Australia

Highlights Butterflies & Yield Curve Models: With bond market volatility now back to the subdued levels seen prior to the COVID-19 market turbulence earlier in 2020, it is a good time to update our global yield curve valuation models to look for attractive butterfly trade ideas. Valuations: The models generally indicate that flattener trades offer better value across all countries. Our medium-term strategic bias, however, is towards steeper yield curves with policy rates on hold and depressed global inflation expectations likely to continue drifting higher over the latter half of the year. Yield Curve Trades: We are initiating the first set of yield curve trades within our rebooted Tactical Trade Overlay: going long a 7-year bullet vs. a 5-year/10-year barbell in the US; long a 2-year/30-year barbell vs. a 5-year bullet in France; long a 5-year/30-year barbell vs. a 10-year bullet in Italy; and long a 3-year/20-year barbell vs. a 10-year bullet in the UK. Feature In a Special Report published back in February of this year, we dusted off our model-based framework to find value in trades focused on the shape of government bond yield curves.1 By comparing the market-implied short-term interest rate expectations extracted from our curve models to our own macro views, we are able to come up with actionable buy or sell signals across the yield curve in nine developed markets: the US, Germany, France, Italy, Spain, the UK, Japan, Canada, and Australia. Table 1Most Attractive Butterfly Trades

Global Yield Curve Trades: Netting Returns With Butterflies

Global Yield Curve Trades: Netting Returns With Butterflies

Given the extreme market turbulence around the time we published that report, as the full scope of the COVID-19 pandemic was becoming evident, we chose not to recommend any curve trades from our models until global volatility subsided to acceptable levels. The vigorous action from central banks to manipulate bond yields since then - quantitative easing, aggressive forward guidance, outright yield curve control in Japan and Australia, and other unconventional monetary policy measures - introduced another layer of difficulty in implementing successful curve trades using models estimated in more normal times. With global bond market volatility now back down to pre-COVID levels, we feel that the time is right to use our curve models to help identify opportunities. Specifically, we are implementing new recommended yield curve trades in the US, France, Italy, and the UK. Table 1 shows the most attractive butterfly trades across all the markets covered in this analysis. Note that three of the four trades we are initiating include very long-dated bonds where yields are less susceptible to direct central bank influence. The only exception is our US long 7-year bullet vs. 5-year/10-year barbell trade, the reasoning for which we outline later in this report. Three of the four trades we are initiating include very long-dated bonds where yields are less susceptible to direct central bank influence. The only exception is our US long 7-year bullet vs. 5-year/10-year barbell trade. Before delving into our analysis proper, a quick note: in the interest of brevity, we will limit ourselves to a simple explanation of butterfly strategies and our yield curve models in this report. For those interested in a deeper explanation of the curve modeling framework, please refer to our February 25, 2020 Special Report. A Recap On Butterflies And An Update On Our Yield Curve Models A butterfly fixed income strategy involves two main components: a barbell (a weighted combination of long-term and short-term bonds) and a bullet (a medium-term bond that sits within the yield curve segment selected in the barbell). To implement a butterfly strategy, a bond investor would go long (short) the barbell while simultaneously going short (long) the bullet. By weighting the combination of the long- and short-term bonds in the butterfly such that the weighted sum of their duration equals the duration of the medium-term bond in the bullet, we achieve immunization to parallel shifts in the yield curve. At the same time, due to the relatively higher duration of the longer-term component of the butterfly, we get exposure to specific changes in the slope of the yield curve. In general, the barbell will outperform the bullet in a flattening yield curve environment, and vice-versa. Chart of the WeekButterfly Spreads & Yield Curves

Butterfly Spreads & Yield Curves

Butterfly Spreads & Yield Curves

To actually decide how, and on which parts of the yield curve, to implement our butterfly strategies, we make use of our yield curve models. These models rely on the positive relationship typically observed between the butterfly spread and the slope of the yield curve. When the curve steepens, the butterfly spread widens, and vice-versa (Chart of the Week). This has to do with mean reversion: as the curve steepens, it increases the odds that the curve will flatten in the future since it cannot steepen indefinitely. Consequently, investors will ask for greater compensation to enter a curve steepener trade when the curve is already steepening. As a result, we can create simplified models of the yield curve by regressing any butterfly spread on its corresponding curve slope. Deviations from these fair value models indicate which butterfly strategies are cheap or expensive. However, the model output does not by itself constitute a buy or sell signal and must be integrated with our macro view on the slope of the curve. For example, a butterfly strategy with an expensive bullet implies that there is already a certain amount of steepening discounted in the yield curve. If the yield curve flattens, or even steepens by an amount smaller than what is discounted in the yield curve over the investment horizon, the barbell will outperform, as expected. However, if we see more steepening than is discounted in the yield curve, the bullet will outperform, even though it was already at relatively expensive levels. Therefore, it is crucial to integrate our macro view on how much the curve will steepen or flatten over the investment horizon into our curve trade selection framework. In recent reports, we have emphasized our high-conviction view that global inflation expectations will drift higher in the coming months, driven by reflationary fiscal and monetary policy and a continued rebound in global commodity prices (most notably, oil).2 However, a rise in inflation expectations does not necessarily translate to a “one-to-one” rise in nominal yields if it is offset by a compression in real bond yields. To disentangle this, we look at the 3-year rolling betas of nominal 10-year government bond yields to the corresponding 10-year breakeven inflation rates using inflation-linked bonds (Chart 2). The data suggest a currently weaker relationship between inflation expectations and nominal yields, with all betas well below their post-crisis maxima. Our overall macro bias is towards a global steepening in yield curves, but given our strong belief in a rebound in inflation expectations, we would be more willing to enter steepener trades in higher-beta regions such as Germany, Canada, the US, and Australia where it is more likely that a rise in inflation expectations will translate to higher nominal yields. Conversely, we are less hesitant to enter flatteners in the lower-beta regions such as the UK, France, Italy, and Japan. Chart 2The Link Between Nominal Yields And Inflation Expectations Has Weakened

Global Yield Curve Trades: Netting Returns With Butterflies

Global Yield Curve Trades: Netting Returns With Butterflies

When we said earlier this year that we were “dusting off” our yield curve models, that was not just a figure of speech. The models date back originally to 2002, meaning that they are old enough to vote—perhaps even for a popular rapper. Even though we have been refining and updating it along the way, one of our concerns was that this model was estimated for a pre-crisis sample period before near-zero rates became ubiquitous in developed markets. Our overall macro bias is towards a global steepening in yield curves, but given our strong belief in a rebound in inflation expectations, we would be more willing to enter steepener trades in higher-beta regions such as Germany, Canada, the US, and Australia. To test that the curve relationships within our models are maintained when global central banks are pinning policy rates near 0%, we have re-estimated all the regressions for the post-financial crisis period from 2009 to 2017 when most central banks kept rates near the zero bound. Chart 3 shows the results for the representative 2-year, 5-year and 10-year portions of the yield curve. On the whole, the coefficients are weaker but still positive with the exception of Japan, where many years of zero rates and quantitative easing have caused the 2-year/5-year/10-year butterfly spread to become largely unmoored from the 2-year/10-year slope. Chart 3Looking For Structural Shifts In Our Yield Curve Models

Global Yield Curve Trades: Netting Returns With Butterflies

Global Yield Curve Trades: Netting Returns With Butterflies

Therefore, we still see value in our curve modeling approach, even in the current environment where central banks are likely to be on hold for a period measured in years, not months. Bottom Line: Butterfly strategies are an effective way to position for changes in the slope of the yield curve without exposure to shifts in the curve. Our current strategic bias is to expect steepening of developed market yield curves through rising longer-term inflation expectations, but our global yield curve models indicate better value in most flattening trades. Thus, we need to be extremely selective in recommending trades based on the results of our yield curve models. Yield Curve Models And Trades By Region In the remaining pages of this report, we present the current read-outs from of our yield curve models for each of the major developed markets. More specifically, we provide the deviations from fair value for different combinations of bullets and barbells and highlight the most attractive butterfly strategy. The deviations from fair value shown in Tables 2-10 are standardized to facilitate comparisons between the different butterfly combinations. In addition, for each country we provide a quick assessment of the performance of these butterfly strategies over time by applying a simple mechanical trading rule. Every month, we enter the most attractive butterfly strategy, i.e. the one with the highest absolute standardized deviation from its model fair value. The overall message from the models is that barbells appear attractive relative to bullets across all the countries shown. However, we will only initiate trades in cases where the model output and our macro outlook complement each other. US Looking solely at our model output, US Treasury curve flatteners appear most attractive, with the long 3-year/30-year barbell vs. 5-year bullet trade displaying the greatest deviation from fair value with a residual of -1.55 (Table 2). However, we are inclined to agree with our colleagues at BCA Research US Bond Strategy on how to interpret Treasury curve valuation in the current environment. They argue that even though steepeners in the US are currently expensive, valuations can become even more overstretched with the Fed signaling no rate increases for at least the next two years and the market priced for an extended period of near-zero rates.3 Table 2US: Butterfly Strategy Valuation: Standardized Residuals

