Consumer

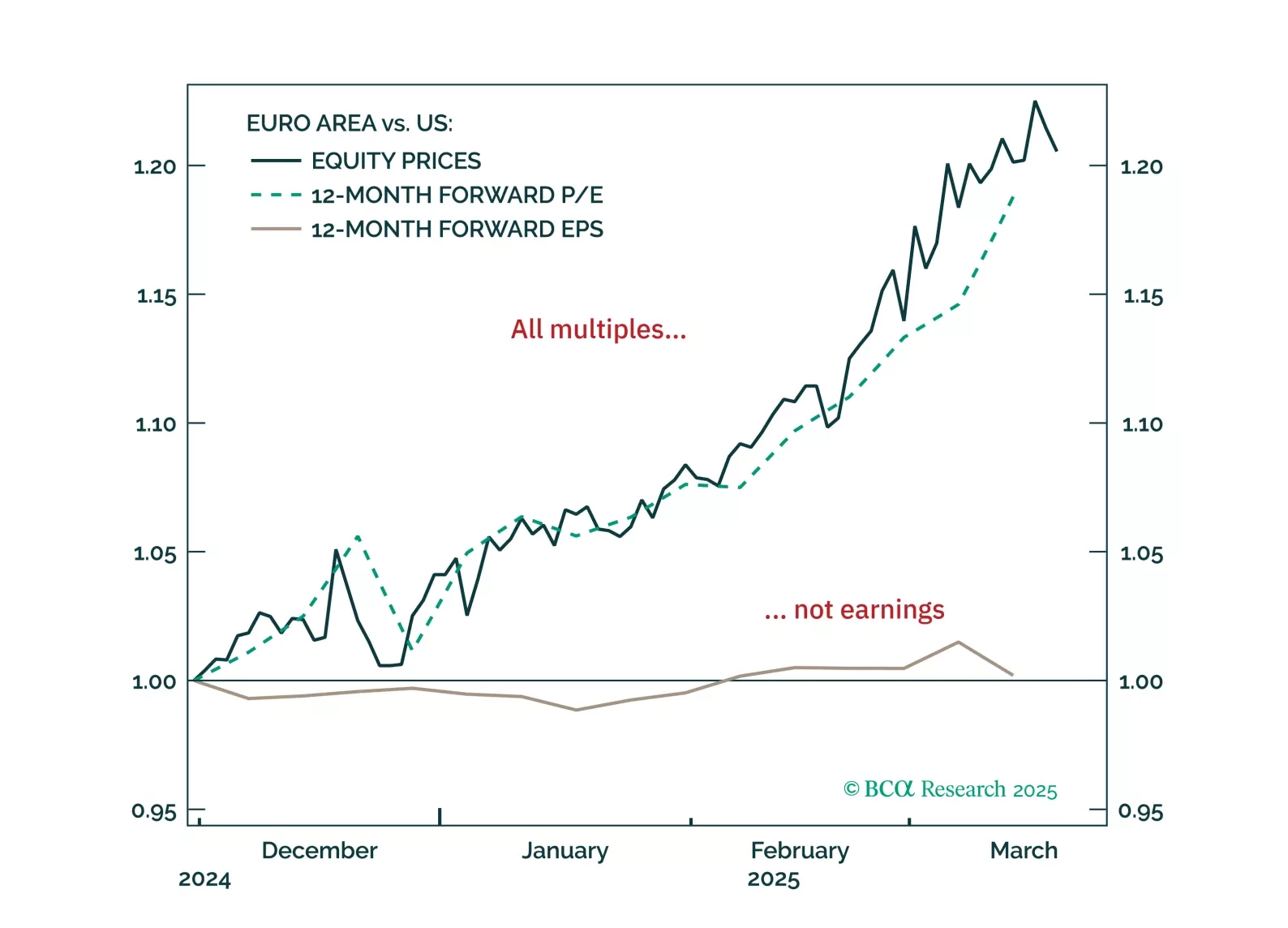

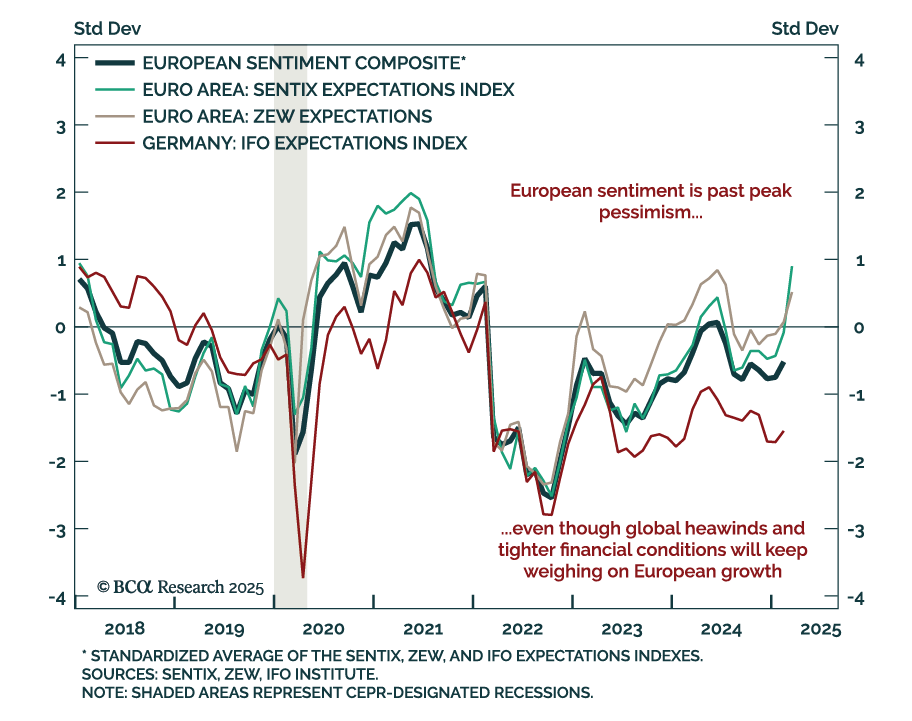

European equities have surged on hopes of a low-inflation boom—but the rally has likely gone too far, too fast. With a pullback now likely, how should investors position themselves over the next 3–6 months?

