UK

This report looks at the FX implications of the Trump tariffs, and the review of our Q1 trades.

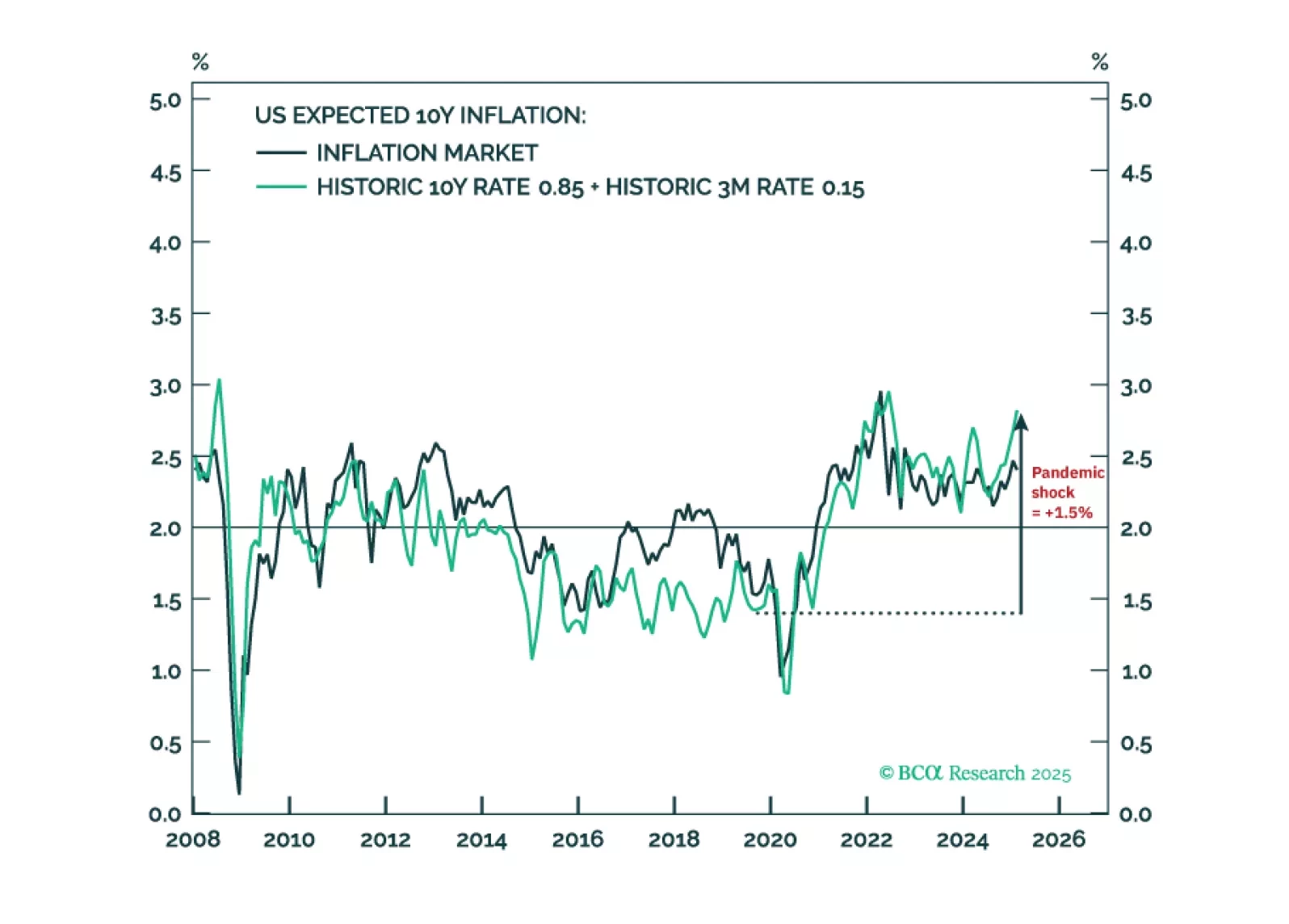

Tariffs will make a difficult job almost impossible. Hitting and sustaining a precise 2 percent inflation target is more about luck than judgement. It requires both the starting point for inflation expectations and any inflation/deflation shock to combine perfectly to 2 percent. While structural inflation expectations in the euro area and Japan could be close to 2 percent, those in the US and the UK will be stuck uncomfortably above 2 percent. We discuss the investment implications for rates and FX. Plus: gold is vulnerable to a tactical reversal.