Global Yield Curve Trades: Netting Returns With Butterflies

Global Yield Curve Trades: Netting Returns With Butterflies

Our fundamental bias is towards US Treasury curve steepening, with the Fed locking down the front end of the curve and rising inflation expectations putting upward pressure on longer-term yields. Thus, we are entering into the long 7-year bullet vs. 5/10 barbell trade which has a small but positive model residual of +0.17. That represents a better valuation starting point than the other US butterfly spreads, and is therefore a more efficient and profitable way to position for steepeners becoming even more expensive going forward. As highlighted earlier, nominal yields in the US are also more sensitive to rising inflation expectations—another reason to enter into a curve steepener. The specific securities used to execute this trade, as well as the weights for the barbell component used to the make both legs of the trade duration-equivalent, can be found on Page 27 within our Tactical Trade Overlay table. Nominal yields in the US are also more sensitive to rising inflation expectations—another reason to enter into a curve steepener. The 7-year bullet appears just 1bp cheap according to our model and would only underperform its counterpart given a flattening in the 5-year/10-year Treasury slope greater than 22bps, which we believe is unlikely given the reasons outlined above (Chart 4A). Chart 4AUS 5/7/10 Spread Fair Value Model

US 5/7/10 Spread Fair Value Model

US 5/7/10 Spread Fair Value Model

Chart 4BUS Butterfly Strategy Performance

US Butterfly Strategy Performance

US Butterfly Strategy Performance

Following the mechanical trading rule has delivered steady returns with only a few periods of negative year-over-year returns (Chart 4B). Germany The most attractively valued butterfly combination on the German yield curve is going long the 1-year/30-year barbell and shorting the 5-year bullet, which is almost one standard deviation above its model-implied fair value, with a standardized residual of -0.97 (Table 3). Table 3Germany: Butterfly Strategy Valuation: Standardized Residuals

Global Yield Curve Trades: Netting Returns With Butterflies

Global Yield Curve Trades: Netting Returns With Butterflies

The 5-year bullet appears 29bps expensive according to our model and would only outperform its counterpart given a steepening in the 1-year/30-year German curve slope greater than 50bps (Chart 5A). Chart 5AGermany 1/5/30 Spread Fair Value Model

Germany 1/5/30 Spread Fair Value Model

Germany 1/5/30 Spread Fair Value Model

Chart 5BGermany Butterfly Strategy Performance

Germany Butterfly Strategy Performance

Germany Butterfly Strategy Performance

Following the mechanical trading rule has been quite profitable, delivering consistently positive year-over-year returns for all but the initial period of our sample (Chart 5B). France The most attractively valued butterfly combination on the French OAT yield curve is going long the 2-year/30-year barbell and shorting the 5-year bullet (Table 4). This combination is a little less than one standard deviation over its model-implied fair value with a standardized residual of -0.84. Nominal yields in France are also relatively less correlated with inflation expectations, which makes this a prime candidate for a flattener trade. The specific securities used to execute this trade, as well as the weights for the barbell component used to the make both legs of the trade duration-equivalent, can be found on Page 27 within our Tactical Trade Overlay table. Table 4France: Butterfly Strategy Valuation: Standardized Residuals

Global Yield Curve Trades: Netting Returns With Butterflies

Global Yield Curve Trades: Netting Returns With Butterflies

The 5-year bullet appears 21bps expensive according to our model and would only outperform its counterpart given a steepening in the 2-year/30-year French curve slope greater than 48bps (Chart 6A). Chart 6AFrance 2/5/30 Spread Fair Value Model

France 2/5/30 Spread Fair Value Model

France 2/5/30 Spread Fair Value Model

Chart 6BFrance Butterfly Strategy Performance

France Butterfly Strategy Performance

France Butterfly Strategy Performance

As with Germany, following the mechanical trading rule in the French OAT market has also been profitable, with only three periods of negative year-over-year returns in our sample period (Chart 6B). Italy And Spain In Italy, the most attractively valued butterfly combination is going long the 5-year/30-year barbell and shorting the 10-year bullet – a combination with a standardized residual of -0.79 (Table 5). In Spain, going long the 3-year/30-year barbell and short the 5-year bullet seems most attractive with a standardized residual of -0.83 (Table 6). Of the two peripheral euro area countries, we are choosing to put on a trade in the relatively larger and more liquid Italian government bond market. As with France, Italian nominal yields also display a relatively low beta to inflation breakevens. The specific securities used to execute this trade, as well as the weights for the barbell component used to the make both legs of the trade duration-equivalent, can be found on Page 27 within our Tactical Trade Overlay table. Table 5Italy: Butterfly Strategy Valuation: Standardized Residuals

Global Yield Curve Trades: Netting Returns With Butterflies

Global Yield Curve Trades: Netting Returns With Butterflies

Table 6Spain: Butterfly Strategy Valuation: Standardized Residuals

Global Yield Curve Trades: Netting Returns With Butterflies

Global Yield Curve Trades: Netting Returns With Butterflies

In Italy, the 10-year bullet appears 22bps expensive according to our model and would only outperform its counterpart given a steepening in the 5-year/30-year Italian curve slope greater than 153bps (Chart 7A). Following the mechanical trading rule in Italy has yielded strong excess returns, with only one very short period of negative year-over-year returns in our sample period (Chart 7B). As with Italy, following the mechanical trading rule in Spain has yielded some of the strongest excess returns on a cumulative and year-over-year basis. Chart 7AItaly 5/10/30 Spread Fair Value Model

Italy 5/10/30 Spread Fair Value Model

Italy 5/10/30 Spread Fair Value Model

Chart 7BItaly Butterfly Strategy Performance

Italy Butterfly Strategy Performance

Italy Butterfly Strategy Performance

In Spain, the 5-year bullet appears 14bps expensive according to our model and would only outperform its counterpart given a steepening in the 3-year/30-year Spanish curve slope greater than 47bps (Chart 8A). As with Italy, following the mechanical trading rule in Spain has yielded some of the strongest excess returns on a cumulative and year-over-year basis (Chart 8B). Chart 8ASpain 3/5/30 Spread Fair Value Model

Spain 3/5/30 Spread Fair Value Model

Spain 3/5/30 Spread Fair Value Model

Chart 8BSpain Butterfly Strategy Performance

Spain Butterfly Strategy Performance

Spain Butterfly Strategy Performance

UK On the UK Gilt yield curve, the most attractive butterfly combination is holding a 3-year/20-year barbell versus a 10-year bullet, which currently displays a standardized residual of -1.08 (Table 7). As with France and Italy, not only is this flattener trade attractively valued, the UK is also one of the countries where inflation breakevens are relatively less correlated with nominal yields, making this another excellent candidate for our Tactical Trade Overlay. The specific securities used to execute this trade, as well as the weights for the barbell component used to the make both legs of the trade duration-equivalent, can be found on Page 27. Table 7UK: Butterfly Strategy Valuation: Standardized Residuals

Global Yield Curve Trades: Netting Returns With Butterflies

Global Yield Curve Trades: Netting Returns With Butterflies

The 10-year bullet appears 13bps expensive according to our model and would only outperform its counterpart given a steepening in the 3-year/20-year Gilt curve slope greater than 52bps (Chart 9A). Chart 9AUK 3/10/20 Spread Fair Value Model

UK 3/10/20 Spread Fair Value Model

UK 3/10/20 Spread Fair Value Model

Chart 9BUK Butterfly Strategy Performance

UK Butterfly Strategy Performance

UK Butterfly Strategy Performance

Following the mechanical trading rule in the UK has produced consistent returns on a year-over-year basis (Chart 9B). Canada The most attractively valued butterfly combination on the Canadian yield curve is favoring the 5-year/30-year barbell versus the 7-year bullet, which currently displays a standardized residual of -1.41 (Table 8). Table 8Canada: Butterfly Strategy Valuation: Standardized Residuals

