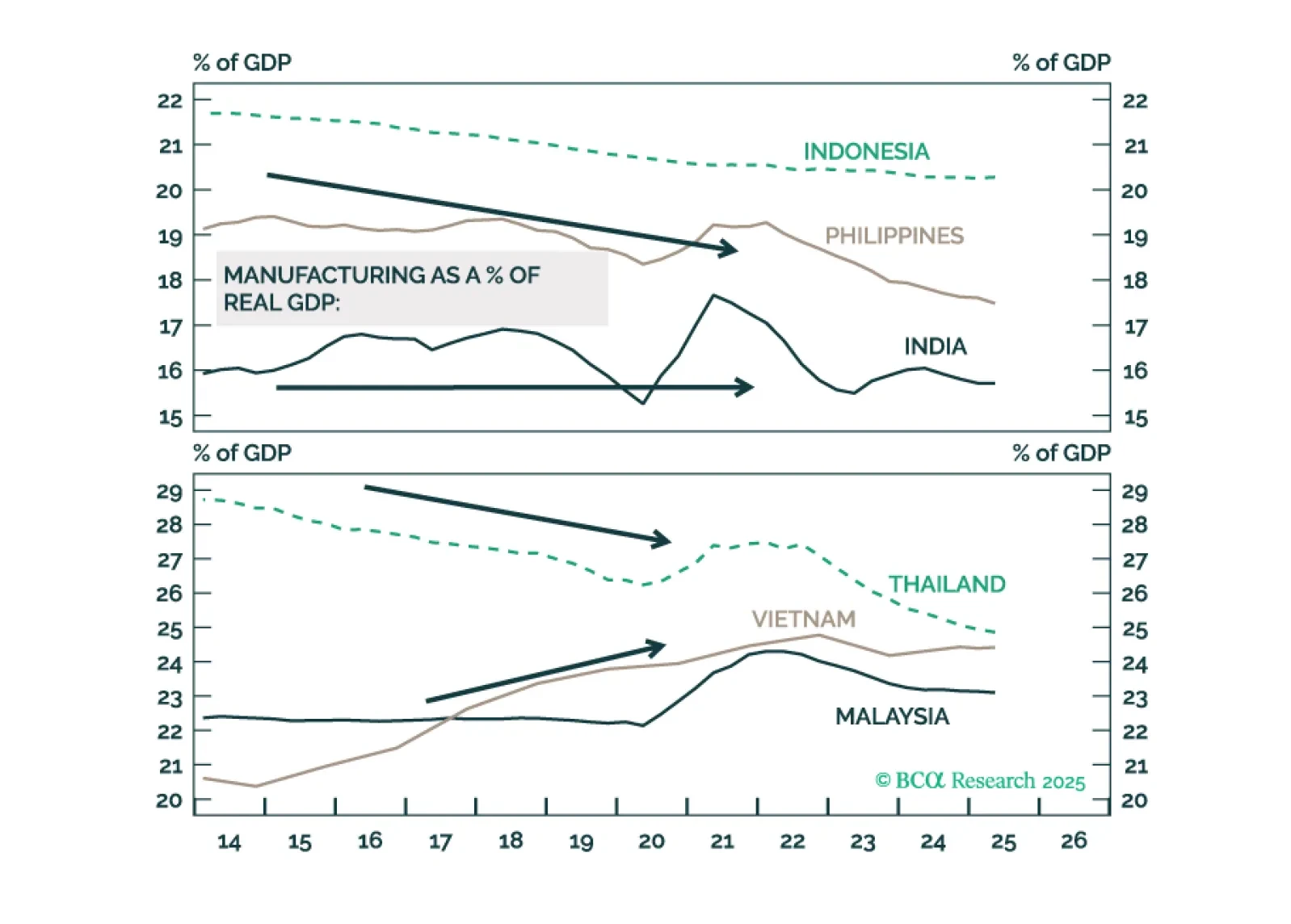

Manufacturing

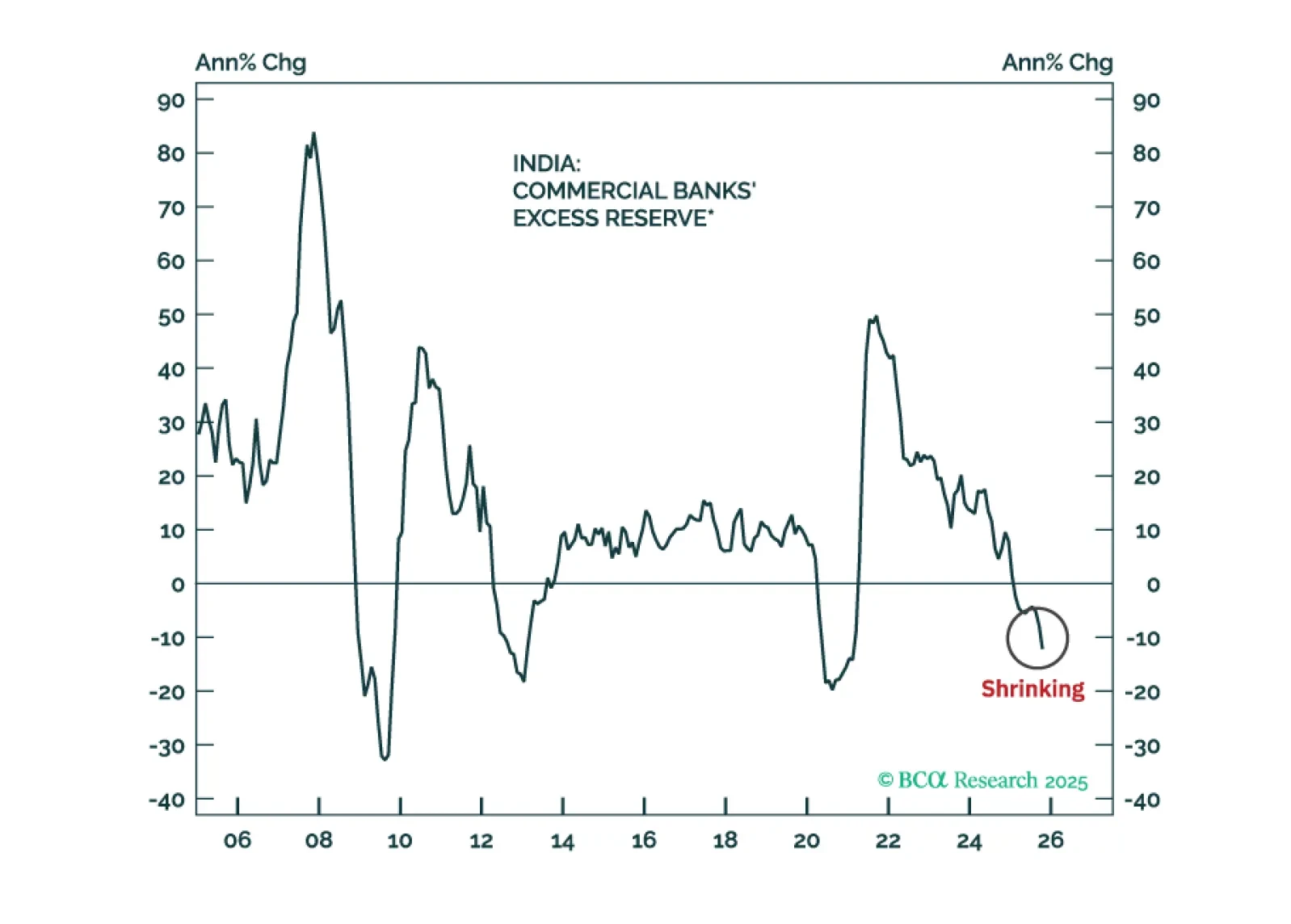

Indian stocks have further downside in absolute terms as profits disappoint. Their underperformance versus the EM equity benchmark, however, is late, which warrants a shift from underweight to neutral allocation.

