Australia

In this <i>Insight</i>, we answer a few crucial questions: Do the BoC and RBA decisions have any impact on what we can expect from other major central banks next week? Are there any profitable trades that can be put on, given the recent hawkish shift by these two central banks? How should global bond investors be positioned in a fixed income portfolio?

In this report, we follow up on the upgrade to our US duration stance from last week with a review of our rates views and government bond allocations outside the US. We conclude that while we now find US Treasuries to be more attractive from a value perspective, even better value is available in euro area and UK government debt.

In this Month-In-Review report, we go over the latest G10 data releases and rank currencies’ fundamental standing based on our updated macroeconomic model.

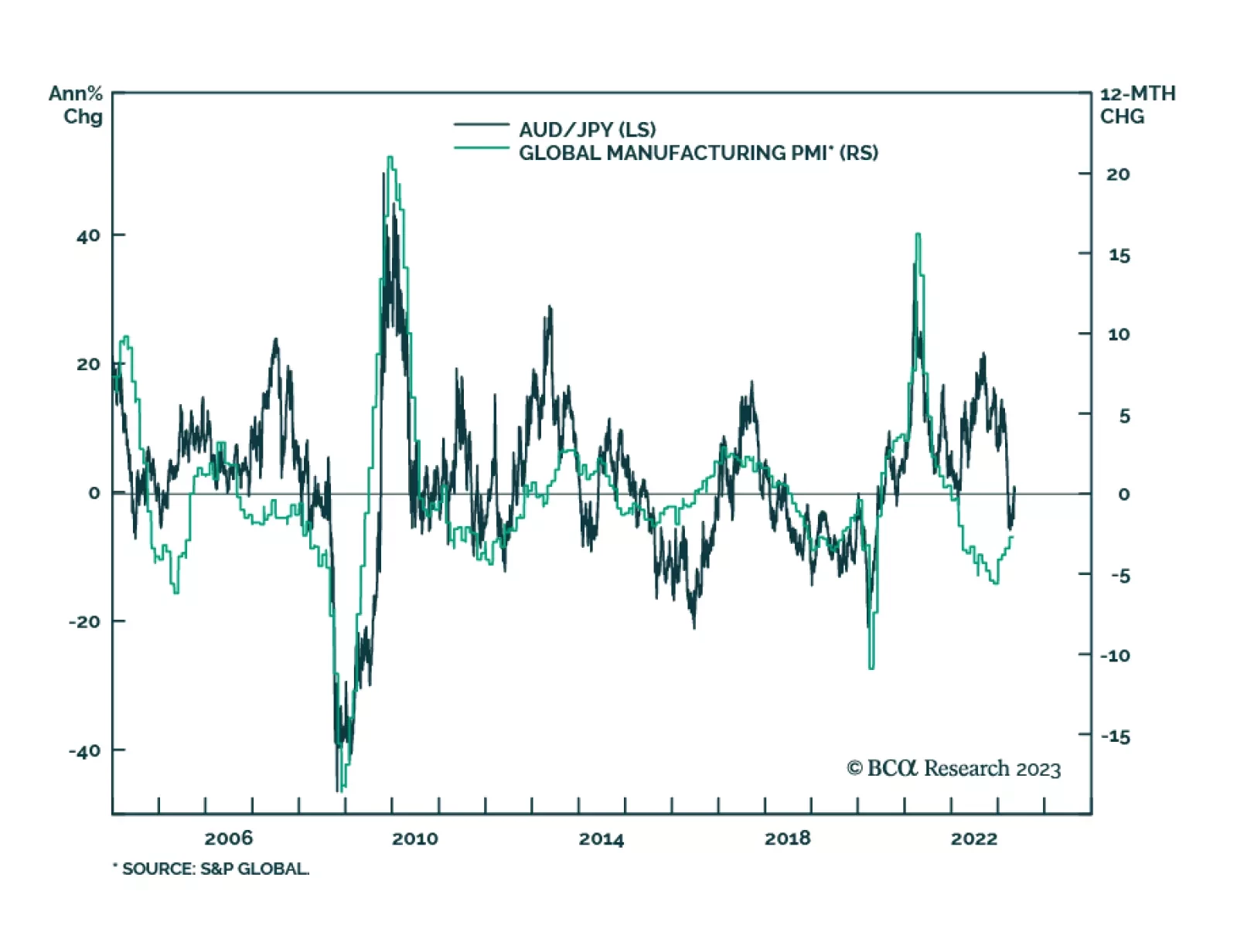

In this Special Report, we evaluate future prospects for the Australian dollar and Australian government bonds. The currency remains fundamentally cheap, and positioning is very short, but the AUD will continue to underperform in the near-term due to sluggish global growth. Australian government bonds have had a nice run of outperformance over the past year, but it is now time to take profits with given the uncertainty that the RBA will deliver the rate cuts currently discounted.

