Canada

The January Canadian labor report missed estimates. The January LFS showed headline job losses of 24.8k, compared with a 10.1k gain in December. Unemployment fell to 6.5% from 6.8%, driven by lower labor force participation rather than stronger employment.…

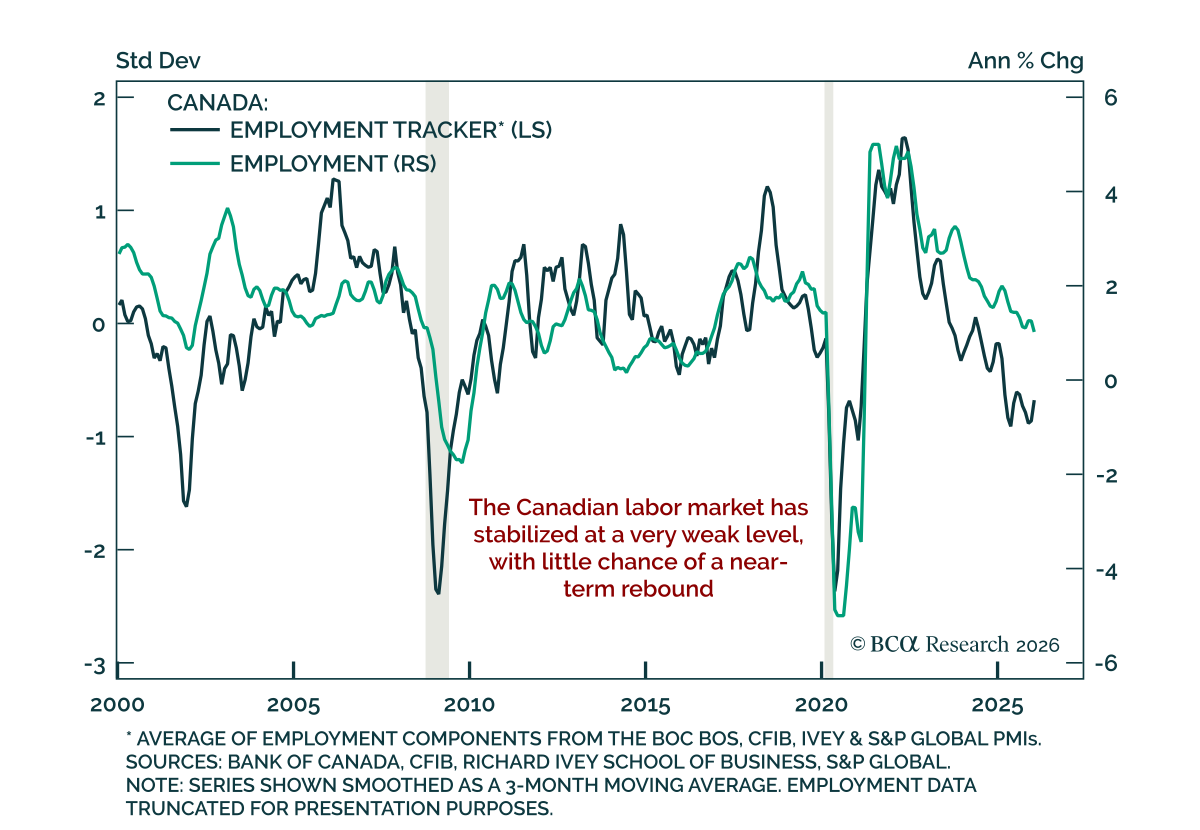

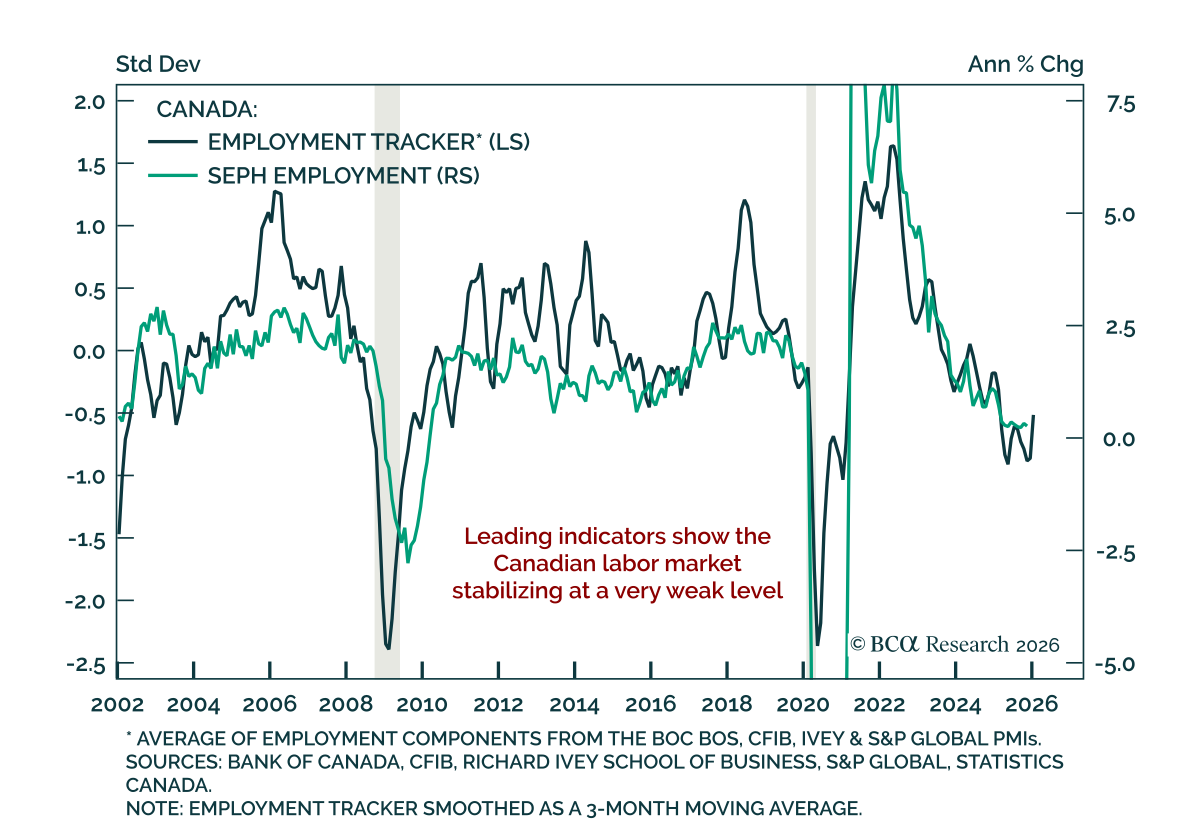

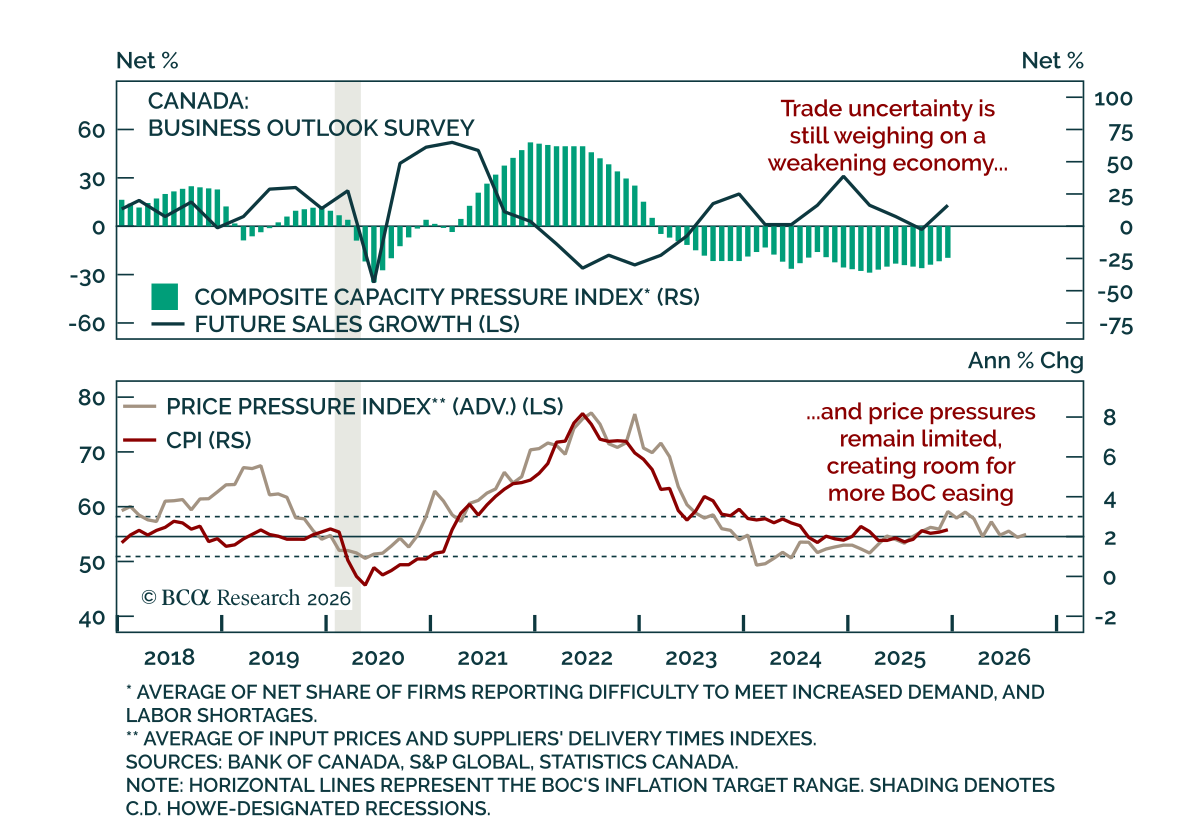

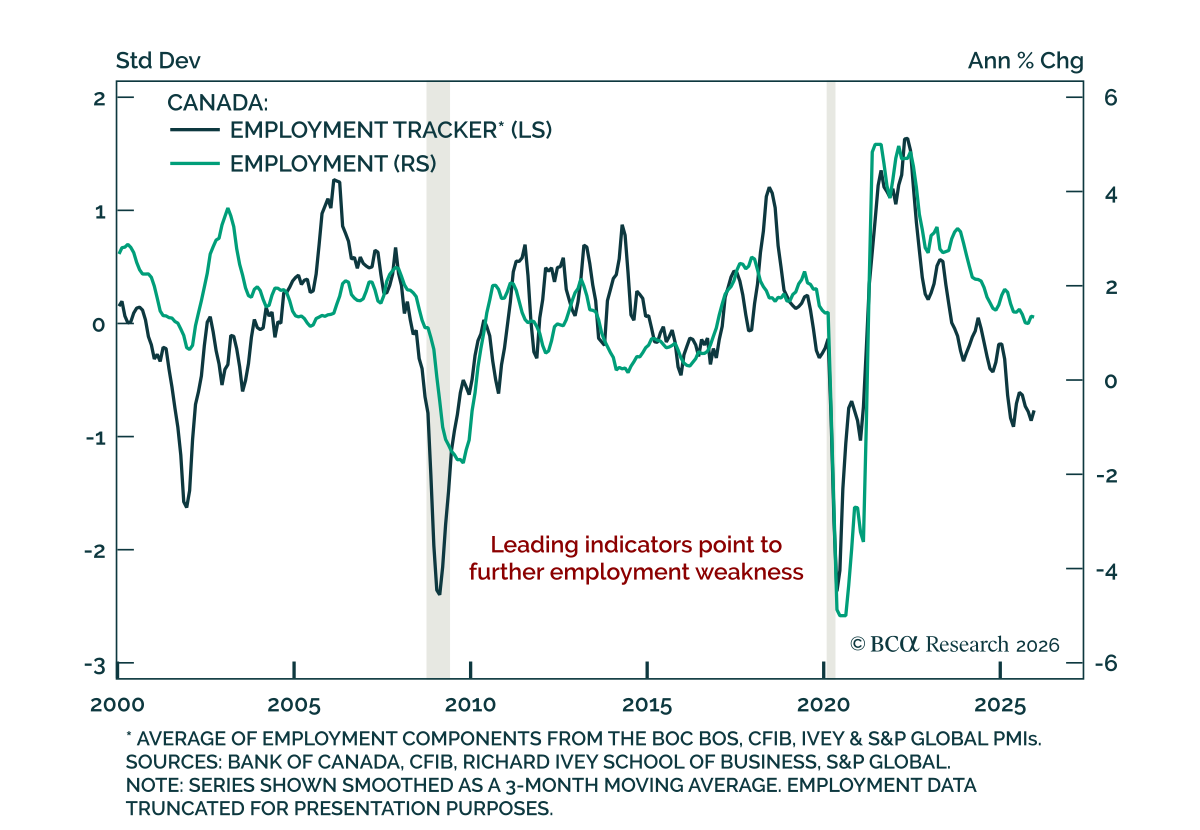

Downside risks dominate Canada’s outlook, supporting further BoC easing and CAD steepeners. Canada’s employment data show an intriguing divergence. The widely followed Labour Force Survey (LFS) has stabilized, but its volatility and frequent revisions make it…

