Australia

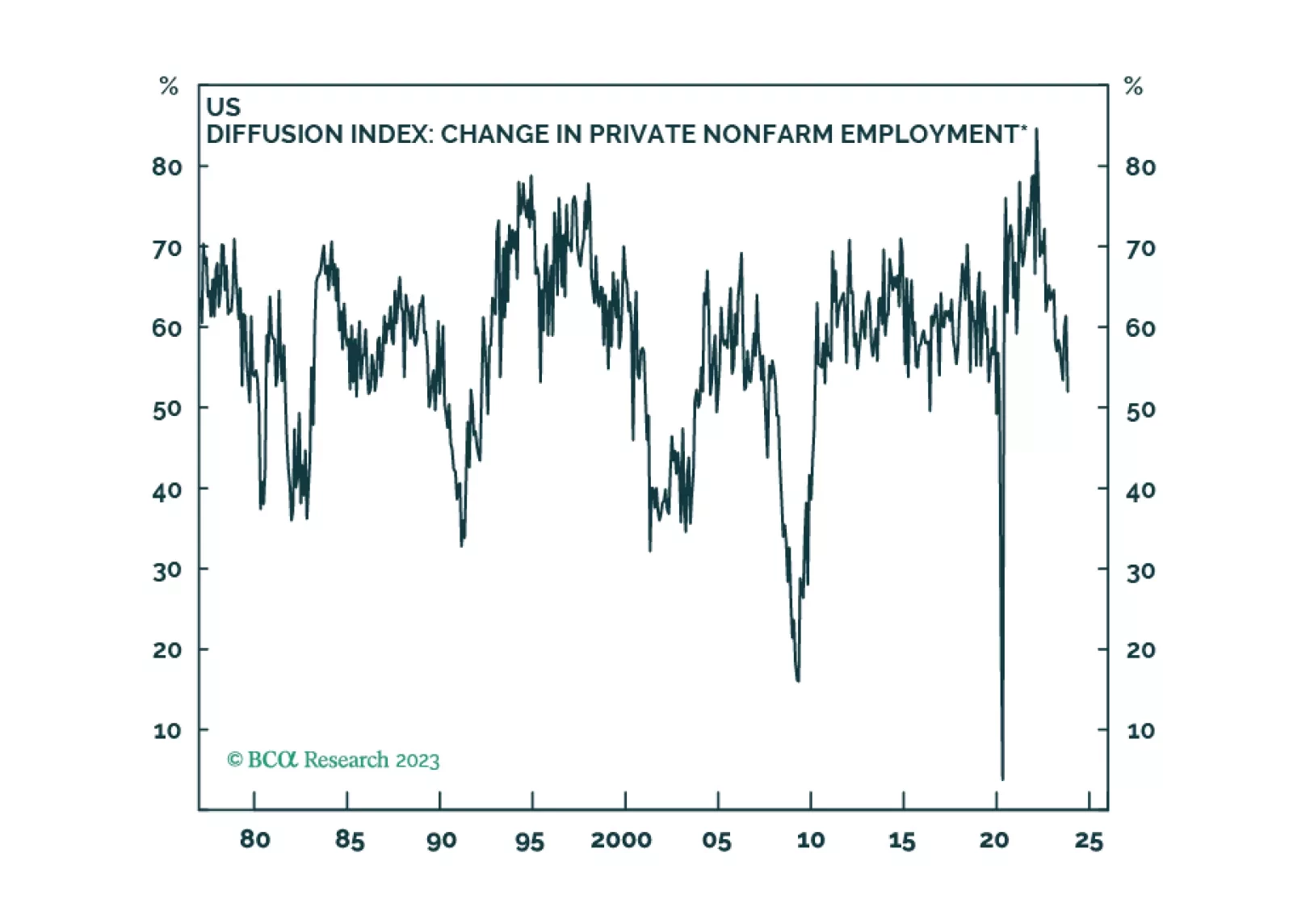

Investors have taken comfort in the fact that unemployment has remained low in the major economies. But underneath the surface, there are clear signs that labor demand is weakening. The clock keeps ticking towards our H2 2024 recession call. After being bullish on risk assets last year, we are slowly turning more defensive.

