Asset Allocation

Despite our bearish predisposition towards stocks, we are open-minded to anything that could challenge our thesis. As such, in this report, we review five upside scenarios for equities.

The US economy is set to enter a recession within the next few months. Stay underweight equities and overweight cash. Look to increase fixed-income duration exposure over the coming months. The euro is likely to strengthen and European stocks should outperform US stocks over the next month or so, but these trends will reverse by the middle of this year.

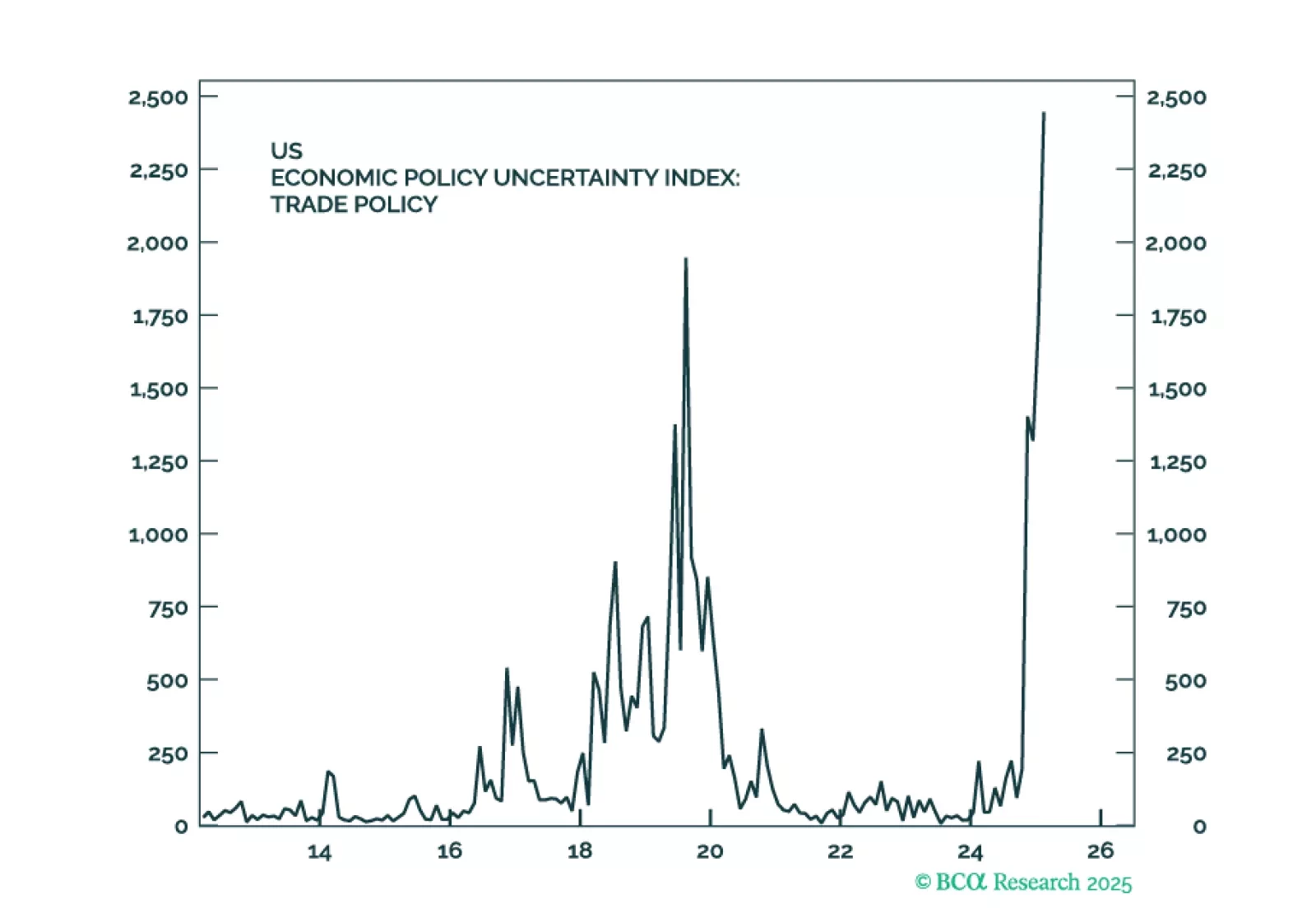

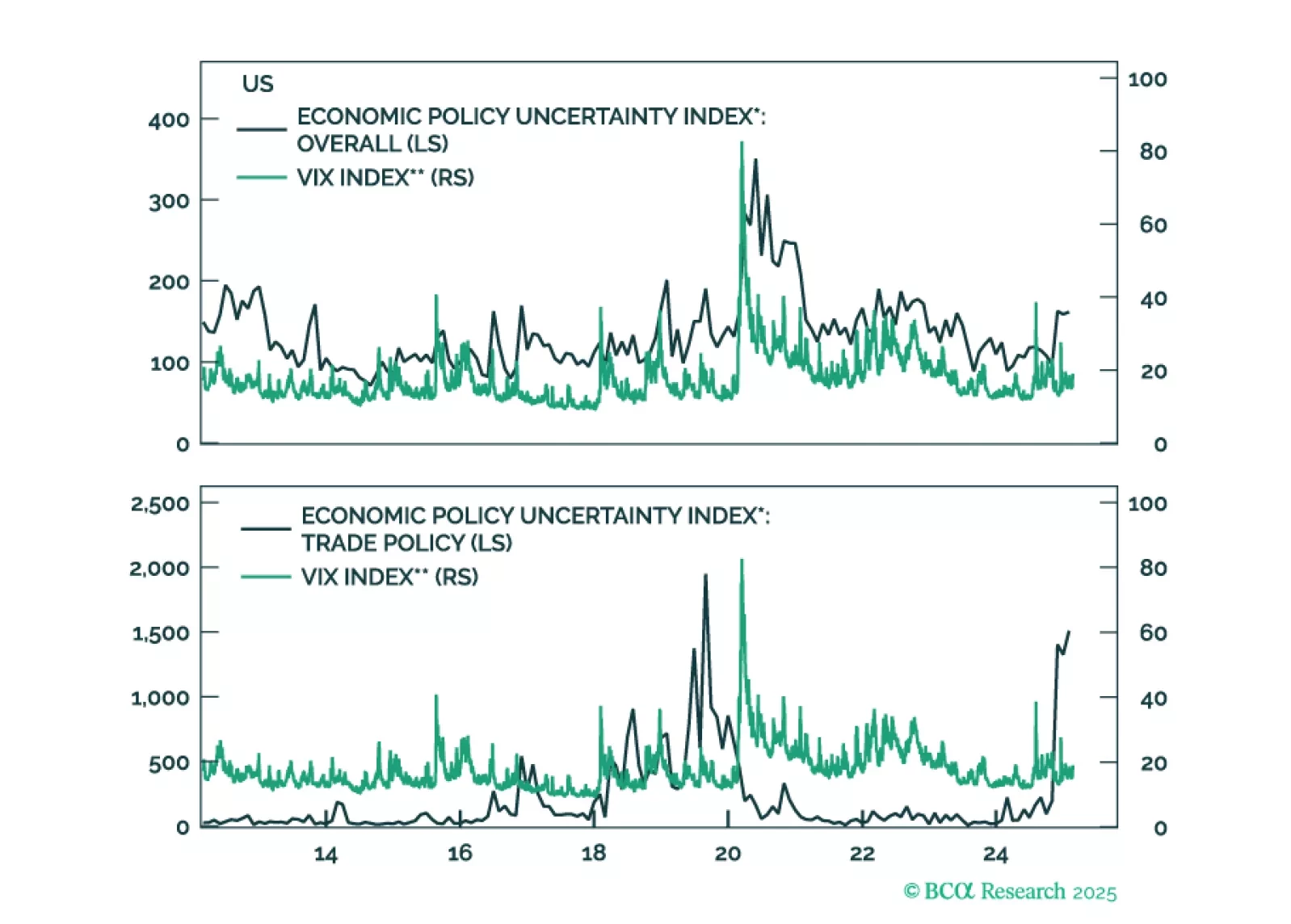

Investors see Europe as a museum: A continent stuck in the past, with no ability to innovate, much less generate profits. But is this view accurate? In this report we argue that the structural headwinds to European profitability are a thing of the past. Political change and improving sentiment are also a tailwind for Europe. Meanwhile, in the US, economic uncertainty brought about by Trump’s policies have reversed the surge in animal spirits that followed the election. All of this is happening within the context of weakening growth. We upgrade European equities from neutral to overweight and downgrade US equities from neutral to underweight.

