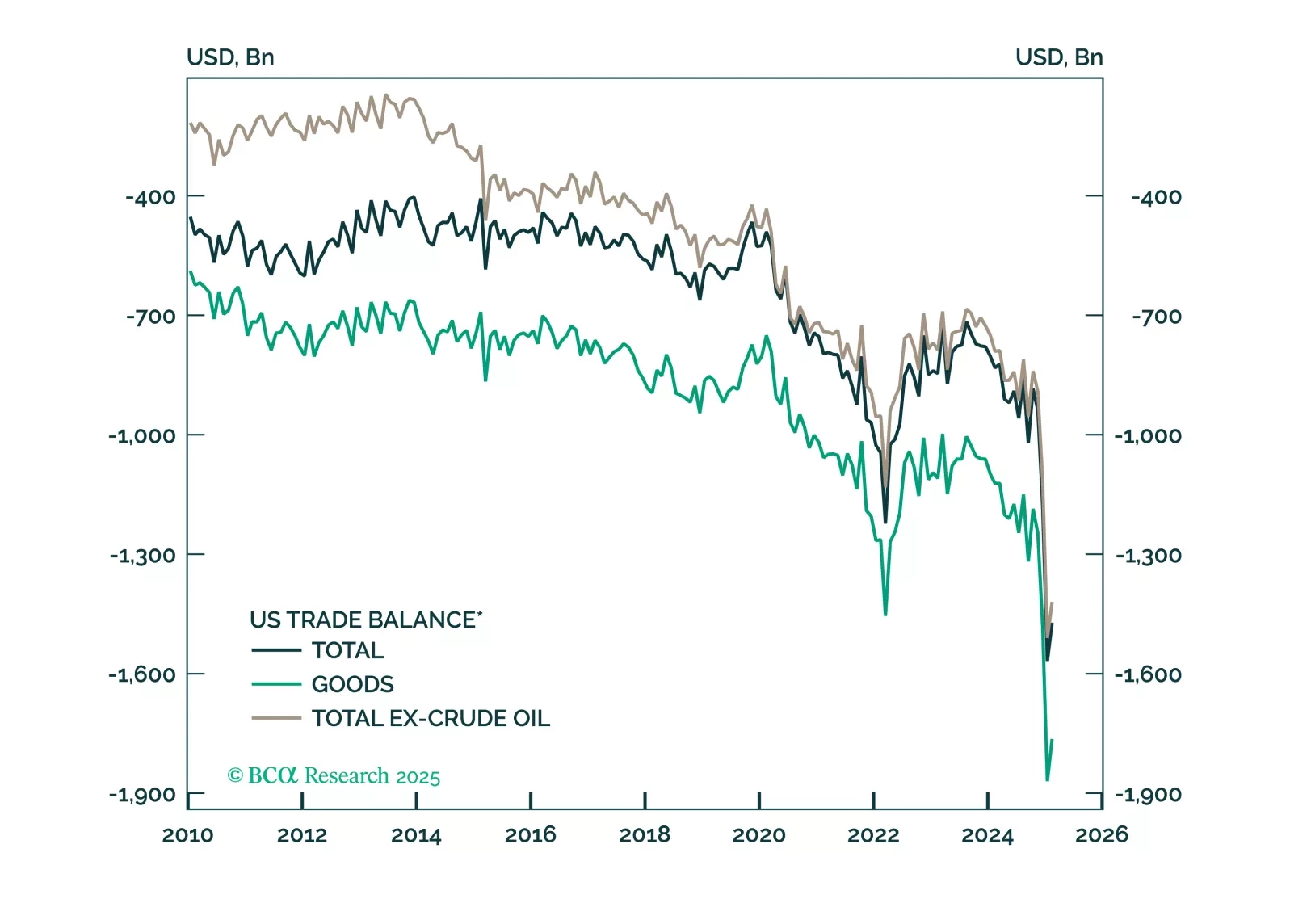

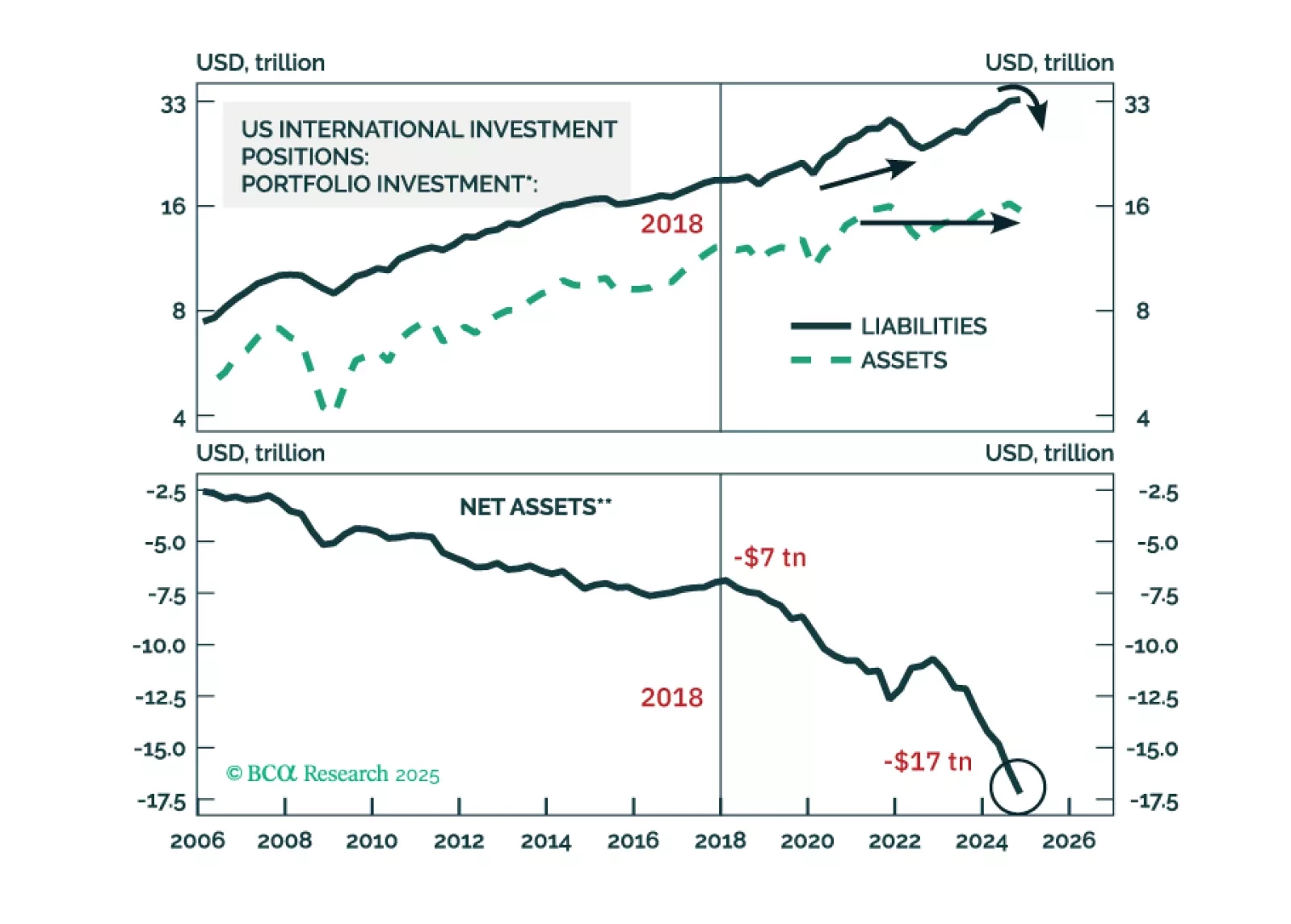

US Dollar

