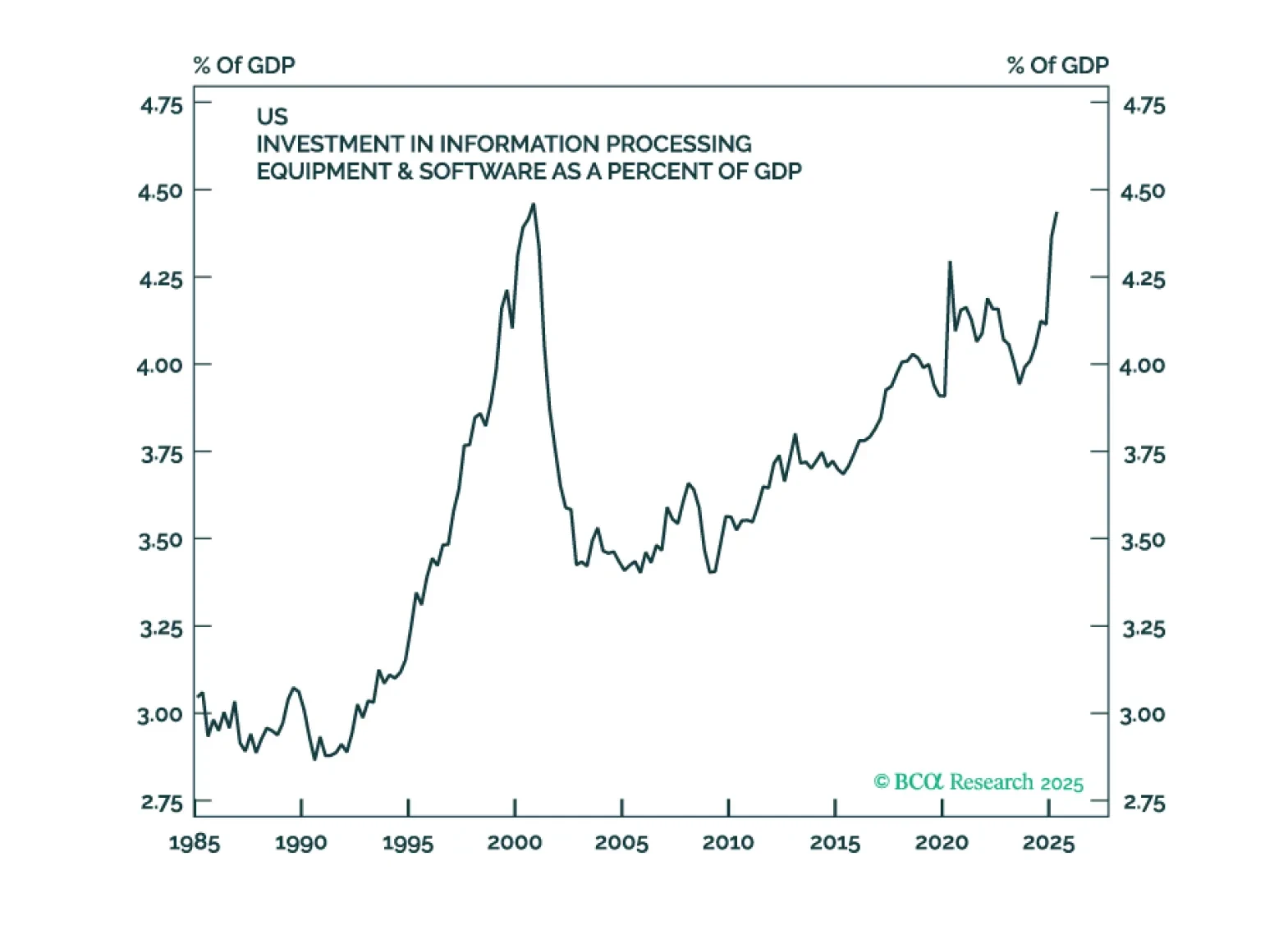

AI

Disparities between households and between companies’ earnings and equity performance are widening, but the overall status quo remains in place. We reiterate our neutral asset class recommendations while watching for early signs of whether activity might break out or break down.