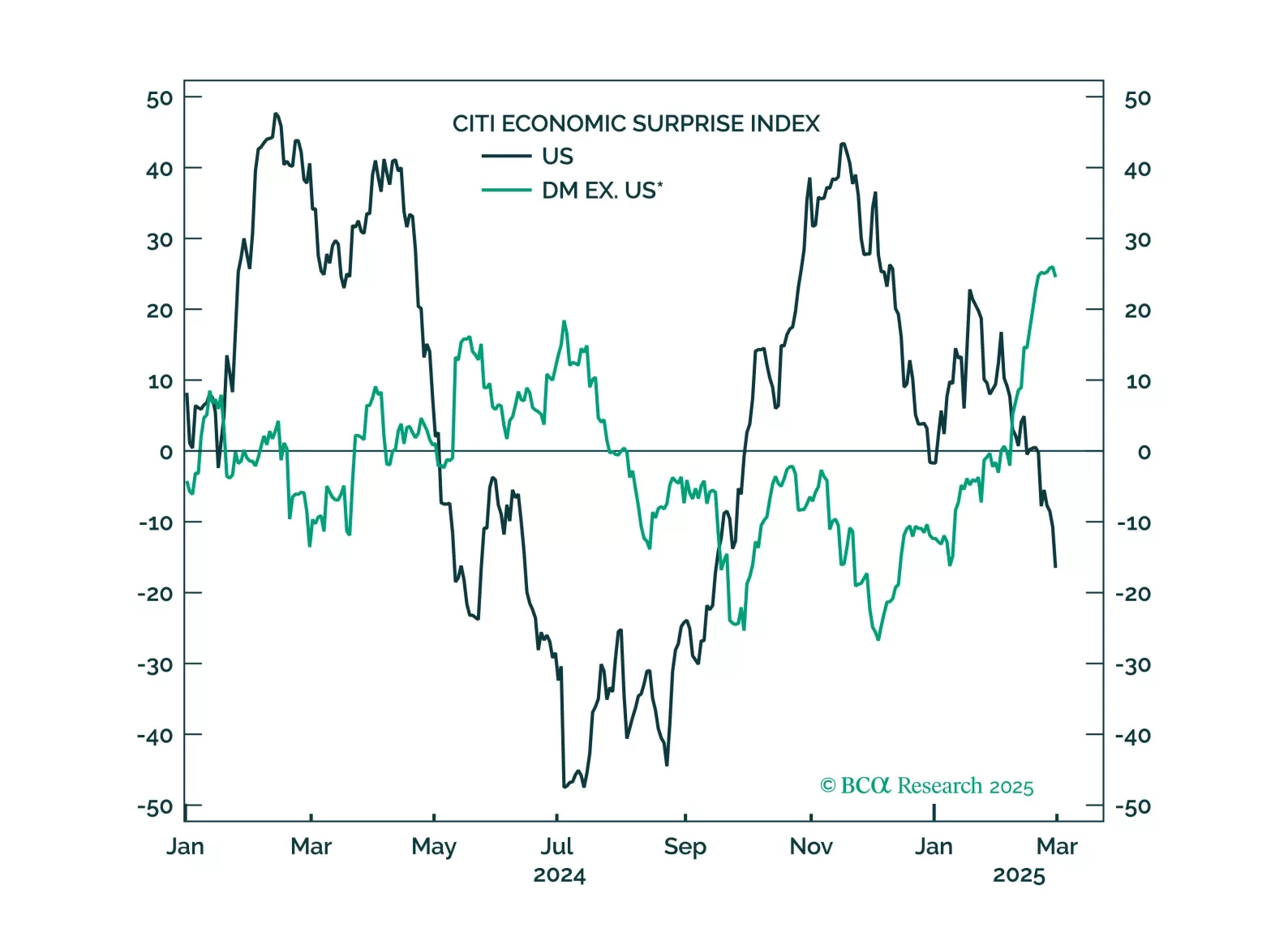

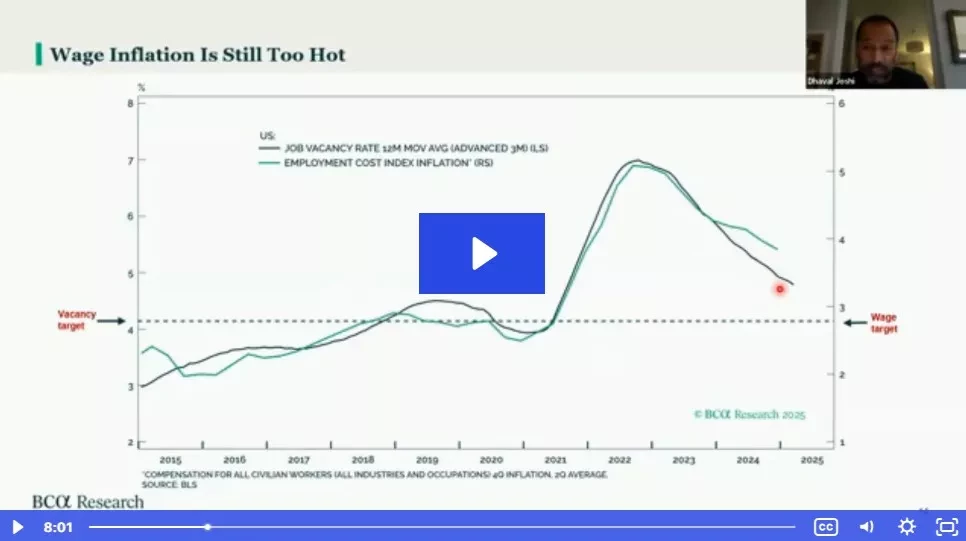

US growth has slowed in recent weeks. This can be seen in the weaker data on retail sales, consumer confidence, services PMIs, and a swath of housing releases (notably starts, existing home sales, homebuilder confidence, and stock prices). It can also be seen in the decline in GDP tracking estimates. The Atlanta Fed's GDPNow model projects growth of 2.3% in Q1, down from a peak of 3.9% on February 3. The Citi US Economic Surprise Index has also dipped into negative territory.