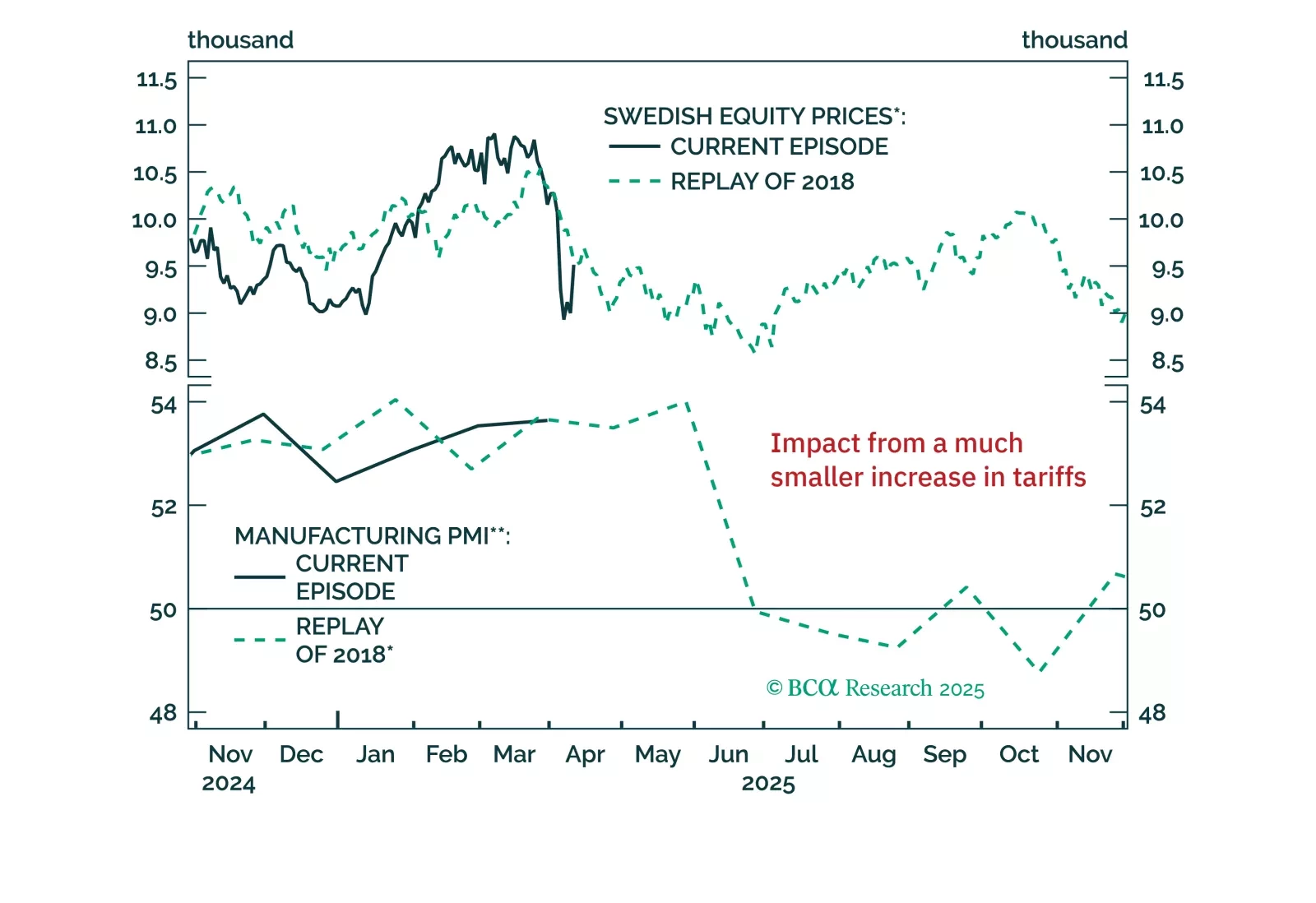

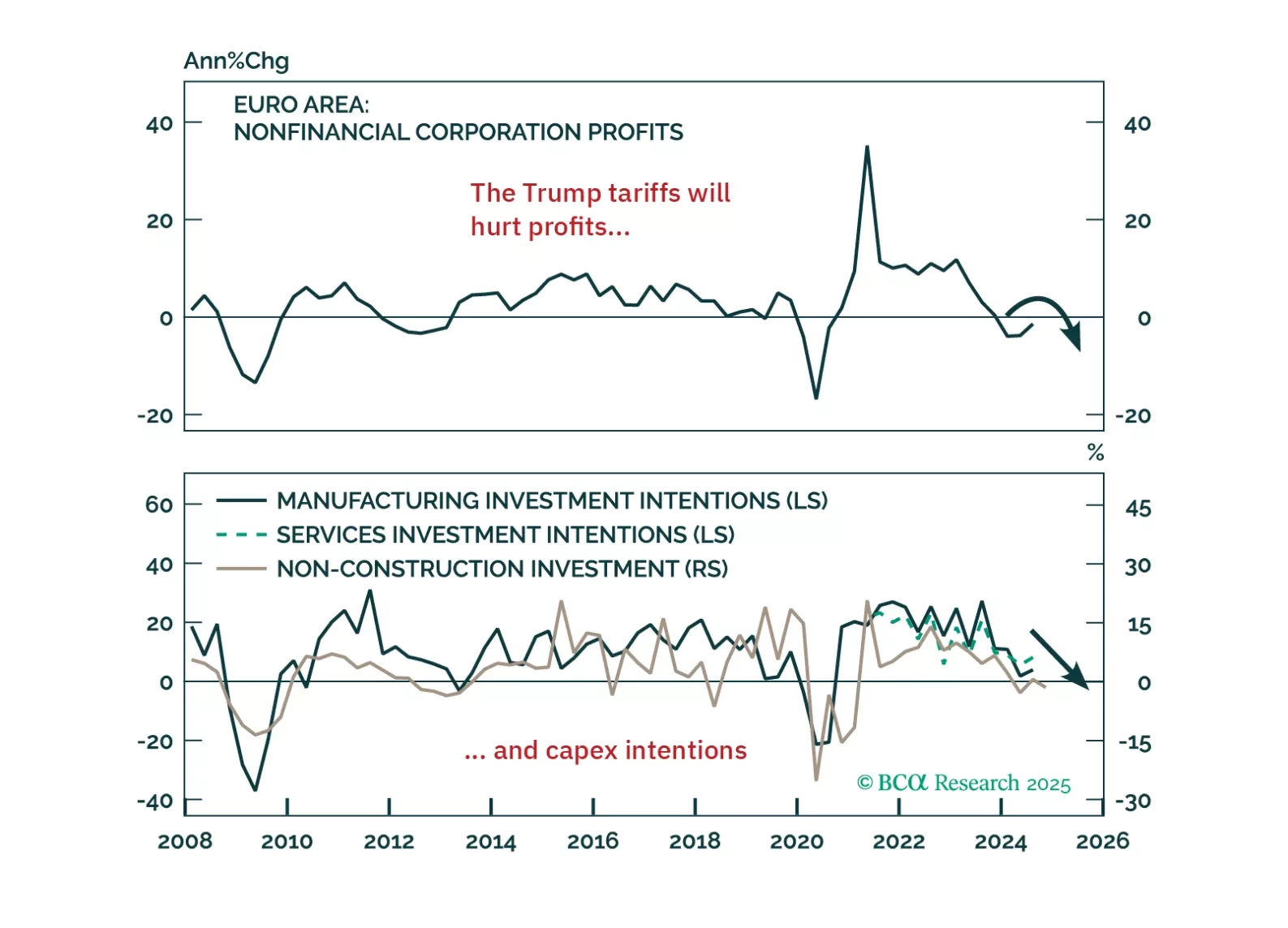

Europe’s near-term outlook remains clouded by uncertainty, even after the tariff reprieve. Our latest update breaks down why the risks to growth, profits, and financial conditions are still skewed to the downside — with Sweden standing out as a key bellwether.

