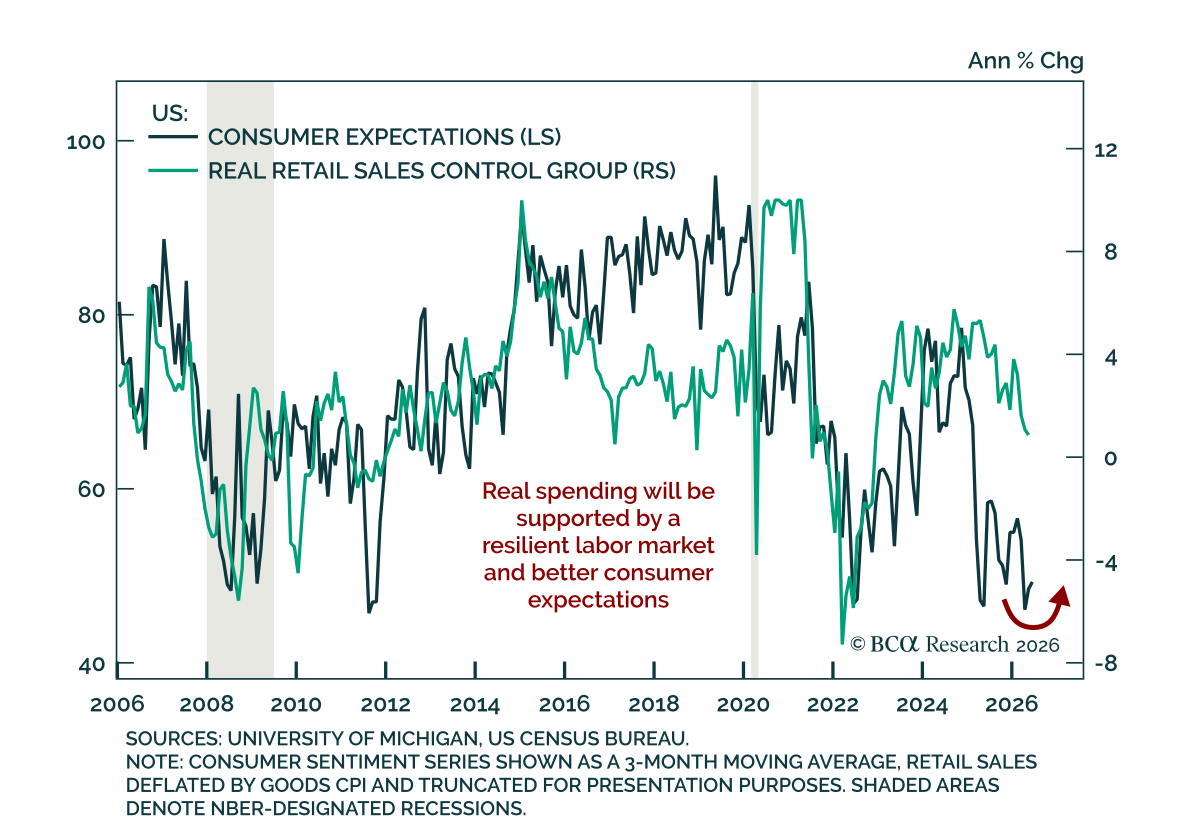

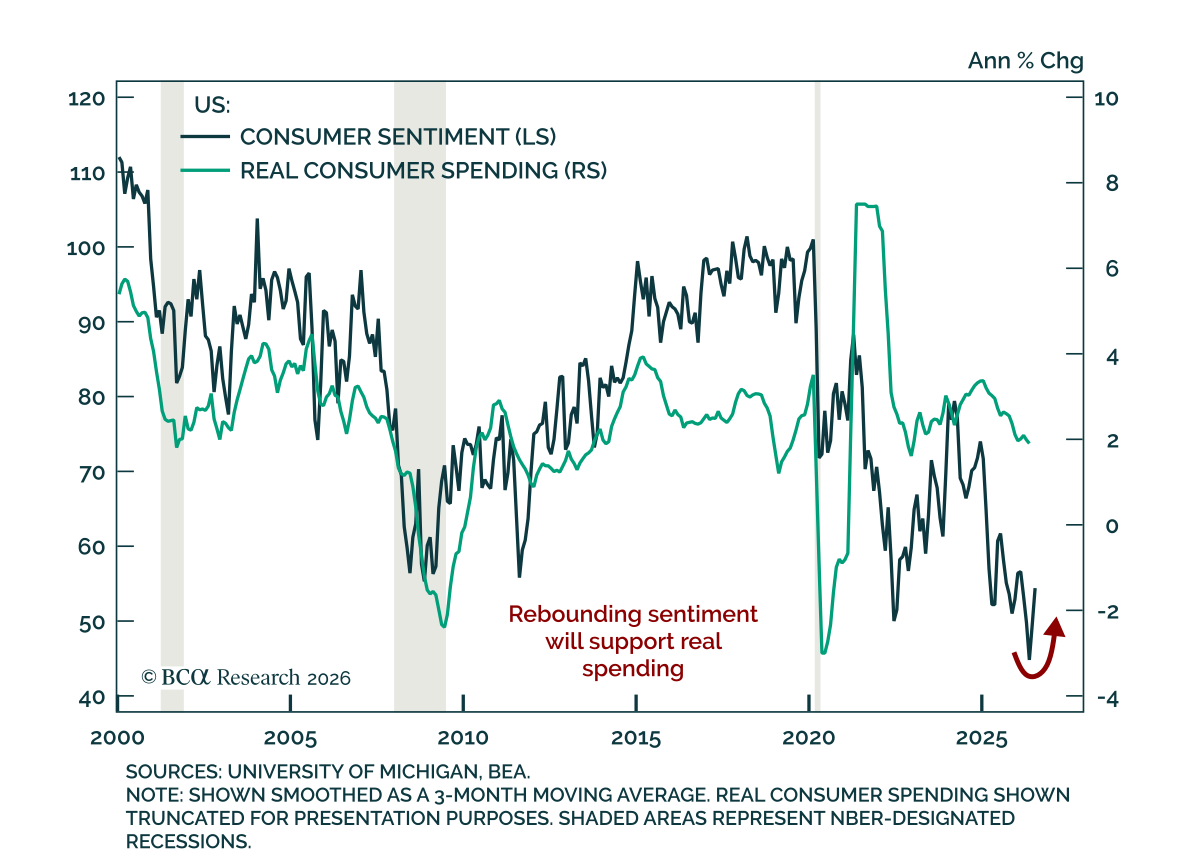

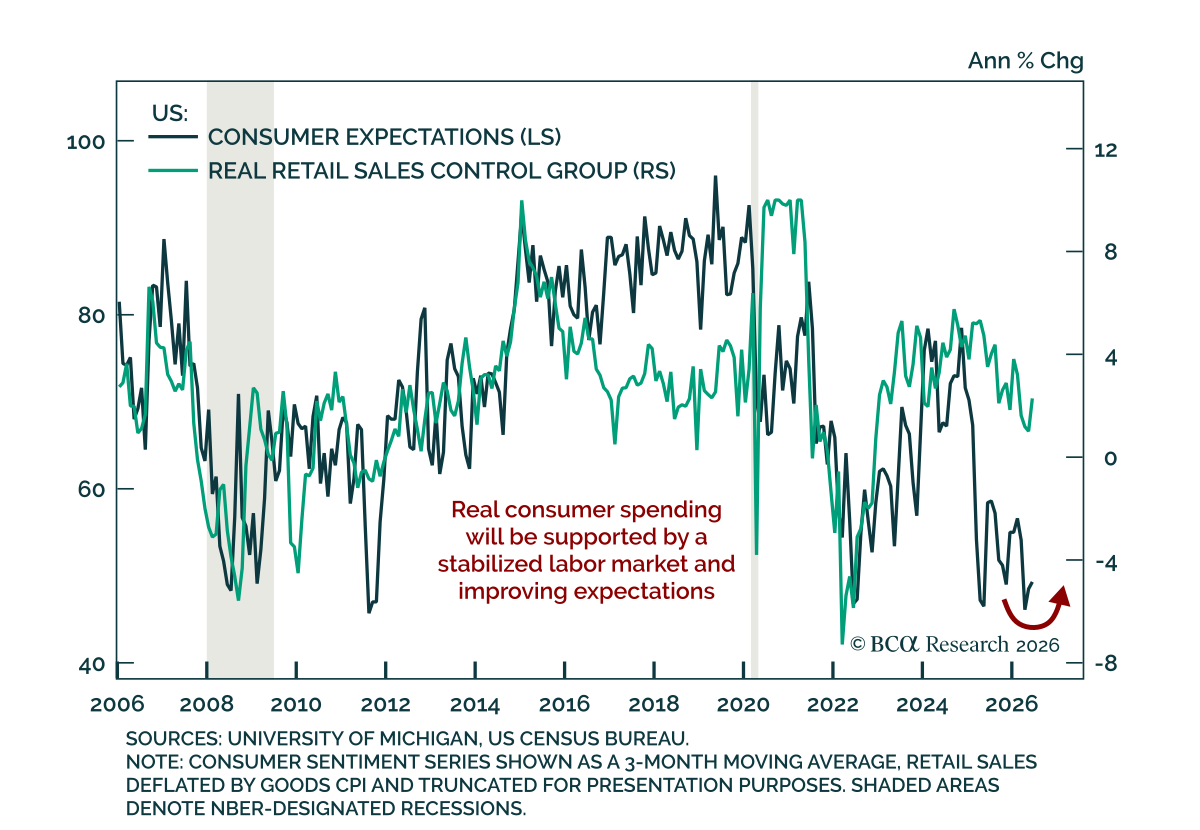

Consumer

As long as the AI boom keeps booming, all other investment considerations will remain on the back burner. However, if the AI trade fizzles, this would expose deep-seated problems within the global economy, which could very well lead to an economic downturn as early as next year.

News flash: Young urban professionals are not gasping under the weight of an impossible rent burden. Investors should not be led astray by lightly examined popular narratives.

