US Dollar

In this Second Quarter Strategy Outlook, we explore the major trends that are set to drive financial markets for the rest of 2025 and beyond.

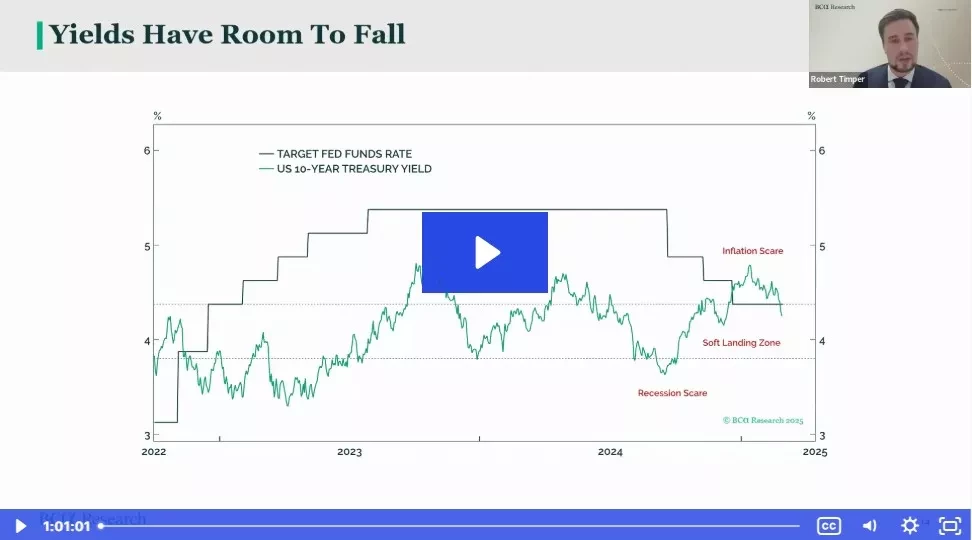

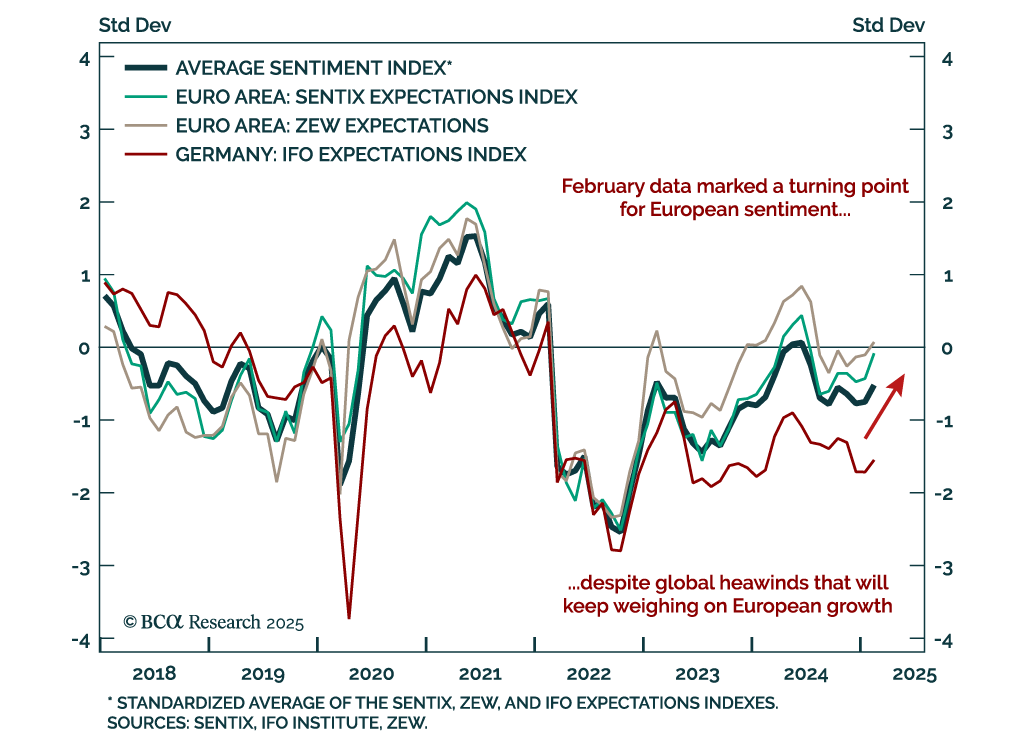

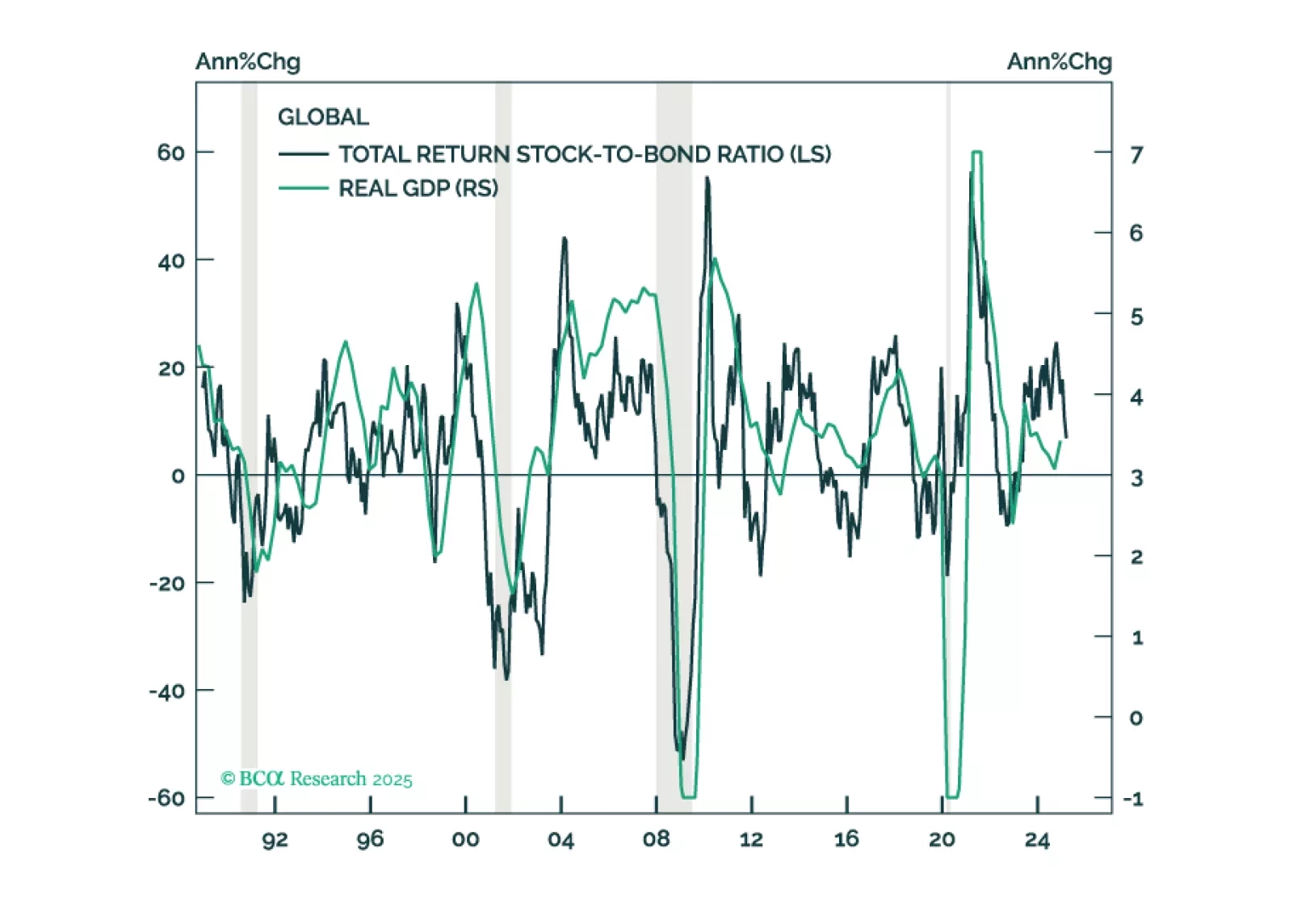

This report presents our interpretation of signals from the main equity, bond, and currency markets around the world. The key takeaways are: (1) Chinese stocks are behind the resilience of the EM MSCI Index; (2) Investors have become too bullish on Europe and will be disappointed; (3) The US dollar will likely rebound in the near term; (4) US long-term bond yields will be sticky in the short run; (5) The global equity selloff is not over.