With economic headwinds building and fiscal dynamics shifting, bond markets are at a turning point. Our latest note outlines why German bund yields are set to decline and why UK gilts are poised to outperform — and how to position accordingly.

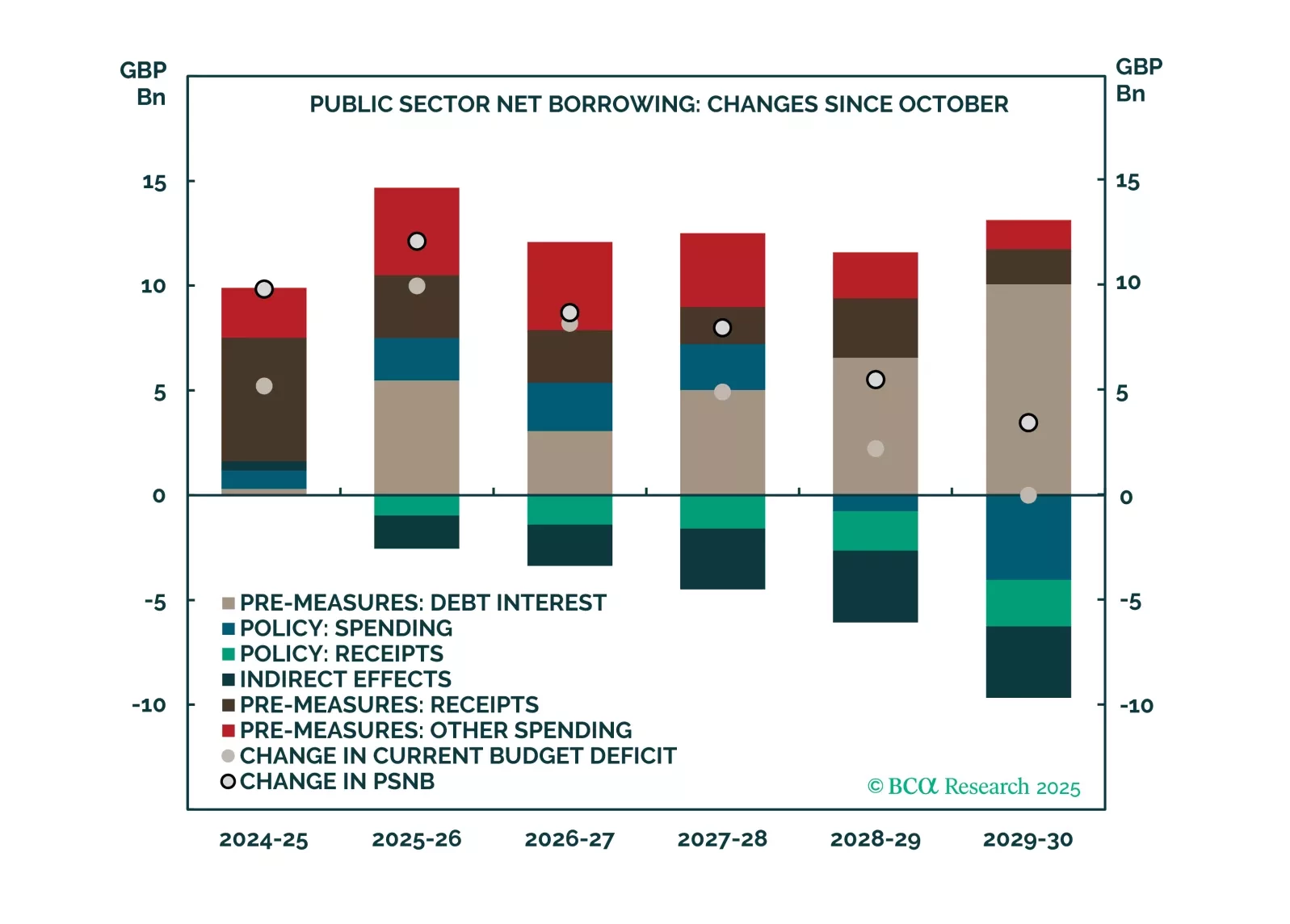

This report is a quick take on our views on UK bonds and FX, given the recent budget.