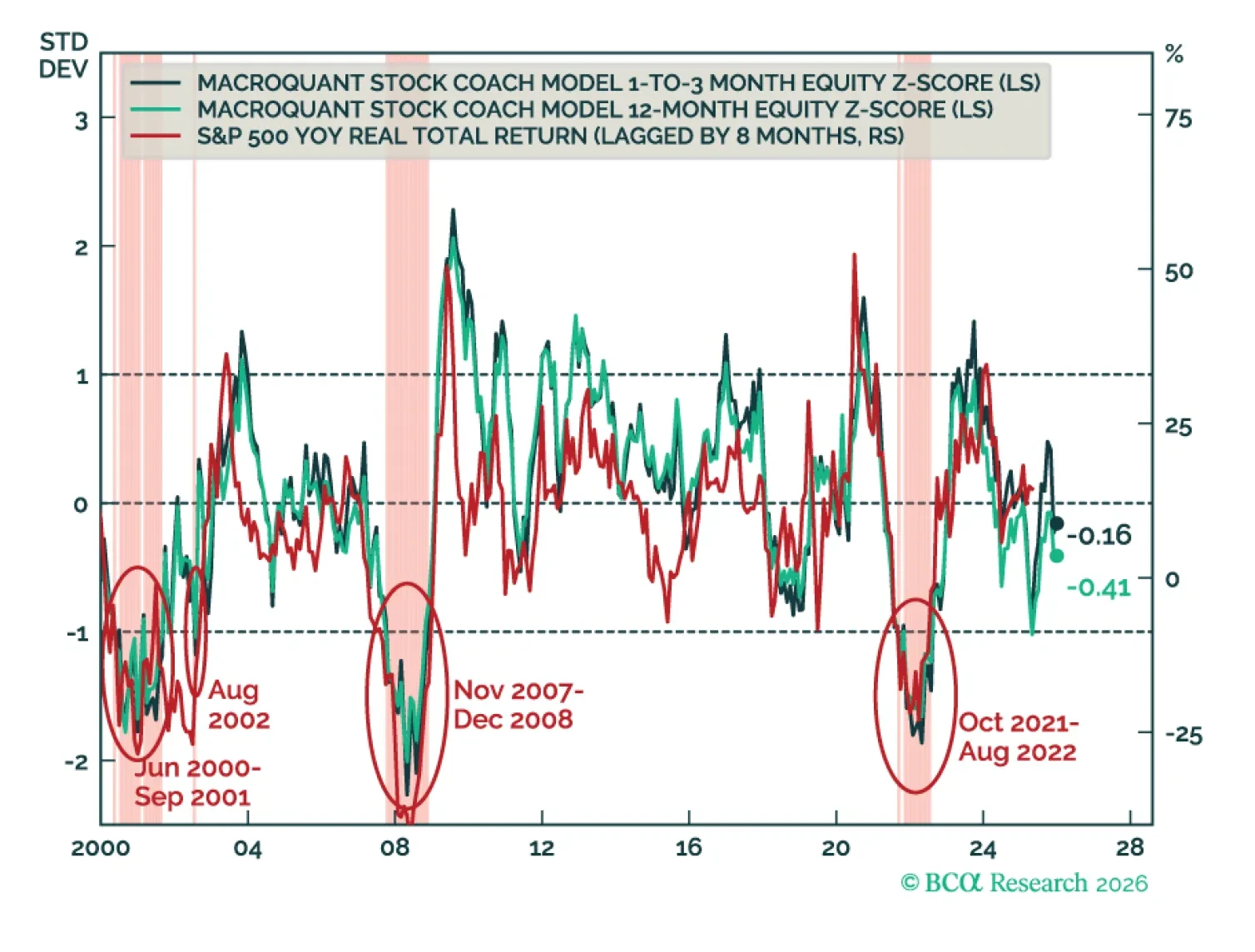

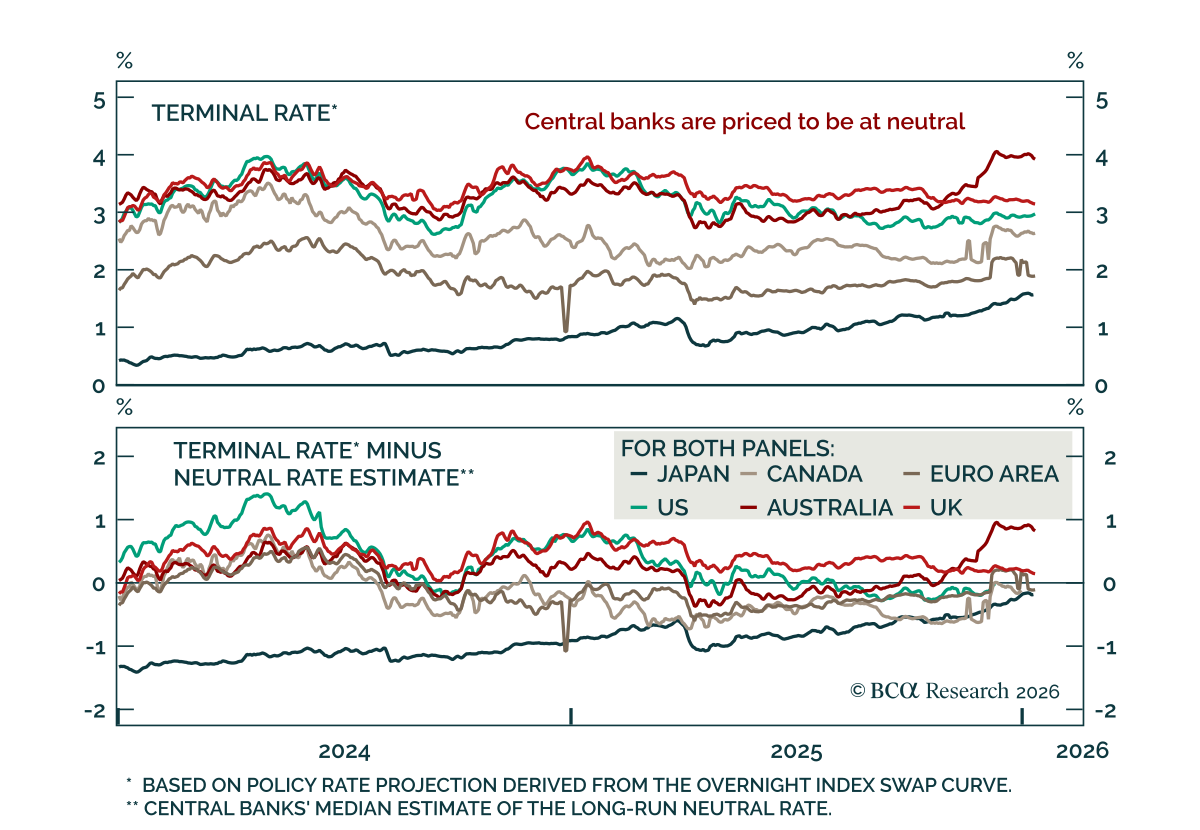

MacroQuant recommends a slight underweight in equities, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has upgraded oil and copper to overweight, and is bullish on gold.

