BCA Indicators/Model

In our simulations of fairly deep global recessions averaging -1.5% in 2024 global GDP growth, we expect OPEC 2.0 to reduce output enough to offset lost demand. Even so, we find oil prices drop ~ $22/bbl – from ~ $100/bbl in 1H24 to ~ $78/bbl in 2H24. We remain long the XOP and COMT ETFs to retain oil and commodity exposures.

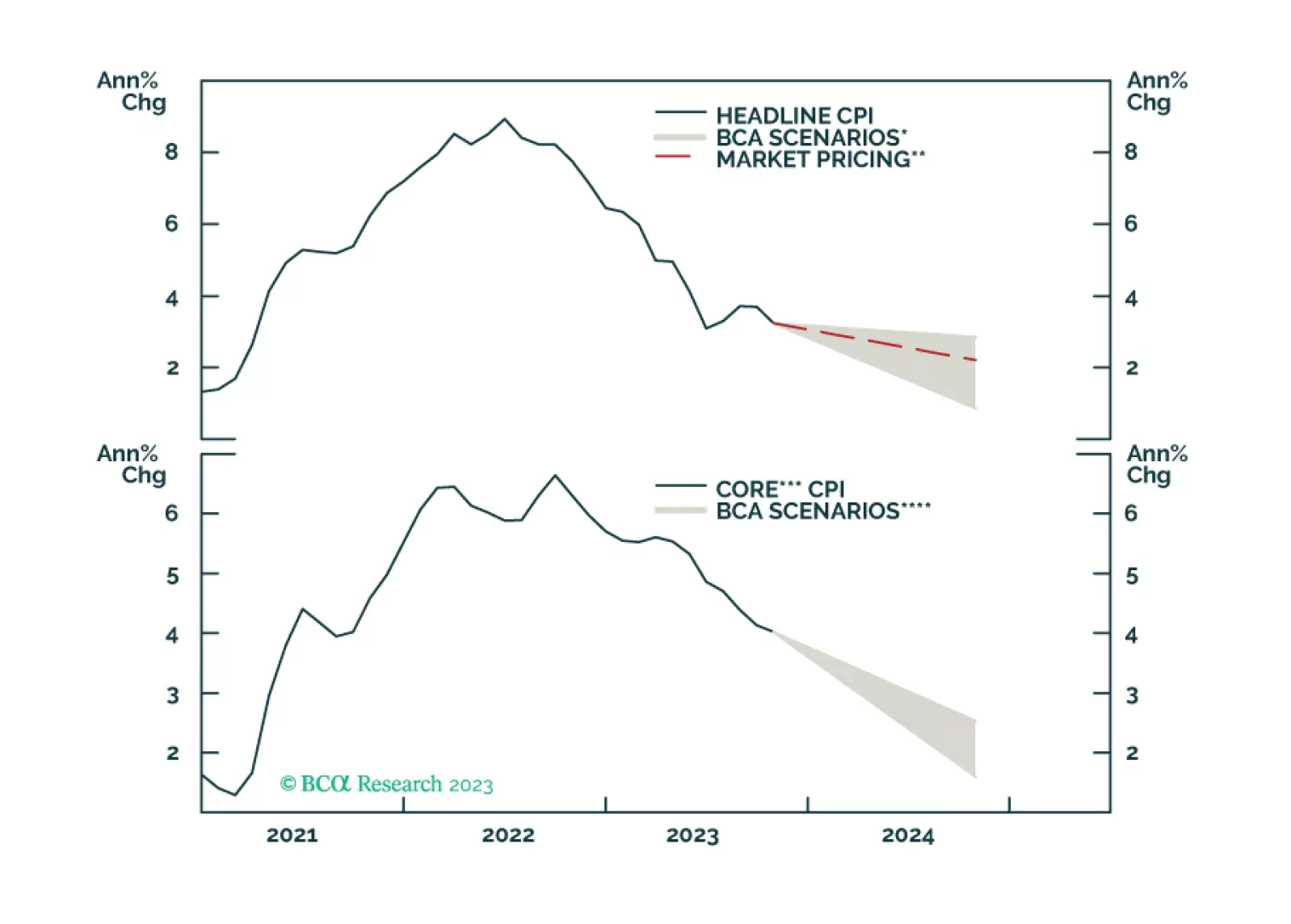

This week’s Special report revisits our TIPS Golden Rule. We provide a 12-month inflation forecast and discuss how it impacts our TIPS view.