Given the meetings between the Bank of Japan, the Bank of England, and the Swiss National Bank, our highest convictions views are:

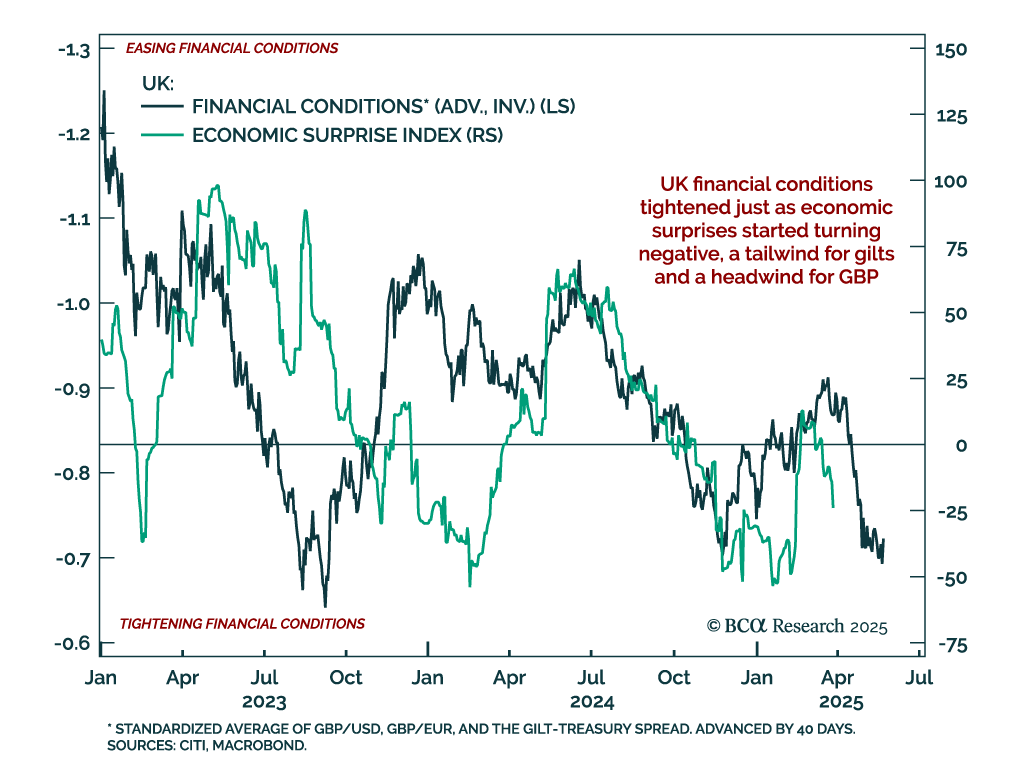

Overweight UK Gilts. It is also time to sell sterling. We are short sterling, as of 1.30.

Underweight JGBs. Correspondingly, be long the yen.

A short CHF/JPY position remains a core holding. Selling GBP/JPY is also a great trade.