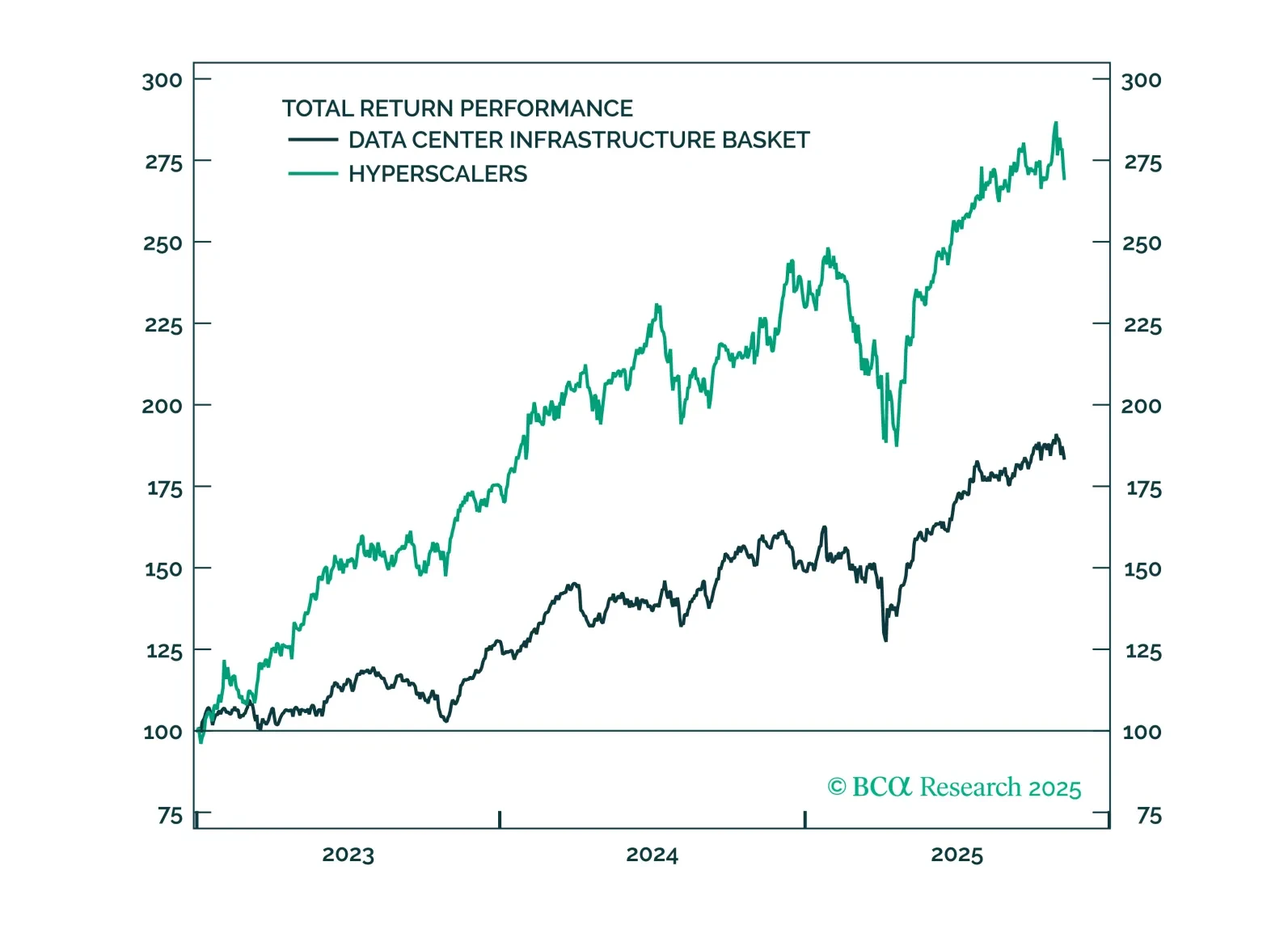

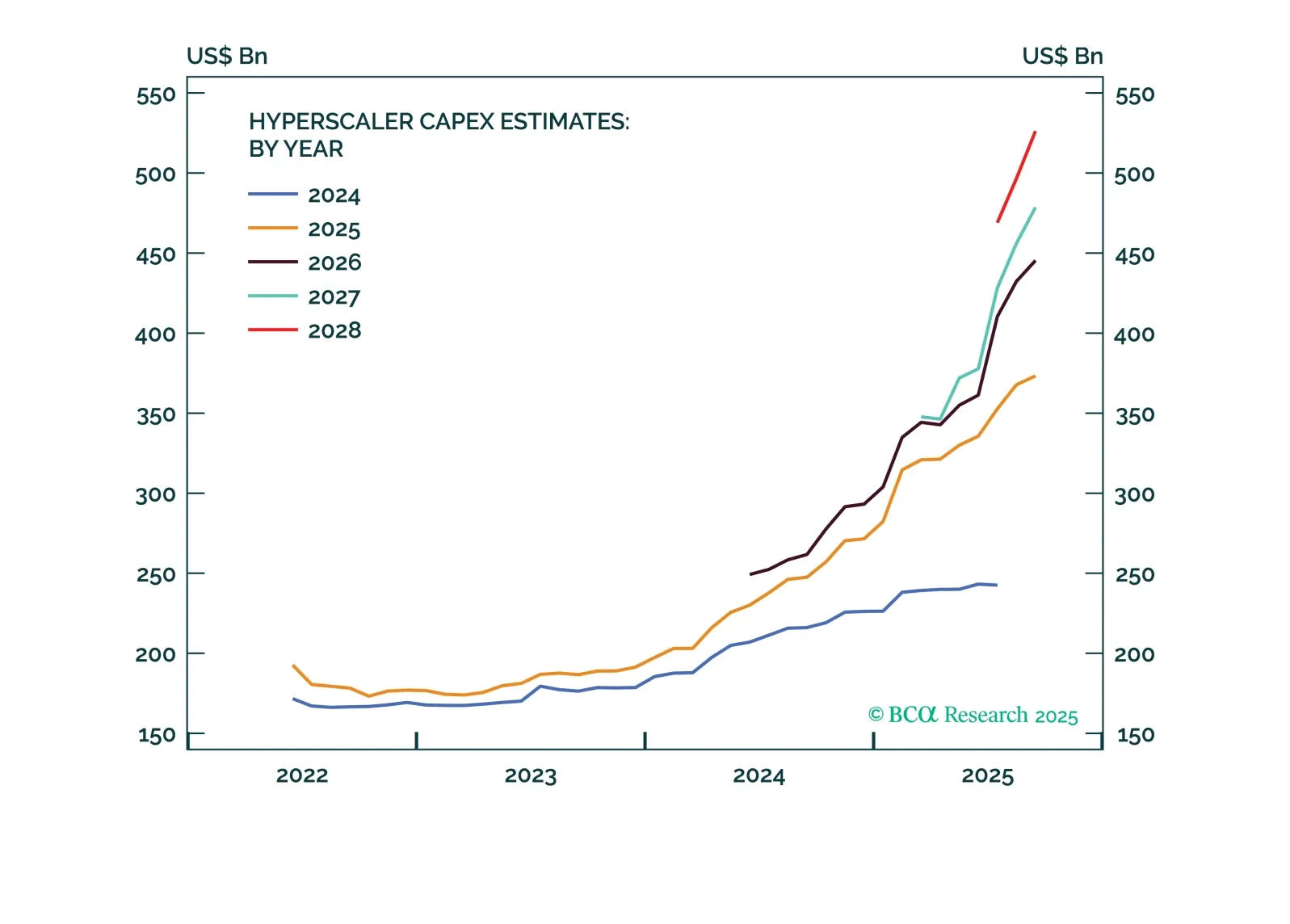

As hyperscalers expand global data center capacity, they are igniting a powerful industrial cycle. Capital Goods and Materials companies supplying turbines, grid components, cooling systems, and advanced connectivity materials for data center and energy infrastructure are emerging as key beneficiaries, positioned to capture structural growth as GenAI demand reshapes the economy.