In this, our final report of the year, we present our main global fixed income investment themes and recommendations for 2024.

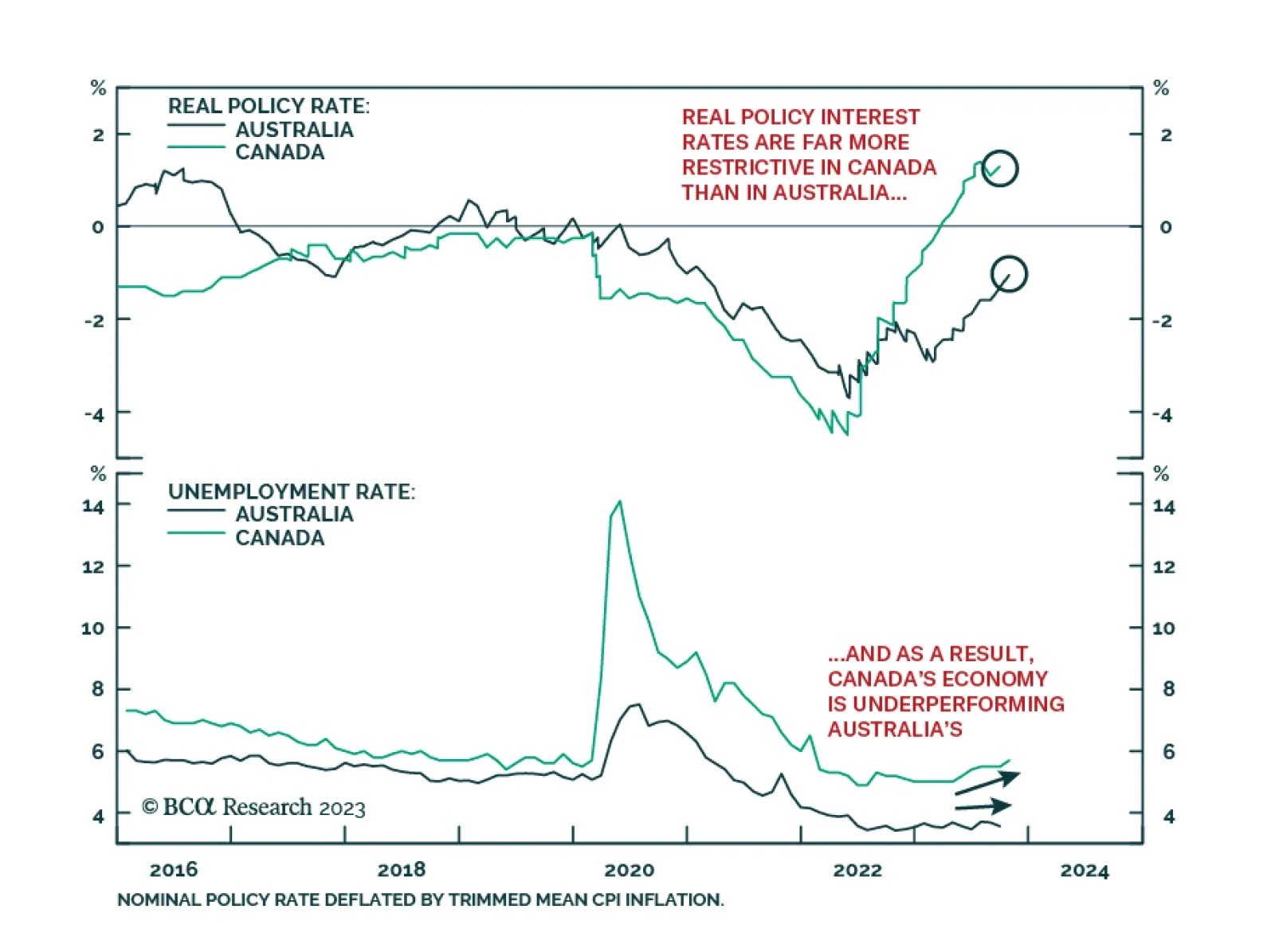

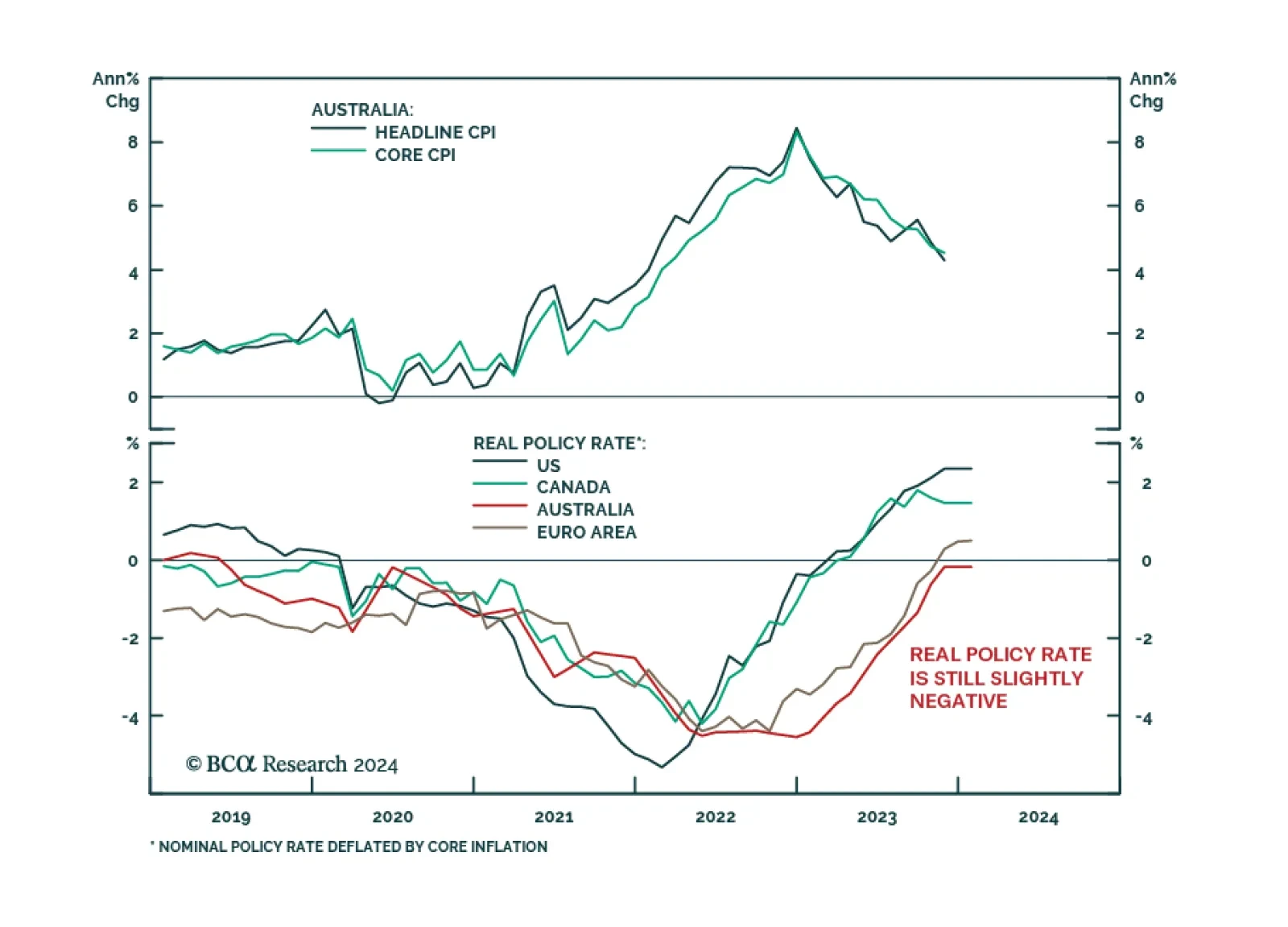