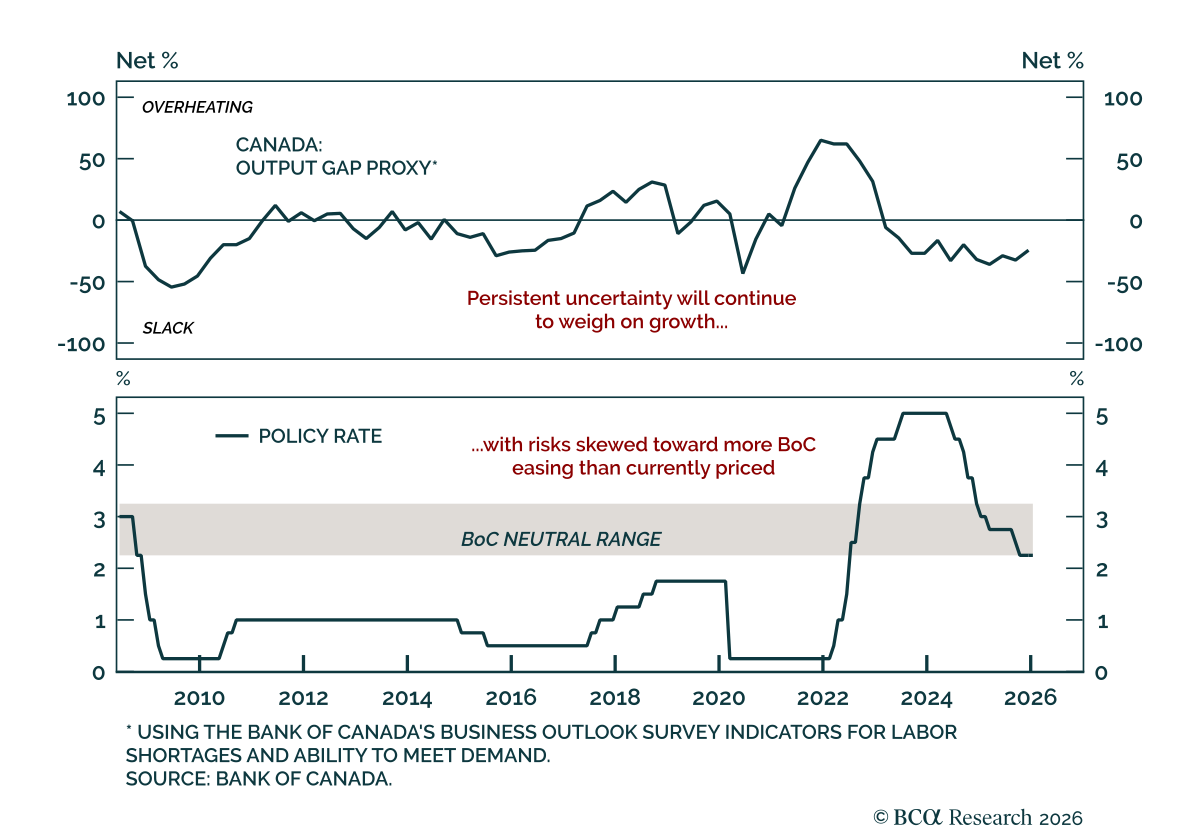

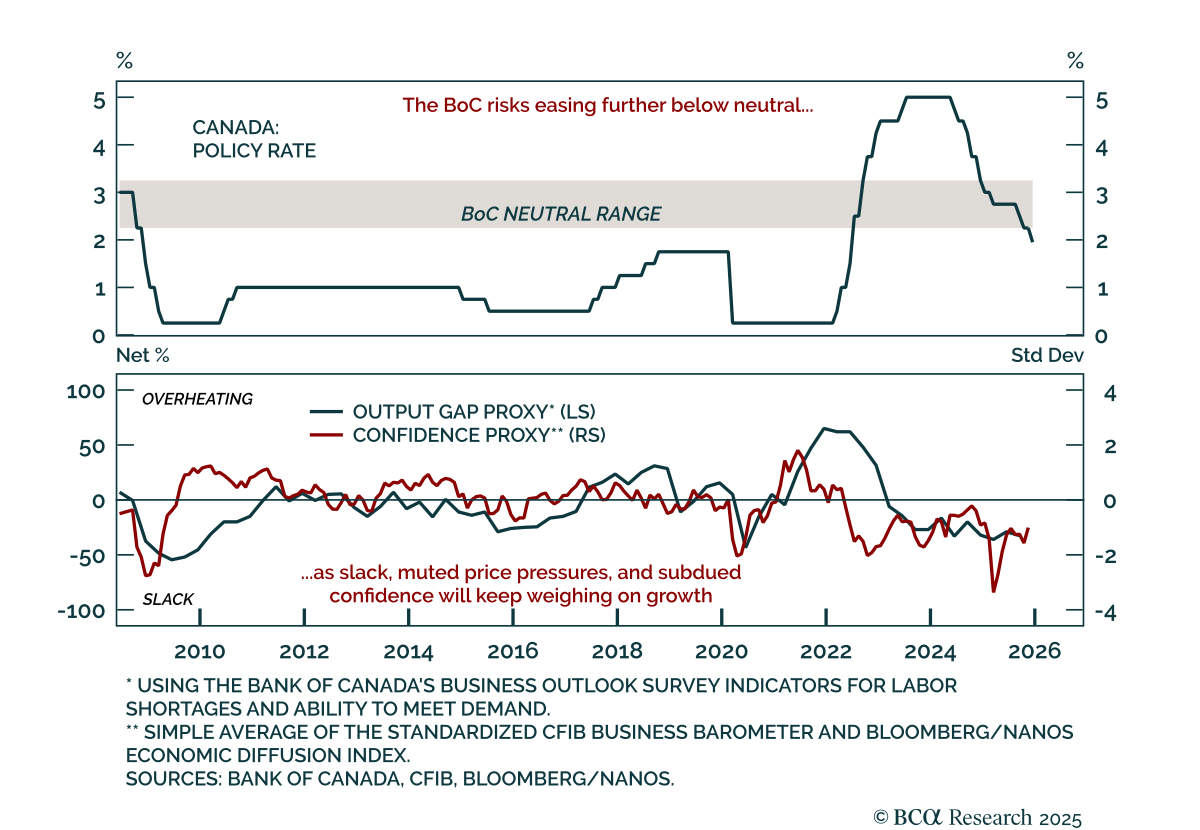

Downside risks dominate the Canadian outlook despite stabilization and a BoC pause. The Bank of Canada held the overnight rate at 2.25% for a second consecutive meeting, as expected. After cutting from 3.5% in early 2025, the BoC signaled at its October…

