BCA Indicators/Model

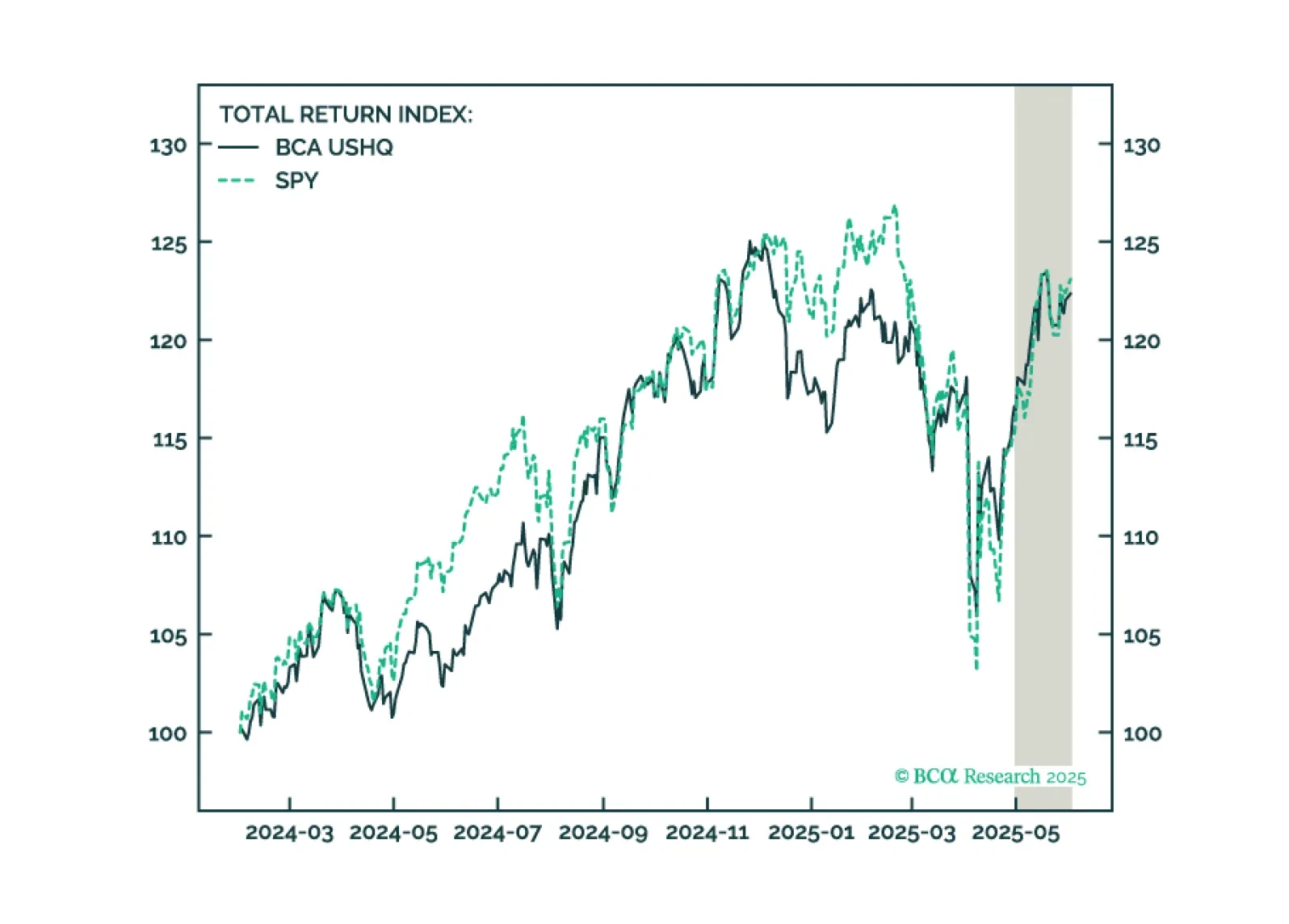

The US High Quality (USHQ) portfolio underperformed its benchmark through May, returning 5.1%, whilst its SPY benchmark returned 6.1%. On a trailing three-month basis, performance is also slightly weaker vs. benchmark, with USHQ underperforming by approx. 130bps. Notably, volatility and drawdown remain lower than the SPY, aiding risk-adjusted performance.