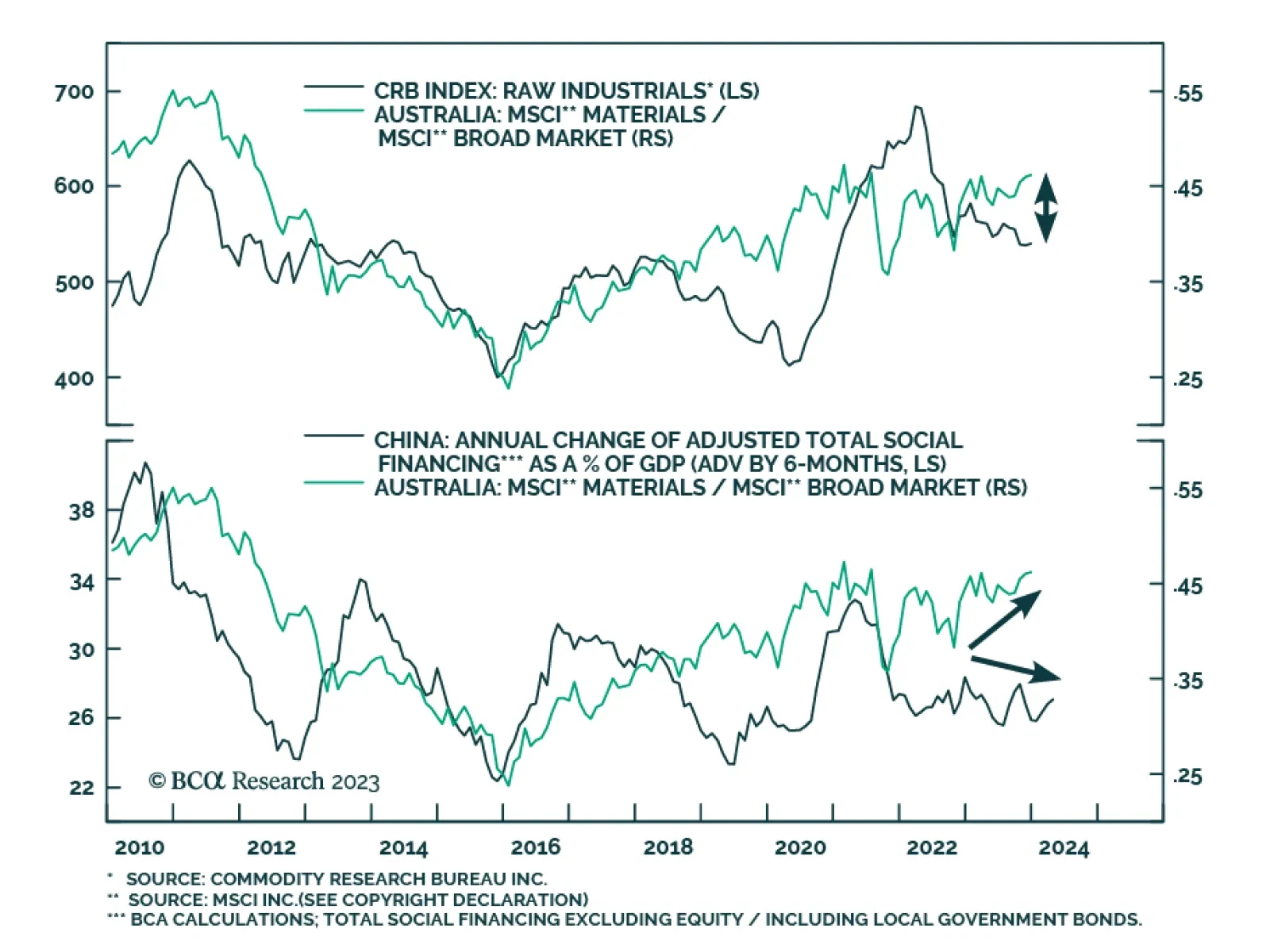

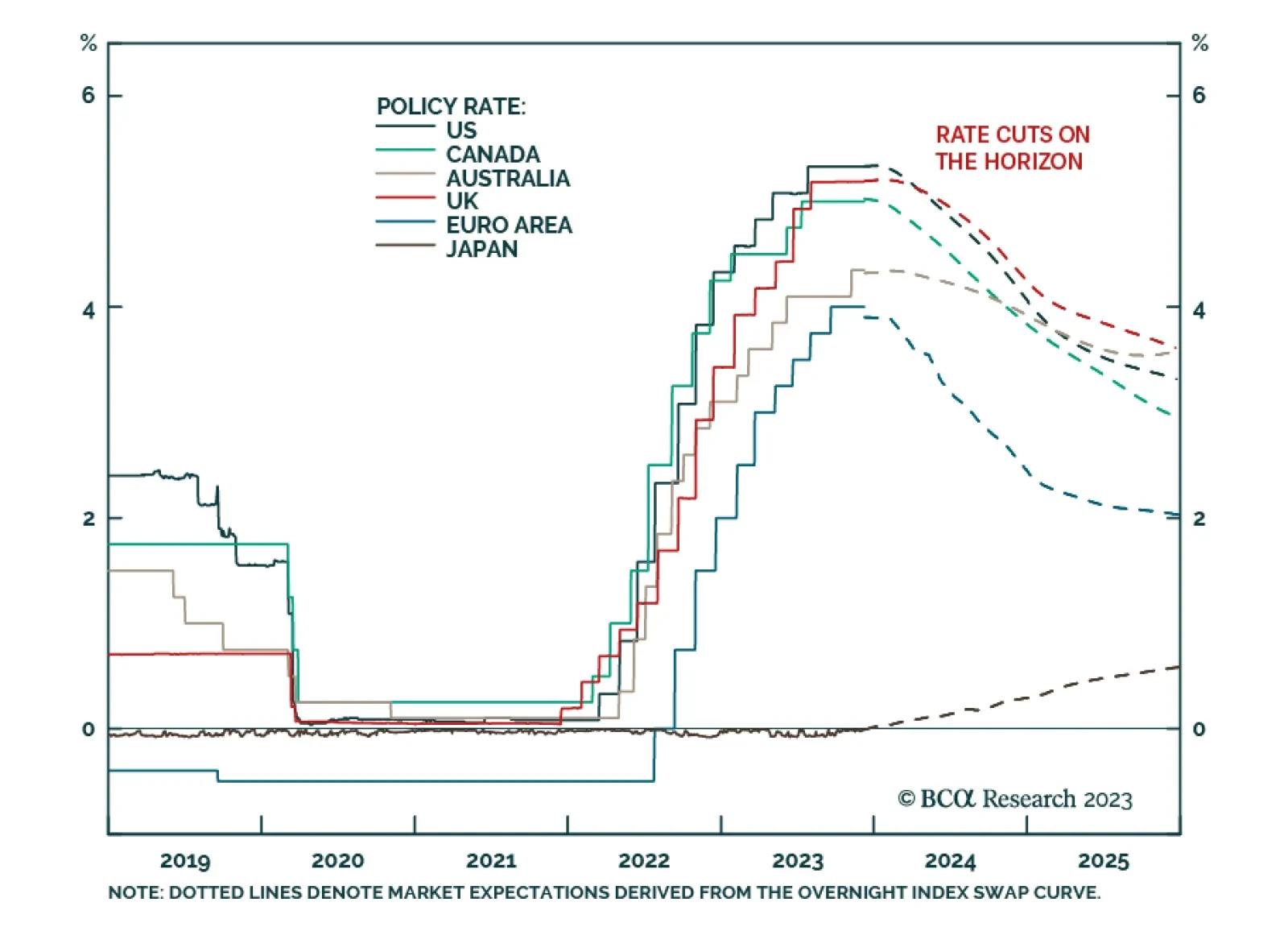

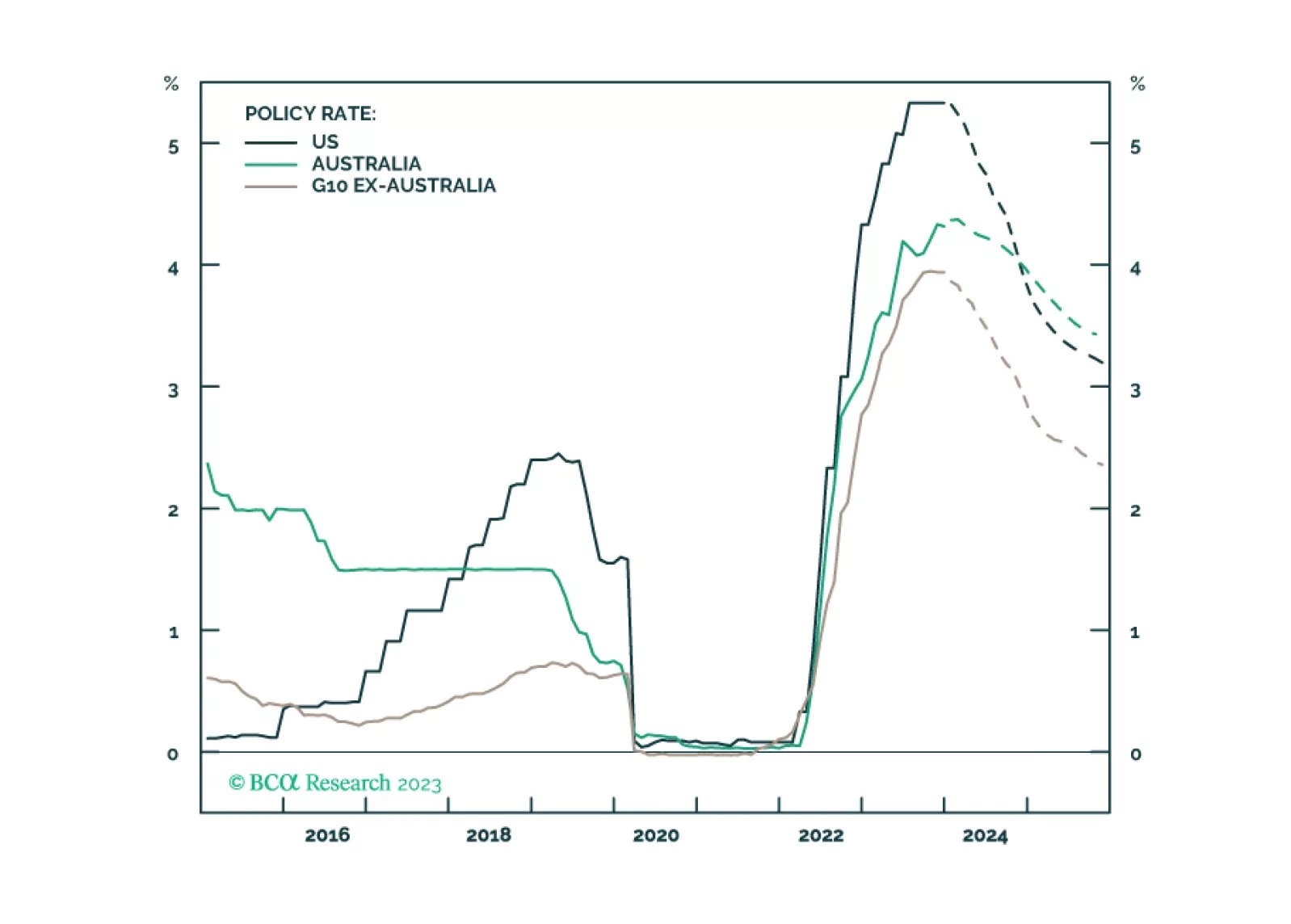