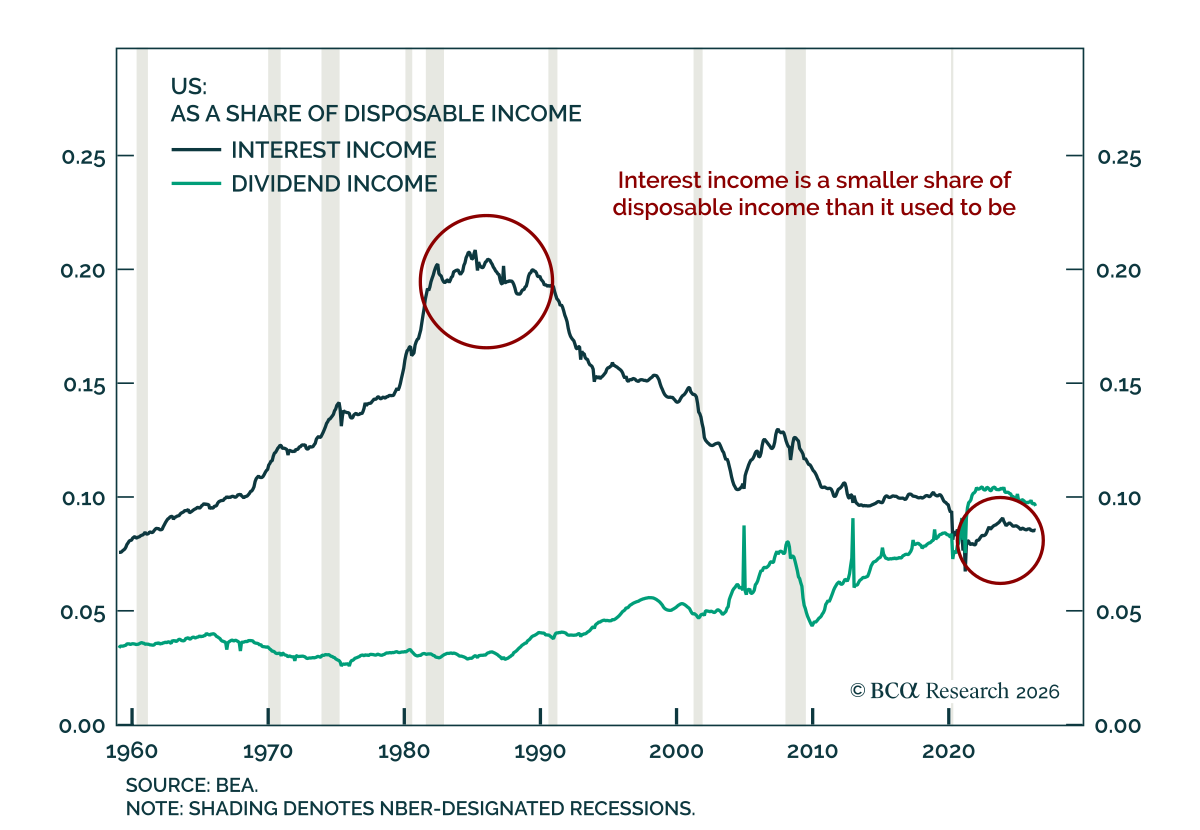

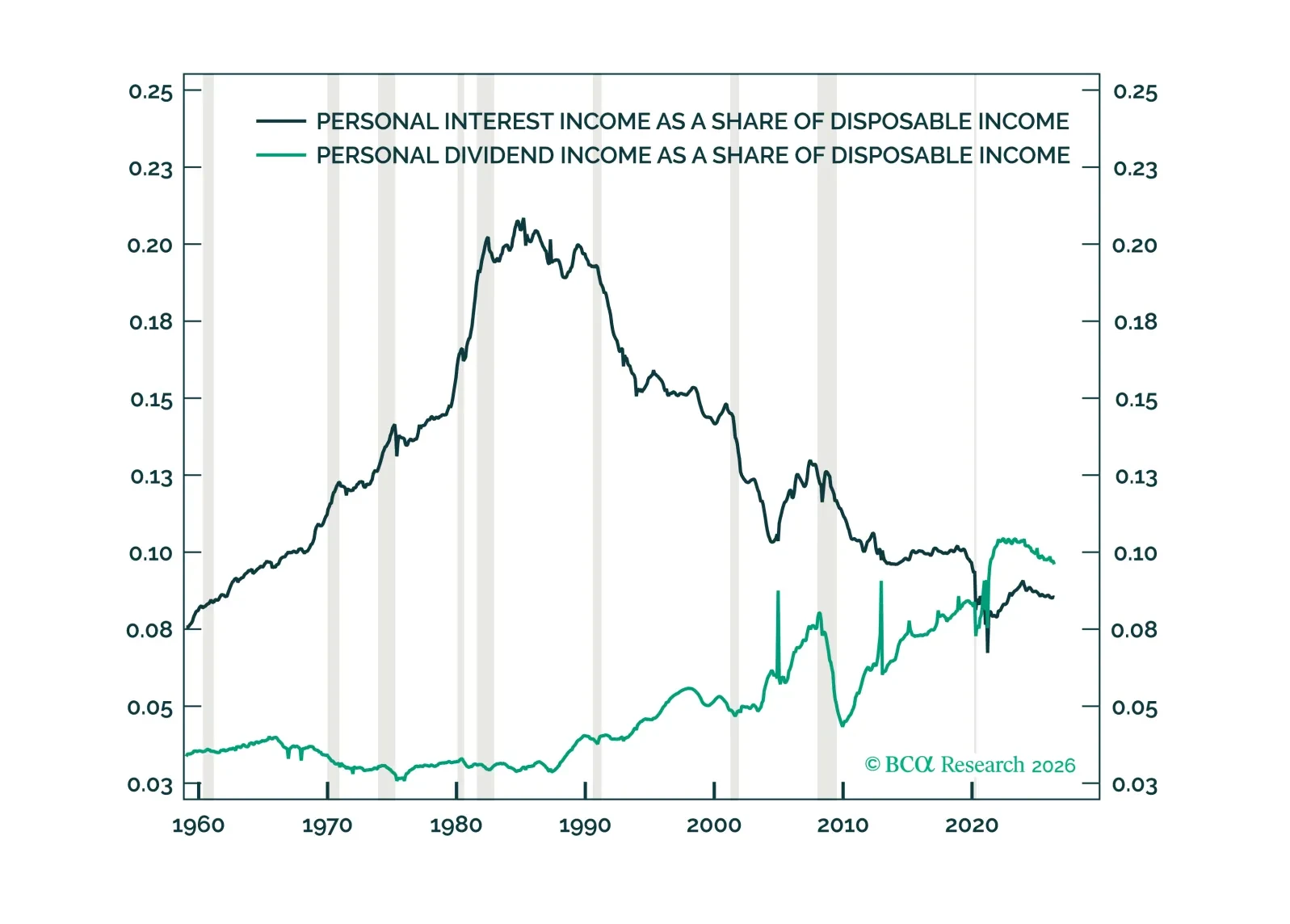

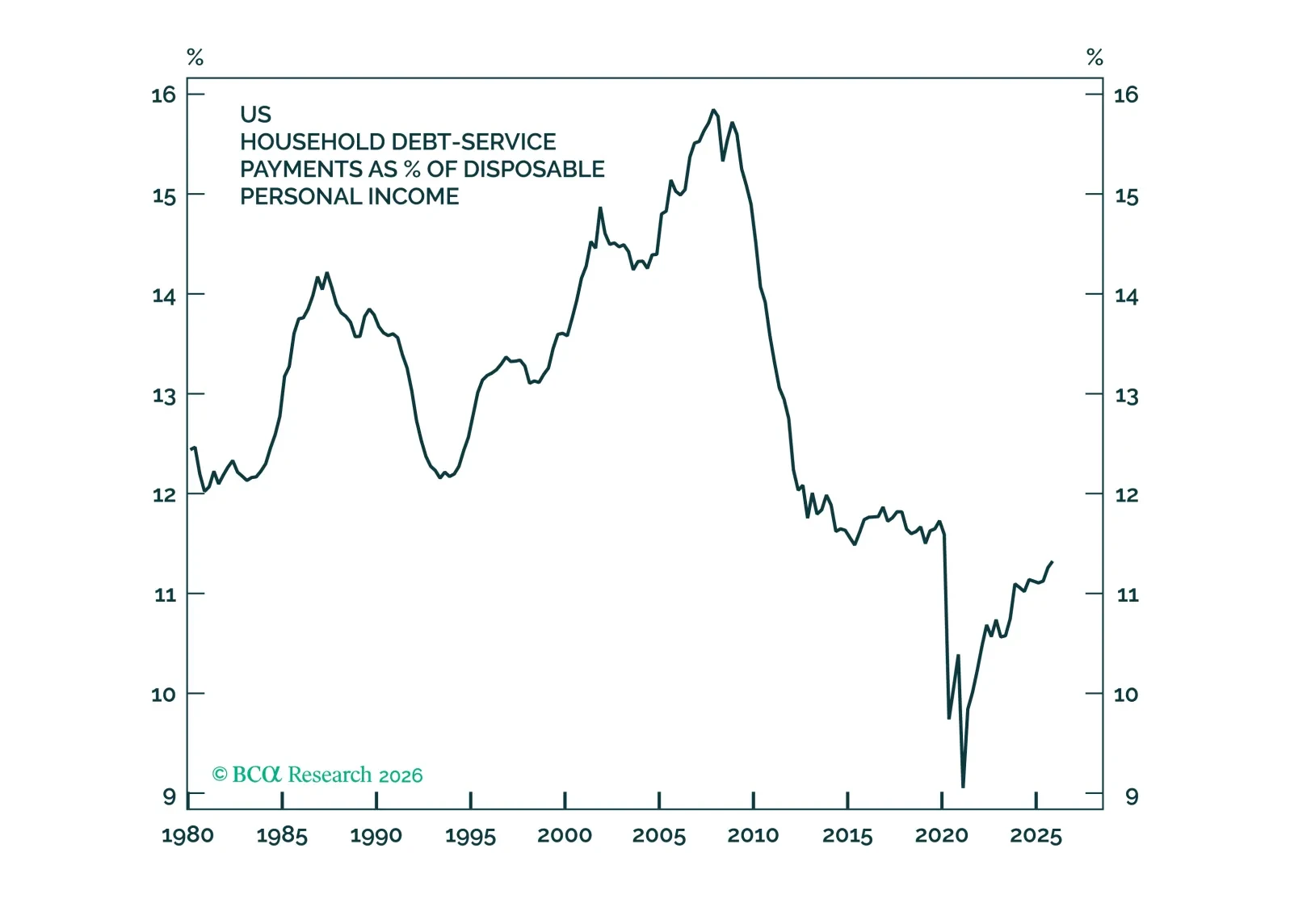

We are increasingly being asked if higher for longer interest rates could help spur consumption by boosting interest income. This report examines household income and balance sheet data to see if they might.