Our Portfolio Allocation Summary for June 2025.

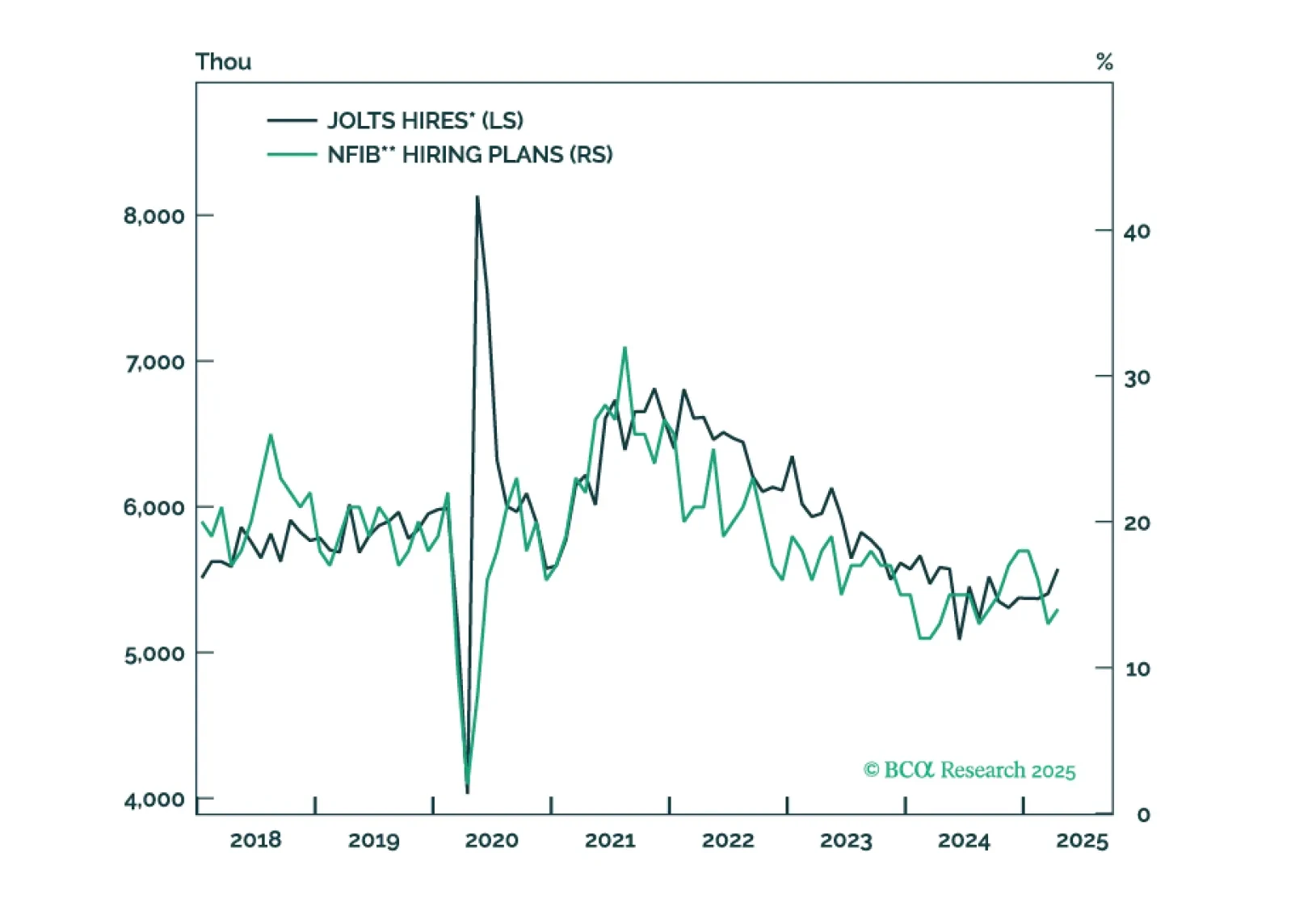

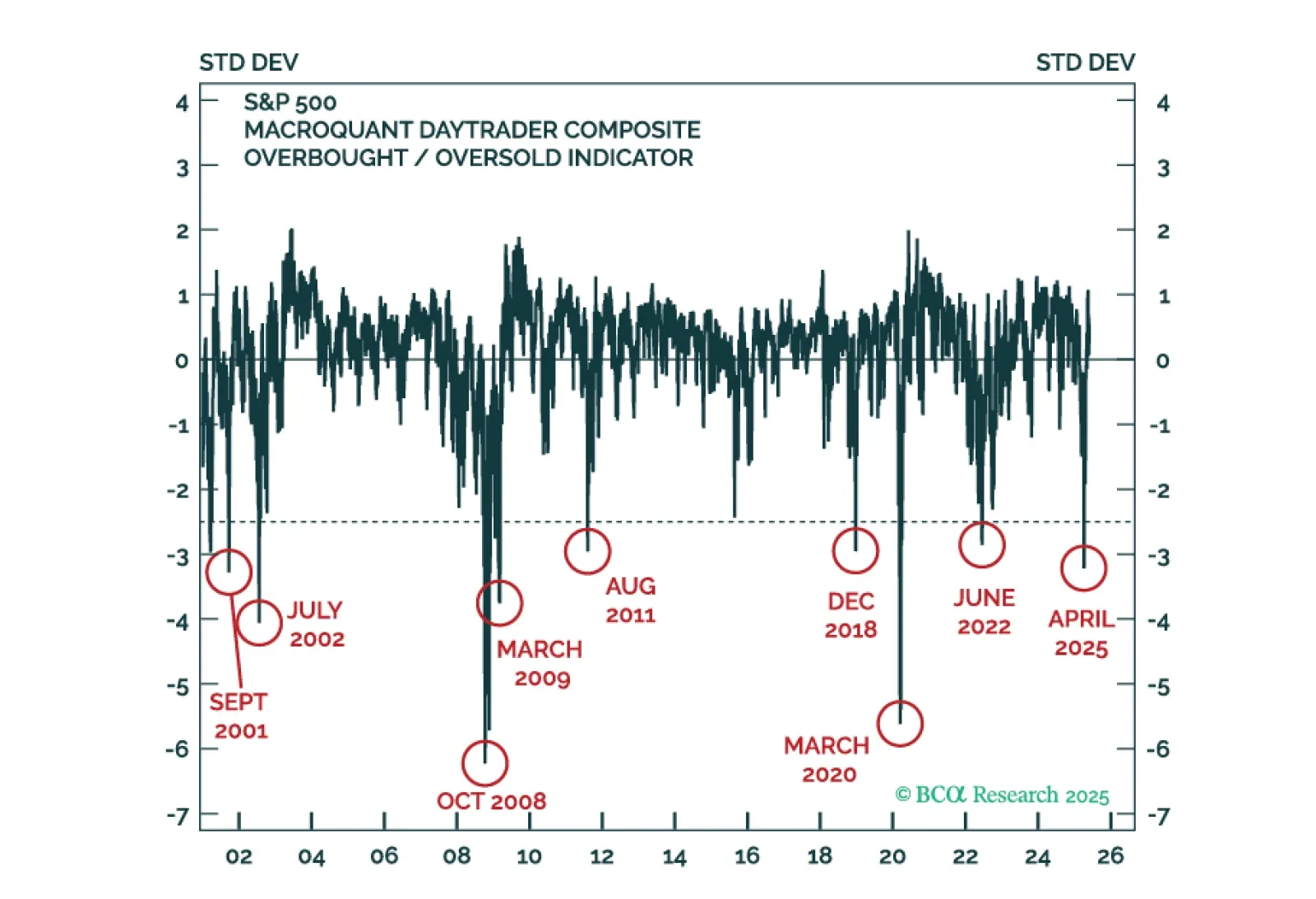

MacroQuant warns that US equities are pricing in very little economic risk. The model is shunning equities and recommends a large overweight to cash.

MacroQuant warns that US equities are pricing in very little economic risk. The model is shunning equities and recommends a large overweight to cash.