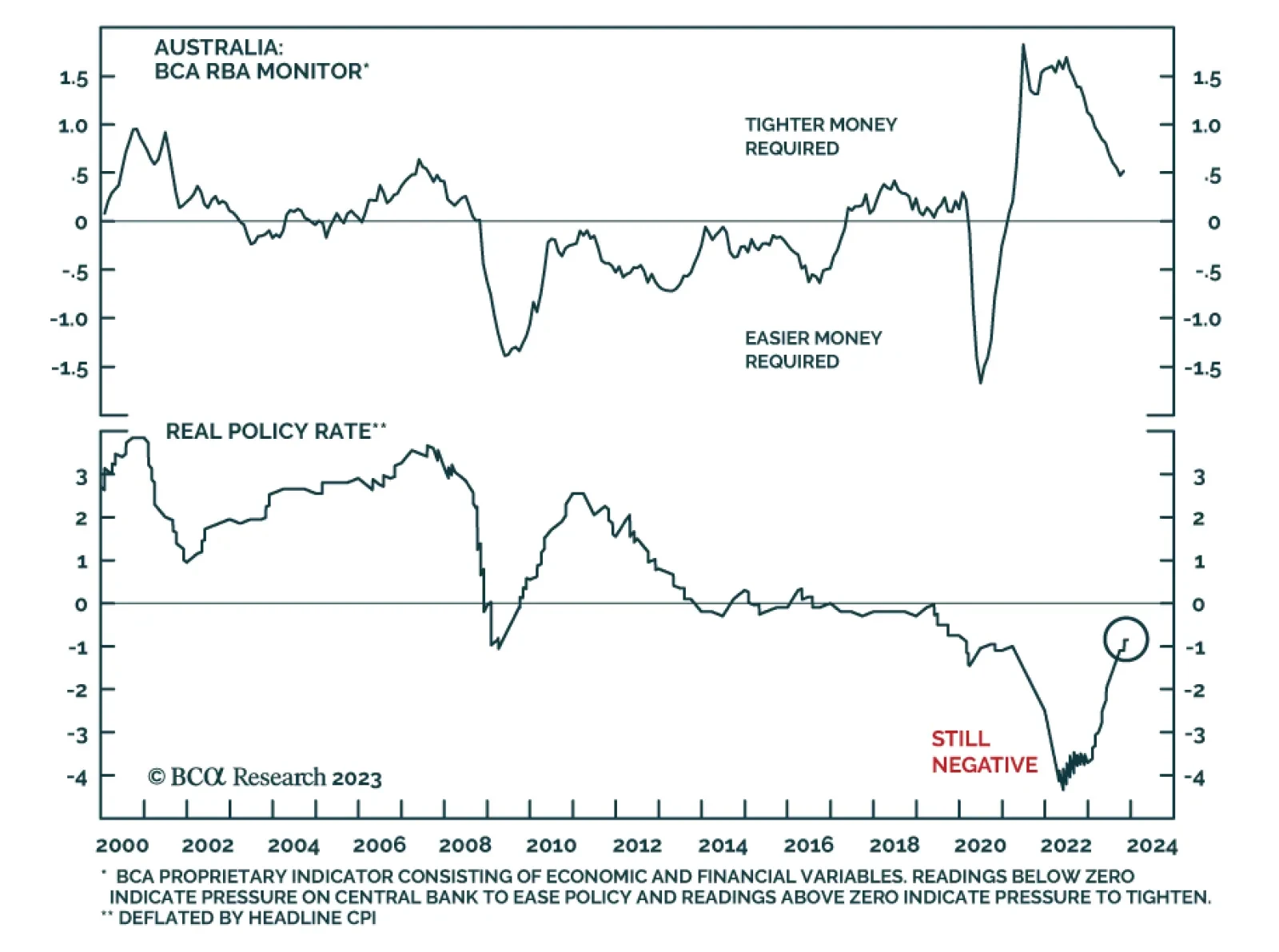

In this Special Report, we take an in-depth look at the outlook for monetary policy in Australia and discuss the impact of an elevated policy rate on the economy. We recommend an underweight country allocation to Australian government bonds and look for opportunities to go long the Australian dollar.

