Consumer

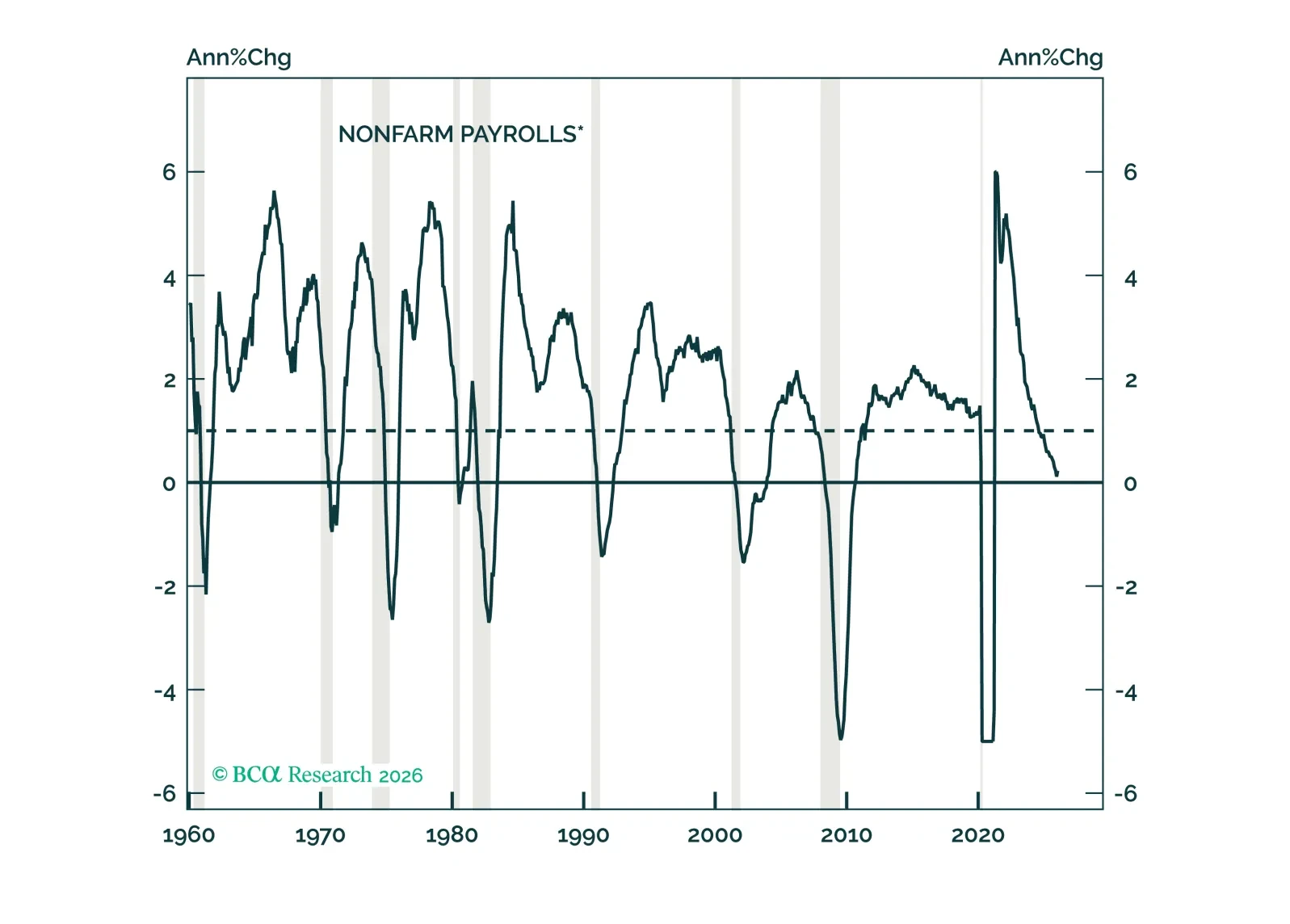

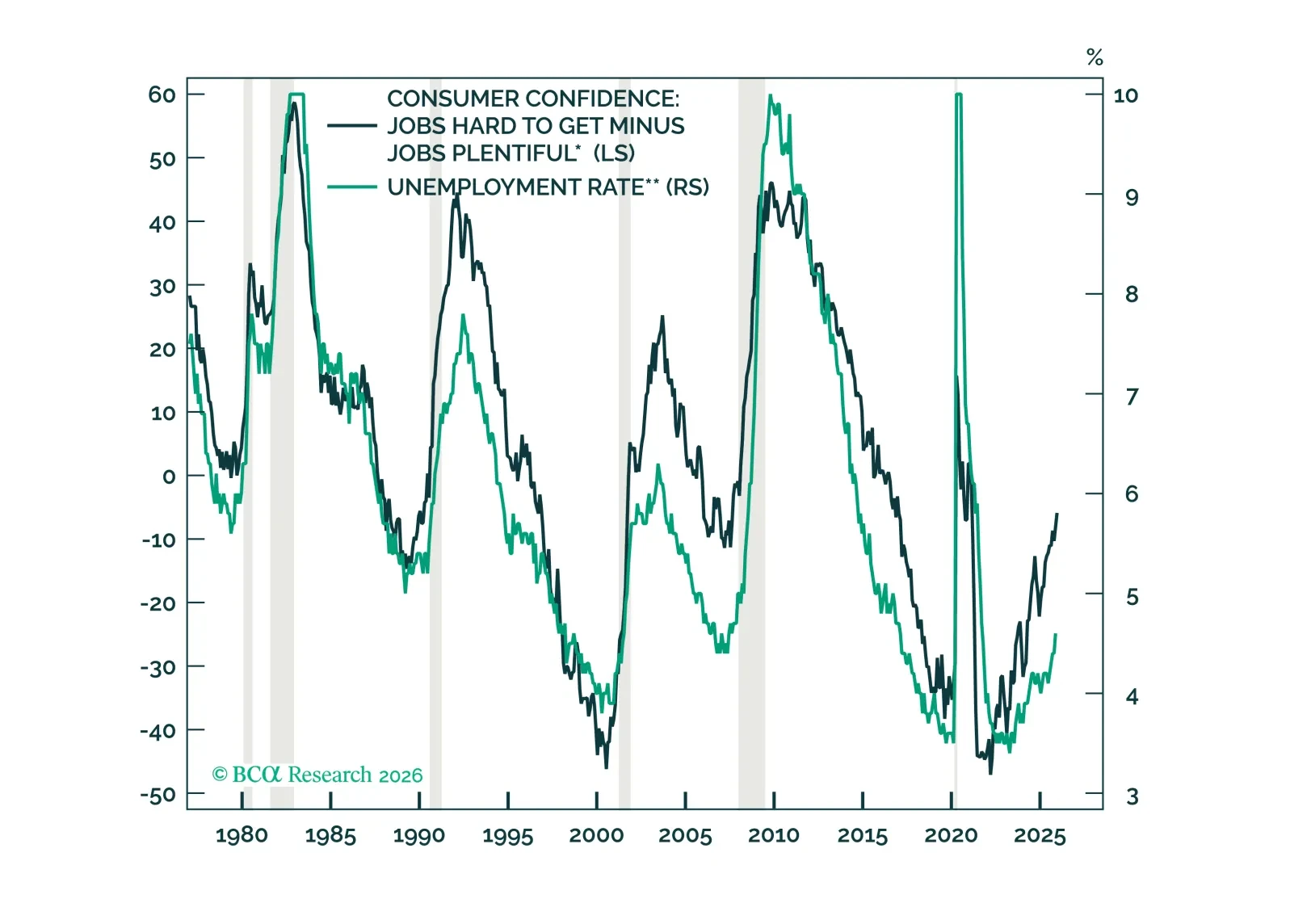

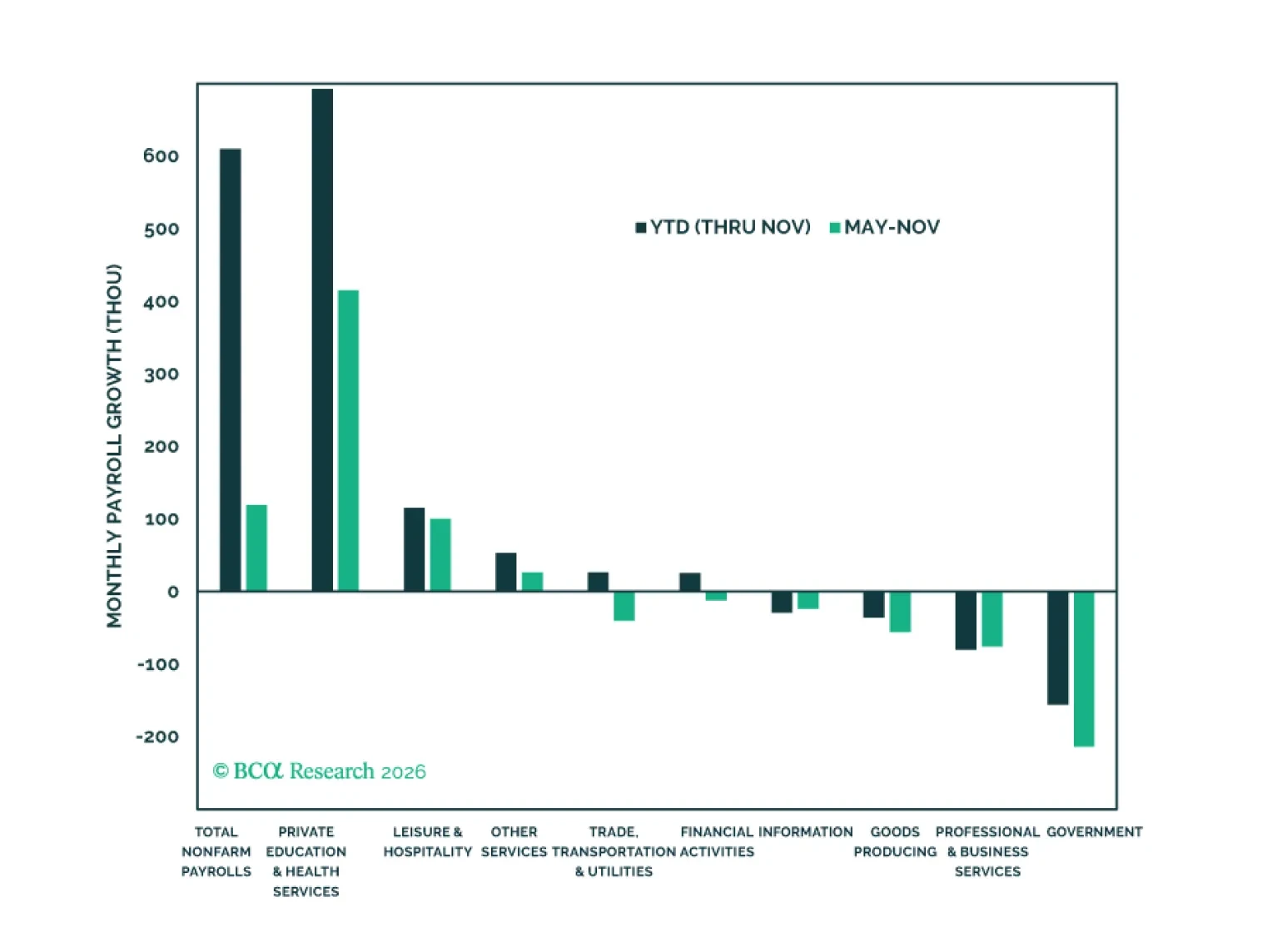

The annual benchmark payrolls revisions revealed that the labor market has been weaker