Global Yield Curve Trades: Netting Returns With Butterflies

Global Yield Curve Trades: Netting Returns With Butterflies

The 7-year bullet appears 7bps expensive according to our model and would only outperform its counterpart given a steepening in the 5-year/30-year Canadian curve slope greater than 42bps (Chart 10A). Chart 10ACanada 5/7/30 Spread Fair Value Model

Canada 5/7/30 Spread Fair Value Model

Canada 5/7/30 Spread Fair Value Model

Chart 10BCanada Butterfly Strategy Performance

Canada Butterfly Strategy Performance

Canada Butterfly Strategy Performance

Following the mechanical trading rule in Canada has historically been a good strategy, but we do note two periods of minor losses in 2013 and 2019 (Chart 10B). Japan The most attractively valued butterfly combination on the JGB yield curve is the 5-year/20-year barbell versus the 7-year bullet, which currently has a standardized residual of -1.03 (Table 9). As we noted earlier, however, valuations in the JGB market are likely distorted due to the Bank of Japan’s long-running programs of quantitative easing, zero policy rates and Yield Curve Control that aims to keep the 10-year JGB yield around 0%. Table 9Japan: Butterfly Strategy Valuation: Standardized Residuals

Global Yield Curve Trades: Netting Returns With Butterflies

Global Yield Curve Trades: Netting Returns With Butterflies

The 7-year bullet appears 6bps expensive according to our model and would only outperform its counterpart given a steepening in the 5-year/20-year Japan curve slope greater than 23bps (Chart 11A). Following our mechanical trading rule has produced decent returns, especially given the dormant nature of the JGB market, with only a couple minor periods without positive year-over-year returns. Chart 11AJapan 5/7/20 Spread Fair Value Model

Japan 5/7/20 Spread Fair Value Model

Japan 5/7/20 Spread Fair Value Model

Chart 11BJapan Butterfly Strategy Performance

Japan Butterfly Strategy Performance

Japan Butterfly Strategy Performance

Following our mechanical trading rule has produced decent returns, especially given the dormant nature of the JGB market, with only a couple minor periods without positive year-over-year returns (Chart 11B). Australia The most attractively valued butterfly combination on the Australian yield curve is going long the 2-year/10-year barbell versus the 7-year bullet, displaying a standardized residual of -1.73 (Table 10). Table 10Australia: Butterfly Strategy Valuation: Standardized Residuals

Global Yield Curve Trades: Netting Returns With Butterflies

Global Yield Curve Trades: Netting Returns With Butterflies

The 7-year bullet appears 15bps expensive according to our model and would only outperform its counterpart given a steepening in the 2-year/10-year Australian curve slope greater than 101bps (Chart 12A). Chart 12AAustralia 2/7/10 Spread Fair Value Model

Australia 2/7/10 Spread Fair Value Model

Australia 2/7/10 Spread Fair Value Model

Chart 12BAustralia Butterfly Strategy Performance

Australia Butterfly Strategy Performance

Australia Butterfly Strategy Performance

Compared to the other markets in our analysis, following the mechanical trading rule in Australia has not produced stellar returns (Chart 12B). However, excess returns on a year-over-year basis have been positive barring two periods. Shakti Sharma Research Associate ShaktiS@bcaresearch.com Footnotes 1 Please see BCA Research Global Fixed Income Strategy Special Report, "Global Yield Curve Trades: Follow The Butterflies", dated February 25, 2020, available at gfis.bcaresearch.com. 2 Please see BCA Research Global Fixed Income Strategy Weekly Report, "How To Play The Revival Of Global Inflation Expectations", dated June 23, 2020, available at gfis.bcaresearch.com. 3 Please see BCA Research US Bond Strategy Weekly Report, "Take A Look At High-Yield Technology Bonds", dated June 23, 2020, available at usbs.bcaresearch.com. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Global Yield Curve Trades: Netting Returns With Butterflies

Global Yield Curve Trades: Netting Returns With Butterflies

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Highlights Our intermediate-term timing models suggest the US dollar is broadly overvalued. We are maintaining a modest procyclical currency stance (long NOK, GBP and SEK), but also have a portfolio hedge (short USD/JPY). Go long a basket of petrocurrencies versus the euro. Stay short the gold/silver ratio. Feature Our fundamental intermediate-term timing models (FITM) are one of the toolkits we use in currency management. These simple models enable us to time shifts in developed-market currencies using two key variables. Real Interest Rate Differentials: G10 currencies tend to move with their real rate differentials. Under interest rate parity, if one country is expected to have high interest rates versus another, its currency will rise today so as to gradually depreciate in the future and nullify the interest rate advantage. Risk factor: The ebb and flow of risk aversion affects the path of currencies, as it does their domestic capital markets. Procyclical currencies tend to perform better during risk-on periods. We use high-yield spreads and/or commodity prices as a gauge for risk. For all countries, the variables are highly statistically significant and of the expected signs. These models help us understand in which direction fundamentals are pushing the currencies we look at. These models are more useful as timing indicators on a three-to-nine month basis, as their error terms revert to zero quickly. For the most part, our models have worked like a charm. On a risk adjusted-return basis, a dynamic hedging strategy based on our models has outperformed all static hedging strategies for all investors with six different home currencies since 2001.1 The US Dollar Chart I-1USD Is Overvalued By 4.4%

USD Is Overvalued By 4.4%

USD Is Overvalued By 4.4%

The dollar is a sell, according to the model, with a fair value that is falling much faster than the DXY index itself. Going forward, the Federal Reserve’s dovish stance should keep real interest rate differentials moving against the dollar. This will especially be the case if the authorities move to some form of yield curve control. The wildcard is how risk aversion gyrates as we navigate the volatile summer months, especially given rising geopolitical tensions and the potential for an equity market correction (Chart I-1). One of the factors holding up the dollar is that US domestic growth has been relatively strong, with the Citigroup economic surprise index at the highest level since the inception of the series. For the dollar to decline meaningfully, these positive surprises will need to be repeated abroad. On the data front this week, pending home sales rose 44.3% month-on-month in May, following a 21.8% decline the previous month. House prices are rebounding, to the tune of 4%. The ISM manufacturing index broke out to 52.6 in June from 43.1 the prior month. Job gains for the month of June came in at 4.8 million versus expectations of 3.23 million, pushing the unemployment rate down to 11.1%. These strong numbers provide a high hurdle that non-US growth will need to overcome in order for dollar weakness to continue. The Euro Chart I-2EUR/USD Is Undervalued By 3.8%

EUR/USD Is Undervalued By 3.8%

EUR/USD Is Undervalued By 3.8%

The euro is not excessively undervalued versus the US dollar (Chart I-2). Usually, strong buy signals for the euro have been triggered at a discount of about 10% or so relative to the greenback. That said, the euro can still bounce towards 1.16, or about 3%-4% higher, to bring it back to fair value. The biggest catalyst for the euro remains that interest rate differentials with the US are quite wide and can continue to mean revert. The Treasury-bund spread peaked at 2.8%, and has since lost around 1.7%. Yet, a gap of 100 basis points remains wide by historical standards. On the data front, the CPI numbers from the euro area this week were quite instructive. German inflation came in at +0.8% versus a decline of -0.3% in Spain. In a general sense, inflation in Germany has been outperforming that in the periphery for a few months now, which is a sea-change from the historical trend in eurozone inflation, where both the core and periphery have seen CPI tied at the hip. If rising competitiveness in the periphery is a key driver, then the fair value of the Spanish “peseta” is rapidly catching up to that of the German “Deutsche mark,” which is positive for the euro. The Yen Chart I-3USD/JPY Is Overvalued By 10.3%

USD/JPY Is Overvalued By 10.3%

USD/JPY Is Overvalued By 10.3%

The yen’s fair value has benefited tremendously from the plunge in global bond yields, making rock-bottom Japanese rates relatively attractive from a momentum standpoint (Chart I-3). This has pushed the yen to undervalued levels, supporting our tactically short USD/JPY position. The data out of Japan this week suggest that deflationary forces remain quite strong, which will continue to boost real rates and support the yen. The jobs-to-applicants ratio, a key barometer of labor market health, plunged to 1.20 in May from a cycle high of 1.63. Industrial production fell 25.9% year-on-year in May, the worst since the financial crisis. Meanwhile, the second quarter all-important Tankan survey suggests small businesses will continue to bear the brunt of the economic slowdown. With most of the increase in the Bank of Japan’s balance sheet coming from USD swaps with the Fed rather than asset purchases, it suggests little ammunition or appetite for more stimulus. Fiscal policy remains the wild card that could help lift domestic demand. The British Pound Chart I-4GBP/USD Is Undervalued By 5.9%

