Consumer

Chinese export growth in USD terms accelerated from 7.0% y/y to a larger-than-expected 8.7% in August. China’s exports to its major trading partners (US, EU and ASEAN) were all growing in August on a year-on-year basis, though at a decelerating pace in the US…

Consumer credit rose by USD 25.5bn in July (to USD 5,093.7 bn outstanding), more than twice the expected growth. However, revisions suggest that June’s consumer credit growth was slower than initially reported (USD 8.9bn to 5.2bn). Nonrevolving credit…

Eurozone GDP’s final estimate indicates that growth was slower than expected in Q2. Output grew 0.2% q/q in Q2, compared to 0.3% previously reported. A significant downward revision to capex (2.2% contraction against 1.8% previously estimated) drove the…

August nonfarm payrolls expanded by 142 thousand workers, from a downwardly revised 89 thousand and below expectations of 165 thousand. Payroll growth fell to a four-year-low of 116 thousand on a 3-month moving average basis. Notably, pro-cyclical…

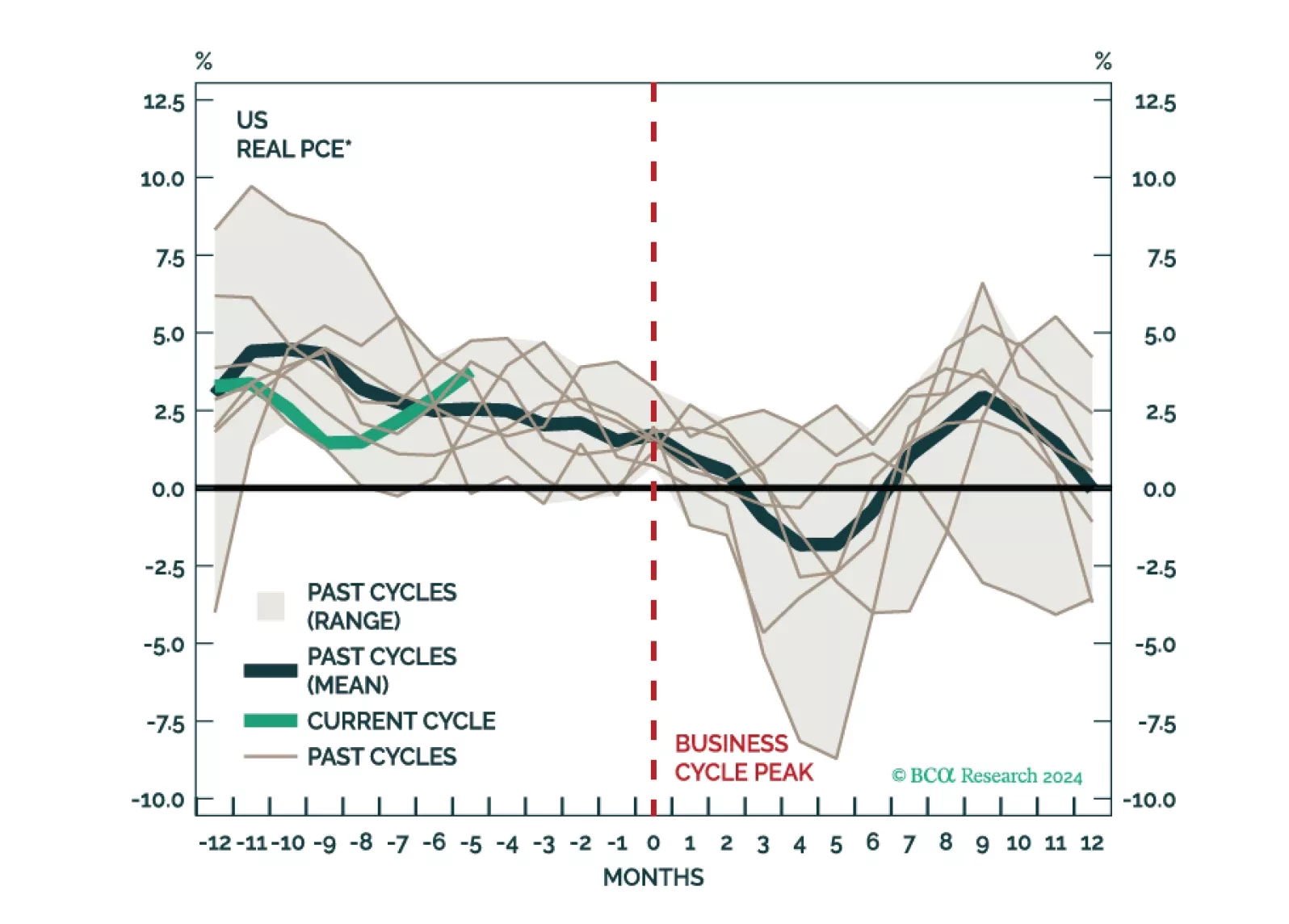

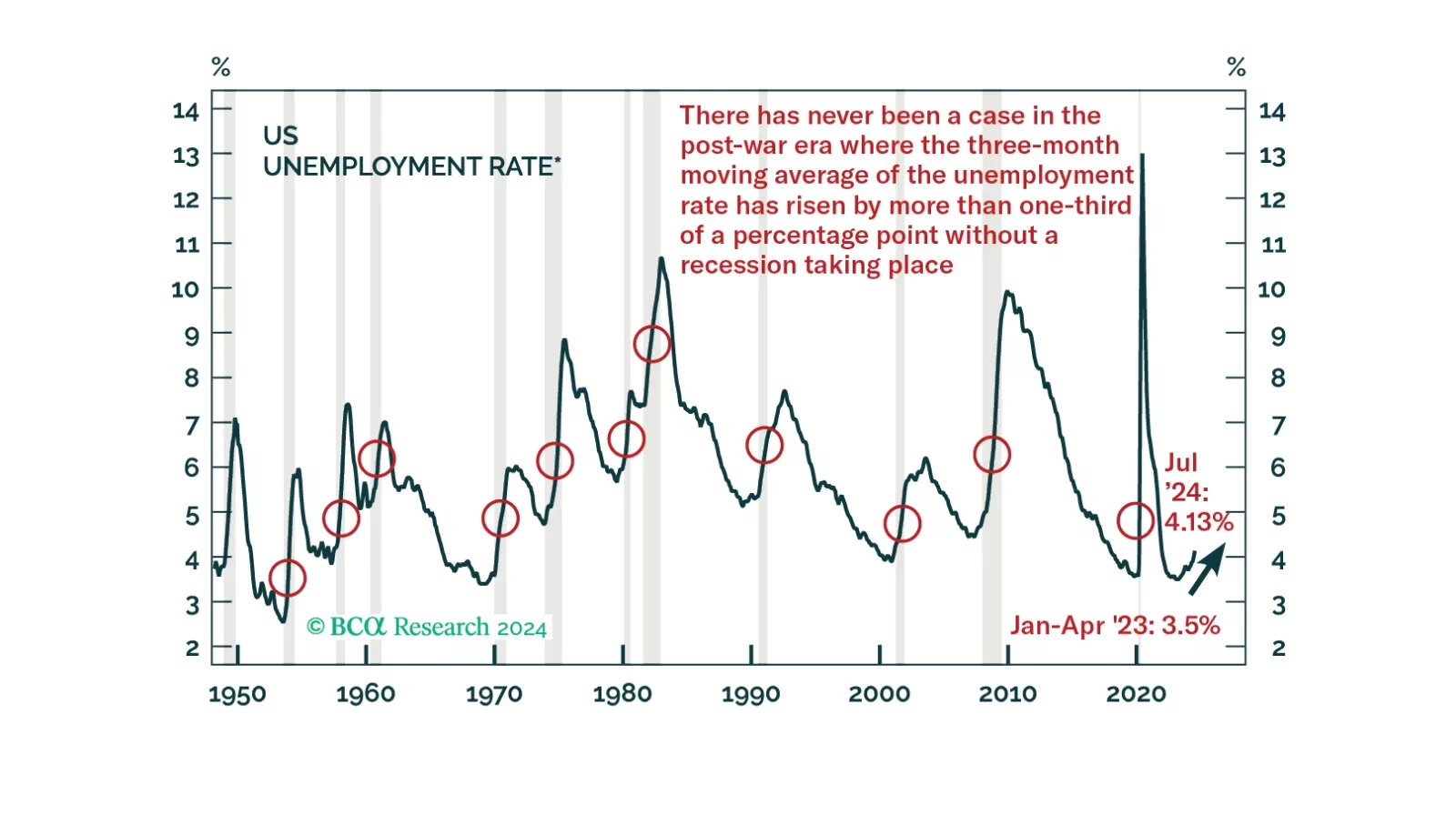

In this Special Report, we analyze the behavior of economic data leading up to US recessions and discuss some common patterns.

The ISM services PMI remained mostly stable in August, extending a second consecutive month of modest expansion. The headline index ticked 0.1 point higher to 51.5. However, although new orders continued to expand, new export orders fell a whopping 7.6…

The Fed’s Beige Book compiles qualitative input sourced from business and other organizational contacts in each of its 12 Districts. It precedes FOMC meetings by a couple of weeks and is meant to help participants trace the evolution of economic conditions. …

US job openings declined from a downwardly revised 7.91 million to 7.67 million in July, the lowest level since 2021 and well short of expectations of 8.1 million. The downward revision indicates that labor demand actually declined in June, when it was…

The Q2 2024 earnings season is drawing to a close with 93% of S&P 500 companies having reported results as we go to press. Nearly 80% (60%) of companies have topped earnings (sales) expectations in Q2, according to Factset. Excluding Materials and Real…

Our annual end-of-summer chartbook report traces the labor market deterioration that led us to downgrade equities at the beginning of August. It also highlights the soft-landing expectations that the credit and equity markets are discounting. We like the risk-reward profile of our newly defensive stance.