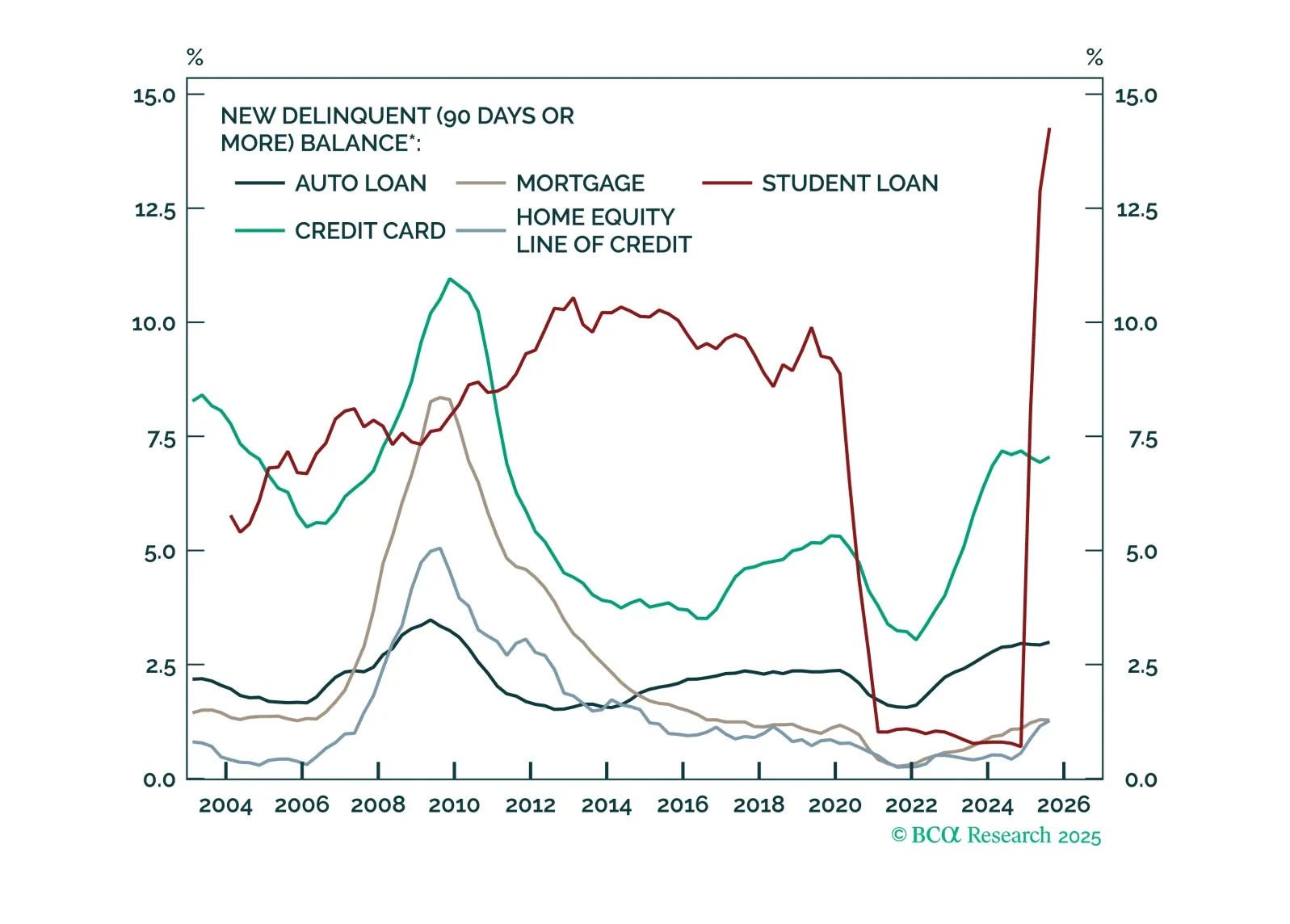

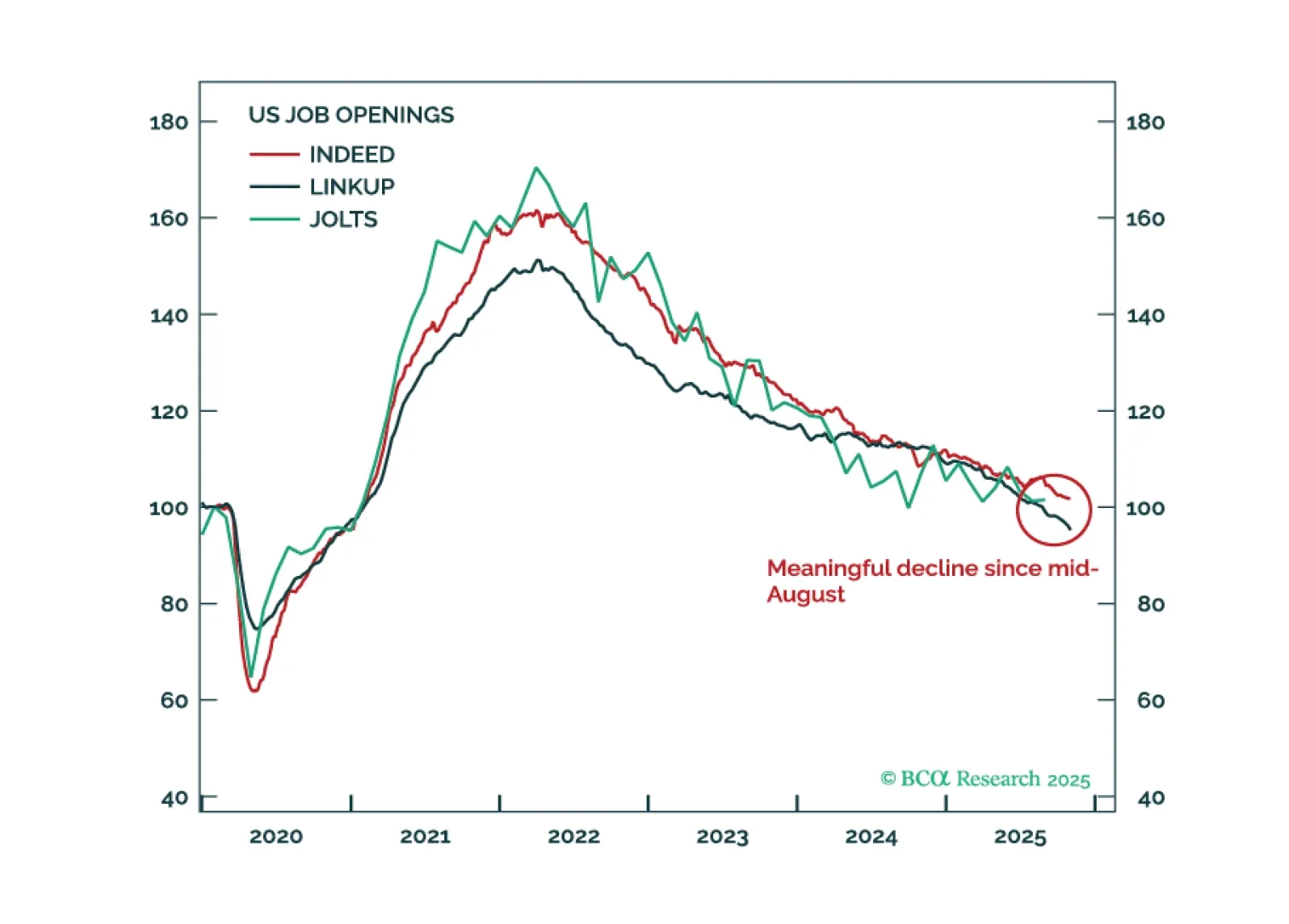

In the absence of official government data, investors are turning to alternative sources to gauge the direction of the US economy. Our analysis of this data suggests that the economy has continued to expand at a moderate pace over the past two months. If the Supreme Court were to strike down the tariffs, this would reduce the near-term odds of a recession while raising the odds of overheating.