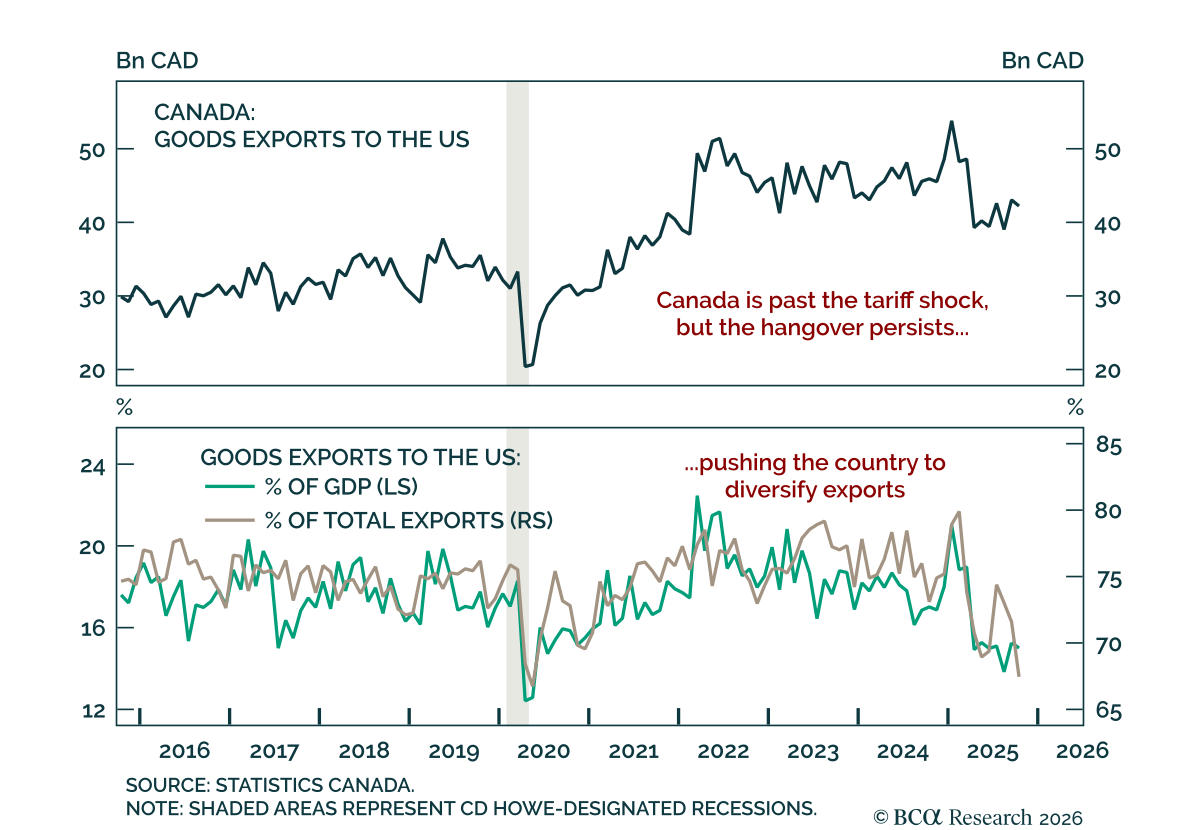

Fade US-Canada tariff threats. President Trump said over the weekend that he would impose 100% tariffs on Canada should it conclude a trade deal with China, a reversal from comments only days earlier encouraging such a deal. We view this as posturing ahead of…