GBP/USD Is Undervalued By 5.9%

GBP/USD Is Undervalued By 5.9%

Our model shows the pound as only slightly undervalued, putting our long cable position at risk. The drop in UK real rates since the Brexit referendum has prevented our model from flagging the pound as being much cheaper. Given the potential for added volatility this summer, we are looking to book modest profits on long cable (Chart I-4). Data out of the UK remains grim. Mortgage approvals fell to 9.3K in May, well below expectations. Consumer credit is falling much faster than during the depths of the financial crisis, suggesting all the BoE’s liquidity measures are still not filtering down to certain pockets of the economy. Meanwhile, the trend in the trade balance suggests that the pound has not yet started to reflate the economy. The Canadian Dollar Chart I-5USD/CAD Is Overvalued By 8.1%

USD/CAD Is Overvalued By 8.1%

USD/CAD Is Overvalued By 8.1%

The Canadian dollar is undervalued by about 8% (Chart I-5). Going forward, movements in the Canadian dollar will be largely dictated by interest rate differentials and crude oil prices, which remain supportive for now. We are going long a petrocurrency basket today, one that includes the Canadian dollar. Canadian data have been slowly improving, with housing starts up 20.2% month-on-month in May and existing home sales up 56.9% month-on-month. House prices have also remained resilient. More importantly, foreign investors have used the plunge in oil prices to deploy some fresh capital into Canadian assets. International security transactions in April stood at C$49 billion, the highest on record, and will likely continue to improve as oil prices recover. The Swiss Franc Chart I-6USD/CHF Is Undervalued By 20.6%

USD/CHF Is Undervalued By 20.6%

USD/CHF Is Undervalued By 20.6%

Our models suggest the Swiss franc is tactically at risk (Chart I-6). The main reason is that the franc has remained strong, despite the pickup in risk sentiment since March. Even if strength in the franc is sniffing market turbulence ahead, the yen remains a better and cheaper hedge. The Swiss National Bank continues to intervene in the foreign exchange market, but this week’s data shows that growth in sight deposits is rolling over. This is happening at a time when the economy remains weak. The June PMI came in at 41.9, well below expectations. Deflation has returned to Switzerland, with the CPI print for June at -1.3%, in line with the May number. While this is boosting real rates, the strength in the franc is an unnecessary headache for the SNB, especially against the euro. The Australian Dollar Chart I-7AUD/USD Is Undervalued By 7.3%

AUD/USD Is Undervalued By 7.3%

AUD/USD Is Undervalued By 7.3%

Despite the 20% rally in the Aussie dollar since March, it still remains 7%-8% cheap, according to our FITM (Chart I-7). Typical reflation indicators such as commodity prices and industrial share prices are showing nascent upturns. This suggests that so far, policy stimulus in China has been sufficient to lift commodity demand. Meanwhile, 10-year Aussie government bonds sport a positive spread vis-à-vis 10-year Treasurys. Recent data in Australia have been holding up. The private sector is slowly releveraging, the CBA manufacturing PMI went to 51.2 in June, and the trade balance continues to sport a healthy surplus, at A$8 billion for the month of May. Meanwhile, LNG is a long-term winner from China’s shift away from coal and will continue to benefit Australian terms of trade. We are currently in an LNG glut due to Covid-19, but should electricity generation in China, Japan, and other Asean countries recover to pre-crisis peaks, this will ease the glut. The New Zealand Dollar Chart I-8NZD/USD Is Overvalued By 4.9%

NZD/USD Is Overvalued By 4.9%

NZD/USD Is Overvalued By 4.9%

Unlike the AUD, our FITM for the NZD is in expensive territory. This favors long positions in AUD/NZD (Chart I-8). The New Zealand economy will certainly benefit from having put Covid-19 mostly behind it. Both the ANZ business confidence and activity outlook indices continue to rebound strongly from their lows, with the final print for June released this week. However, the hit to tourism will still impact national income. Meanwhile, the adjustment to housing, especially given the ban to foreign purchases, will continue to constrain domestic spending, relative to its antipodean neighbor. In terms of trading, long CAD/NZD and AUD/NZD remain attractive positions. The Norwegian Krone Chart I-9USD/NOK Is Overvalued By 16.9%

USD/NOK Is Overvalued By 16.9%

USD/NOK Is Overvalued By 16.9%

Our fundamental model for the Norwegian krone shows it as squarely undervalued. This favors long NOK positions, which we have implemented via multiple crosses in our bulletins (Chart I-9). The Norwegian economy remains closely tied to oil, and the negative oil print in April probably marked a structural bottom in prices. With inflation near the central bank’s target and our expectation for oil prices to grind higher, the Norwegian currency will likely fare better than a lot of its G10 peers. In terms of data, the unemployment rate ticked higher in April, but at 4.8%, it remains much lower than other developed economies. Our bet is that once the global economy stabilizes, the Norges Bank might find itself ahead of the pack, in any hiking cycle. The Swedish Krona Chart I-10USD/SEK Is Overvalued By 10.6%

USD/SEK Is Overvalued By 10.6%

USD/SEK Is Overvalued By 10.6%

Like its Scandinavian counterpart, the Swedish krona is also quite cheap and is one of our favorite longs at the moment (Chart I-10). Meanwhile, since the Fed extended its USD swap lines, SEK has lagged the bounce in AUD, NZD, and NOK, suggesting some measure of catch up is due. The export-driven Swedish economy was hit hard by Covid-19, despite no widespread lockdowns being implemented. As such, the Riksbank expanded its QE program this week, boosting asset purchases from SEK 300 billion to SEK 500 billion, until June 2021. In September, it will start purchasing corporate bonds in addition to government, municipal, and mortgage bonds. While the repo rate was left unchanged at zero, interest rates on the standing loan facility were slashed 10 basis points and on weekly extraordinary loans by 20 basis points. These measures should provide sufficient liquidity to allow Sweden to recover as economies open up across the globe. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Please see Foreign Exchange Strategy / Global Asset Allocation Strategy Special Report titled, "Currency Hedging: Dynamic Or Static? – A Practical Guide For Global Equity Investors (Part II)", dated October 13, 2017. Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

Highlights Recommended Allocation

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

The coronavirus pandemic is not over. Enormous fiscal and monetary stimulus will soften the blow to the global economy, but there remain significant risks to growth over the next 12 months. The P/E ratio for global equities is near a record high. This suggests that the market is pricing in a V-shaped recovery, and ignoring the risks. We can, therefore, recommend no more than a neutral position on global equities. But government bonds are even more expensive, with yields having largely hit their lower bound. Stay underweight government bonds, and hedge downside risk via cash. The US dollar is likely to depreciate further: It is expensive, US liquidity has risen faster than elsewhere, interest-rate differentials no longer favor it, and momentum has swung against it. A weakening dollar – plus accelerating Chinese credit growth – should help commodities. We raise the Materials equity sector to neutral, and put Emerging Market equities on watch to upgrade from neutral. Corporate credit selectively remains attractive where central banks are providing a backstop. We prefer A-, Baa-, and Ba-rated credits, especially in the Financials and Energy sectors. Defensive illiquid alternative assets, such as macro hedge funds, have done well this year. But investors should start to think about rotating into private equity and distressed debt, where allocations are best made mid-recession. Overview Cash Injections Vs. COVID Infections The key to where markets will move over the next six-to-nine months is (1) whether there will be a second wave of COVID-19 cases and how serious it will be, and (2) how much appetite there is among central banks and fiscal authorities to ramp up stimulus to offset the damage the global economy will suffer even without a new spike in cases. A new wave of COVID-19 in the northern hemisphere this fall and winter is probable. It is not surprising, after such a sudden stop in global activity between February and May, that economic data is beginning to return to some sort of normality. PMIs have generally recovered to around 50, and in some cases moved above it (Chart 1). Economic data has surprised enormously to the upside in the US, although it is lagging in the euro zone and Japan (Chart 2). Chart 1Data Is Rebounding Sharply

Data Is Rebounding Sharply

Data Is Rebounding Sharply

Chart 2US Data Well Above Expectations

US Data Well Above Expectations

US Data Well Above Expectations

New COVID-19 cases continue to rise alarmingly in some emerging economies and in parts of the US, but in Europe and Asia the pandemic is largely over (for now) and lockdown regulations are being eased, allowing economic activity to resume (Chart 3). Nonetheless, consumers remain cautious. Even where economies have reopened, people remain reluctant to eat in restaurants, to go on vacation, or to visit shopping malls (Chart 4). While shopping and entertainment activities are now no longer 70-80% below their pre-pandemic levels, as they were in April and May, they remain down 20% or more (Chart 5). Chart 3Few COVID-19 Cases Now In Europe And Asia