Détente between China and the US is a big deal. Economic data continues to give the Fed reasons to cut. What is there to be worried about? Very little. But we chew on some bearish thoughts as we start thinking about 2026.

We discuss which variables we are tracking to assess the risks to the bull market in the absence of government data. So far, we do not see any obvious red flags. Remain overweight on equities and fixed income.

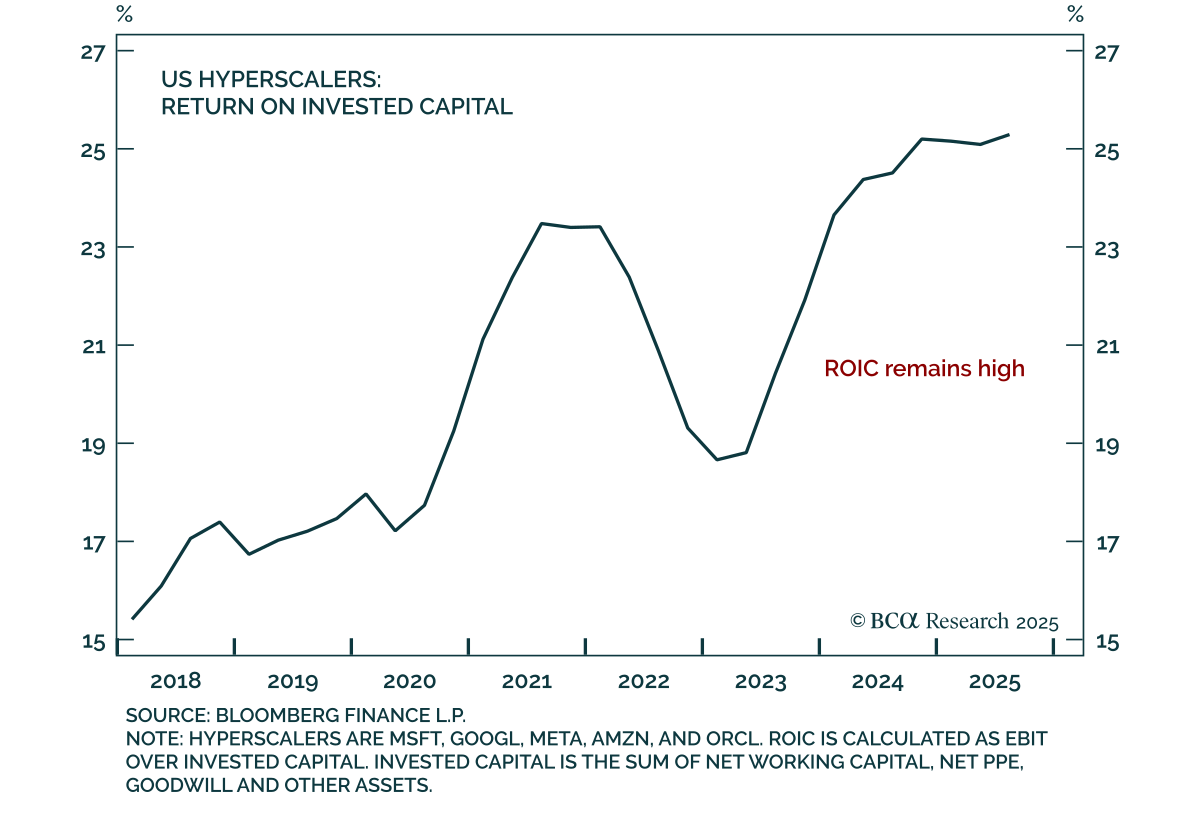

Fresh off a month of boning up on all things AI, we walk through a high-level Q&A discussing AI capex and how much the AI investing boom is really contributing to US growth.