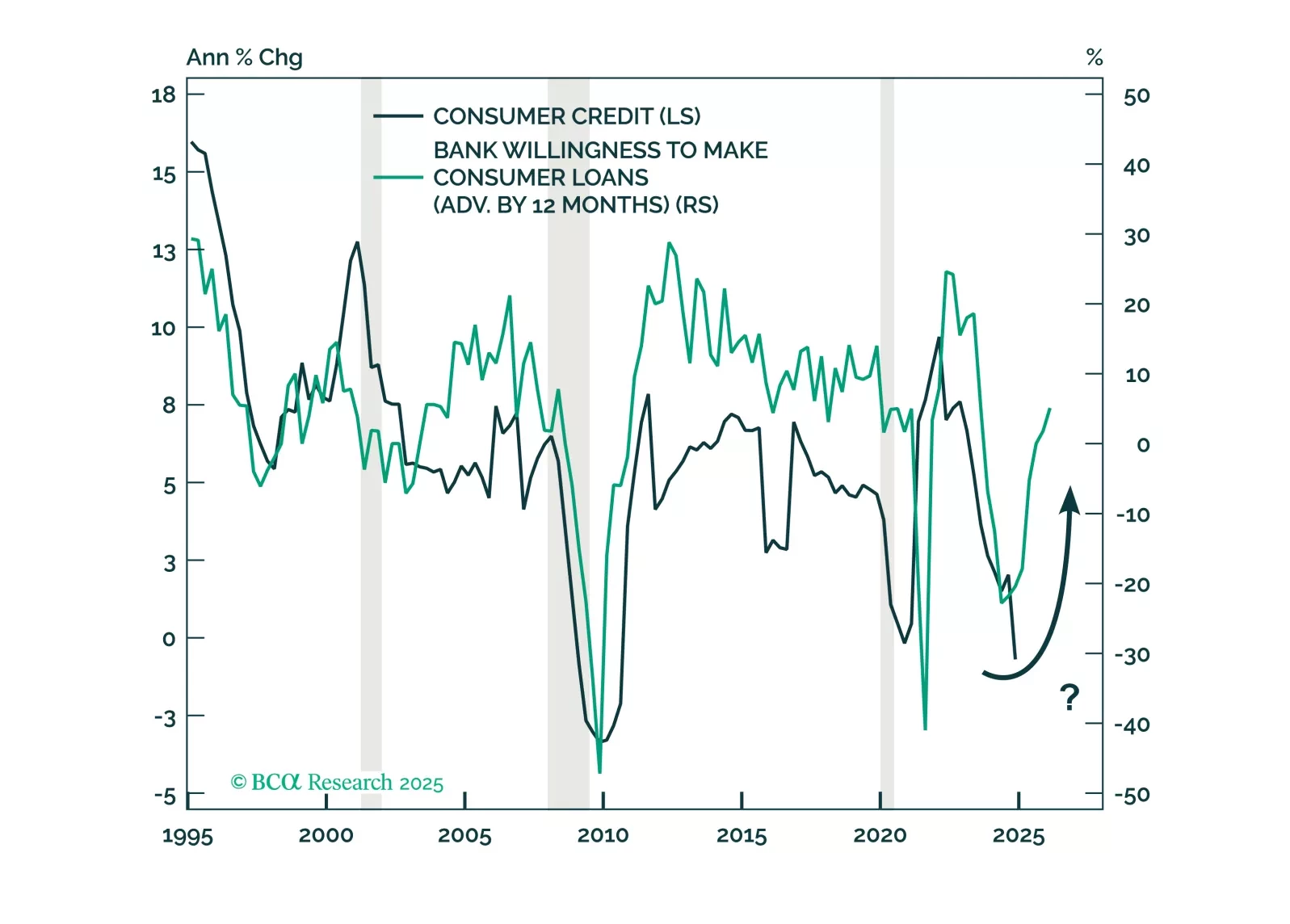

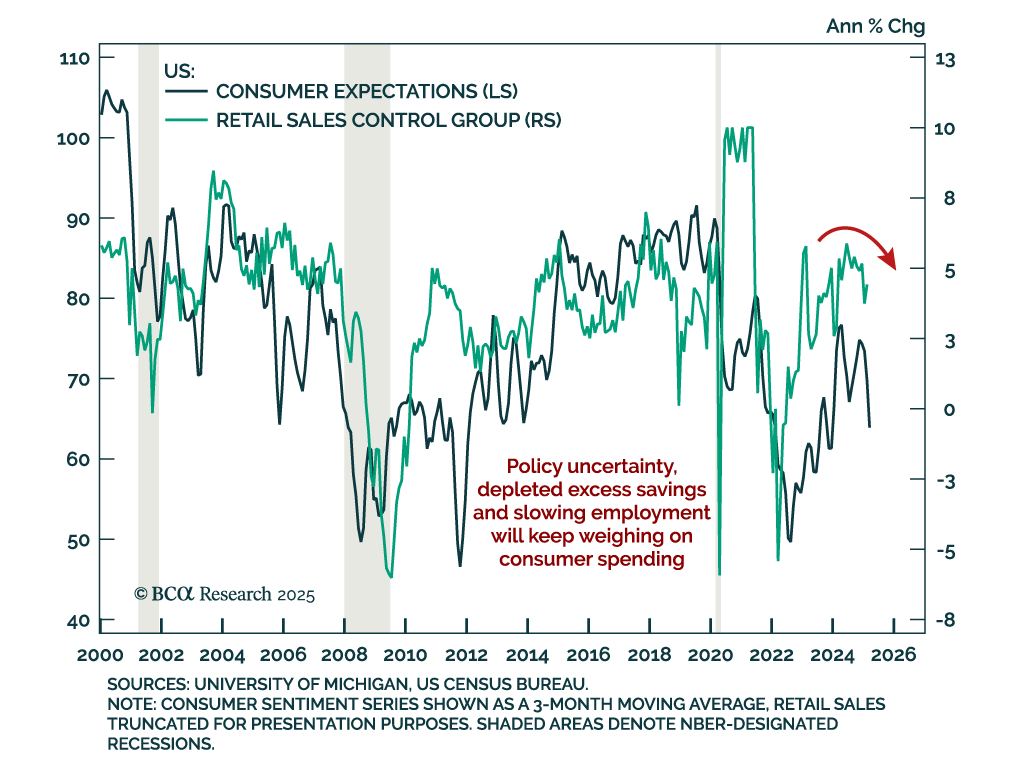

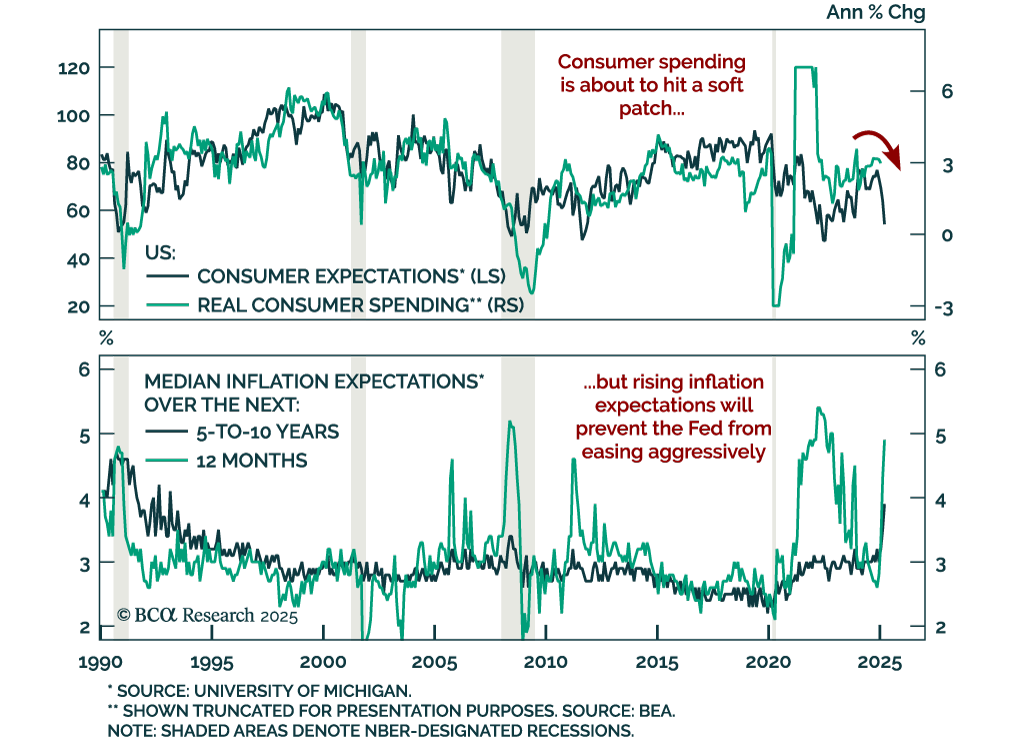

Households’ healthy balance sheets do not square with the rise in credit cards and auto loans delinquencies. The tailwinds that have supported higher-income cohorts’ spending have faded, presaging broad-based deterioration in credit performance.