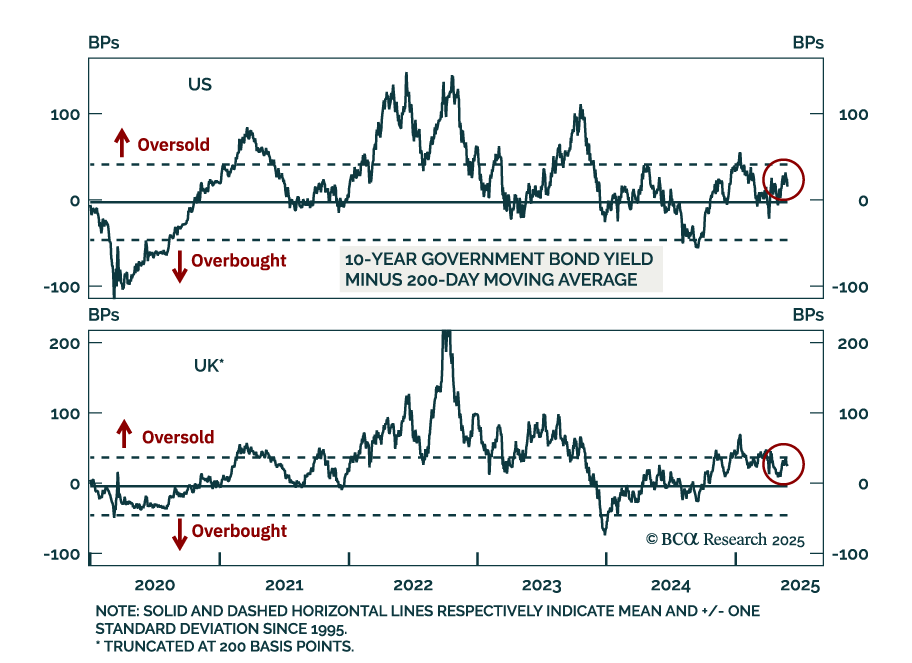

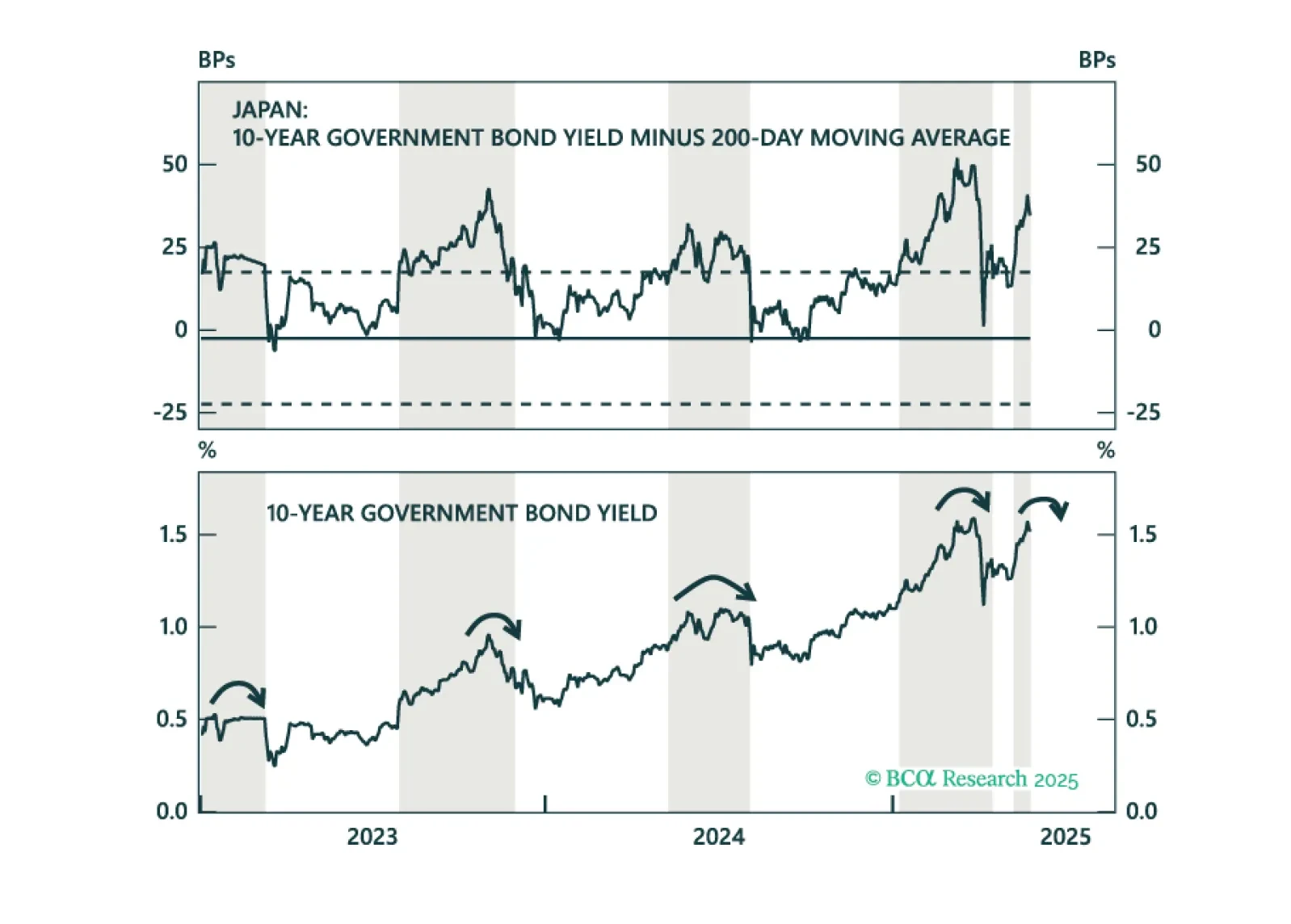

Are bond yields overextended? We introduce a new global technical indicator that helps spot mean-reversion opportunities and shows which markets are nearing exhaustion.

