullback this month which has made the sky-high index valuation look less-so (second and third panels). Our take is that the decreased diversification has added specific risk that should naturally increase the index’s volatility and, accordingly, our valuation and technical indicators are less reliable. As such, we are maintaining our benchmark allocation recommendation, though we are growing more constructive as the valuation declines. The ticker symbols for the stocks this index are: BLBG: S5INRE - AMZN, BKNG, EBAY, EXPE. 1 Please see BCA U.S. Equity Strategy Special Report, “New Lines Of Communication” dated October 1, 2018, available at uses.bcaresearch.com.

One sector that saw some important changes was the S&P internet retail index, a sub-sector of consumer discretionary, with Netflix and TripAdvisor moving out and eBay moving in. Our thesis of continued elevated profit growth being offset by sky-high…