for longer than initially reported. The probability that a crack in consumption is just around the corner is much reduced and we have therefore dialed back our recession expectations. Though our asset allocation recommendations remain neutral across the board, we are more optimistic than we were at the beginning of the year.

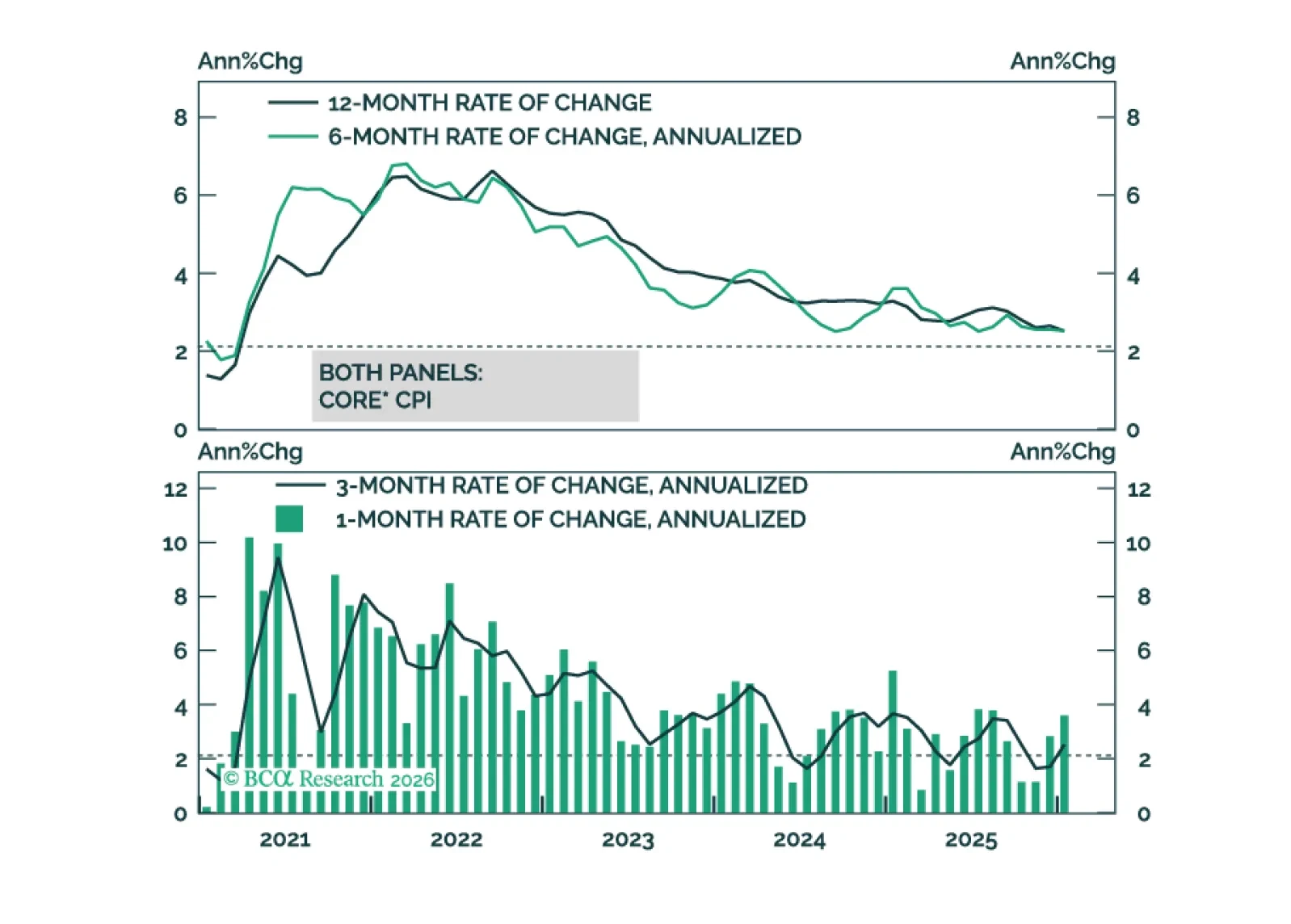

Core inflation will get close to the Fed’s 2% target by the end of this year.