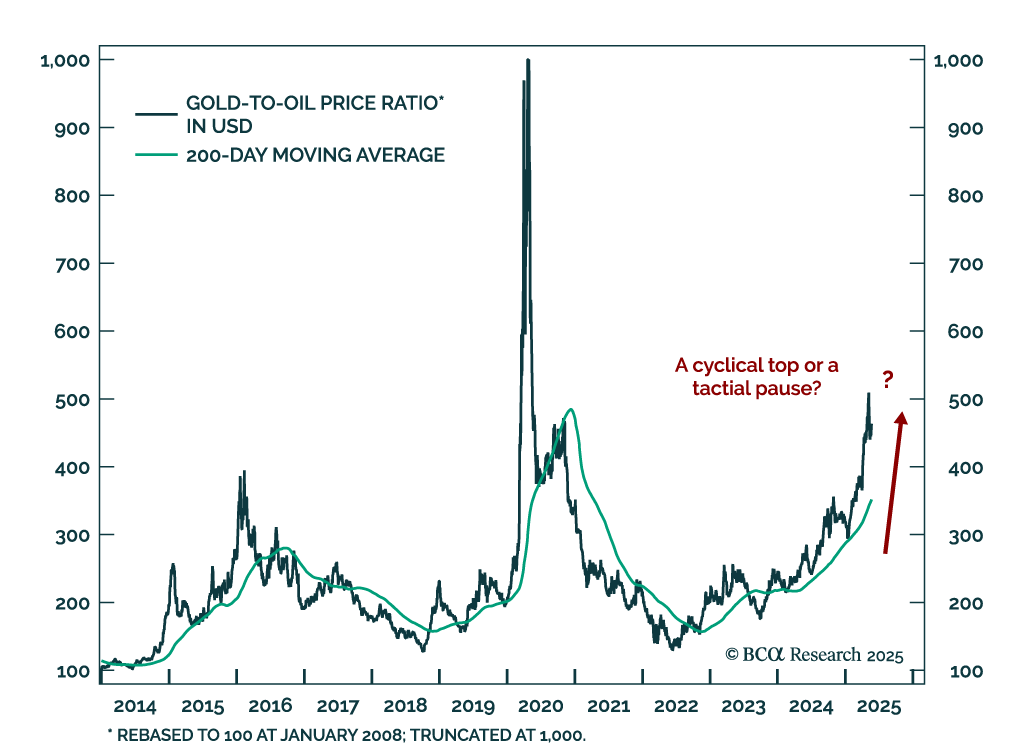

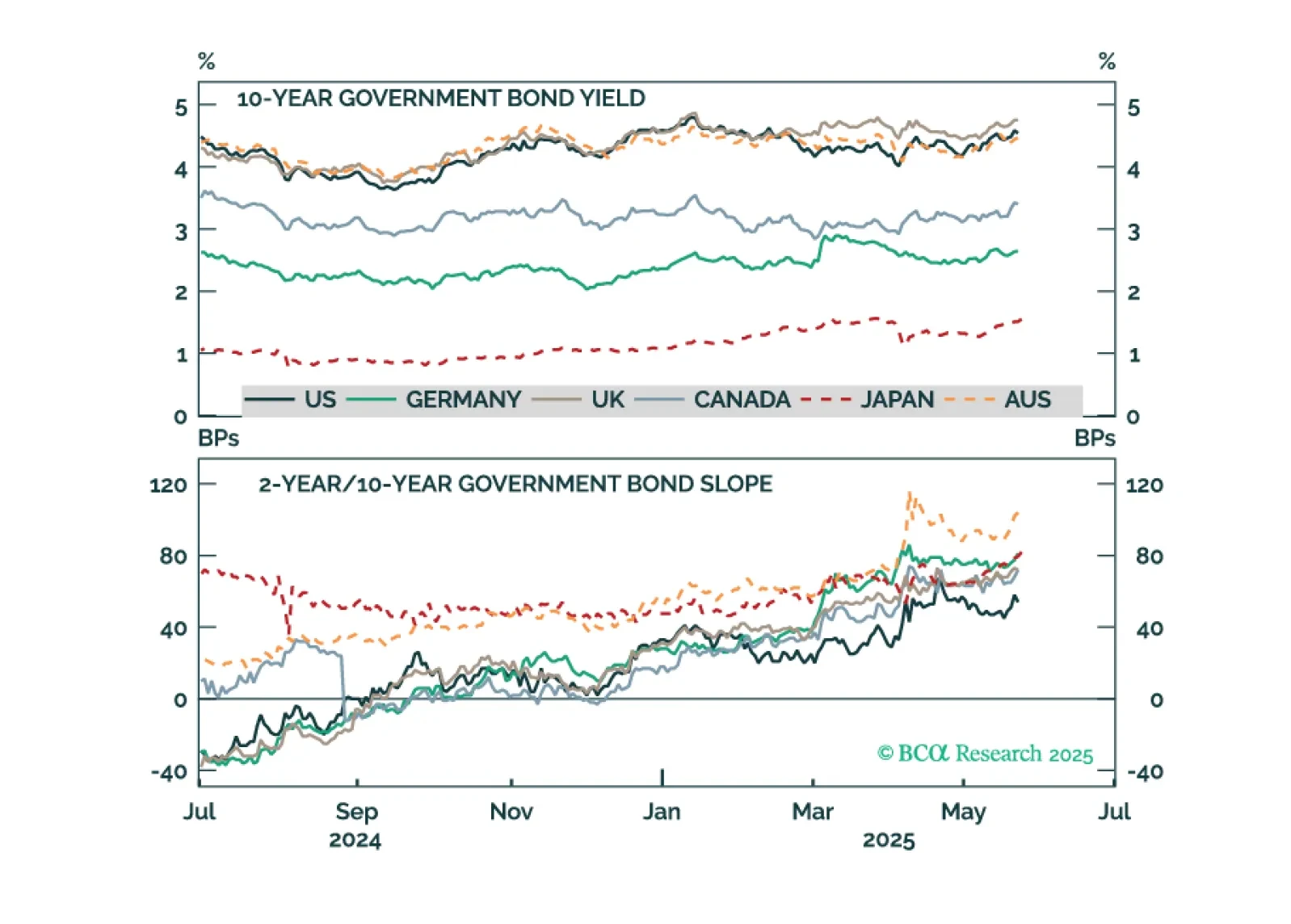

We perform a decomposition of yields moves across six major developed government bond markets to get to the bottom of what’s been driving the global bond selloff of the past eight months.

