Consumer

The November flash Eurozone inflation estimate met expectations, with headline HICP accelerating to 2.3% y/y from 2.0% in October, above the ECB’s target. Core inflation remained constant at 2.7%. At 3.9%, services inflation is still elevated. The outlook…

The Fed’s preferred measure of inflation, core PCE, met expectations of 0.3% m/m in October, and accelerated to 2.8% y/y from 2.7% in September. Inflation rose on the back of hot inputs from the PPI report, which is not expected to last. The market-based core…

Consumer confidence came in as expected in November, with The Conference Board’s index rising to 111.7 from 108.7 in October, a level not seen since August 2023. Both the assessment of consumers’ present and future situation drove the increase. The…

Our US Investment Strategy team analyzed recent US consumer trends through the lens of major retailers’ earnings calls, which highlighted increasingly prudent spending. Consumer caution is apparent in these earnings calls as pandemic-era savings fade, and…

The force of the post-election momentum leads us to believe we could be stopped out of our defensive positioning before the week is out, but we still believe in our recession call. If we are eventually stopped out, we will seek a more opportune entry point to bet against risk assets once the election fever runs its course.

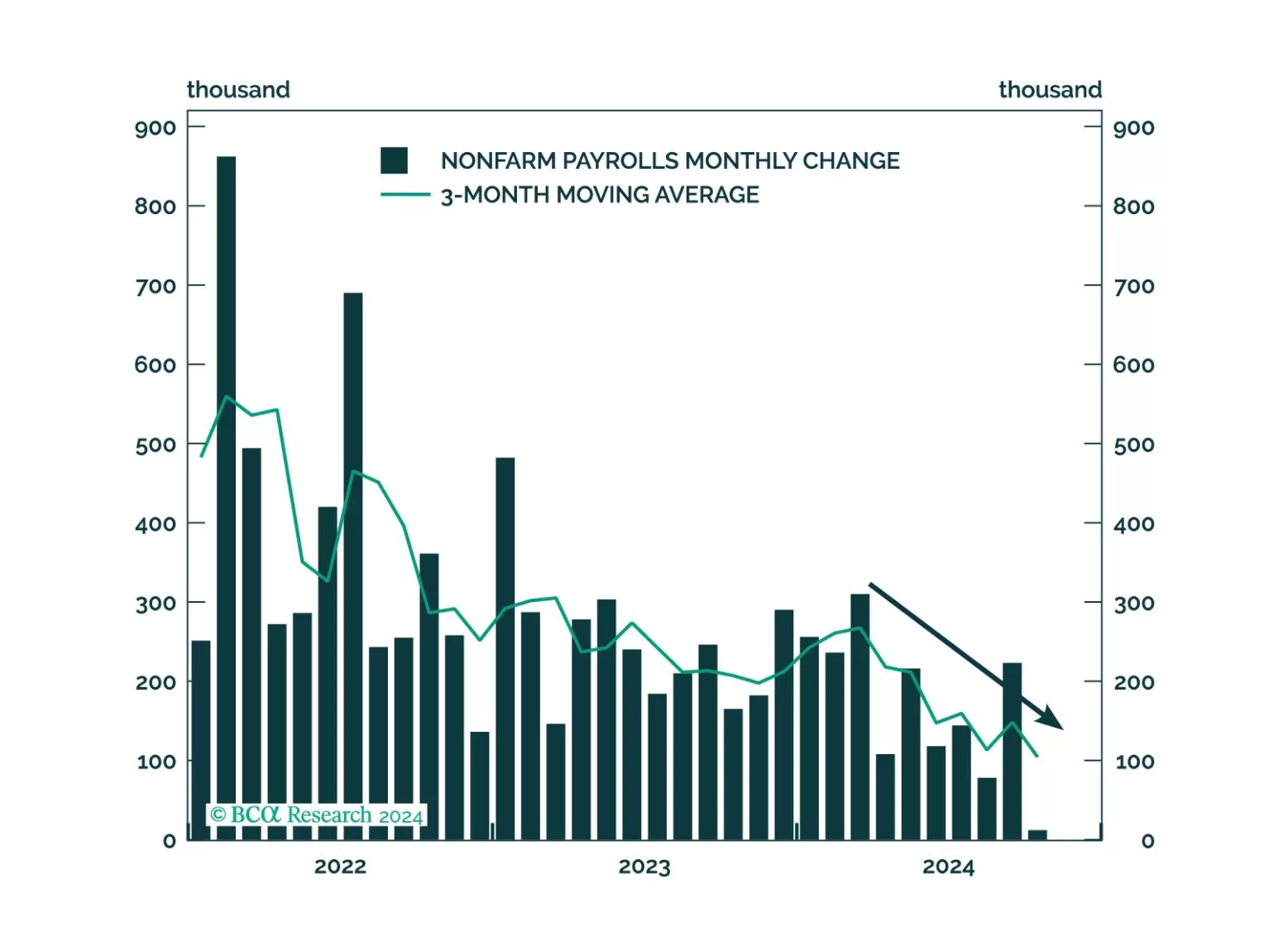

The October US jobs report had mixed signals and was skewed by hurricanes and industrial strikes. Unemployment met expectations by staying unchanged at 4.1%, although it rose nearly 0.1 percentage point on an unrounded basis. Nonfarm payrolls were flat with…