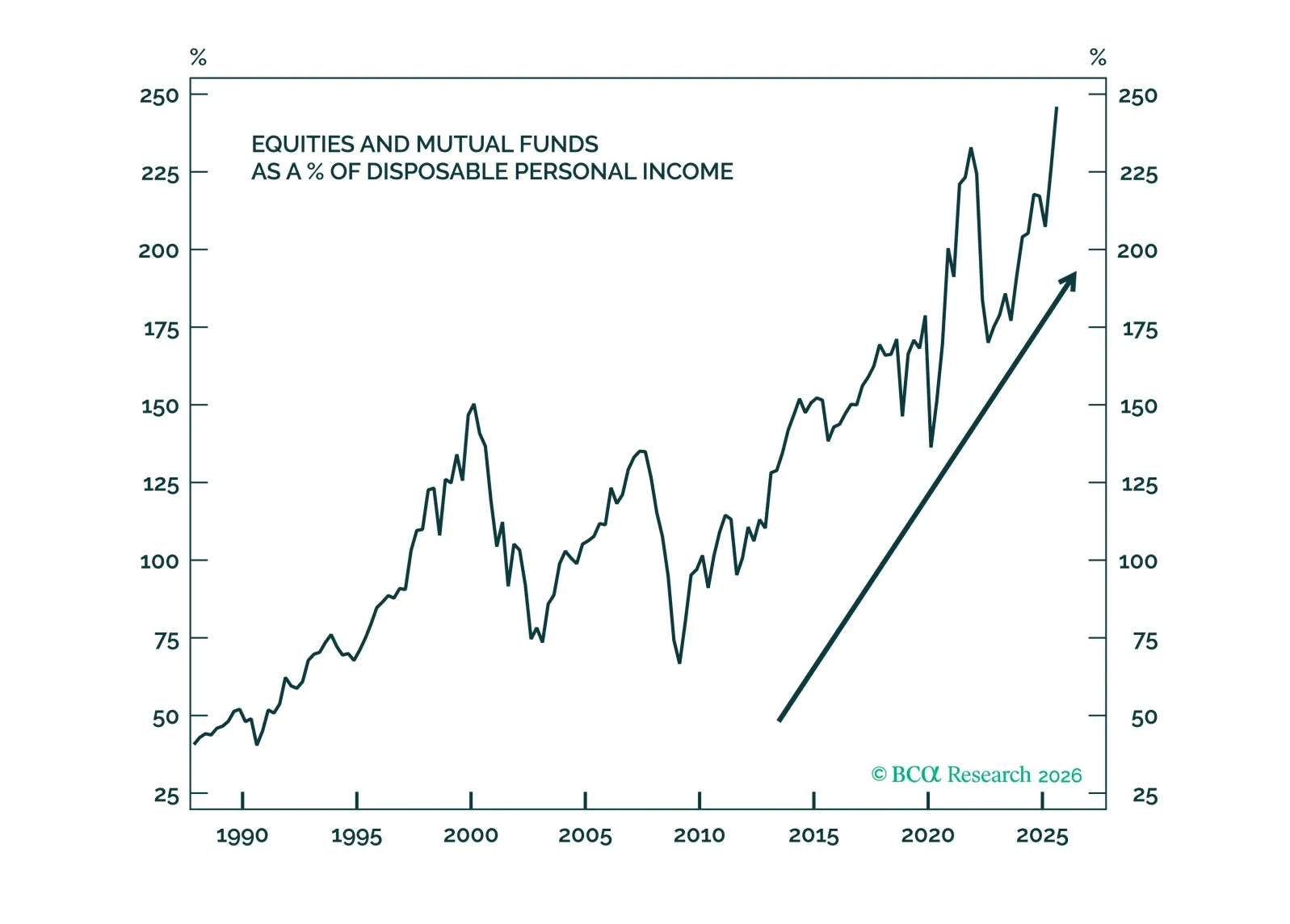

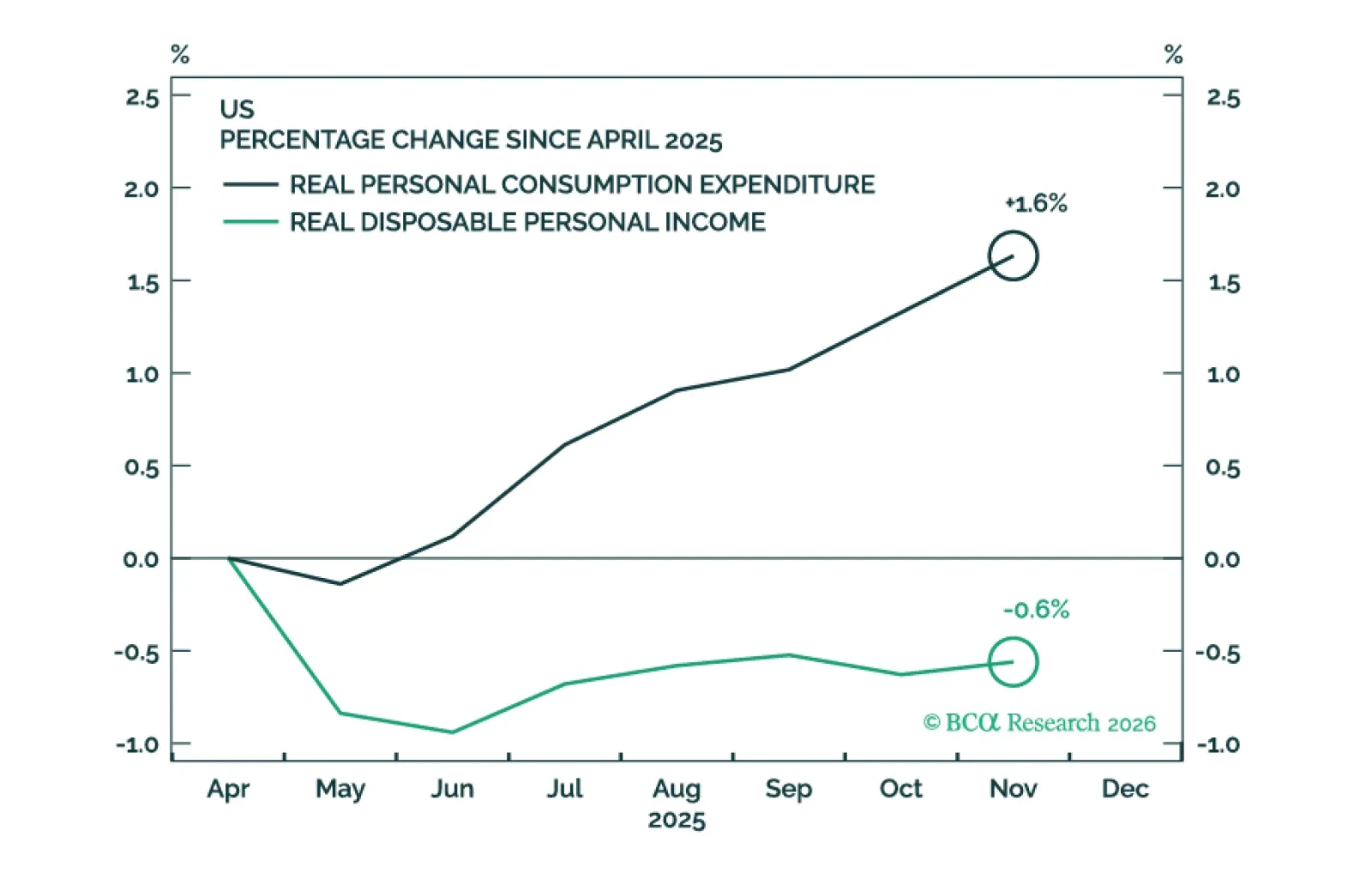

It appears that households have been able to spend more than they’ve earned since May by dipping into their swollen brokerage accounts. Bulked-up equity holdings could herald a future where consumption is more sensitive to stock market ups and downs. That’s great in bull markets but could be an unexpected drag on activity when the next bear arrives.

In Section I, Doug highlights the risks to US consumption if job growth does not soon recover. The US economy has yet to pass its tipping point, however, arguing against defensive positioning for now. In Section II, Jonathan examines whether the AI “scaling laws” are likely to hold. They will over the near term, but cracks are already beginning to form in the narrative of ever-improving AI.