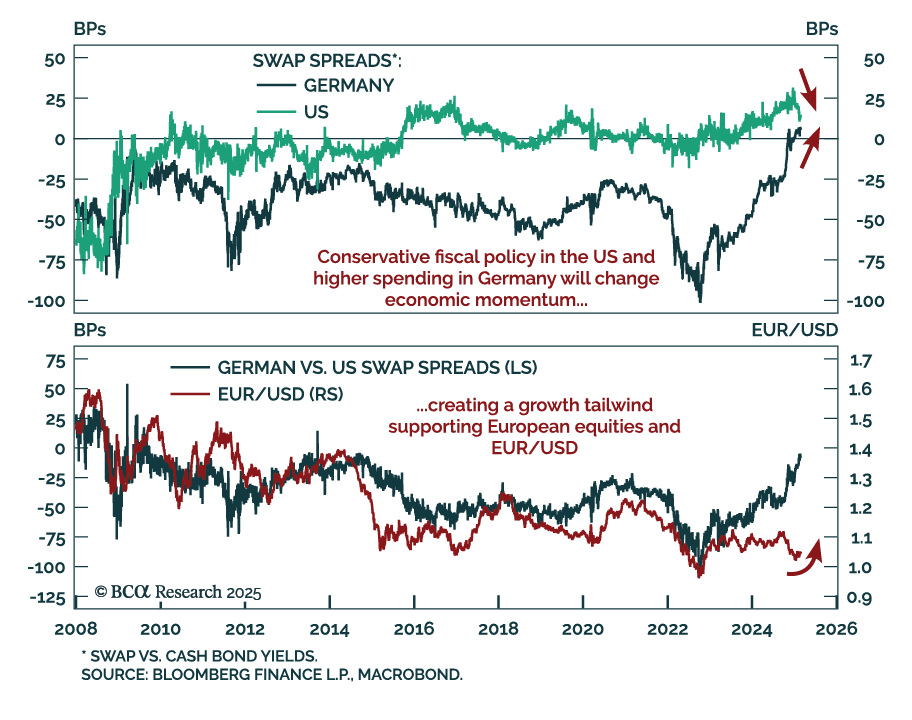

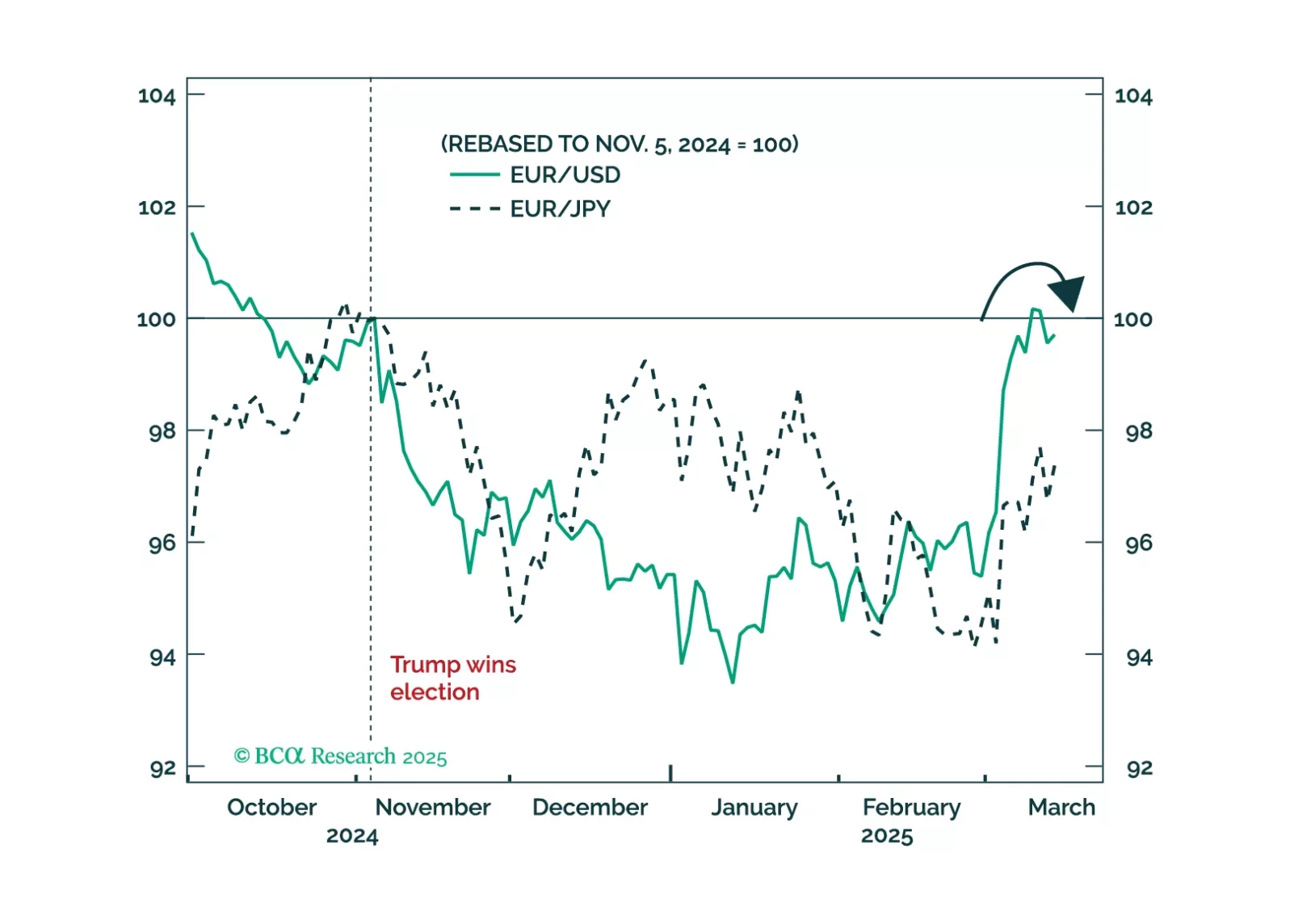

Trump’s foreign policy can be explained by rational US interests, but it requires settling the trade war with allies sooner rather than later. Book gains on EUR-USD for now.