Few COVID-19 Cases Now In Europe And Asia

Few COVID-19 Cases Now In Europe And Asia

Chart 4Consumers Still Reluctant To Go Out

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Chart 5Spending Well Below Pre-Pandemic Levels

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

So how big is the risk of further spikes in COVID-19 cases? Speaking on a recent BCA Research webcast, the conclusion of Professor Peter Doherty, a Nobel prize-winning immunologist connected to the University of Melbourne, was that, “It’s not unlikely we’ll see a second wave.”1 But experts can’t be sure. It seems that the virus spreads most easily when people group together indoors. That is why US states where it is hot at this time of the year, such as Arizona, have seen rising infections. This suggests that a new wave in the northern hemisphere this fall and winter is probable. Offsetting the economic damage caused by the coronavirus has been the staggering amount of liquidity injected by central banks, and huge extra fiscal spending. Major central bank balance-sheets have grown by around 5% of global GDP since March, causing a spike in broad money growth everywhere (Chart 6). Fiscal spending programs also add up to around 5% of global GDP (Chart 7), with a further 5% or so in the form of loans and guarantees. Chart 6Remarkable Growth In Money Supply...

Remarkable Growth In Money Supply...

Remarkable Growth In Money Supply...

Chart 7...And Unprecedented Fiscal Spending

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

But is it enough? Considerable damage has been done by the collapse in activity. Bankruptcies are rising (Chart 8) and, with activity still down 20% in consuming-facing sectors, pressure on companies’ business models will not ease soon – particularly given evidence that banks are tightening lending conditions. Household income has been buoyed by government wage-replacement schemes, handout checks, and more generous unemployment benefits (Chart 9). But, when these run out, households will struggle if the programs are not topped up. Central banks are clearly willing to inject more liquidity if need be. But the US Congress is prevaricating on a second fiscal program, and the Merkel/Macron proposed EUR750 billion spending package in the EU is making little progress. It will probably take a wake-up call from a sinking stock market to push both to take action. Chart 8Companies Feeling The Pressure

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Considerable damage has been done by the collapse in activity. We lowered our recommendation for global equities to neutral from overweight in May. We are still comfortable with that position. Given the high degree of uncertainty, this is not a market in which to take bold positioning in a portfolio. When you have a high conviction, position your portfolio accordingly; but when you are unsure, stay close to benchmark. With stocks up by 36% since their bottom on March 23rd, the market is pricing in a V-shaped recovery and not, in our view, sufficiently taking into account the potential downside risks. P/E ratios for global stocks are at very stretched levels (Chart 10). Chart 9Households Dependent On Handouts

More Stimulus Forthcoming? Households Dependent On Handouts

More Stimulus Forthcoming? Households Dependent On Handouts

Chart 10Global Equities Are Expensive...

Global Equities Are Expensive...

Global Equities Are Expensive...

Nonetheless, we would not bet against equities. Simply, there is no alternative. Most government bond yields are close to their effective lower bound. Gold looks overbought (in the absence of a significant spike in inflation which, while possible, is unlikely for at least 12 months). No sensible investor in, say, Germany would want to hold 10-year government bonds yielding -50 basis points. Assuming 1.5% average annual inflation over the next decade, that guarantees an 18% real loss over 10 years. The only investors who hold such positions have them because their regulators force them to. Chart 11...But They Are Cheap Against Bonds

...But They Are Cheap Against Bonds

...But They Are Cheap Against Bonds

The Sharpe ratio on 10-year US Treasurys, which currently yield 70 BPs, will be 0.16 (assuming volatility of 4.5%) over the next 10 years. A simple calculation of the likely Sharpe ratio for US equities (earnings yield of 4.5% and volatility of 16%) comes to 0.28. One would need to assume a disastrous outlook for the global economy to believe that stocks will underperform bonds in the long run. Though equities are expensive, bonds are even more so. The equity risk premium in most markets is close to a record high (Chart 11). With such mathematics, it is hard for a long-term oriented investor to be underweight equities. Garry Evans, Senior Vice President Chief Global Asset Allocation Strategist garry@bcaresearch.com What Our Clients Are Asking Chart 12Premature Opening Of The Economy Is Risky

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

COVID-19: How Risky Is Reopening? Countries around the world are rushing to reopen their economies, claiming victory over the pandemic. It is hard to be sure whether a second wave of COVID-19 will hit. What is certain, however, is that a premature relaxation of measures is as risky as a tardy initial response. That was the lesson from our Special Report analyzing the Spanish Flu of 1918. The risk is certainly still there: Herd immunity will require around 70% of the population to get sick, and a drug or vaccine will (even in an optimistic scenario) not be available until early next year. China and South Korea, for example, after reporting only a handful of daily new cases in early May, were forced to impose new restrictions over the past few weeks as COVID-19 cases spiked again (Chart 12, panel 1). We await to see if other European countries, such as Italy, Spain, and France will be forced to follow. Some argue that even if a second wave hits, policy makers – to avoid a further hit to economic output – will favor the “Swedish model”: Relying on people’s awareness to limit the spread of the virus, without imposing additional lockdowns and restrictions. This logic, however, is risky since Sweden suffered a much higher number of infections and deaths than its neighboring countries (panel 2). The US faces a similar fate. States such as Florida, Arizona, and Texas are recording a sharp rise in new infections as lockdowns are eased. In panel 3, we show the daily number of new infections during the stay-at-home orders (the solid lines) and after they were lifted (dashed lines). To an extent, increases in infections are a function of mass testing. However, what is obvious is that the percentage of positive cases per tests conducted has started trending upwards as lockdown measures were eased (panel 4). Our base case remains that new clusters of infections will emerge. Eager citizens and rushed policy decisions will fuel further contagion. If the Swedish model is implemented, lives lost are likely to be larger than during the first wave. Chart 13W Or U, Says The OECD

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

What Shape Will The Recovery Be: U, V, W, Or Swoosh? The National Bureau of Economic Research (NBER) Business Cycle Dating Committee has already declared that the US recession began in March. The economists’ consensus is that Q2 US GDP shrank by 35% QoQ annualized. But, after such a momentous collapse and with a moderate move back towards normalcy, it is almost mathematically certain that Q3 GDP will show positive quarter-on-quarter growth. So does this mean that the recession lasted only one quarter, i.e. a sharp V-shape? And does this matter for risk assets? The latest OECD Economic Outlook has sensible forecasts, using two “equally probable” scenarios: One in which a second wave of coronavirus infections hits before year-end, requiring new lockdowns, and one in which another major outbreak is avoided.2 The second-wave scenario would trigger a renewed decline in activity around the turn of 2020-21: a W-shape. The second scenario looks more like a U-shape or swoosh, with an initial rebound but then only a slow drawn-out recovery, with OECD GDP not returning to its Q4 2019 level before the end of 2021 (Chart 13). Chart 14Unemployment Will Take A Long Time To Come Down

Unemployment Will Take A Long Time To Come Down

Unemployment Will Take A Long Time To Come Down

Why is it likely that, in even the absence of a renewed outbreak of the pandemic, recovery would be faltering? After an initial period in which many furloughed workers return to their jobs, and pent-up demand is fulfilled, the damage from the sudden stop to the global economy would kick in. Typically, unemployment rises rapidly in a recession, but recovers only over many years back to its previous low (Chart 14). This time, many firms, especially in hospitality and travel, will have gone bust. Capex plans are also likely to be delayed. Chart 15Sub-Potential Output Can Be Good For Risk Assets

Sub-Potential Output Can Be Good For Risk Assets

Sub-Potential Output Can Be Good For Risk Assets

However, a slow recovery is not necessarily bad for risk assets. Periods when the economy is recovering but remains well below potential (such as 2009-2015) are typically non-inflationary, which allows central banks to continue accommodation (Chart 15). Is This Sharp Equity Rebound A Retail Investor Frenzy? The answer to this question is both Yes and No. From a macro fundamental perspective, the answer is No, because coordinated global reflationary policies and medical developments to fight the coronavirus have been the key drivers underpinning this equity rebound. “COVID-on” and “COVID-off” have been the main determinants for equity rotations. Chart 16Active Retail Participation Lately