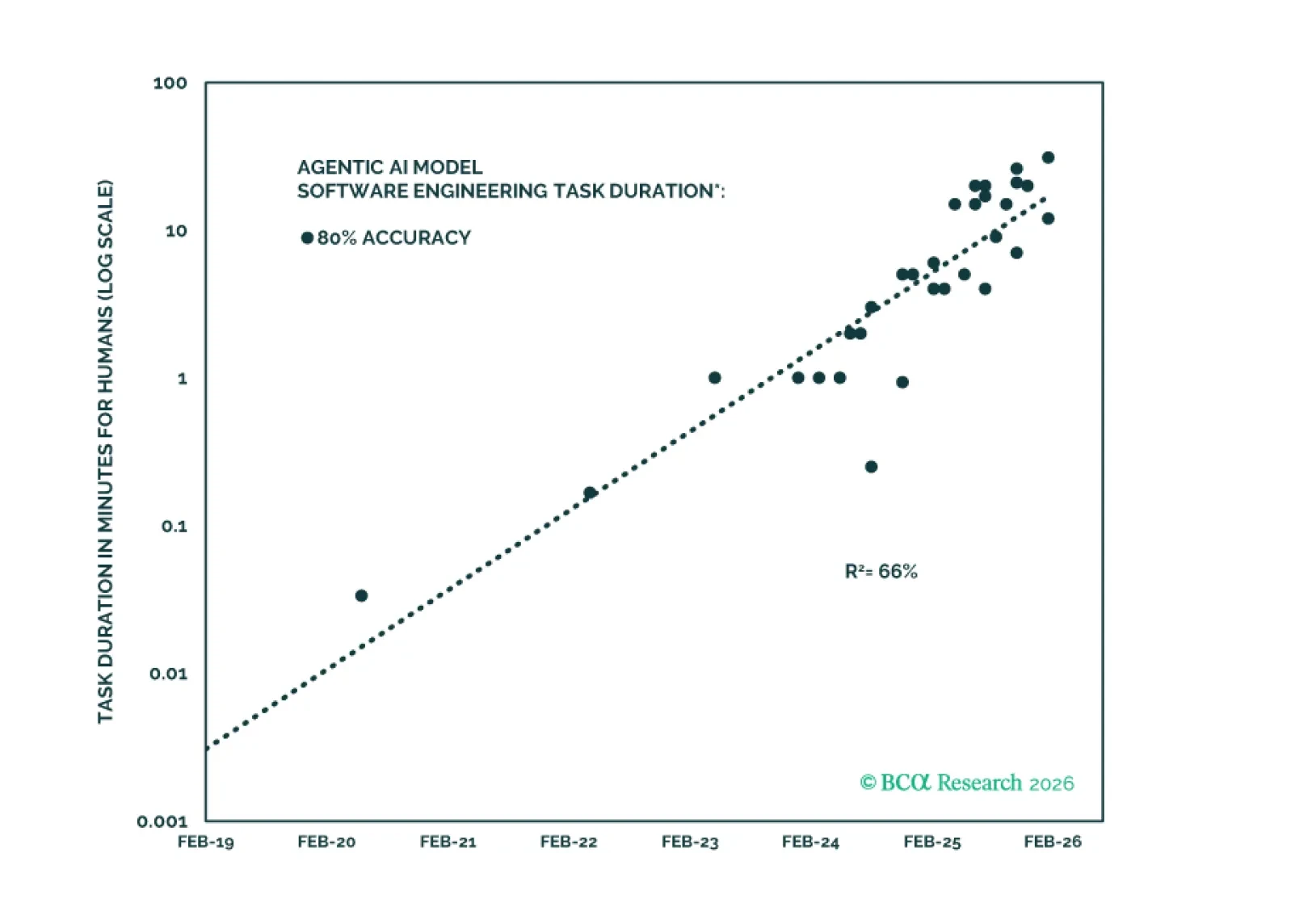

In Section II, Jonathan examines whether the AI “scaling laws” are likely to hold. They will over the near term, but cracks are already beginning to form in the narrative of ever-improving AI.