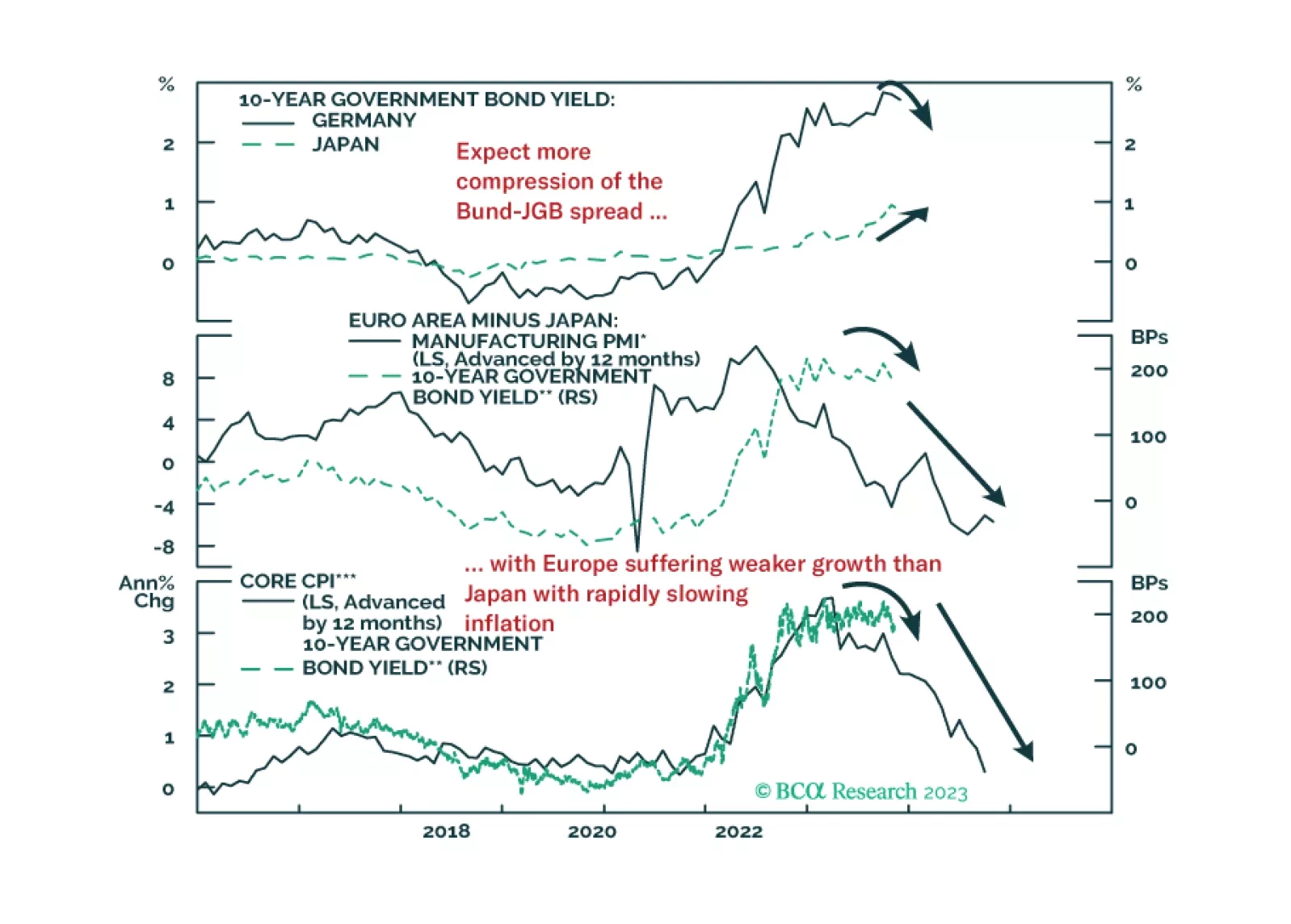

In this Insight, we review the performance and rationale for our current set of tactical fixed income trade recommendations. Our highest conviction positions also happen to be our most successful trades: positioning for a narrowing of the German bund-JGB spread and wider Japanese inflation breakevens.

Labor markets are softening in most developed economies, as is usually the case in the lead-up to recessions. Our base case is that the global recession will begin in the second half of 2024, but we will be monitoring our MacroQuant model on a daily basis for confirmation.