Retail Investors Have Driven Up Trading Volumes Active Retail Participation Lately

Retail Investors Have Driven Up Trading Volumes Active Retail Participation Lately

But at the individual stock level, the answer is Yes. Some of the unusual action in beaten-down stocks over the past few weeks may have its origin in an upsurge of active retail participation (Chart 16). Retail investors on their own are not large enough to influence the market direction. Many online brokerages do not charge any commission for trades, but make money by selling order flows to hedge funds. As such, the momentum set in motion by retail investors may have been amplified by fast-money pools of capital. Retail participation in some beaten-down stocks has also provided an opportunity for institutions to exit. BCA’s US Investment Strategy examined the change in institutional ownership of 12 stocks in three stressed groups between February 23 and June 14, as shown in Table 1. In the case of these stocks, retail investors have served as liquidity providers to institutional sellers seeking to exit their holdings. The redeployment of capital by institutions into large-cap and quality names may have pushed up the overall equity index level. Table 1Individuals Have Replaced Institutions

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

Quarterly Portfolio Outlook: Cash Injections Versus COVID Infections

How Will Inflation Behave After COVID? Some clients have asked us about the behavior of inflation following the COVID epidemic. Over the very short term, inflation could have more downside. However, this trend is likely to reverse rapidly. Headline inflation is mainly driven by changes in the oil price and not by its level. Thus, even if oil prices were to stay at current low levels, the violent recovery of crude from its April lows could bring headline inflation near pre-COVID levels by the beginning of 2021 (Chart 17, top panel). This effect could become even larger if our Commodity strategist price target of 65$/barrel on average in 2021 comes to fruition. Chart 17Rising Oil Prices And Fiscal Stimulus Will Boost Inflation

Rising Oil Prices And Fiscal Stimulus Will Boost Inflation

Rising Oil Prices And Fiscal Stimulus Will Boost Inflation

But will this change in inflation be transitory or will it prove to be sustainable? We believe it will be the latter. The COVID crisis may have dramatically accelerated the shift to the left in US fiscal policy. Specifically, programs such as universal basic income may now be within the Overton window3 of acceptable fiscal policy, thanks to the success of the CARES Act in propping up incomes amid Depression-like levels of unemployment (middle panel). Meanwhile there is evidence that this stimulus is helping demand to recover rapidly: Data on credit and debit card trends show that consumer spending in the US has staged a furious rally, particularly among low-income groups, where spending has almost completely recovered (bottom panel). With entire industries like travel, restaurants and lodging destroyed for the foreseeable future, the political will to unwind these programs completely is likely to be very low, given that most policymakers will be queasy about an economic relapse, even after the worst of the crisis has passed. Such aggressive fiscal stimulus, coupled with extremely easy monetary policy will likely keep inflation robust on a cyclical basis. Global Economy Overview: March-May 2020 will probably prove to be the worst period for the global economy since the 1930s, as a result of the sudden stop caused by the coronavirus pandemic and government-imposed restrictions on movement. As the world slowly emerges from the pandemic, data has started to improve. But there remain many risks, and global activity is unlikely to return to its end-2019 level for at least another two years. That means that further fiscal and monetary stimulus will be required. The speed of the recovery will be partly determined by how much more aggressively central banks can act, and by how much appetite there is among fiscal authorities to continue to bail out households and companies which have suffered a catastrophic loss of income. US: The economy has shown signs of a strong rebound from the coronavirus slump in March and April. Q2 GDP probably fell around 35% quarter-on-quarter annualized, but Q3 will almost certainly show positive growth. The Economic Surprise Index (Chart 18, panel 1) has bounced to a record high, after stronger-than expected May data, for example the 16% month-on-month growth in durable goods orders, and 18% in retail sales. But the next stage of the recovery will be harder: continuing unemployment claims in late June were still 19.5 million. Bankruptcies are rising, and banks are tightening lending conditions. One key will be whether Congress can pass a further fiscal program before the emergency spending runs out in July. Euro Area: Although pandemic lockdowns ended in Europe earlier than in the US, recovery has been somewhat slower. The euro zone PMI rebounded to close to 50 in June but, given that activity had collapsed in February-May, it is surprising (since the PMI measures month-on-month change) that it is not well above 50 (Chart 19, panel 1). Fiscal and monetary stimulus, while large, has not been as aggressive as in the US. The ECB remains circumscribed (as least psychologically) by the German constitutional court’s questioning the justification for previous QE. Germany and France have agreed a EUR750 billion additional package to help the periphery, but this has still to be finalized, due to the opposition of some smaller northern EU members. Chart 18Economic Data Has Started To Surprise To The Upside...

Economic Data Has Started To Surprise To The Upside...

Economic Data Has Started To Surprise To The Upside...

Chart 19...But From Dramatically Low Levels

...But From Dramatically Low Levels

...But From Dramatically Low Levels

Japan: Although Japan escaped relatively easily from pandemic deaths and lockdowns, its economy remains notably weak. New machinery orders in April were still falling 18% YoY, and exports in May were down 28% YoY. The poor economic performance is due to its dependence on overseas demand, distrust in the government, the lingering effects of the ill-timed consumption tax rise last October, and limited room for manoeuvre by the Bank of Japan. The government has announced fiscal stimulus equal to a barely credible 40% of GDP, but much of this is double-counting, and less than half of the household and small-company income-replacement handouts announced in March have so far been paid out. Emerging Markets: India, Brazil, and other Latin American countries are now bearing the brunt of the coronavirus pandemic. Economies throughout Emerging Markets have weakened dramatically as a result. Two factors may come to their aid, though. China is again ramping up monetary stimulus, with a notable acceleration of credit growth over the past three months. Its economy has stabilized as a result, as PMIs show (panel 3). And the US dollar has begun to depreciate, which will take pressure off EM borrowers in foreign currencies, and boost commodities prices. The biggest risk is that many EM central banks have now resorted to printing money, which could result in currency weakness and inflation at a later stage. Interest Rates: Central banks in advanced economies have lowered policy rates to their effective lower bound. It is unlikely the Fed will cut into negative territory, having seen the nefarious effects of this on the banking systems in Japan and the euro zone, and particularly due to the large money-market fund industry in the US, which is unviable with negative rates. Reported inflation everywhere, both headline and core, has fallen sharply, but this is somewhat misleading since the price of items that households in lockdown have actually been buying has risen sharply. Markets have started to sniff out the possibility of inflation once the pandemic is over, and inflation expectations have begun to rise (panel 4). For now, deflation is likely to be the bigger worry and so we do not expect long-term rates to rise much this year. But a sharp pickup in inflation is a definite risk on the 18-24 month time horizon. Global Equities Chart 20Stretched Valuation

Has Earnings Growth Bottomed?

Has Earnings Growth Bottomed?

Valuation Concern: Global equities staged an impressive rebound of 18% in Q2 after the violent selloff in Q1, thanks to the “whatever-it-takes” support from central banks, and massive fiscal stimulus packages around the globe. Within equities, our country allocation worked well, as the US outperformed both the euro Area and Japan. Our sector performance was mixed: The overweight in Info Tech and underweight in Utilities and Real Estate generated good profits, but the overweights in Industrials and Healthcare and the underweight in Materials suffered losses. As shown in Chart 20, even before the pandemic-induced profit contraction, forward earnings were already only flattish in 2019. The sharp selloff in Q1 brought the valuation multiple back down only to the same level as at the end of 2018. Currently, this valuation measure stands at the highest level since the Great Financial Crisis after a 37% increase in Q2 2020 alone. Such a rapid multiple expansion was one of the key reasons why we downgraded equities to Neutral in May at the asset-class level. Going forward, BCA’s house view is that easy monetary policies and stimulative fiscal policies globally will help to revive economic activity, and that a weakening US dollar will give an additional boost to the global economy, especially Emerging Markets. Consequently, we upgrade global Materials to neutral from underweight and put Emerging Market equities (currently neutral) on an upgrade watch (see next page). Warming To Reflation Plays Chart 21EM On Upgrade Watch