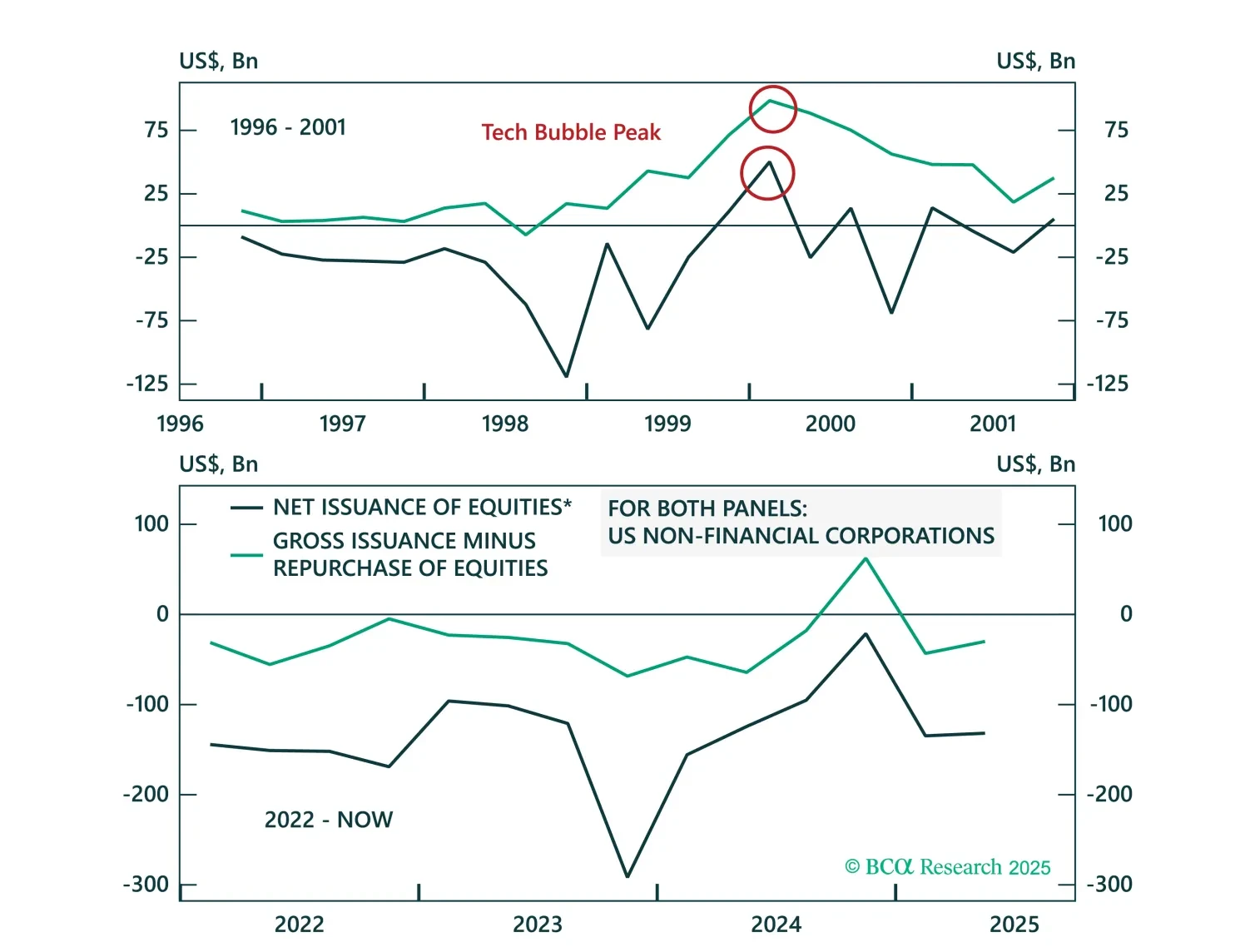

The rush to build AI infrastructure is based on a false premise: that there are significant advantages to being the first to come to market.