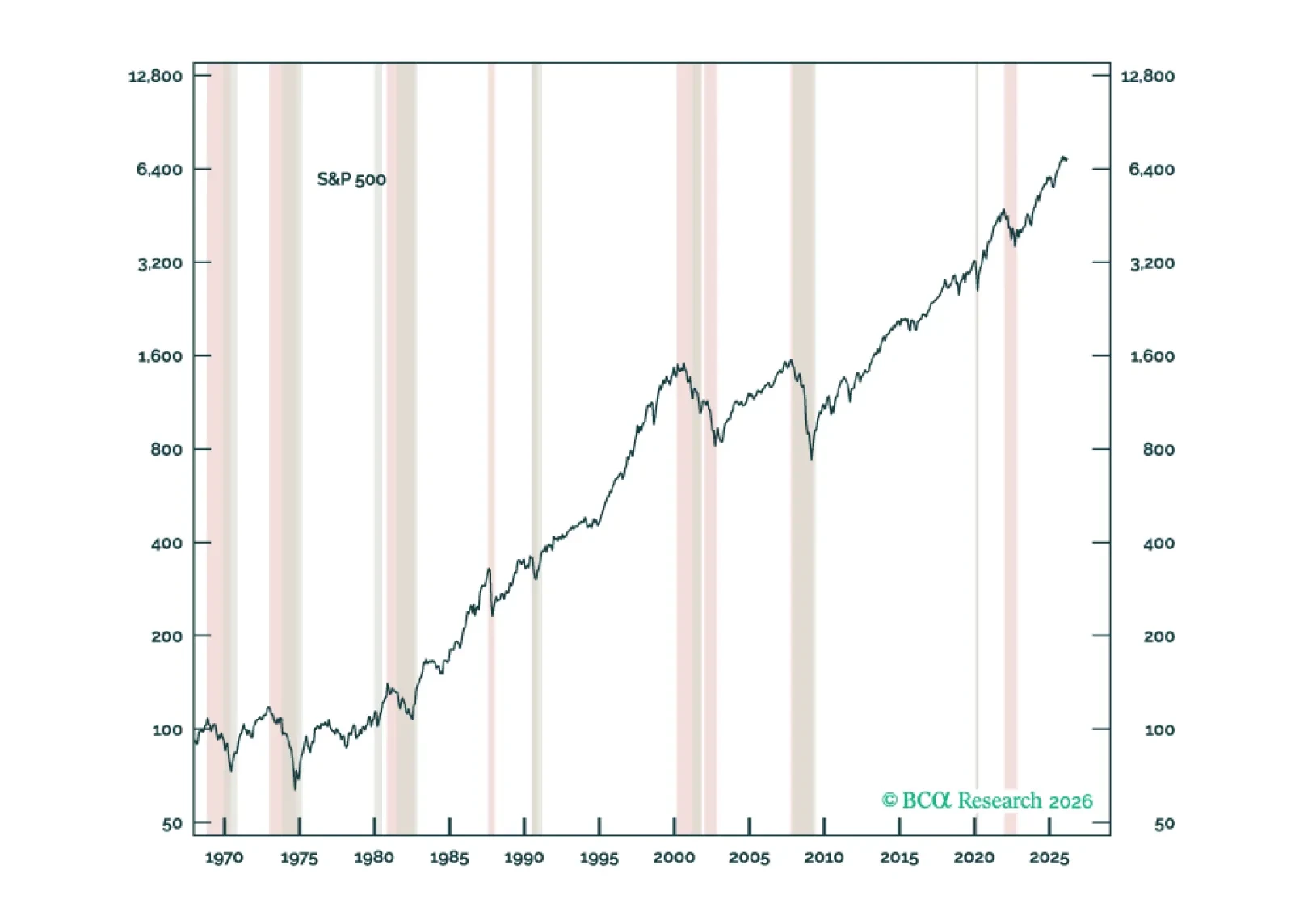

Recent economic data have been reasonably firm. We will cut our 12-month US recession probability to 40% from 50% if the Supreme Court strikes down President Trump’s tariffs. This would take our scenario-weighted year-end 2026 price target for the S&P 500 to 6375 from 6200.

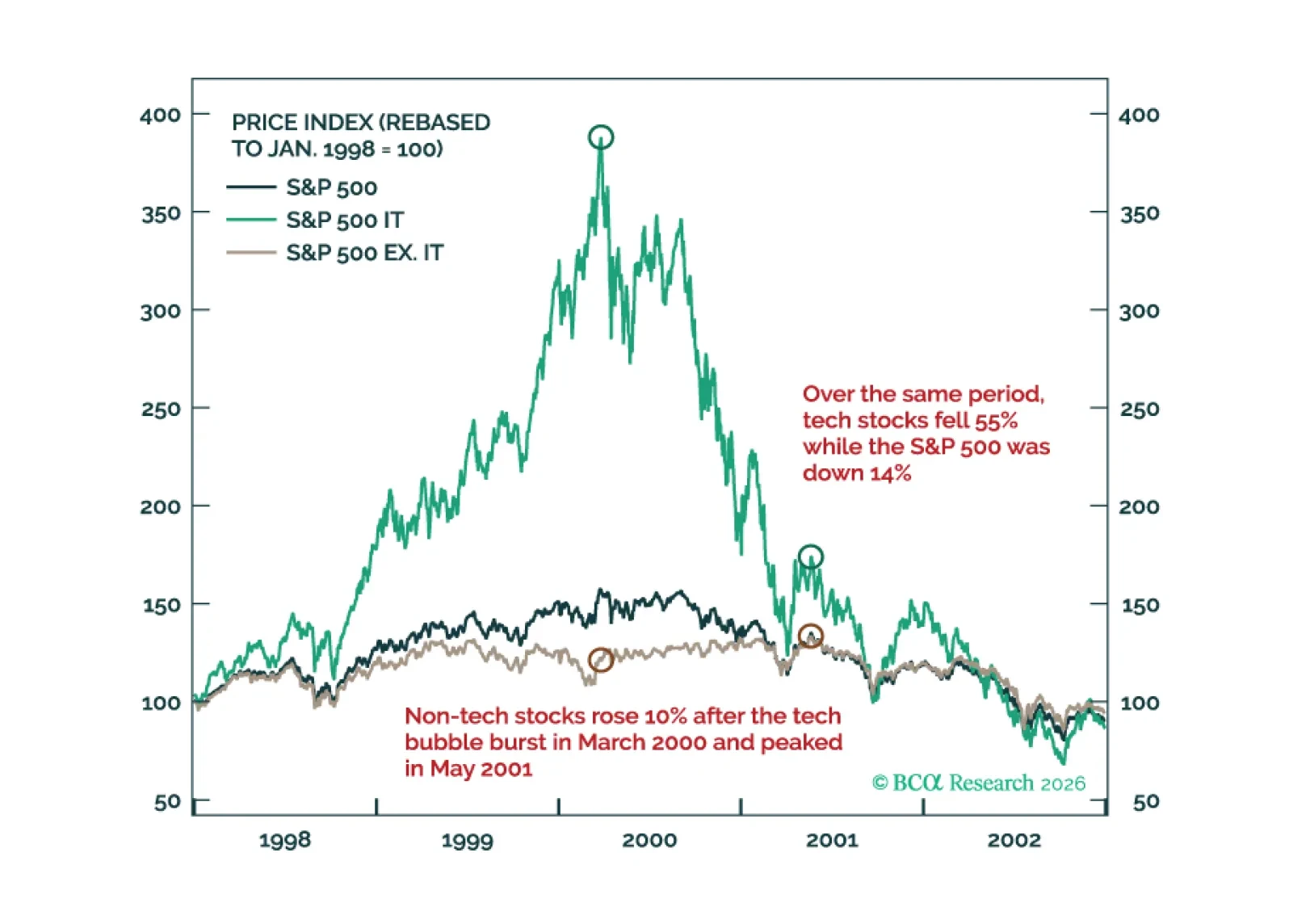

Much like the 2000 episode, we expect this year to unfold in two stages: A “Great Rotation” from tech stocks to non-tech names in the first half of 2026 followed by a broad-based selloff in stocks in the second half on the back of a weakening US economy.