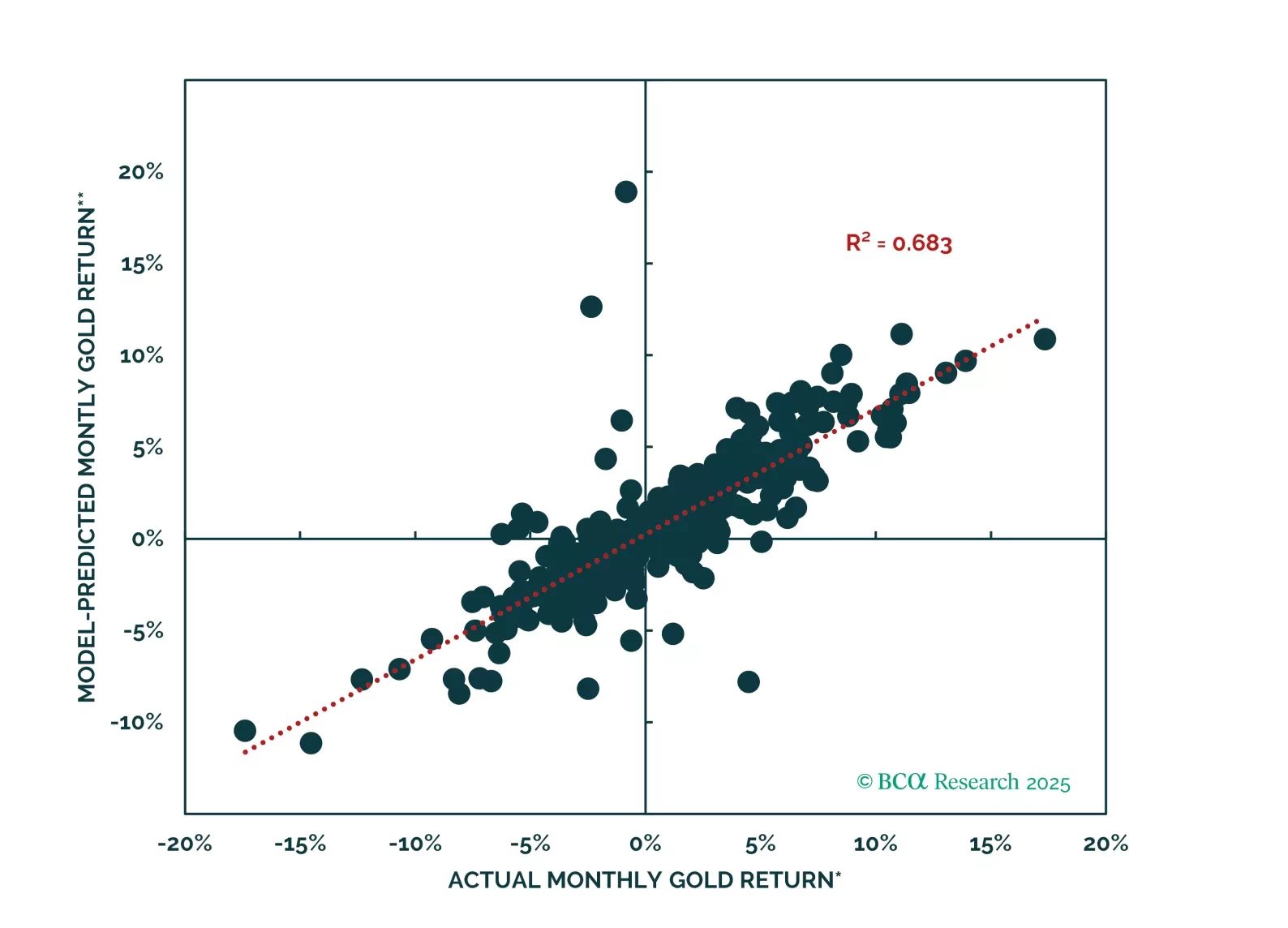

As gold keeps making new highs, many clients have asked us whether a gold allocation makes sense for their portfolios and, if so, how big that allocation should be. In this report we try to answer these questions from the perspective of investors with eight different home currencies. Specifically, we analyze the following properties of gold: 1) What drives gold? 2) What is gold’s role in a portfolio? 3) How much gold should investors own?