The Fed’s preferred measure of inflation, core PCE, met expectations of a reacceleration to 0.3% month-on-month, and reached 2.7% year-over-year. The rest of the Personal Income and Outlays report showed solid consumption growth, although supported by a…

As US consumers remain one of the few engines of global growth, our US Investment Strategy colleagues took a deep dive on consumer trends, augmented with comments from US banks’ earnings calls. Middle-aged consumers have fallen behind the young and old.…

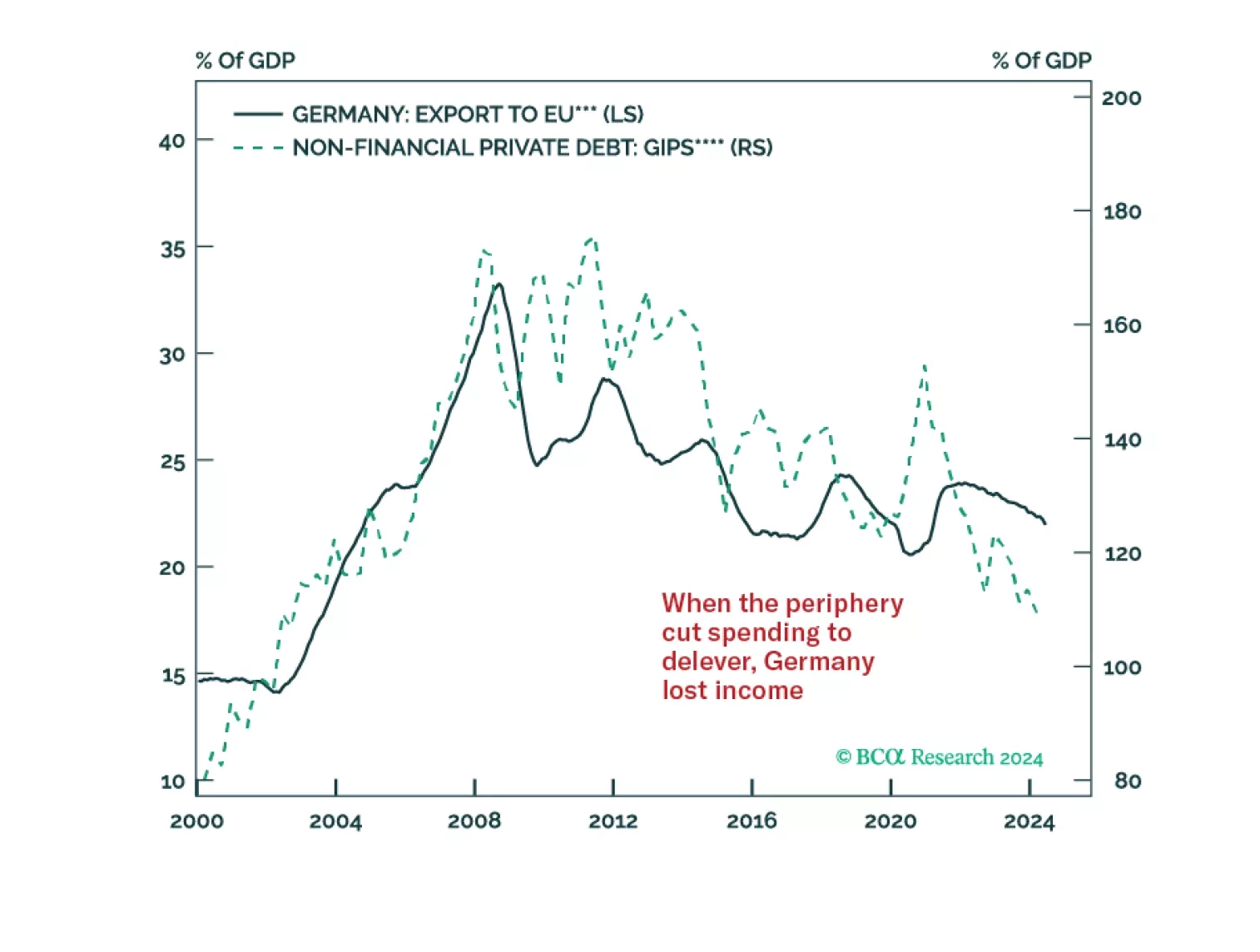

Germany’s economy has lagged that of the rest of Europe for nearly 10 years. So have German stocks. Investors are extrapolating these trends to bet on the country’s deindustrialization. Could Germany manage to beat dismal expectations?