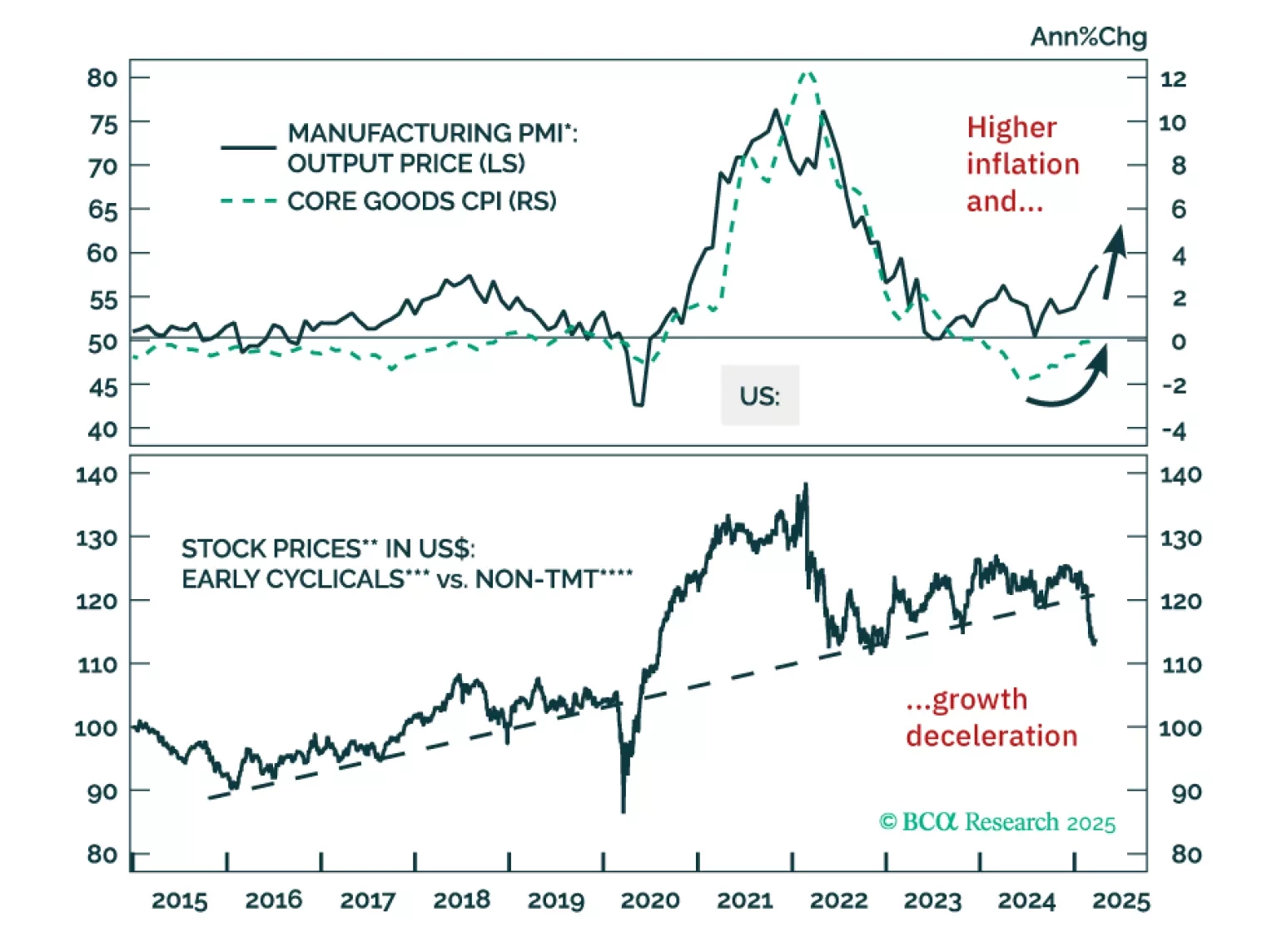

Notwithstanding periodic short-term rebounds, the path of least resistance for global share prices remains down. The resilience of European and Chinese stocks in the face of the US equity selloff is unsustainable. These economies will deteriorate as US demand – the sole pillar of global growth in the past two years – vanishes and tariffs bite. A new currency trade: go long MXN / short an equal-weighted basket of CAD and the euro.

