Consumer

With economic headwinds building and fiscal dynamics shifting, bond markets are at a turning point. Our latest note outlines why German bund yields are set to decline and why UK gilts are poised to outperform — and how to position accordingly.

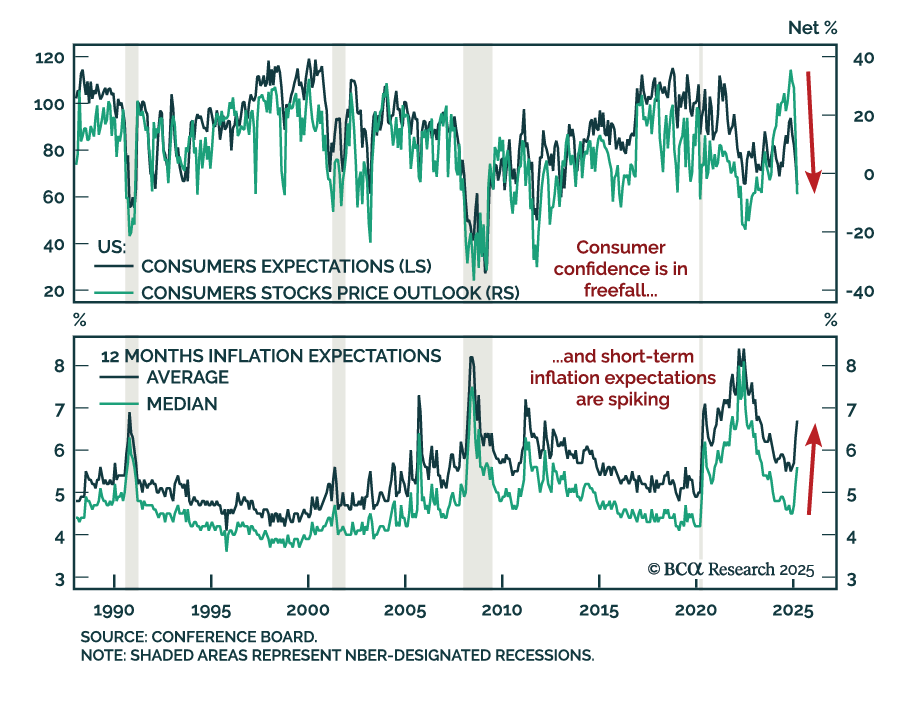

This morning’s weak consumer spending and strong inflation data reinforce our sense that the US economy is heading toward recession.

In this Second Quarter Strategy Outlook, we explore the major trends that are set to drive financial markets for the rest of 2025 and beyond.

The US economy faces a new investment regime characterized by tighter fiscal and easier monetary policies. The market corrected fast, and a short-lived equity rebound is likely. However, over the long term, US equities face economic headwinds.

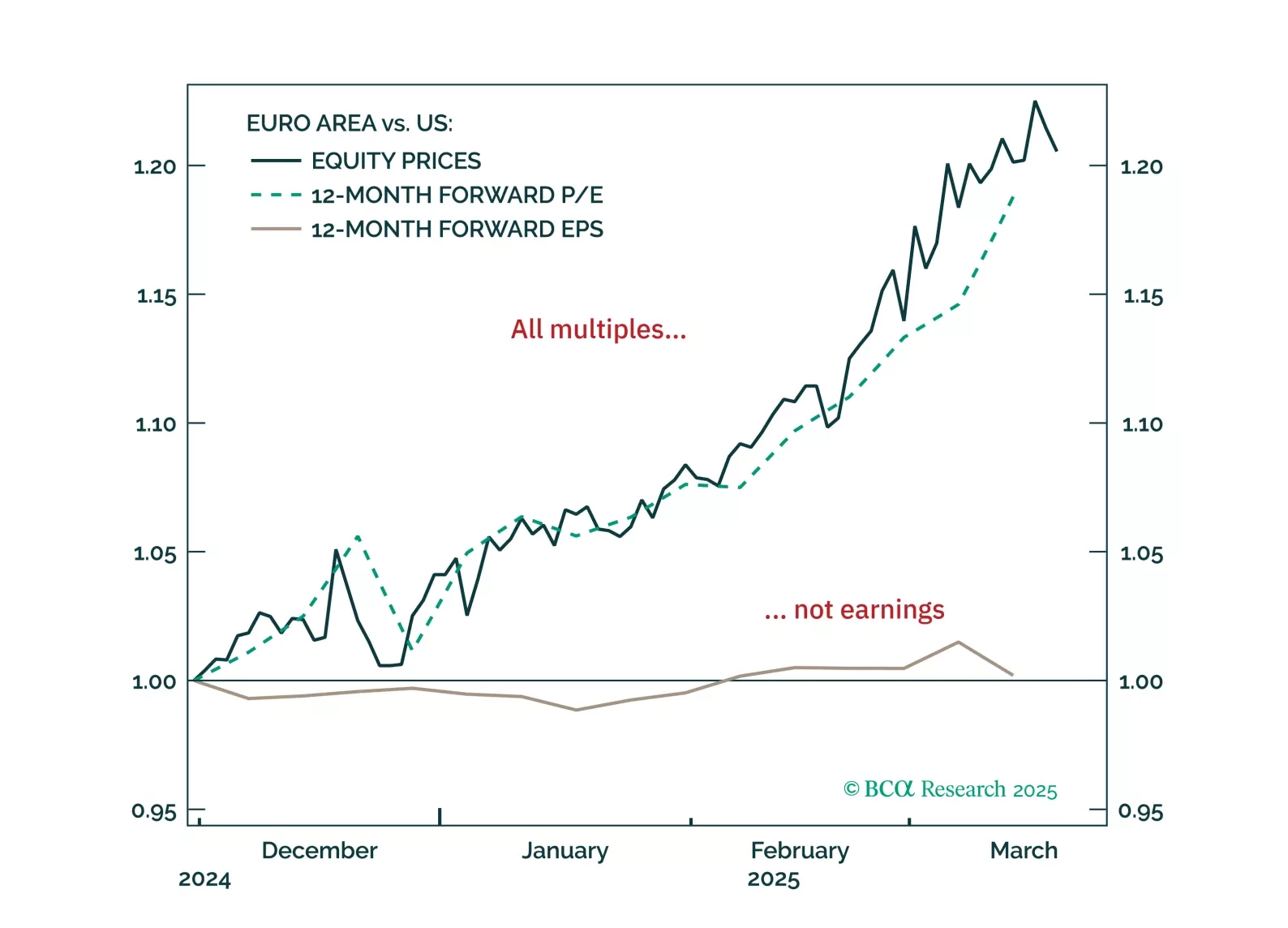

European equities have surged on hopes of a low-inflation boom—but the rally has likely gone too far, too fast. With a pullback now likely, how should investors position themselves over the next 3–6 months?