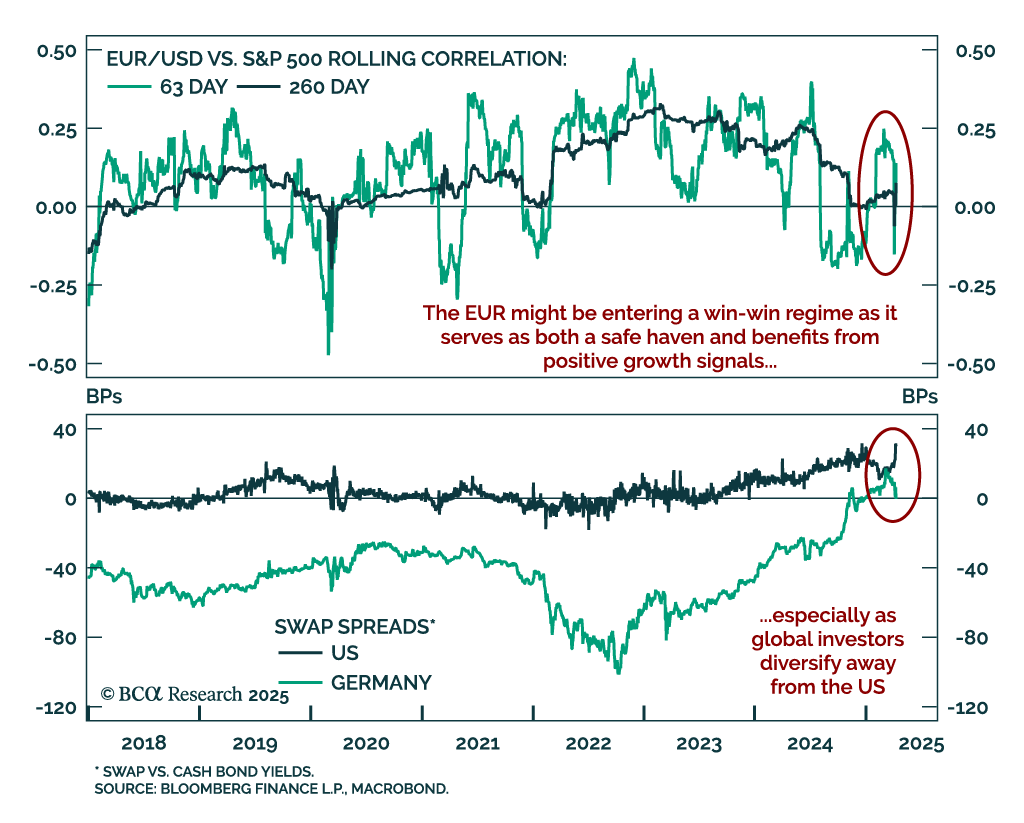

Trump’s tariff shock will push Europe into recession — but it’s also triggering a powerful integration response. In this report, we lay out the tactical case for staying defensive and the structural case for going long European assets when the dust settles.