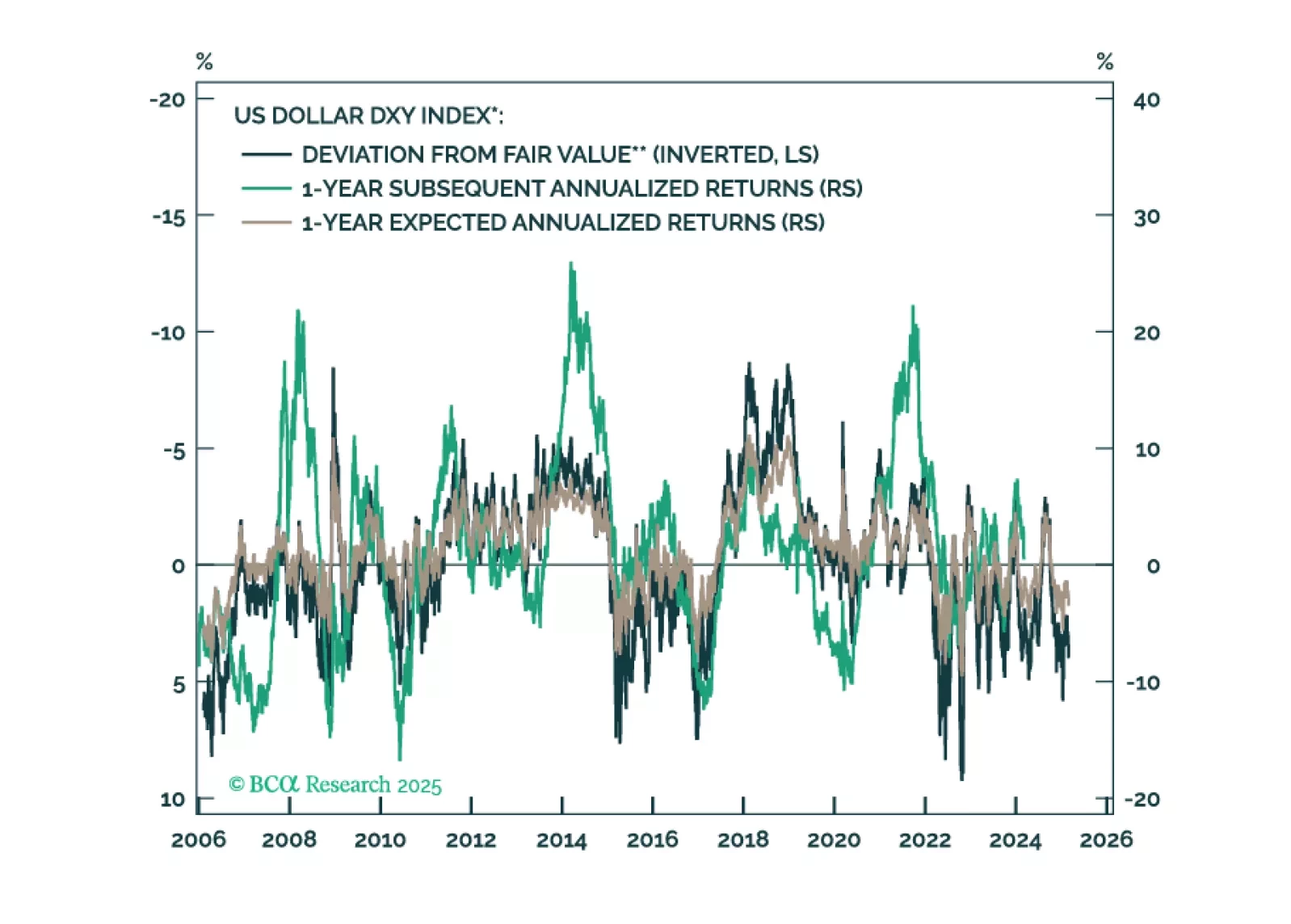

This report is our Part III series on valuation and subsequent returns, where we recalibrate our short-term models to emphasize signals over the next nine-to-twelve months. We will henceforth call these models STTM: Short Term Timing Models.