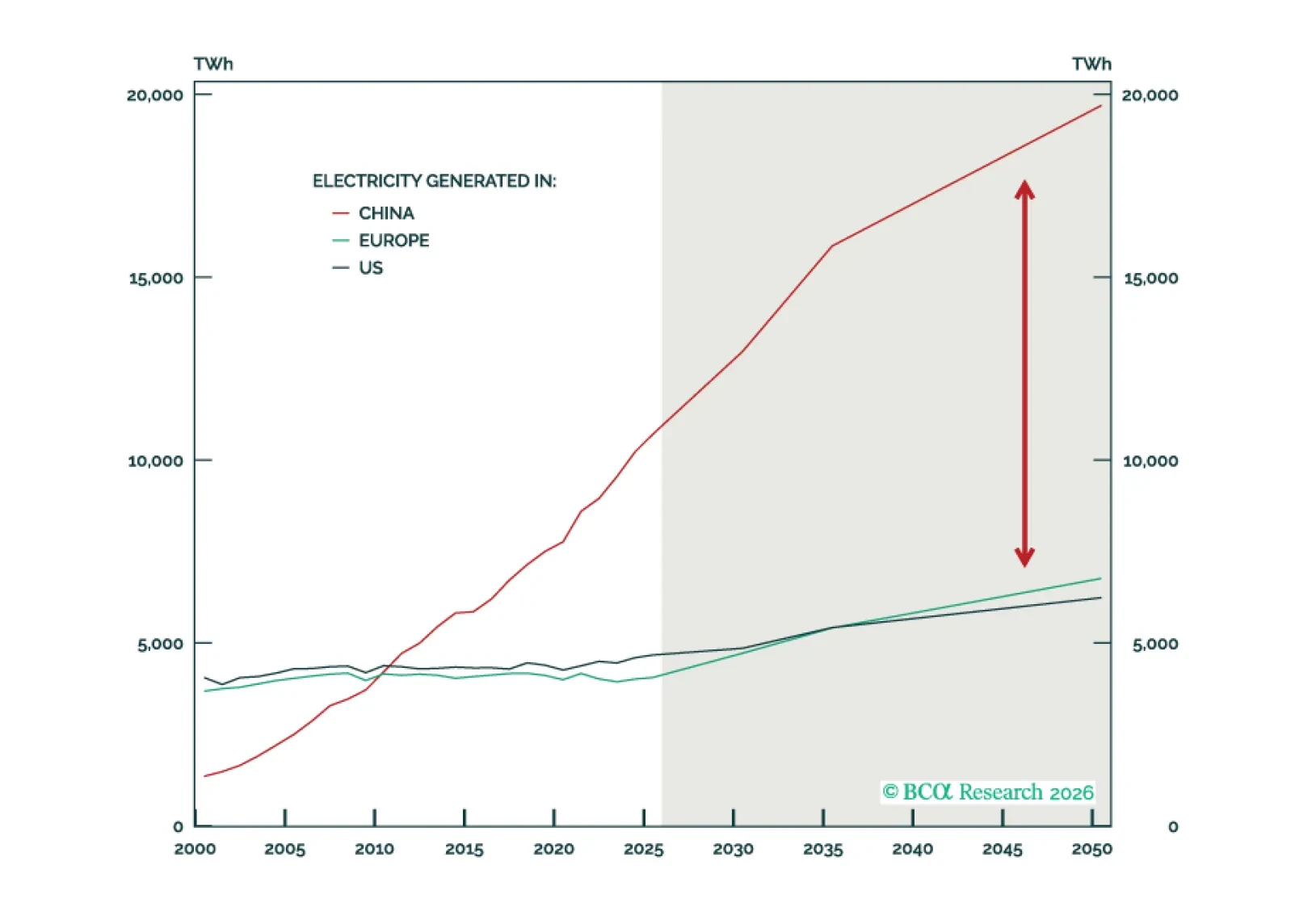

China holds a structural advantage in this "Age of Electricity" by operating the world's largest electricity system. However, this advantage has inherent limits, and the US remains competitive despite its challenges.

Section I maps how the broad distribution of wealth gains is supporting US consumption. Section II examines how countries can meet swelling electricity demand. The winners will find paths to build the infrastructure needed to power the high-tech future.

The most vulnerable households have whittled down their real debt balances while achieving significant real wealth gains. The combination has made consumption more resilient to income hiccups than in past cycles.