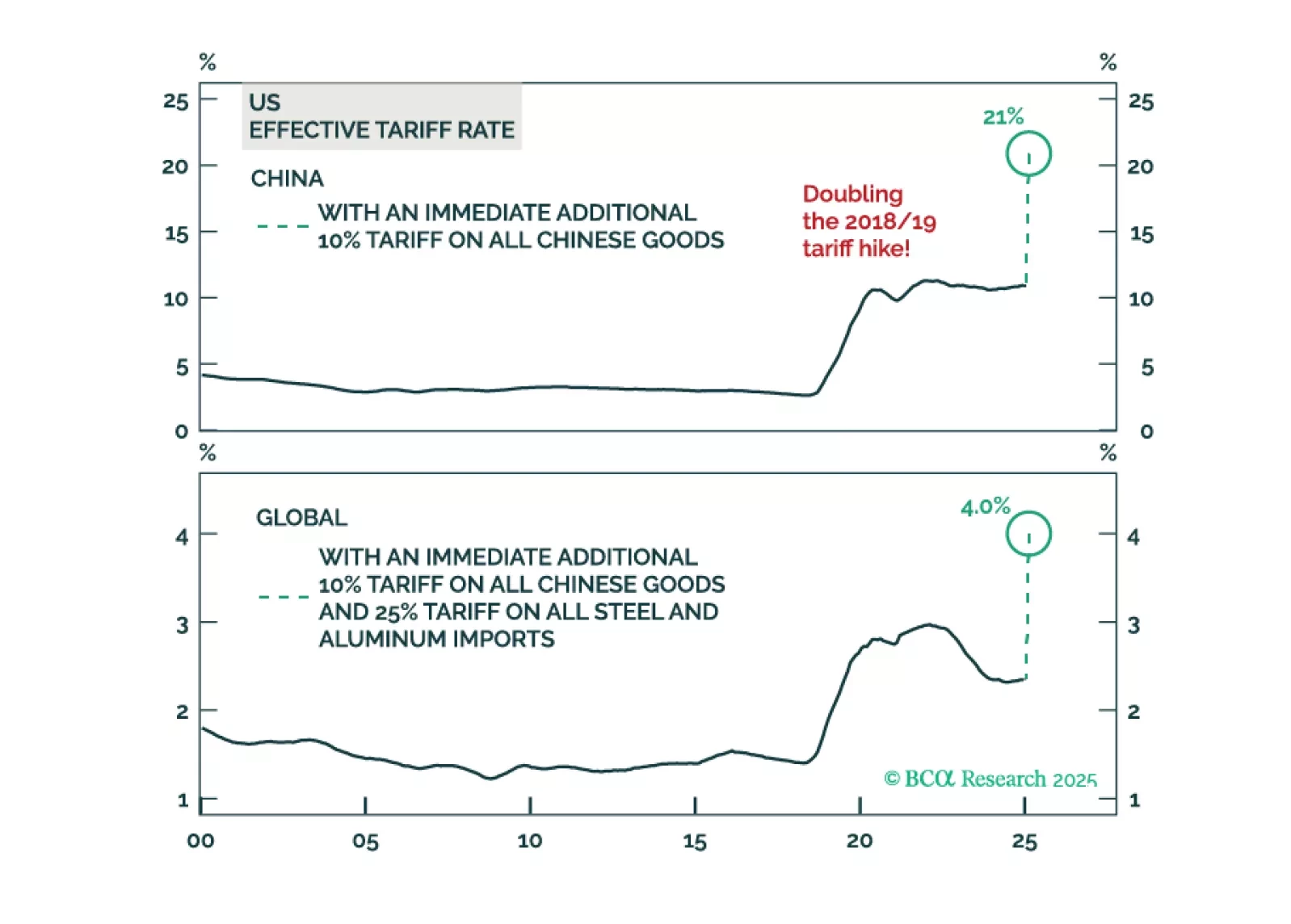

In his latest Thoughts Of The Day, Peter Berezin discusses the different moving parts of the global economy today and the potential impact of Trump's policies.