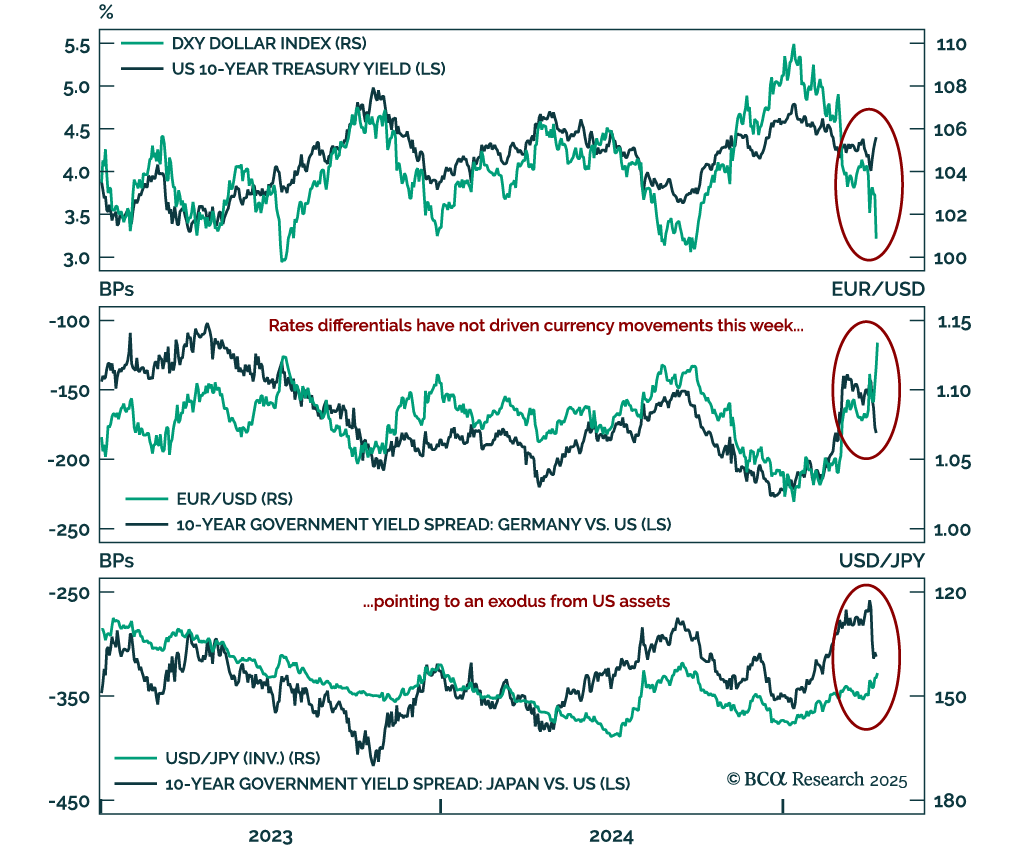

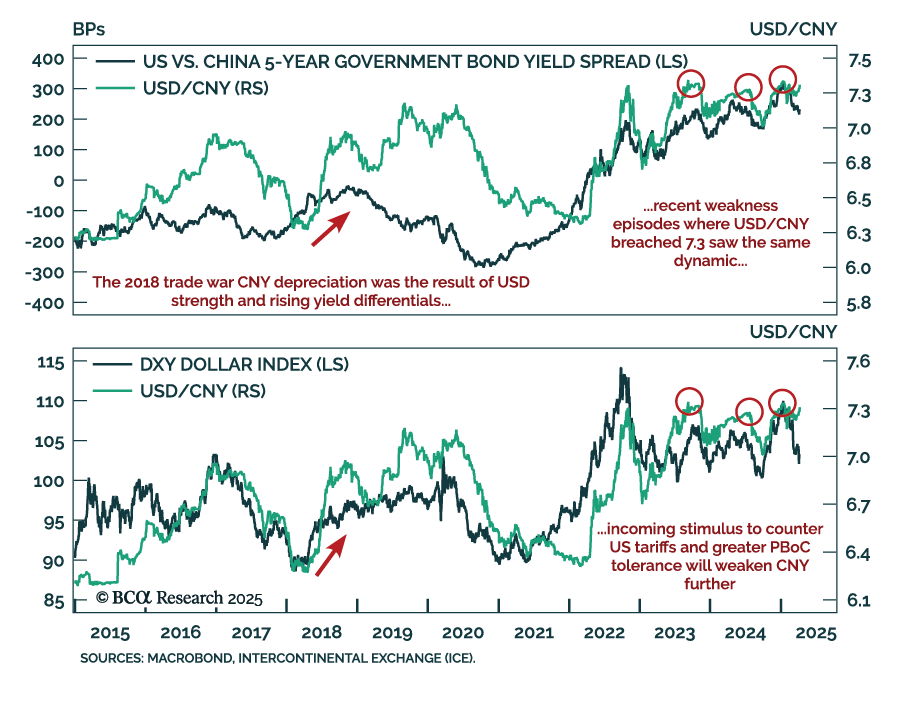

This report looks at the FX implications of the Trump tariffs, and the review of our Q1 trades.

On the one hand, US tariffs are much more deflationary for the rest of the world than for the US, so interest rate differentials might move in favor of the US dollar in the near term. On the other hand, portfolio outflows from the US will weigh on the greenback over a cyclical horizon. We recommend buying Mexican and Central European domestic bonds.