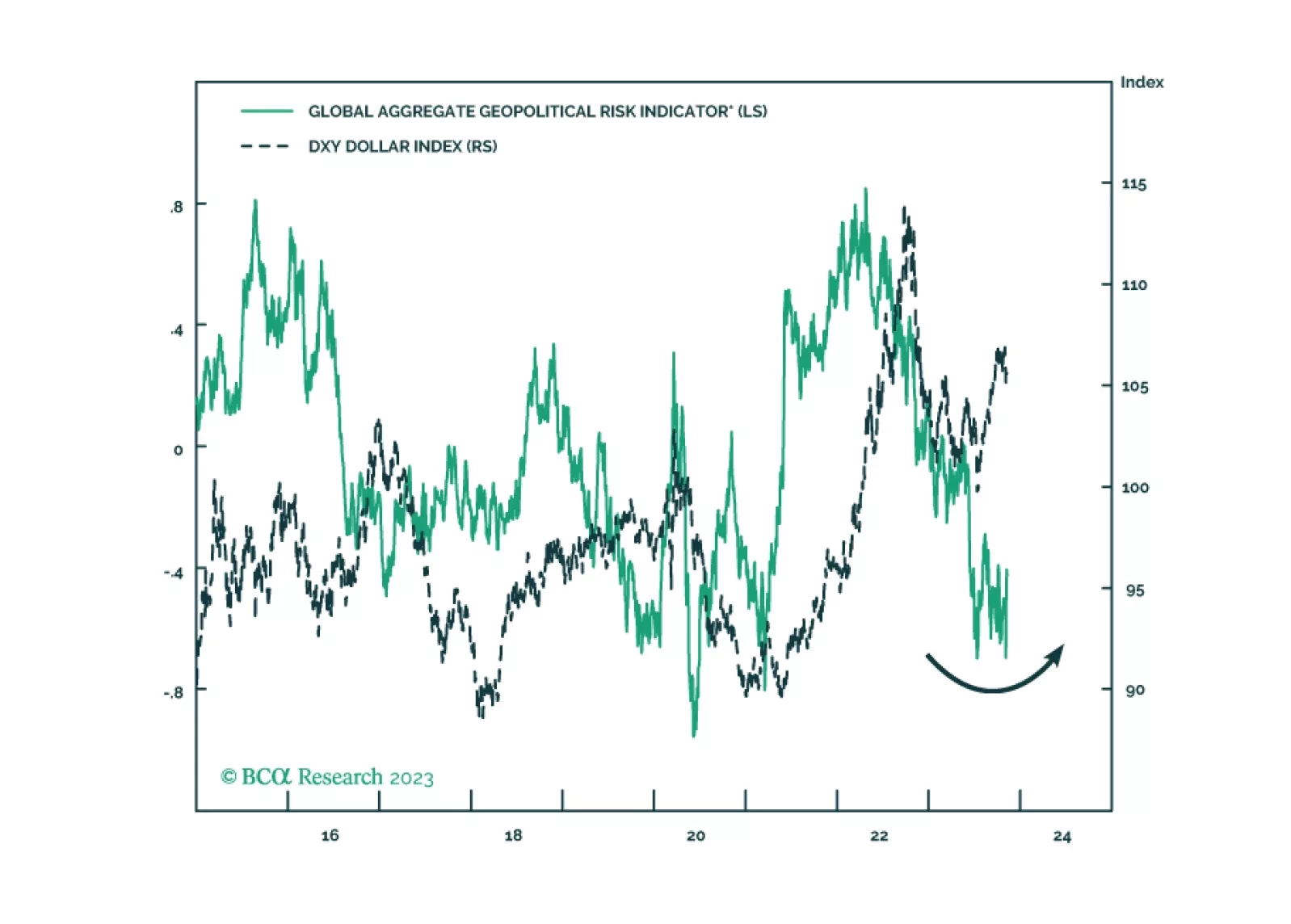

Amid a range of geopolitical narratives, what matters is that the US strategy of economic engagement with its rivals is failing, giving rise to a new strategy of containment that will reinforce the secular rise in geopolitical risk. Our market-based quantitative indicators of geopolitical risk are set to rise in the coming year.

