China

We believe the PBoC’s recent policy stimulus might bolster investor confidence, potentially stabilize onshore Chinese equity prices, and provide modest support to offshore stocks. However, they are unlikely to significantly boost economic growth in the mainland.

Export dynamics from small open economies are a good bellwether for global growth conditions. Taiwan export orders accelerated from 4.8% y/y to a faster-than-anticipated 9.1% in August. The faster pace of growth was also broad-based among the country’s…

The PBoC announced further measures to stimulate the economy on Tuesday. It lowered the reserve requirement ratio from 10% to 9.5%, cut the 7-day reverse repo rate by 20 bps (following Monday’s 10 bps cut to the 14-day reverse repo rate), lowered borrowing…

The PBoC lowered the 14-day reverse repo rate by 10 bps on Monday, a move that follows a string of easing measures in late July when the central bank lowered the 7-day reverse repo rate, several maturities of the loan prime rate and the 1-year medium-term…

Singapore is a small open economy sensitive to global trade dynamics. Its non-oil exports (NODX) are thus a good bellwether for global growth conditions. Overall exports, which are highly volatile on a month-on-month basis, decelerated at a…

Industrial metals returned a whopping 6% over the past week. Bullish investor sentiment is likely driving these gains. The soft-landing narrative has been gaining traction in recent days with markets pricing in increased odds of an outsized 50-bps Fed rate…

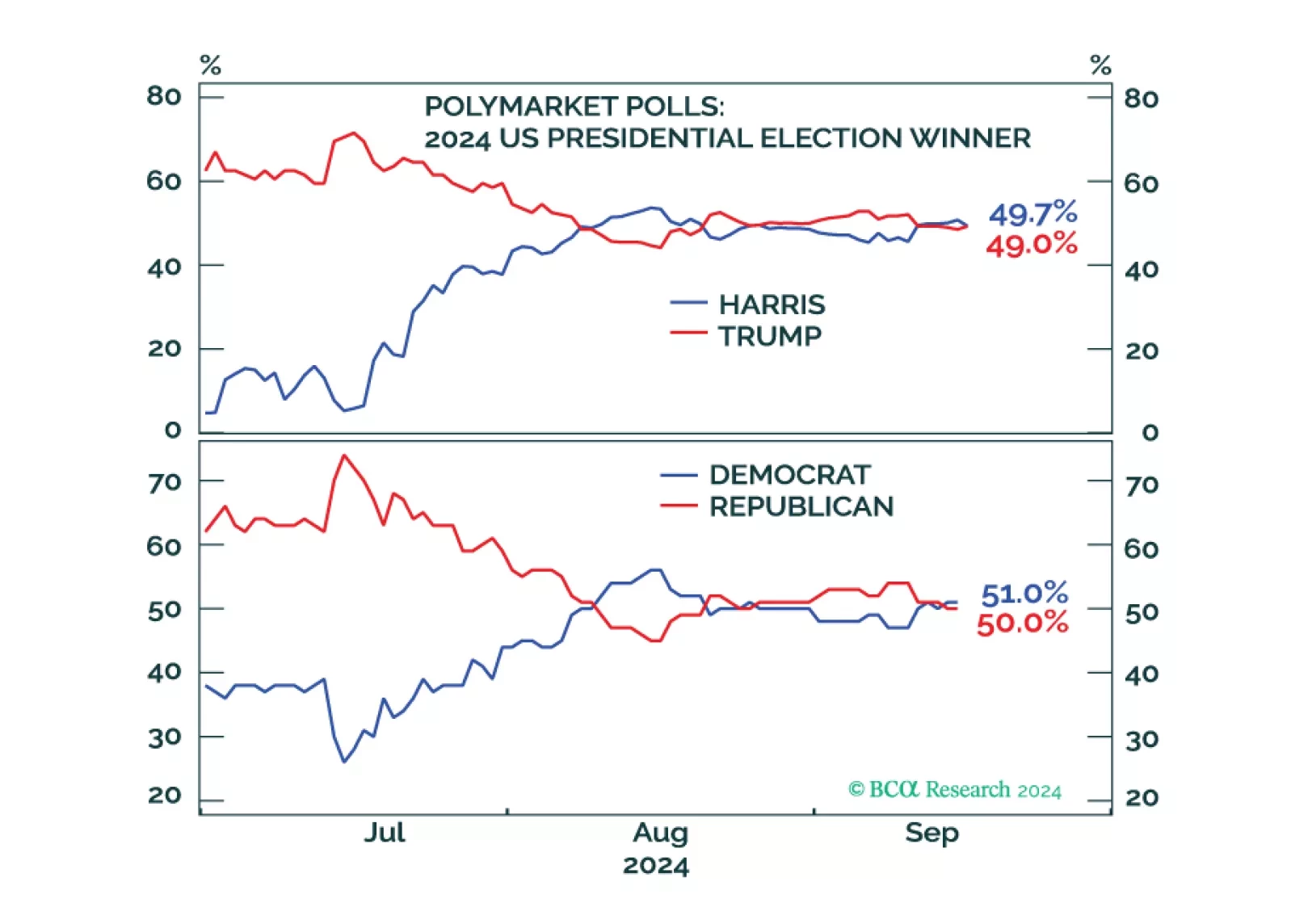

Investors should de-risk tactically in expectation of shocks and surprises ahead of the US election and an uncertain aftermath. Democratic victory with a gridlocked Congress is our base case but would bring minor tax hikes and nuclear brinksmanship with Russia. A Republican single-party sweep offers huge tax cuts but also a global trade war. Recession looms regardless.