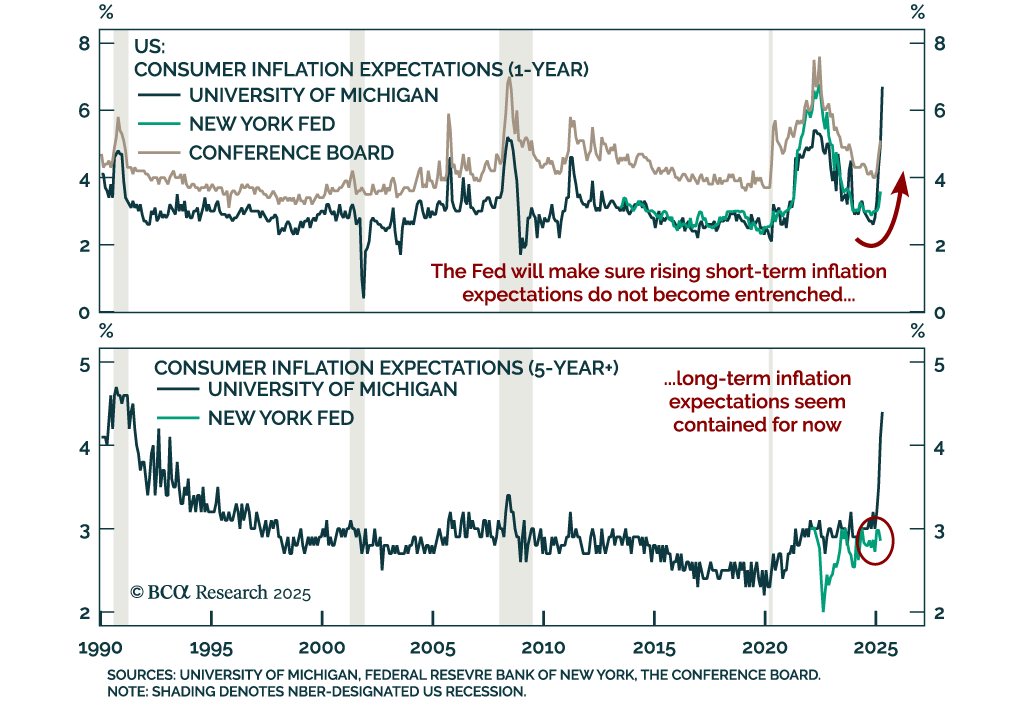

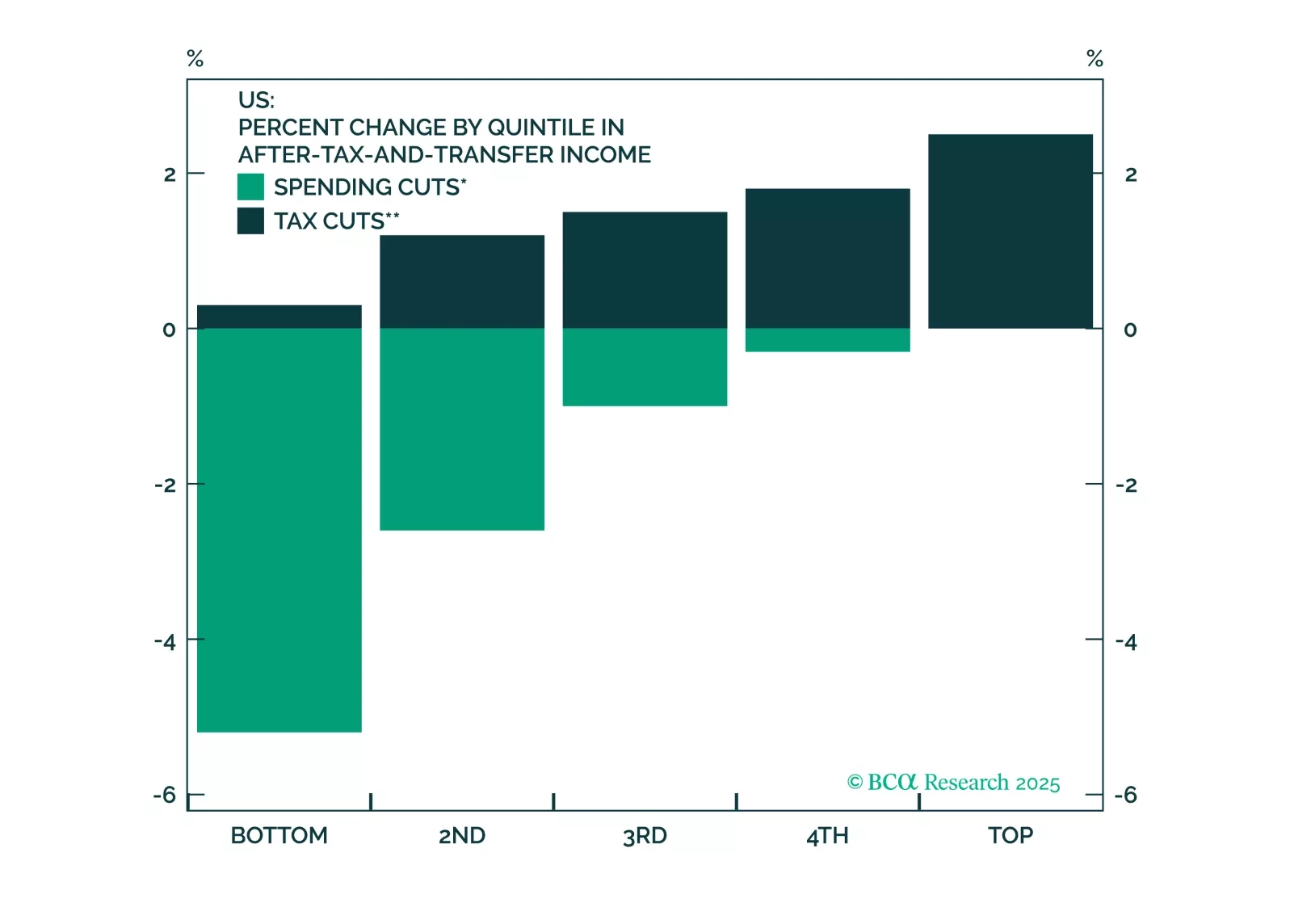

Stocks will continue to struggle in the second quarter as President Trump tries to implement tariffs. Tax cuts will only temporarily dispel growth fears, if at all. Middle Eastern instability will add oil price surprises to an environment that is looking fairly stagflationary.