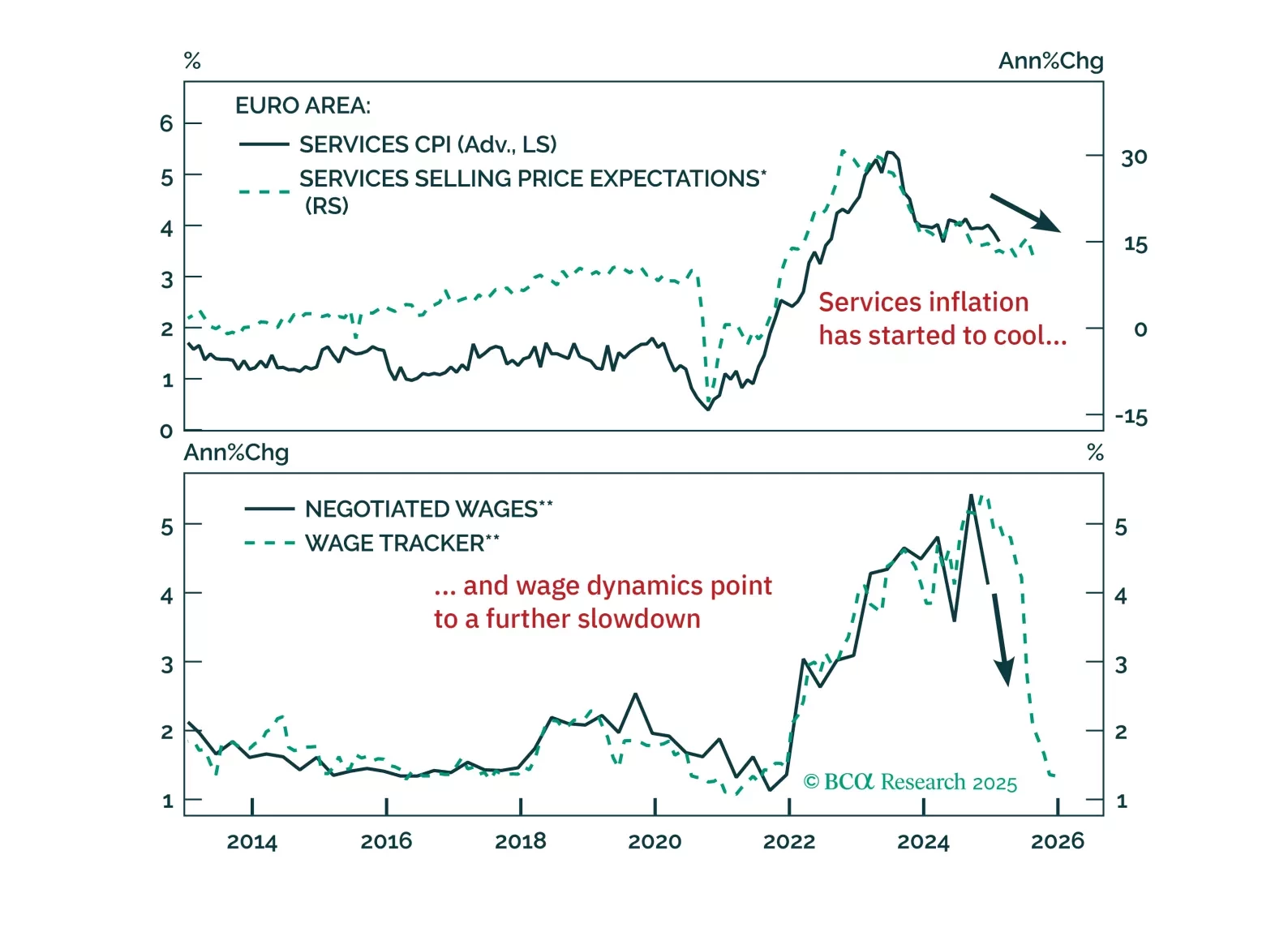

The ECB cut rates as expected, but rising yields and a stronger euro are tightening financial conditions just as fiscal policy shifts the macro landscape. With more rate cuts ahead and market positioning stretched, we outline the key risks, investment opportunities, and our updated call on the ECB’s terminal rate. Read our full report for actionable insights.