EM On Upgrade Watch

EM On Upgrade Watch

Taking risk where risks will most likely be rewarded has been GAA’s philosophy in portfolio construction. As equity valuation reaches an extreme level, the natural thing to do is to rotate into less expensive areas within the equity portfolio. As shown in panel 2 of Chart 21, EM equities are trading at a 31% discount to DM equities based on forward P/E, which is 2 standard deviations below the average discount of past three years. Valuation is not a good timing tool in general, but when it reaches an extreme, it’s time to pay attention and check the fundamental and technical indicators. We are putting EM on upgrade watch (from our current neutral stance, and also closing the underweight in Materials given the close correlation of the two (Chart 21, panel 1). Three factors are on our radar screen: First, reflation efforts in China. The change in China’s total social financing as a % of GDP has been on the rise and BCA’s China Investment Strategy Team expects it to increase further. This bodes well for the momentum of the EM/DM performance, which is improving, albeit still in negative territory (panel 3). Second, a weakening USD is another key driver for EM/DM and the Materials sector relative performance as shown in panel 4. According to BCA’s Foreign Exchange Strategy, the US dollar is likely to churn on recent weakness before a cyclical bear market fully unfolds.4 Last but not least, the recent surge in the number of the coronavirus infections in EM economies, especially Brazil and India, has increased the likelihood of a second wave of lockdowns. Government Bonds Chart 22Bottoming Bond Yields

Bottoming Bond Yields

Bottoming Bond Yields

Maintain Neutral Duration. Global bond yields barely moved in Q2 as the global economy rebounded from the COVID-induced recession low (Chart 22, panel 1). The upside surprise in economic data releases implies that global bond yields will likely go up in the near term (panel 2). For the next 9-12 months, however, the upside in global bond yields might be limited given the increasing likelihood of a new set of COVID-19 lockdowns due to the recent surge in new infections globally, especially in the US, Brazil, and India. As such, a neutral duration stance is still appropriate (Chart 22). Chart 23Inflation Expectations On The Rise

Inflation Expectations On The Rise

Inflation Expectations On The Rise

Favor Linkers Vs. Nominal Bonds. To fight off the risk of an extended recession, policymakers around the world are determined to continue to use aggressive monetary and fiscal stimulus to boost the global economy. The combined effect of extremely accommodative policy settings and the rebound in global commodity prices, especially oil prices, will push up inflation expectations (Chart 23). Higher inflation expectations will no doubt push up nominal bond yields somewhat, but according to BCA’s Global Fixed Income Strategy (GFIS), positioning for wider inflation breakevens remains the “cleaner” way to profit for the initial impact of policy reflation.5 According to GFIS valuation models, inflation-linked bonds in Canada, Italy, Germany, Australia, France, and Japan should be favored over their respective nominal bonds. Corporate Bonds Chart 24Better Value In A-rated and Baa-rated Credit

Better Value In A-rated and Baa-rated Credit

Better Value In A-rated and Baa-rated Credit

Investment-grade: Since we moved to overweight on investment-grade credit within the fixed-income category, it has produced 8.8% in excess returns over duration-matched government bonds. We remain overweight, given that the Federal Reserve has guaranteed to rollover debt for investment-grade issuers, essentially eliminating the left tail of returns. Moreover, the Fed has begun buying both ETFs and individual bond issues, in an effort to keep financial stress contained during the pandemic. However, there are some sectors within the investment-grade space that are more attractive than others. Specifically, our Global Fixed Income Strategy team has shown that A-rated and Baa-rated bonds are more attractive than higher-rated credits (Chart 24). Meanwhile, our fixed-income strategist are overweight Energy and Financials at the sector level.6 High-yield: High-yield bonds – where we have a neutral position - have delivered 11.5% of excess return since April. We are maintaining our neutral position. At current levels, spreads no longer offer enough value to justify an overweight position, specially if one considers that defaults in junk credits could be severe, since the Fed doesn’t offer the same level of support that it provides for investment-grade issuers. Within the high-yield space, we prefer Ba-rated credit. Fallen angels (i.e. bonds which fell to junk status) are particularly attractive given that most qualify for the Fed’s corporate buying program, since issuers which held at least a Baa3 rating as of March 22 are eligible for the Fed’s lending facilities.7 Commodities Chart 25Commodity Prices Will Rise As Growth Revives

Commodity Prices Will Rise As Growth Revives

Commodity Prices Will Rise As Growth Revives

Energy (Overweight): A near-complete lack of storage led WTI prices to go into freefall and trade at -$40 in mid-April: The largest drawdown in oil prices over the past 30 years (Chart 25, panel 1). Since then, oil prices have picked up, reaching their pre-“sudden stop” levels, as the OPEC 2.0 coalition slashed production. Nevertheless, excess supply remains a key issue. Crude inventories have been on the rise as global crude demand weakens. Year-to-date inventories have increased by over 100 million barrels, and current inventories cover over 40 days of supply (panel 2). As long as the OPEC supply cuts hold and demand picks up over the coming quarters, the excess inventories are likely to be worked off. BCA’s oil strategists expect Brent crude to rise back above $60 by year-end. Industrial Metals (Neutral): Last quarter, we flagged that industrial metals face tailwinds as fiscal packages get rolled out globally – particularly in China where infrastructure spending is expected to increase by 10% in the latter half of the year. Major industrial metals have yet to recover to their pre-pandemic levels but, as lockdown measures are lifted and activity is restored, prices are likely to start to rise strongly (panel 3). Precious Metals (Neutral): The merits of holding gold were not obvious during the first phase of the equity sell-off in February and March. Gold prices tumbled as much as 13%, along with the decline in risk assets. Since the beginning of March, however, there have been as many positive return days as there has been negative (panel 4). However, given the uncertainty regarding a second wave of the pandemic, and the rise in geopolitical tensions between the US and China, as well as between India and China, we continue to recommend holding gold as a hedge against tail risks. Currencies Chart 26Momentum For The Dollar Has Turned Negative

Momentum For The Dollar Has Turned Negative

Momentum For The Dollar Has Turned Negative

US Dollar: The DXY has depreciated by almost 3% since the beginning of April. Currently, there are multiple forces pushing the dollar lower: first, interest-rate differentials no longer favor the dollar Second, liquidity conditions have improved substantially thanks to the unprecedented fiscal and monetary stimulus, as well as coordinated swap lines between the Fed and other central banks to keep USD funding costs contained. Third, momentum in the DXY – one of the most reliable indicators for the dollar – has turned negative (Chart 26– top & middle panel). Taking all these factors into account, we are downgrading the USD from neutral to underweight. Euro: The euro should benefit in an environment where the dollar weakens, and global growth starts to rebound. Moreover, outperformance by cyclical sectors as well as concerns about over-valuation in US markets should bring portfolio flows to the Euro area. Therefore, we are upgrading the euro from neutral to overweight. Australian dollar: Last quarter we upgraded the Australian dollar to overweight due to its attractive valuations, as well as the effect of the monetary stimulus coming out of China. This proved to be the correct approach: AUD/USD has appreciated by a staggering 13% since our upgrade – the best performance of any G10 currency versus the dollar this quarter (bottom panel). Overall, while we believe that Chinese stimulus should continue to prop up the Aussie dollar, valuations are no longer attractive with AUD/USD hovering around PPP fair value. This means that the risk-reward profile of this currency no longer warrants an overweight position. Thus, we are downgrading the AUD to neutral. Alternatives Chart 27Opportunities Will Emerge In Private Equity

Opportunities Will Emerge In Private Equity

Opportunities Will Emerge In Private Equity

Return Enhancers: Over the past year, we have flagged that hedge funds, particularly macro funds, will outperform other risk assets during recessions and periods of high market stress. This played out as we expected: macro hedge funds’ drawdown from January to March 2020 was a mere 1.4%, whereas other hedge funds’ drawdown ranged between 9% and 19% and global equities fell as much as 35% from their February 2020 peak. (Chart 27, panel 1). However, unlike other recessions, the unprecedented sum of stimulus should place a floor under global growth. Given the time it takes to move allocations in the illiquid space, investors should prepare for new opportunities within private equity as global growth bottoms in the latter half of this year. In an earlier Special Report, we stressed that funds raised in late-cycle bull markets tend to underperform given their high entry valuations. If previous recessions are to provide any guidance, funds raised during recession years had a higher median net IRR than those raised in the latter year of the preceding bull market (panel 2). Inflation Hedges: Over the past few quarters, we have been highlighting commodity futures as a better inflation hedge relative to other assets (e.g. real estate). Within the asset class, assuming a moderate rise in inflation over the next 12-18 months as we expect, energy-related commodities should fare best (panel 3). This corroborates with our overweight stance on oil over the next 12 months (see commodities section). Volatility Dampeners: We have been favoring farmland and timberland since Q1 2016. While both have an excel track record of reducing volatility, farmland’s inelastic demand during slowdowns will be more beneficial. Investors should therefore allocate more to farmland over timberland (panel 4). Risks To Our View The risks are skewed to the downside. After such a big economic shock, damage could appear in unexpected places. Banking systems in Europe, Japan, and the Emerging Markets (but probably not the US) remain fragile. Defaults are growing in sub-investment grade debt; mortgage-backed securities are experiencing rising delinquencies; student debt and auto loans are at risk. Emerging Market borrowers, with $4 trn of foreign-currency debt, are particularly vulnerable. The length and depth of recessions and bear markets are determined by how serious are the second-round effects of a cyclical slowdown. If the current recession really lasted only from March to July, and the bear market from February to March, this will be very unusual by historical standards (Chart 28). Chart 28Can The Recession And Bear Market Really Be All Over Already?