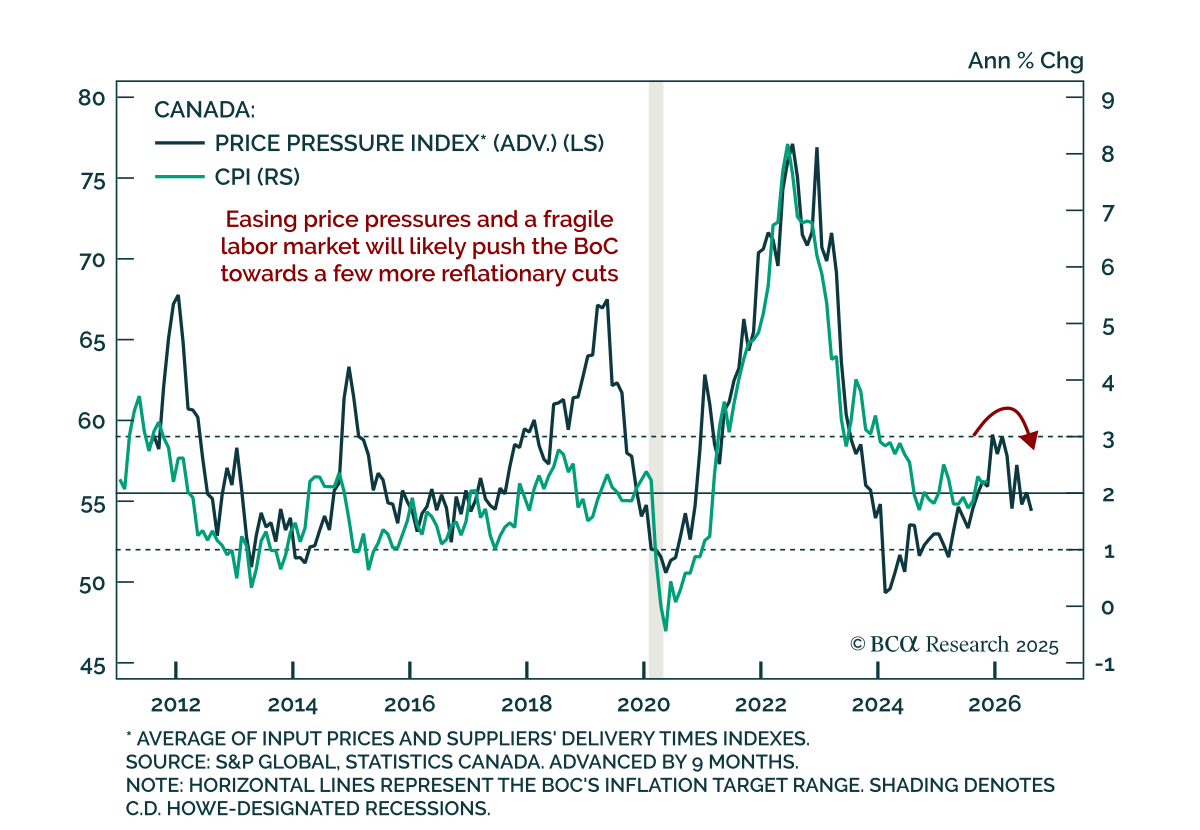

Expect 1-2 additional BoC cuts in 2026 as core inflation eases and the economy stabilizes at a weak level. Canadian December CPI came in slightly above expectations, with headline inflation rising to 2.4% y/y from 2.2%, but the upside surprise reflects…

Our Global Fixed Income strategists maintain an above-benchmark duration stance as labor market risks continue to support downside yield potential, even as the global easing cycle winds down. With policy normalization largely complete, monetary policy is…

Expect additional BoC cuts in 2026 as mixed job gains and persistent uncertainty weigh on growth. Canada’s December jobs report sent mixed signals. Employment increased by 8.2k, above expectations but down from 53.6k in November. Job gains were driven by…

Fade 2026 hike pricing through CAD steepeners as cooling CPI and softening labor conditions keep downside risks for rates and GoC yields. Canadian November CPI came in cooler than expected: Headline held at 2.2% y/y while core measures eased to 2.8% from…

Fade 2026 BoC hike pricing through CAD steepeners as muted inflation and labor softness keep downside risks for rates and GoC yields. The Bank of Canada left the overnight rate unchanged at 2.25% after signaling at its October meeting that it was ready to…