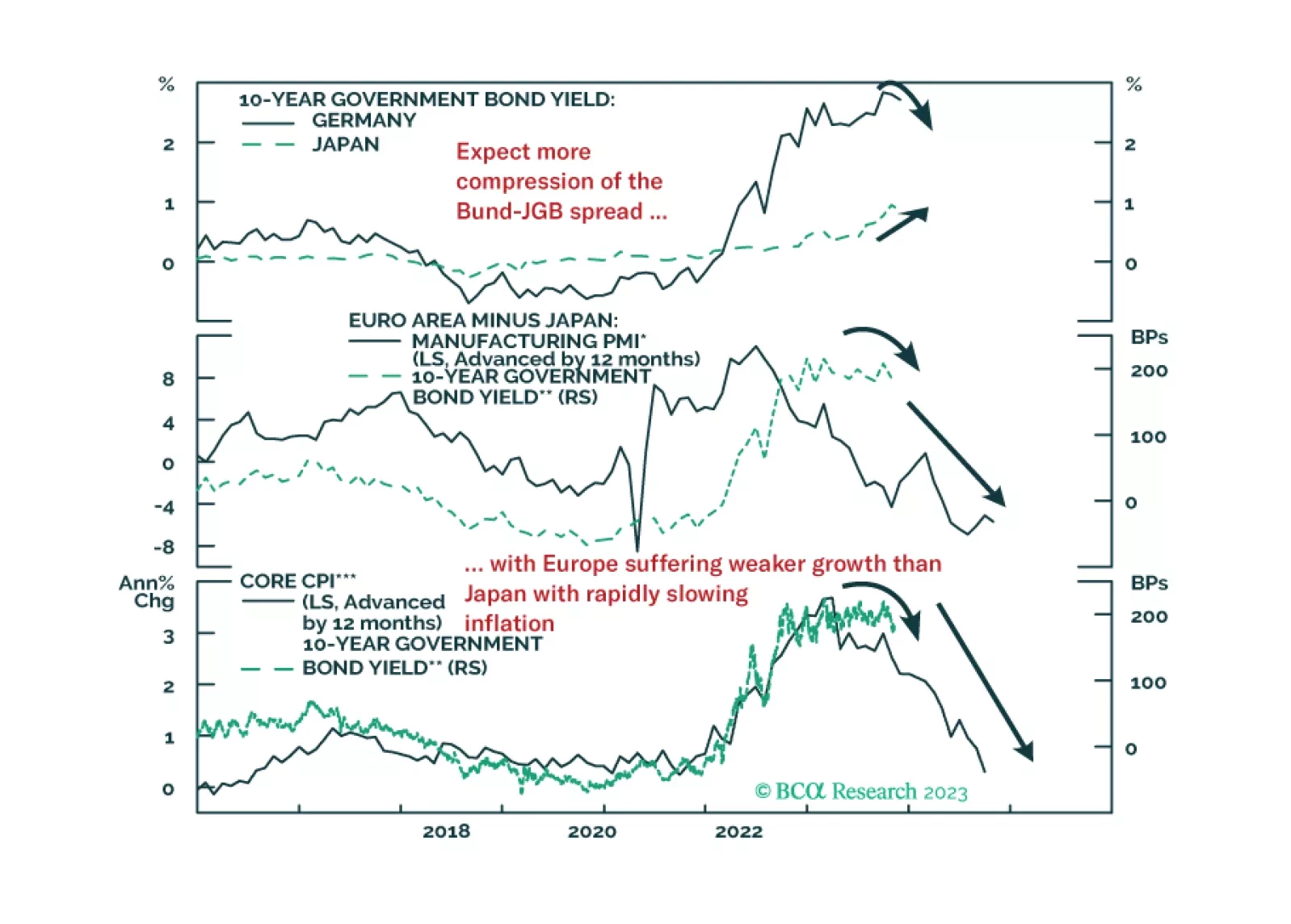

In this Insight, we review the performance and rationale for our current set of tactical fixed income trade recommendations. Our highest conviction positions also happen to be our most successful trades: positioning for a narrowing of the German bund-JGB spread and wider Japanese inflation breakevens.