Business Cycles

Our US Investment Strategy service examines the state of consumer finances in the context of their view that a recession will materialize this year with a double-digit peak-to-trough decline in S&P 500 earnings expectations. They expect the…

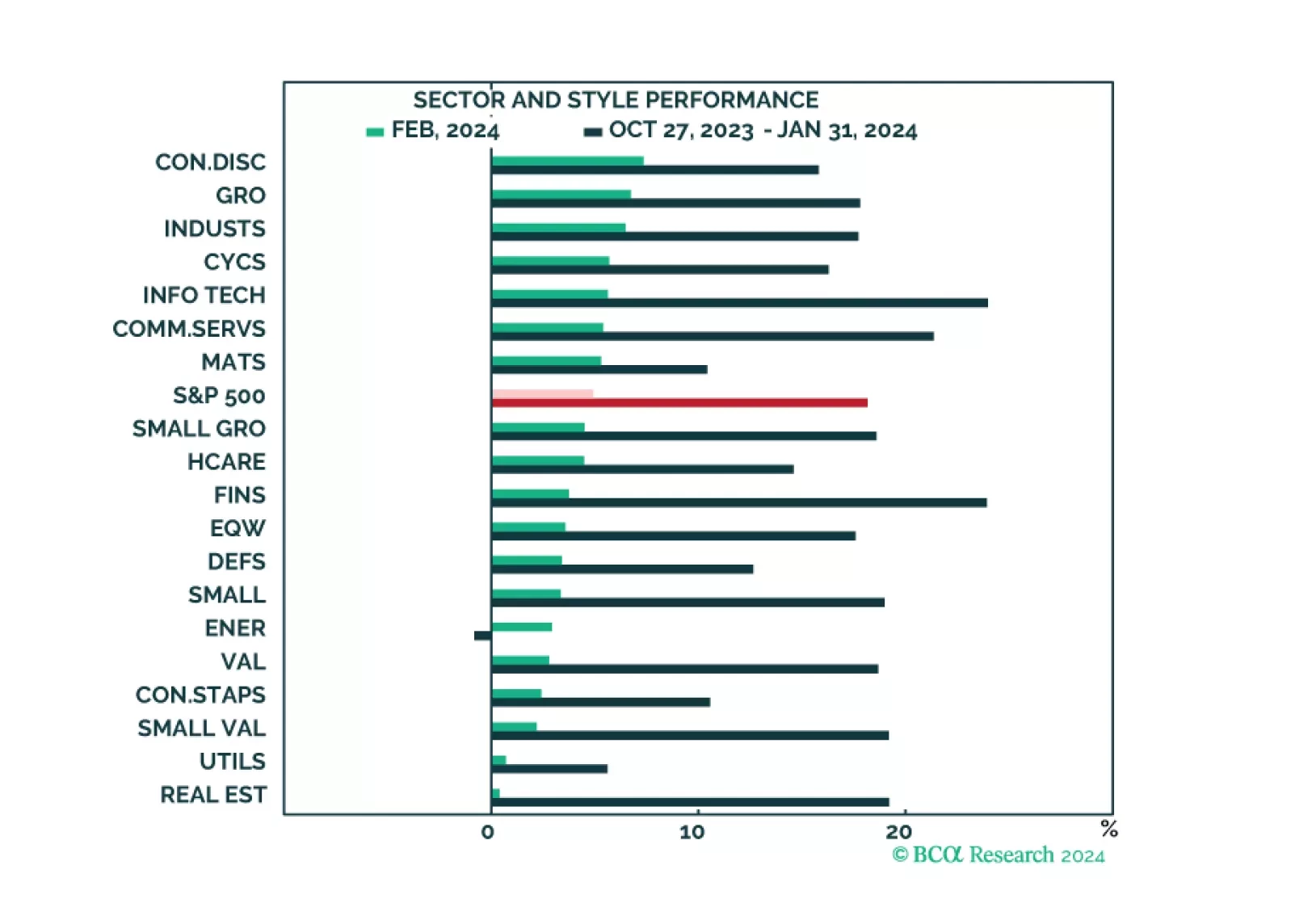

The market narrative continues to be dominated by the Magnificent Six, which drove both market performance and strong Q4 earnings results. While all sectors and styles have recently turned green, the rally is still mostly narrow. Earnings growth appears to be strong, but outside of the Magnificent Six, many companies are struggling. The market appears expensive and overbought, but that is mostly down to the high valuations and the popularity of the Magnificent Six.

China’s NBS PMI release indicates that the Chinese growth is stabilizing at a low level. The composite PMI came in at 50.9 – unchanged from January. The stabilization was led by the non-manufacturing sector though both the manufacturing and non-manufacturing…

Swiss annual inflation continued to decelerate in February, with headline CPI now at 1.2% and core at 1.1%. This is remarkable since inflation continues to track well below the 1.8% forecast by the Swiss National Bank (SNB) for the first quarter. Import and…

Economic sentiment has improved since the December FOMC meeting, with positive momentum extending into February. The chart above neatly summarizes the impact that the Fed’s projected easing has had on sentiment, both on “Wall Street” and “Main Street”. The…

The JPM Global Manufacturing PMI improved from 50.0 to 50.3 in February, indicating that global manufacturing activity is growing again after having contracted for 18 months. Notably, new orders expanded from previously contracting levels (from 49.8 to…

The preliminary Eurozone inflation release suggests that price pressures eased by less than anticipated in February. Headline CPI inflation slowed from 2.8% y/y to 2.6% y/y (slightly above expectations of 2.5% y/y. Similarly, although the core inflation gauge…

As we highlighted in a previous Insight, the breadth of the US equity rally has been relatively narrow, led by extremely strong gains among Big Tech stocks. Tech is still the best performing sector, with the S&P IT price index up 12% year-to-date on top…

The global equity rally – which fizzled at the start of the year – picked up steam again in February with nearly all major regions posting above average returns. After having underperformed last year, Chinese stocks led their global counterparts in terms of…

According to BCA Research’s Geopolitical Strategy and The Bank Credit Analyst services, trade policy under a second Trump presidency represents the greatest cyclical risk to investors. In 2018, the Trump administration’s trade war with China and several…