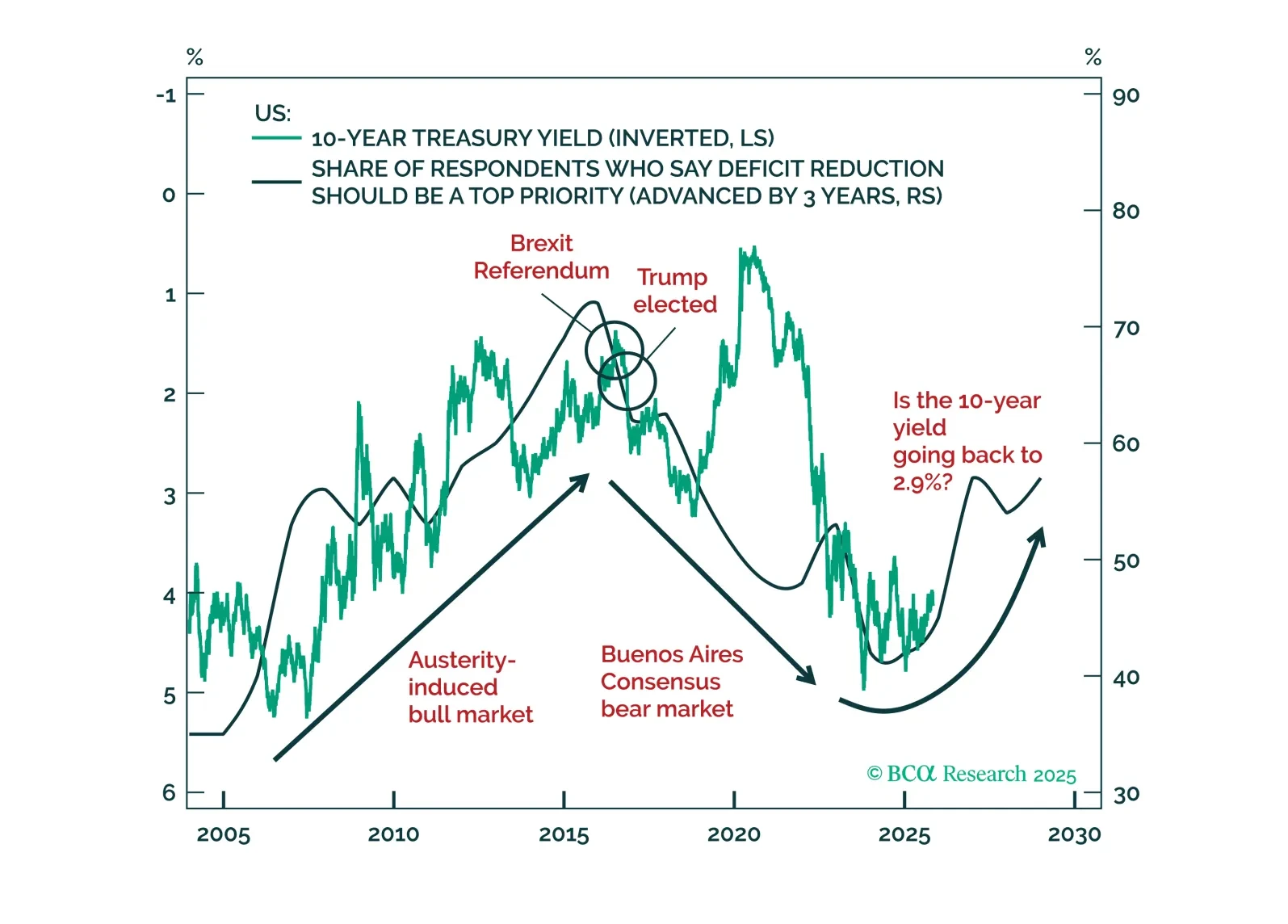

Precious metals, corporate credit, and tech stocks are all showing signs of late-cycle euphoria. We identify various trigger points that investors should monitor to turn more bearish.