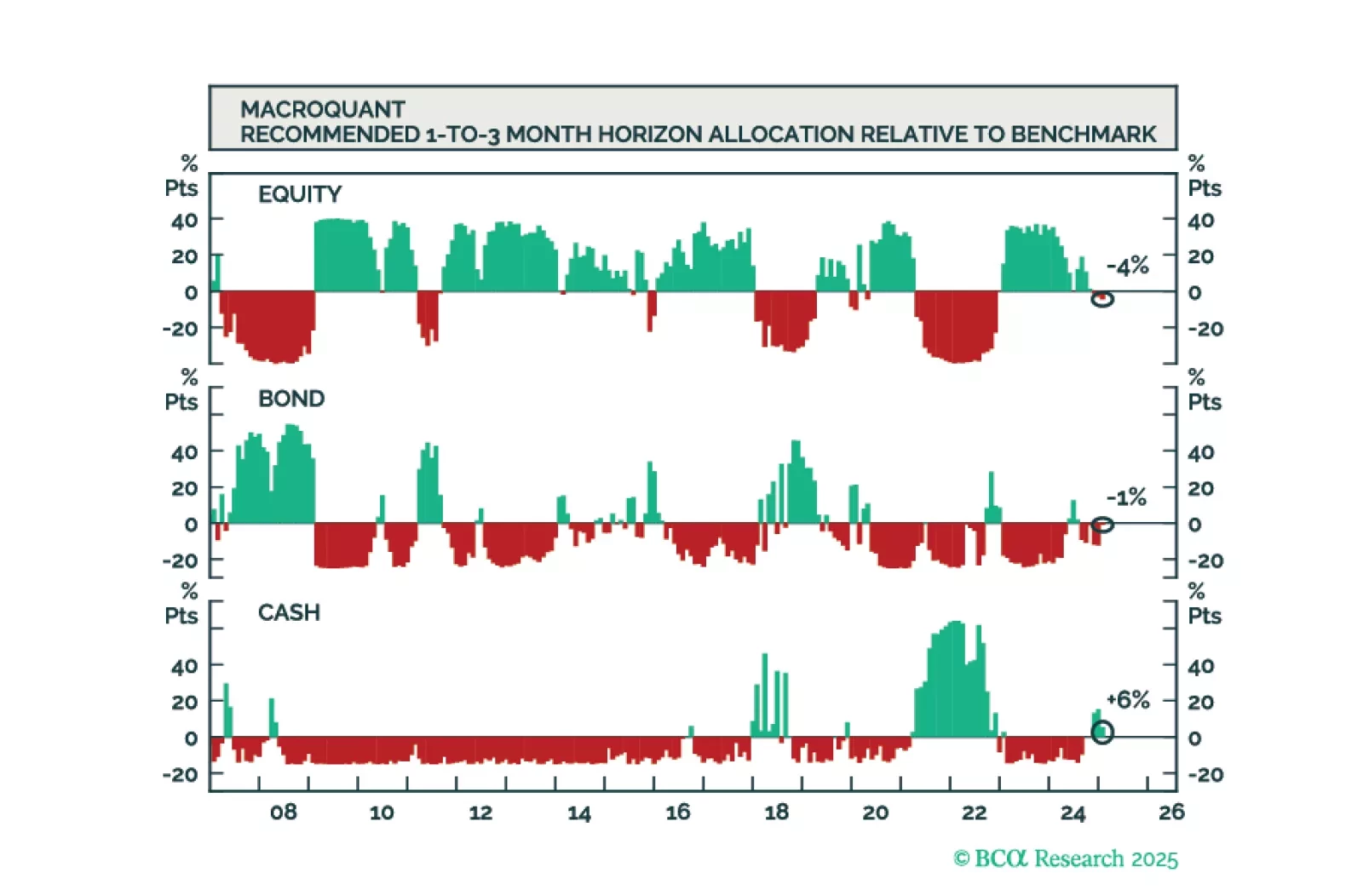

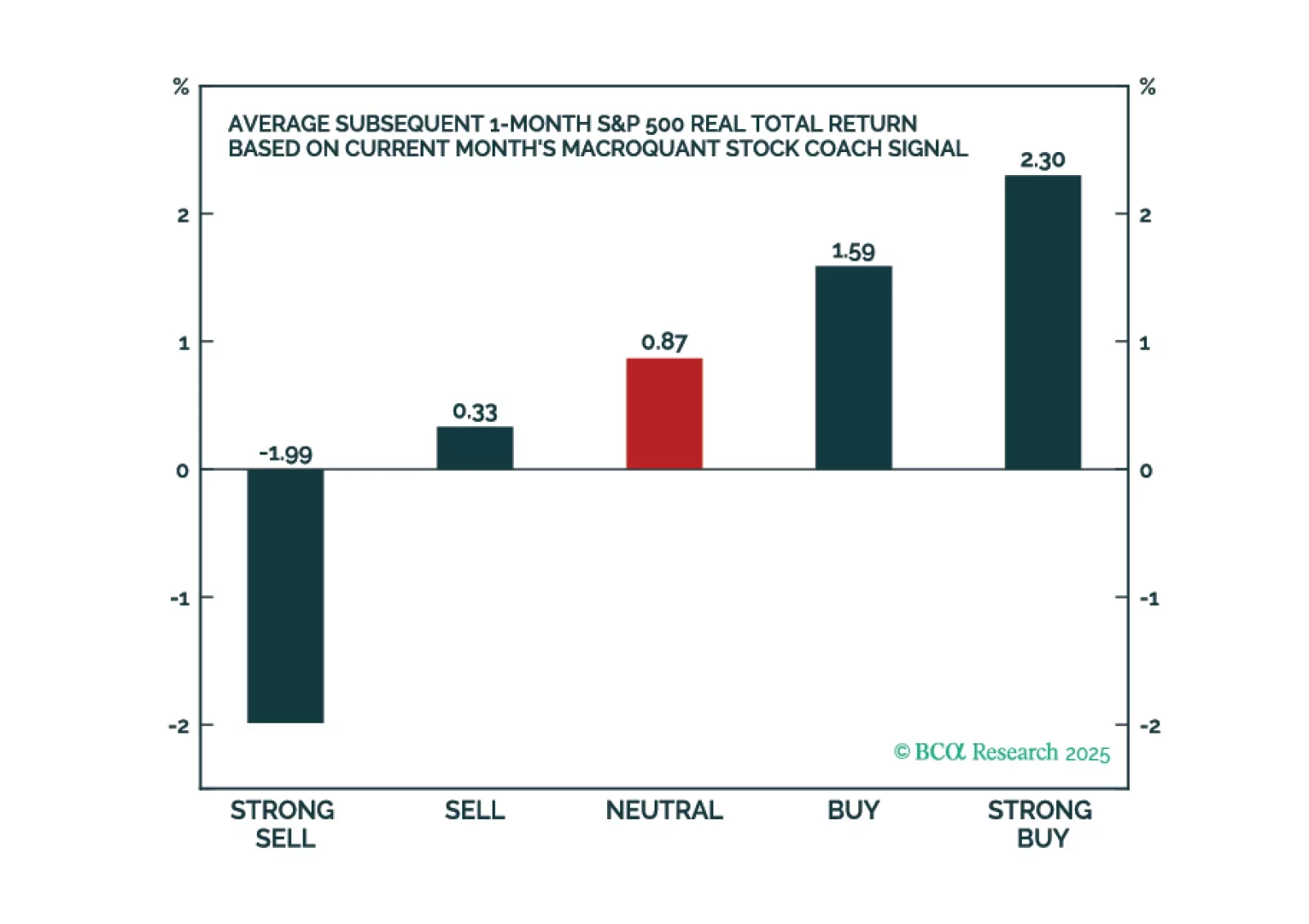

The latest version of the MacroQuant model suggests that the bull market in US stocks is winding down. The model expects Treasury yields to fall later this year but is not ready to go long duration just yet.