We have been surprised that consumption has held up well despite anemic payrolls growth. This brief considers ways that consumption might continue to beat our base-case expectations.

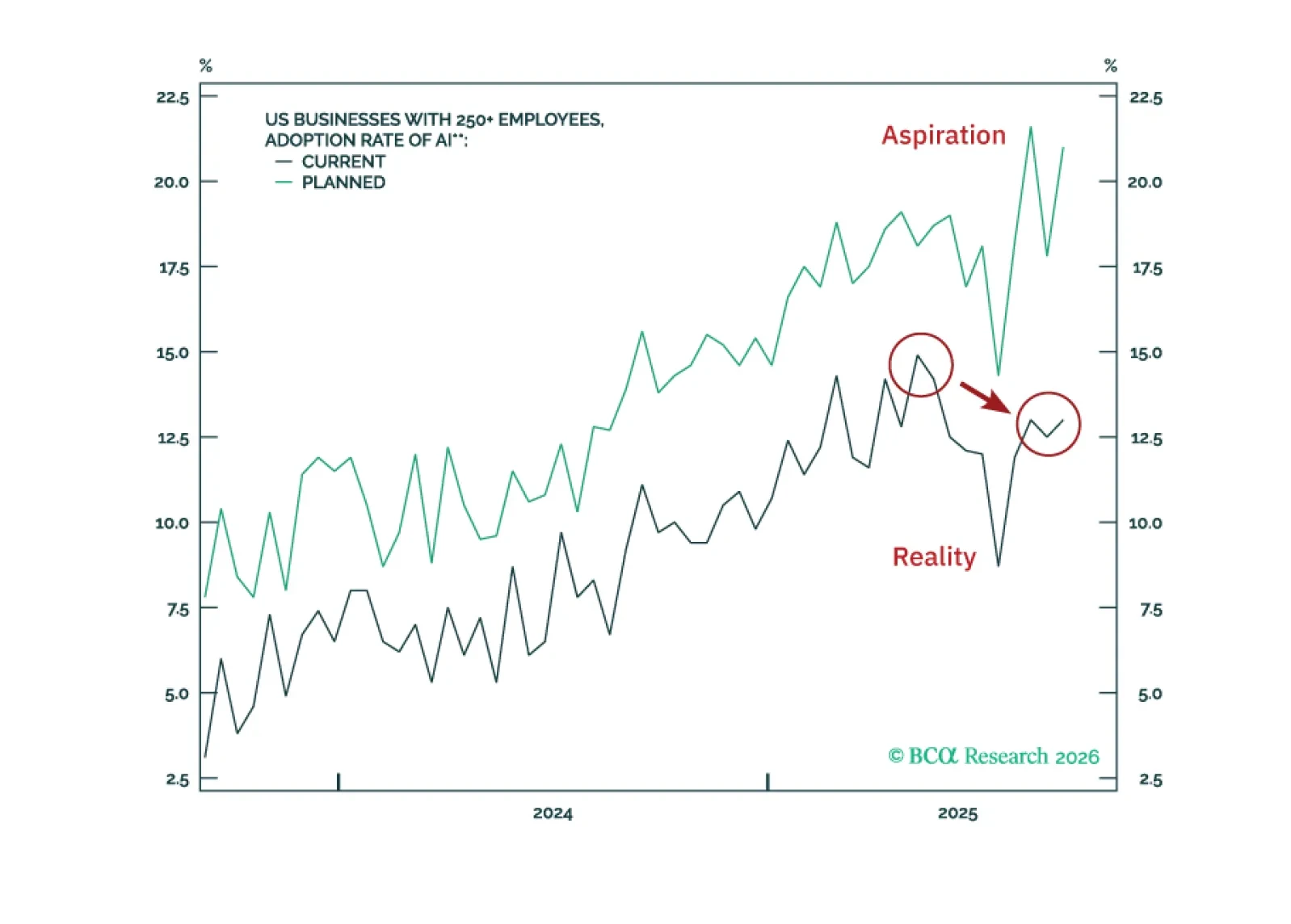

In Section II, Jonathan updates the BCA Artificial Intelligence Productivity Checklist and concludes that the evidence of an AI-driven productivity boom is not convincing.

In Section I, Doug underscores that the US labor market remains weak, crimping the outlook for disposable income growth. It is too soon to decisively bet against the bull market, but downside risks remain quite elevated. In Section II, Jonathan updates the BCA Artificial Intelligence Productivity Checklist and concludes that the evidence of an AI-driven productivity boom is not convincing.