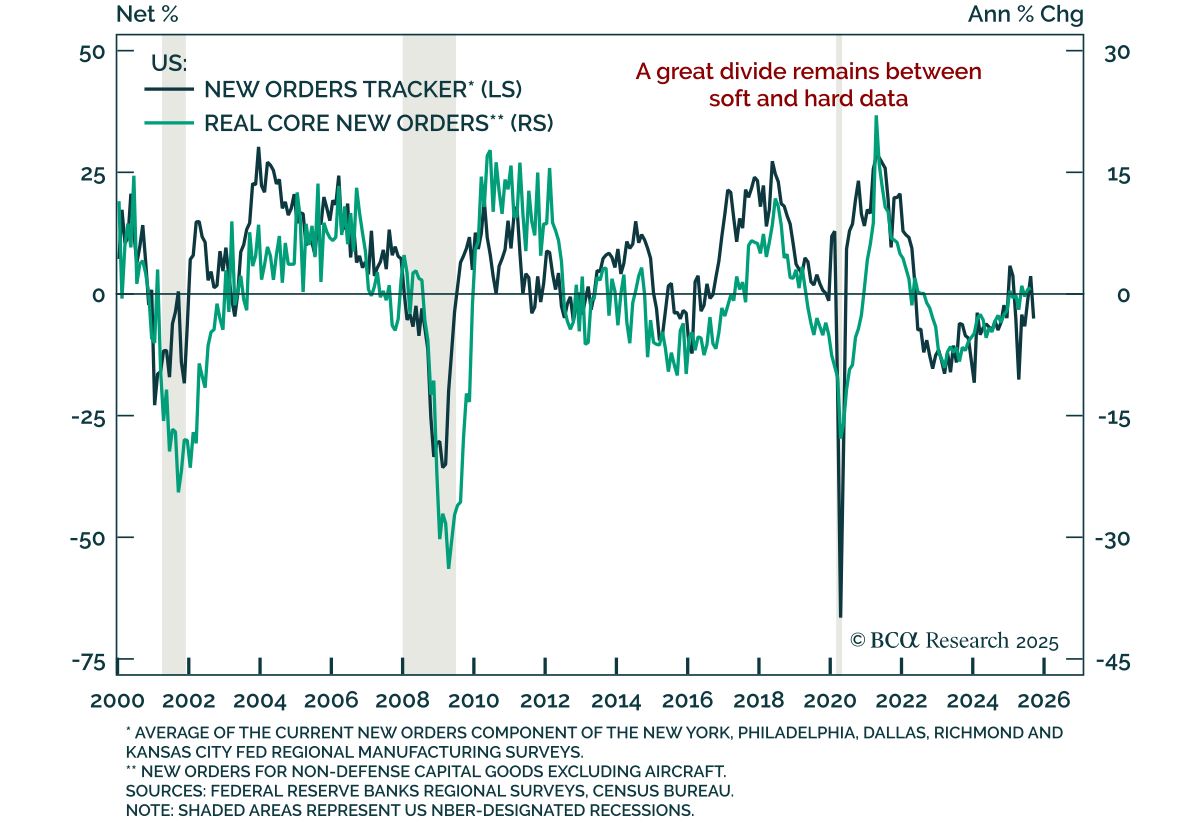

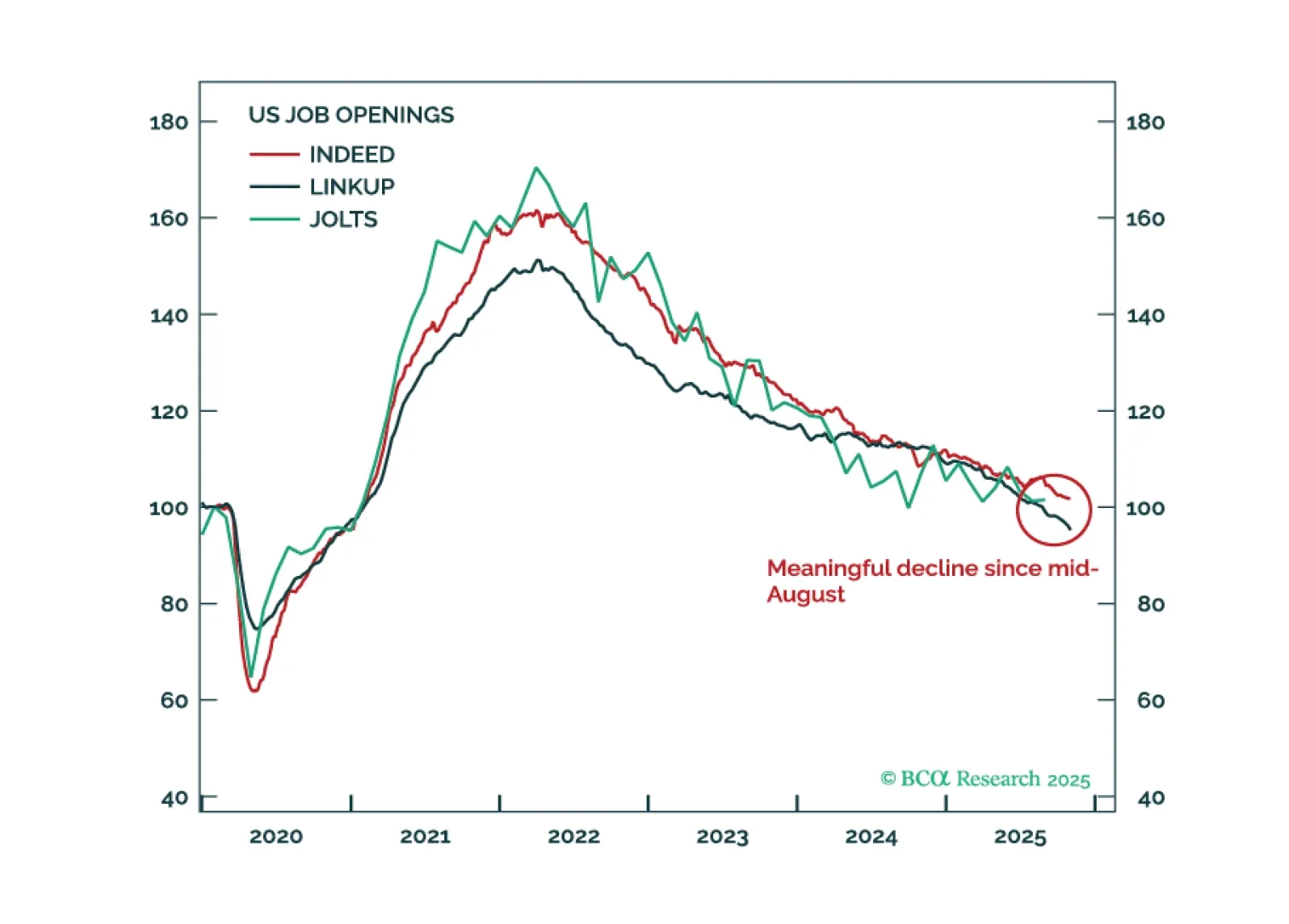

In the absence of official government data, investors are turning to alternative sources to gauge the direction of the US economy. Our analysis of this data suggests that the economy has continued to expand at a moderate pace over the past two months. If the Supreme Court were to strike down the tariffs, this would reduce the near-term odds of a recession while raising the odds of overheating.

Investors should not count on buoyant growth in the ASEAN and Indian economies because of manufacturing relocation away from China in the next couple of years.