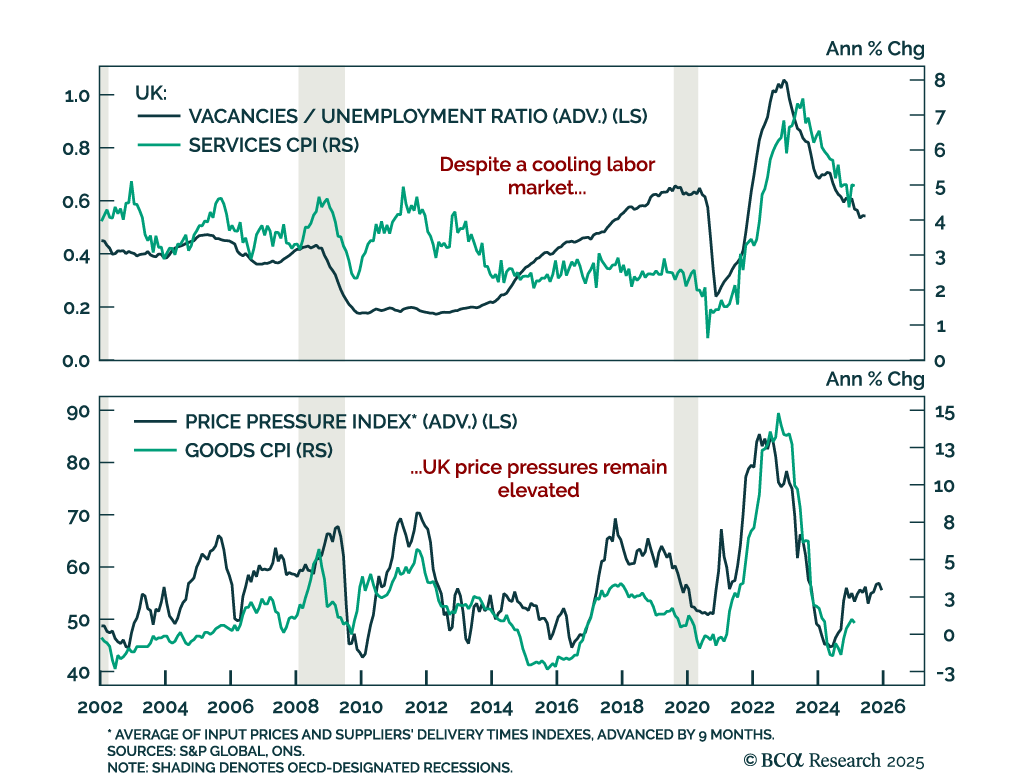

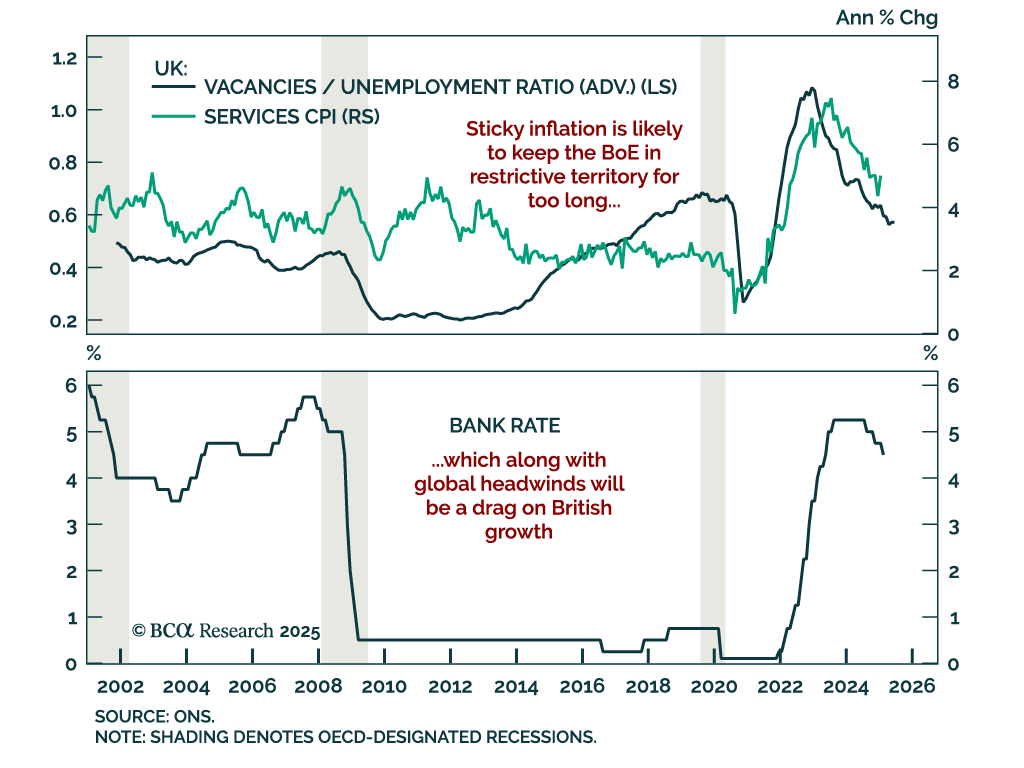

The US (and the UK) is staring down the barrel of a ‘mini-stagflation’ until a deflationary shock arrives to neutralise it. We describe a likely source for the deflationary shock and list three investment conclusions that are valid irrespective of how long it takes for the deflationary shock to arrive. Plus: RCI.B is deeply oversold and ripe for a rebound.