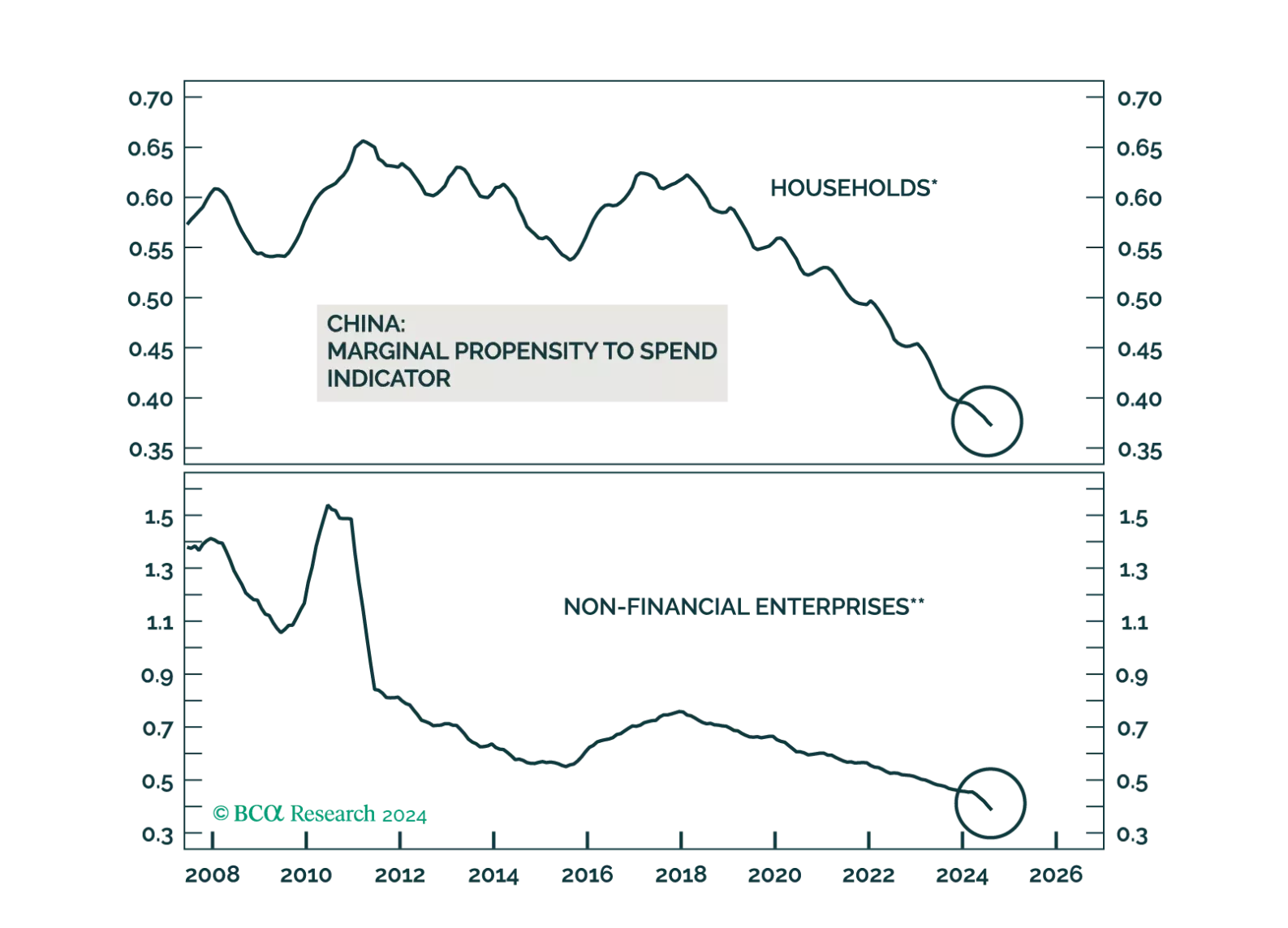

The Chinese economic data in its totality was uninspiring in August. Industrial production and retail sales growth decelerated year-on-year and corroborate the message from August’s import and credit growth data that domestic demand remains lackluster.…

Subdued demand for credit among Chinese private-sector businesses and households persisted through August. Outstanding loan growth decelerated from 8.7% y/y to 8.5%. Moreover, M1’s contraction deepened, from 6.6% to 7.3%. The lackluster appetite for…