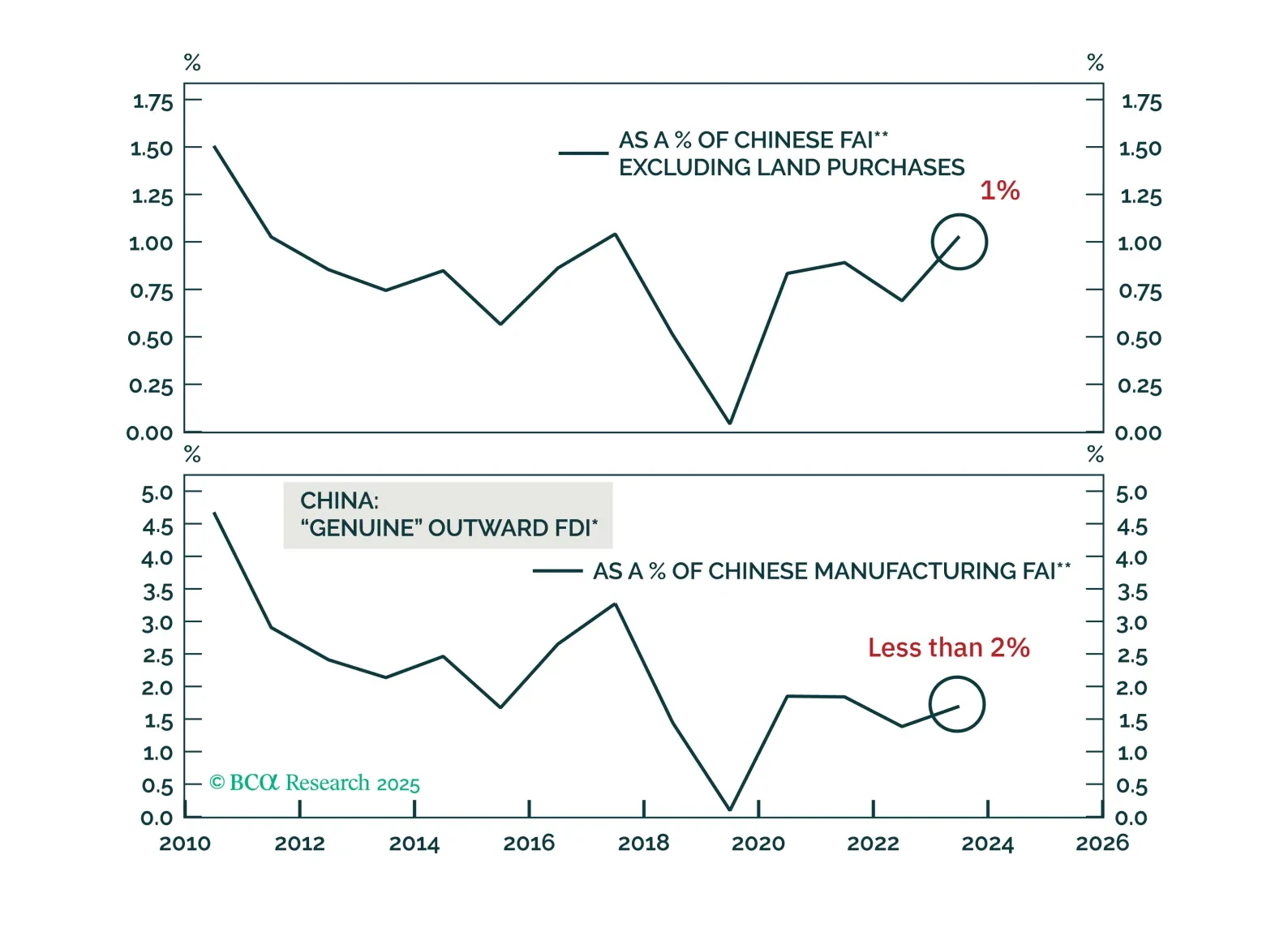

With Sino-US tensions flaring up again, will Chinese manufacturers accelerate their overseas capacity shift? In this Special Report we examine China’s manufacturing offshoring through multiple lenses and tackle the key questions shaping its next phase.