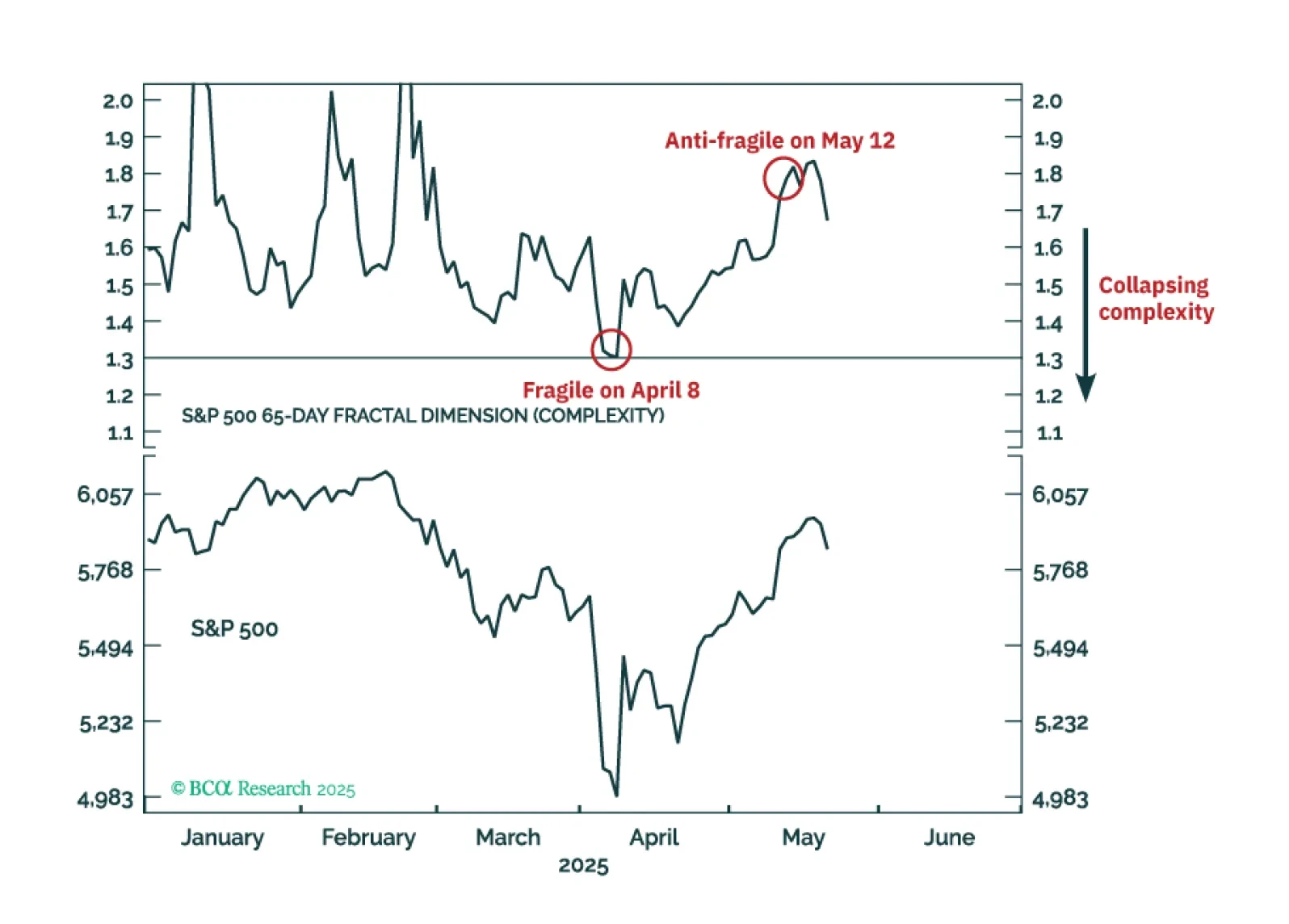

Right now, the major stock and bond markets are more ‘anti-fragile’ than fragile, and the Joshi rule recession indicators signal that a US recession is not imminent. This justifies a neutral, or default, tactical weighting to both stocks and bonds until a major market does become fragile, or until recession risk elevates. The one major price trend that is fragile is the 65-day selloff in the US dollar, which justifies a tactical overweighting to the dollar.