Can It Really Be Over Already?

Can It Really Be Over Already?

Upside surprises are not impossible. A vaccine could be developed earlier than the mid-2021 that most specialists predict. But this is unlikely since the US Food and Drug Administration will not fast-track approval given the need for proper safety testing. If economies continue to improve and newsflow generally remains positive over the coming months, more conservative investors could be sucked into the rally. Evidence suggests that the rebound in stocks since March was propelled largely by hedge funds and individual day-traders. More conservative institutions and most retail investors remain pessimistic and have so far missed the run-up (Chart 29). One key, as so often, is the direction of US dollar. Further weakness in the currency would be a positive indicator for risk assets, particularly Emerging Market equities and commodities. In this Quarterly, we have moved to bearish from neutral on the dollar (see Currency section for details). Momentum has turned negative, and both valuation and relative interest rates suggest further downside. But it should be remembered that the dollar is a safe-haven, counter-cyclical currency (Chart 30). Any rebound in the currency would not only signal that markets are entering a risk-off period, but would cause problems for Emerging Market borrowers that need to service debt in an appreciating currency. Chart 29Many Investors Are Still Pessimistic

Many Investors Are Still Pessimistic

Many Investors Are Still Pessimistic

Chart 30Dollar Direction Is Key

Dollar Direction Is Key

Dollar Direction Is Key

Footnotes 1 Please see BCA Webcast, "The Way Ahead For COVID-19: An Expert's Views," available at bcaresearch.com. 2 OECD Economic Outlook, June 2020, available at https://www.oecd-ilibrary.org/economics/oecd-economic-outlook/volume-2020/issue-1_0d1d1e2e-en 3 The Overton window, named after Joseph P. Overton, is the range of policies politically acceptable to the mainstream population at a given time. It frames the range of policies that a politician can espouse without appearing extreme. 4 Please see Foreign Exchange Strategy Weekly Report, “DXY: False Breakdown Or Cyclical Bear Market?” dated June 5, 2020 available at fes.bcaresearch.com 5 Please see Global Fixed Income Strategy Weekly Report, “How To Play The Revival Of Global Inflation Expectations” dated June 23, 2020 available at gfis.bcaresearch.com 6 Please see Global Fixed Income Strategy, "Hunting For Alpha In The Global Corporate Bond Jungle," dated May 27, 2020, available at gfis.bcaresearch.com. 7 Fallen angels also outperform during economic recoveries. Please see Global Asset Allocation Special Report, "Even Fallen Angels Have A Place In Heaven," dated November 15, 2020, available at gaa.bcaresearch.com. GAA Asset Allocation

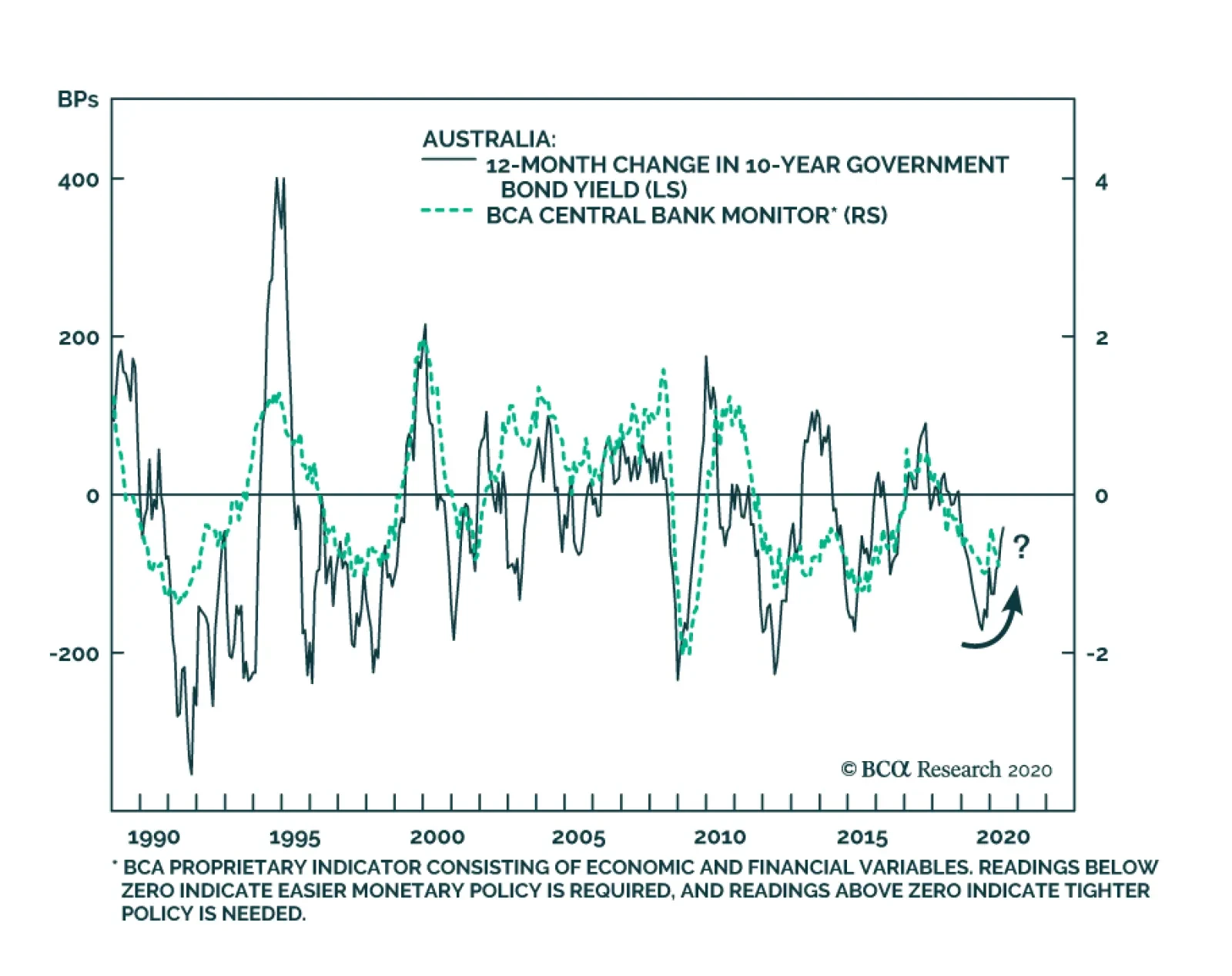

BCA Research's Global Fixed Income Strategy service's Reserve Bank of Australia (RBA) monitor may be turning the corner after Australia delivered 125bps of stimulus since June 2019. The Australian unemployment gap has widened dramatically, owing to job…

Highlights In this Weekly Report, we present our semi-annual chartbook of the BCA Central Bank Monitors. All of the Monitors are now below the zero line, indicating the need for continued easy global monetary policy to help mitigate the COVID-19 recession (Chart of the Week). Central bankers have already responded in an intense and rapid fashion to the crisis, delivering a series of rate cuts, increased asset purchase programs and measures to support bank lending to businesses suffering under quarantines. All of these vehicles have helped trigger a powerful rally in global bond markets that helped revitalize risk assets as well. After the coordinated global easing response of the past few months, the optimal policy choices now differ from country to country. This creates opportunities to benefit from country allocation decisions even in a world of puny government bond yields. The overall signal from our Central Bank Monitors is still bond bullish, however – at least over the next few months until there is evidence of how fast global growth is rebounding from the COVID-19 lockdowns. An Overview Of The BCA Central Bank Monitors Chart of the WeekUltra-Accommodative Monetary Policies Are Still Required

Ultra-Accommodative Monetary Policies Are Still Required

Ultra-Accommodative Monetary Policies Are Still Required

Chart 2A Bond-Bullish Message From Our CB Monitors

A Bond-Bullish Message From Our CB Monitors

A Bond-Bullish Message From Our CB Monitors