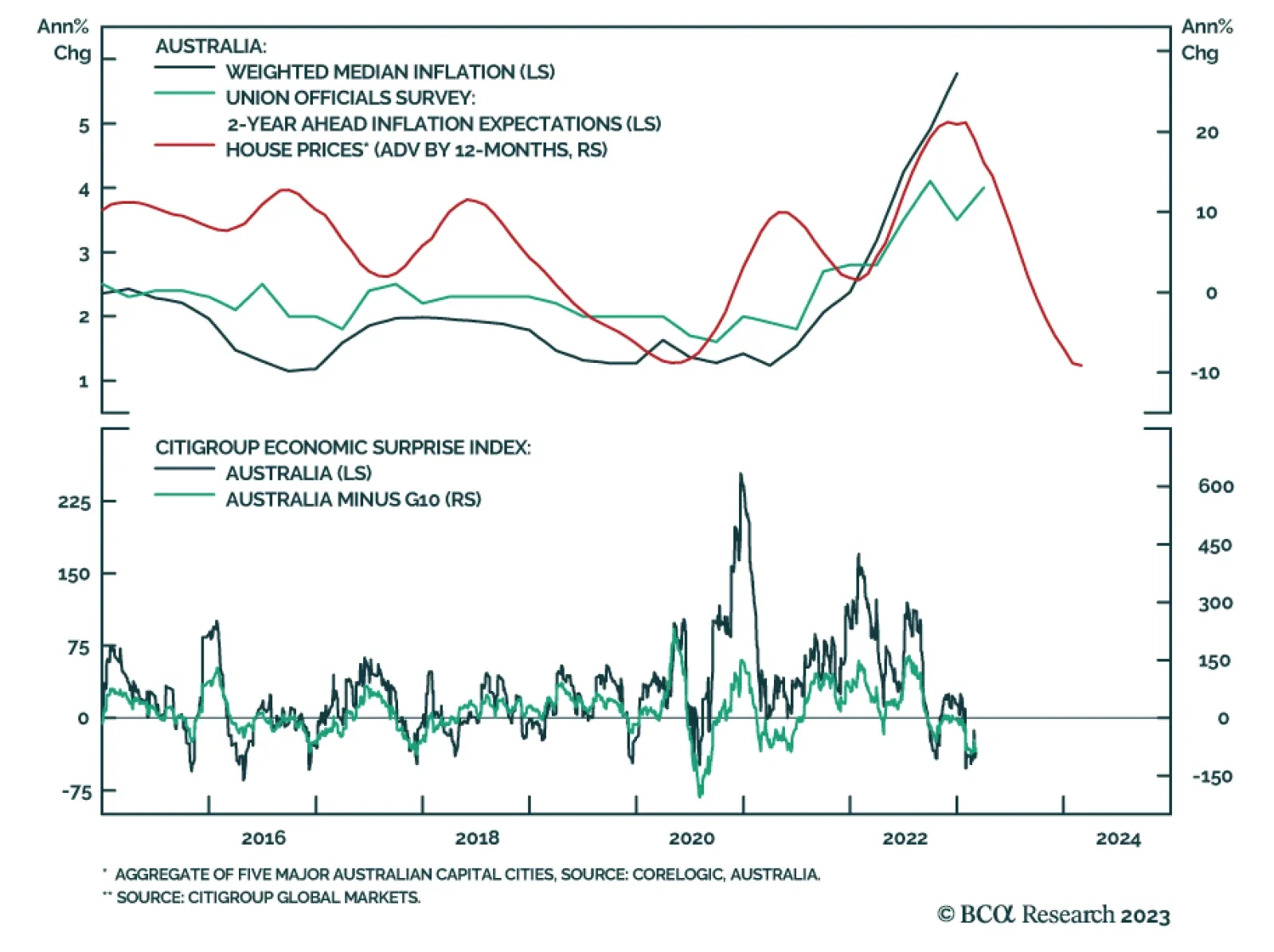

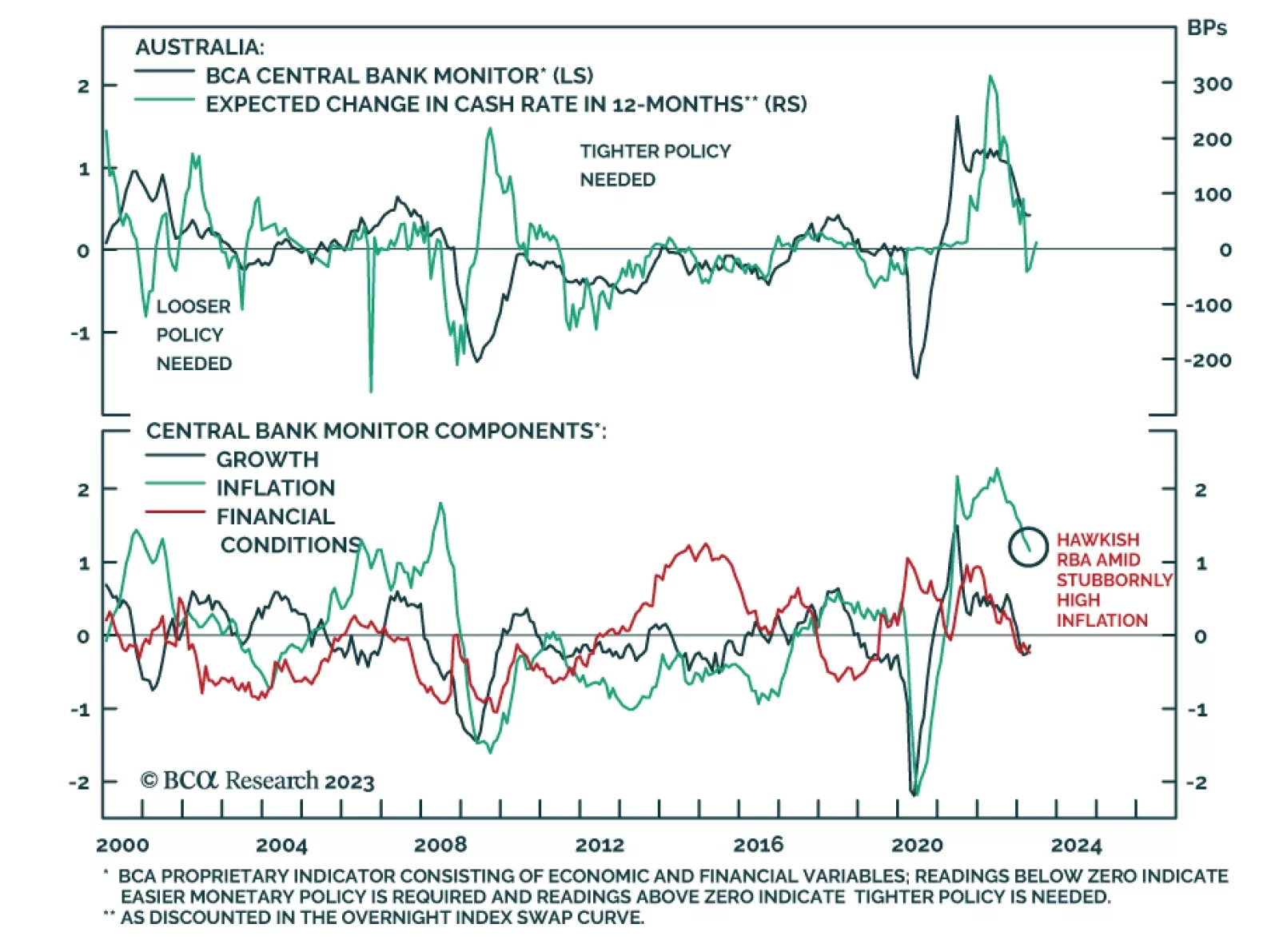

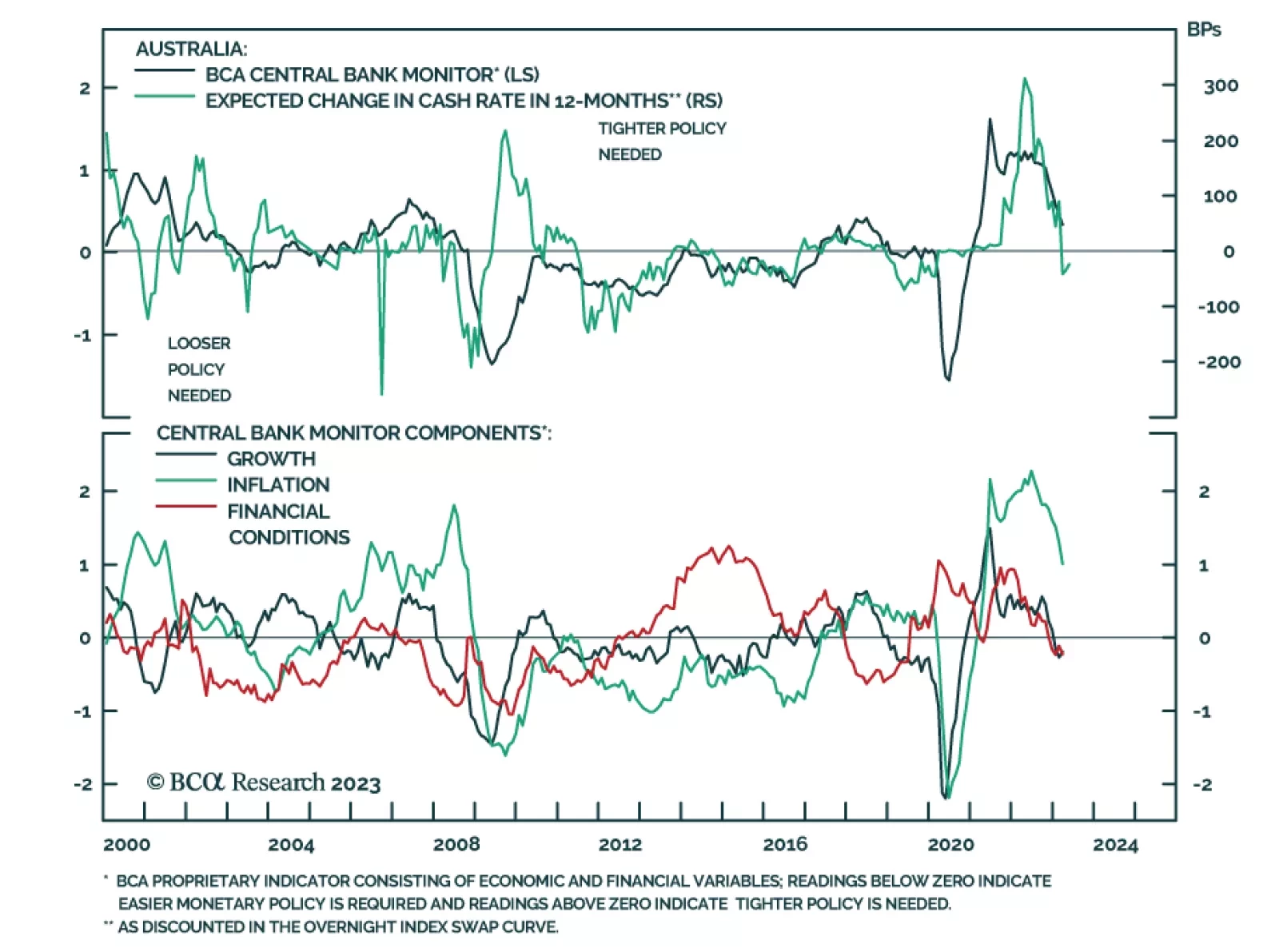

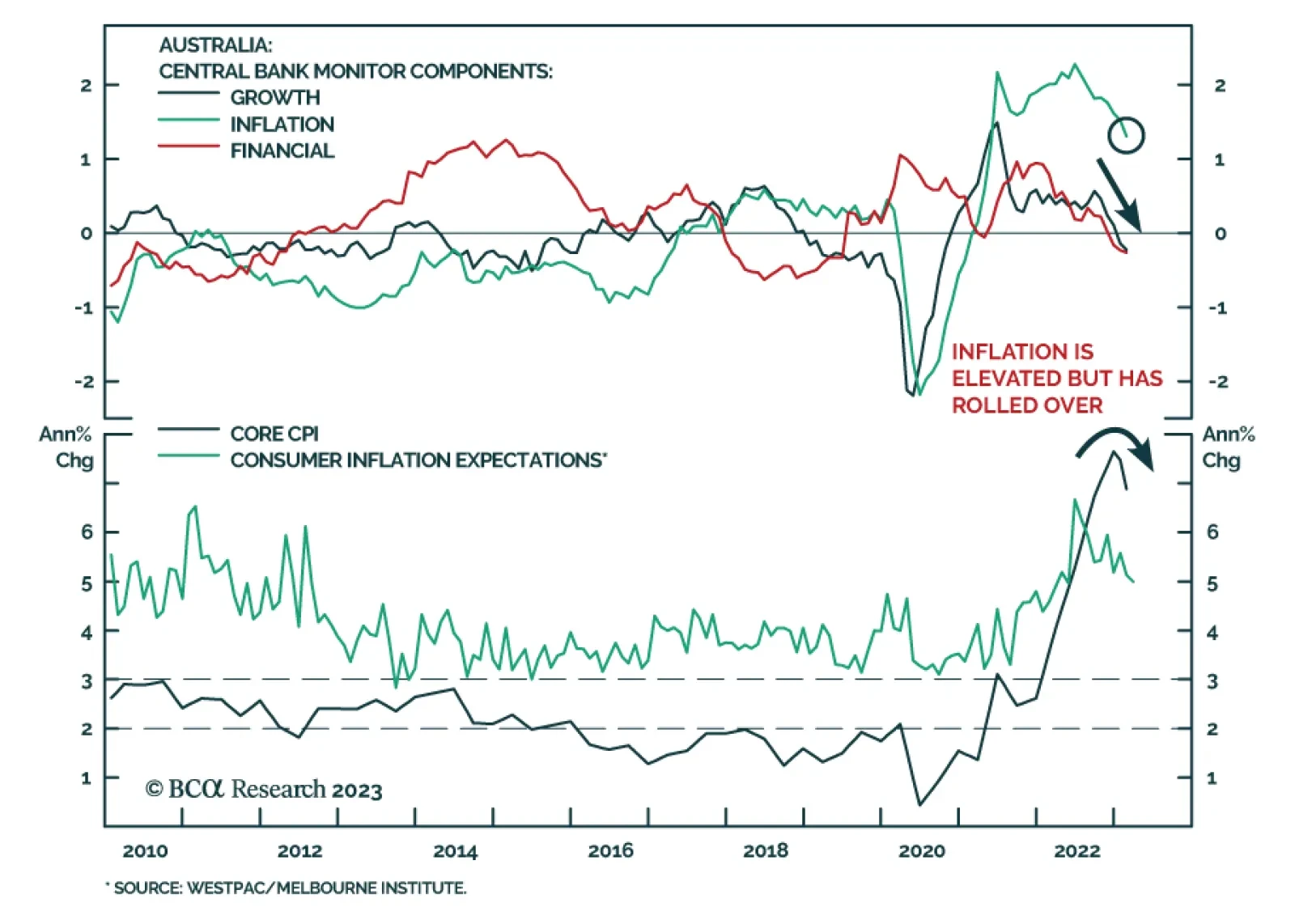

In this Special Report, we present our updated Central Bank Monitors for the US, Canada, Australia, New Zealand and Japan. We have improved the methodology used to calculate the monitors to make them more dynamic to structural changes over time. The main message from the Monitors is consistent across all five countries. The pressure to hike rates is diminishing, suggesting that the end of tightening cycles is approaching, but it is still too soon to expect rate cuts.