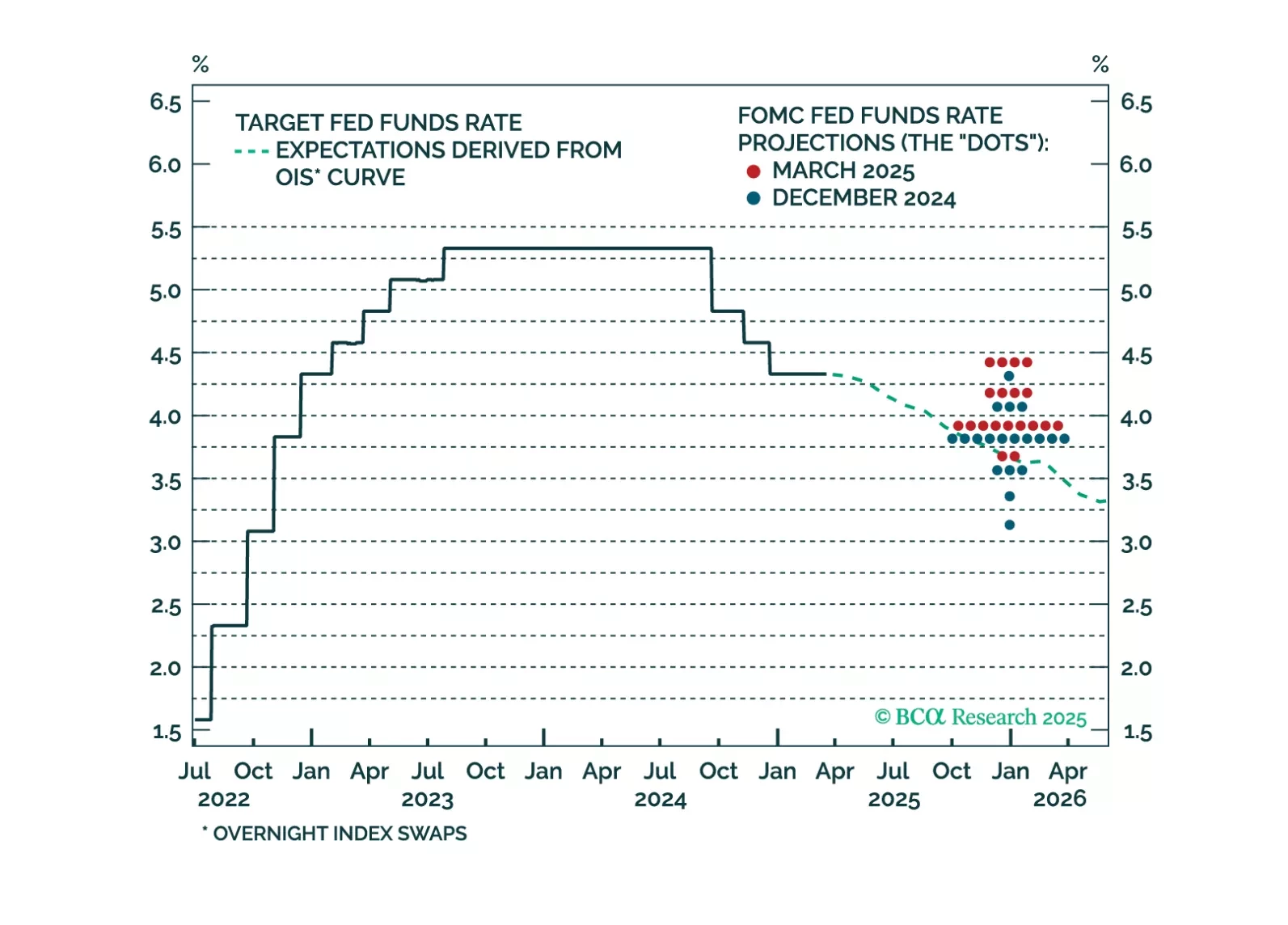

The market reaction to this afternoon’s Fed meeting looks overdone. Investors could be in for a hawkish surprise when it becomes apparent that the Fed won’t ease policy into higher tariff-driven inflation prints.

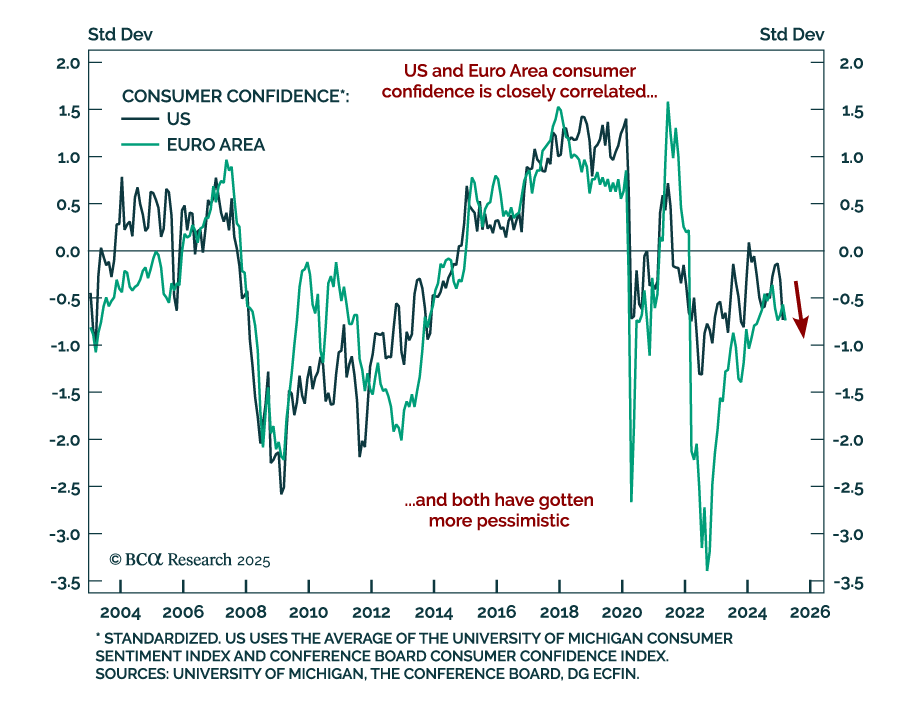

The Q4 earnings results were spectacular but are now in the rear-view mirror. Now, investors are laser-focused on tariff threats, earnings headwinds brought about by a stronger dollar, and an unhappy consumer. Our analysis of earnings commentary found that, while companies often refer to tariffs during their earnings calls, most are perplexed and still in a “wait and see” mode. A strong dollar is negative for earnings, but the recent dollar retrenchment will bring relief. Wealthy consumers are still spending, but there are early signs of stress.