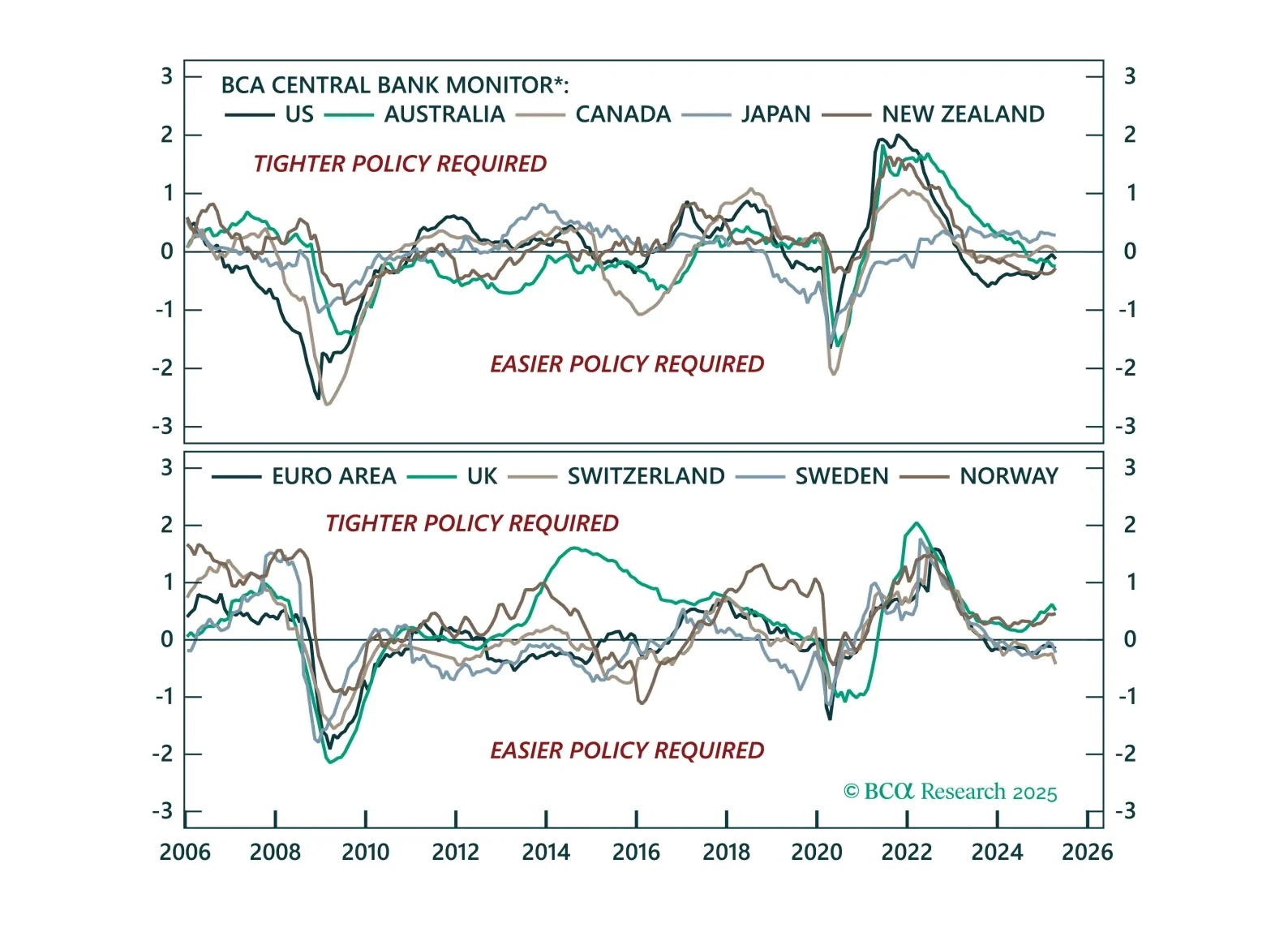

The easing bias remains, but not all central banks are equal. This Central Bank Monitor update reveals who is ready to cut more and who is still pretending not to.