Consumer

Chinese retail sales grew 3.7% y/y in May, from 2.3% in April, upending expectations of a more muted 3.0% increase. The government appliance trade-in program has likely boosted these figures. Sales of home-related goods such as communication appliances,…

Housing is the most interest-rate-sensitive sector of the economy. Yet, the very aggressive monetary tightening cycle has only had a muted effect on home prices. While recent housing market data have been mixed, prices have not tumbled. Indeed, a tight…

Declines in Chinese new and used home prices accelerated in May to 0.71% m/m and 1.00% m/m respectively, and the contraction in residential investment deepened to 10.1% YTD y/y. These figures come on the heels of relaxed purchase and mortgage rules, as well…

In this insight, we update our thinking on the recent BoJ move in terms of positioning for the yen and JGB yields.

Chinese new loans grew from CNY 10.2 tr to CNY 11.1tr in May, disappointing expectations of CNY 11.3tr. Year-to-date aggregate financing also came short of anticipations, growing from CNY 12.7tr to CNY 14.8tr. Notably, the contraction in M1 worsened from 1.4%…

The BoE had to deal with a stagflationary headache in the second half of 2023. Inflation was stickier and growth was weaker in the UK than in many of its DM peers. This trend turned around earlier this year with a late-cycle growth reacceleration. The UK…

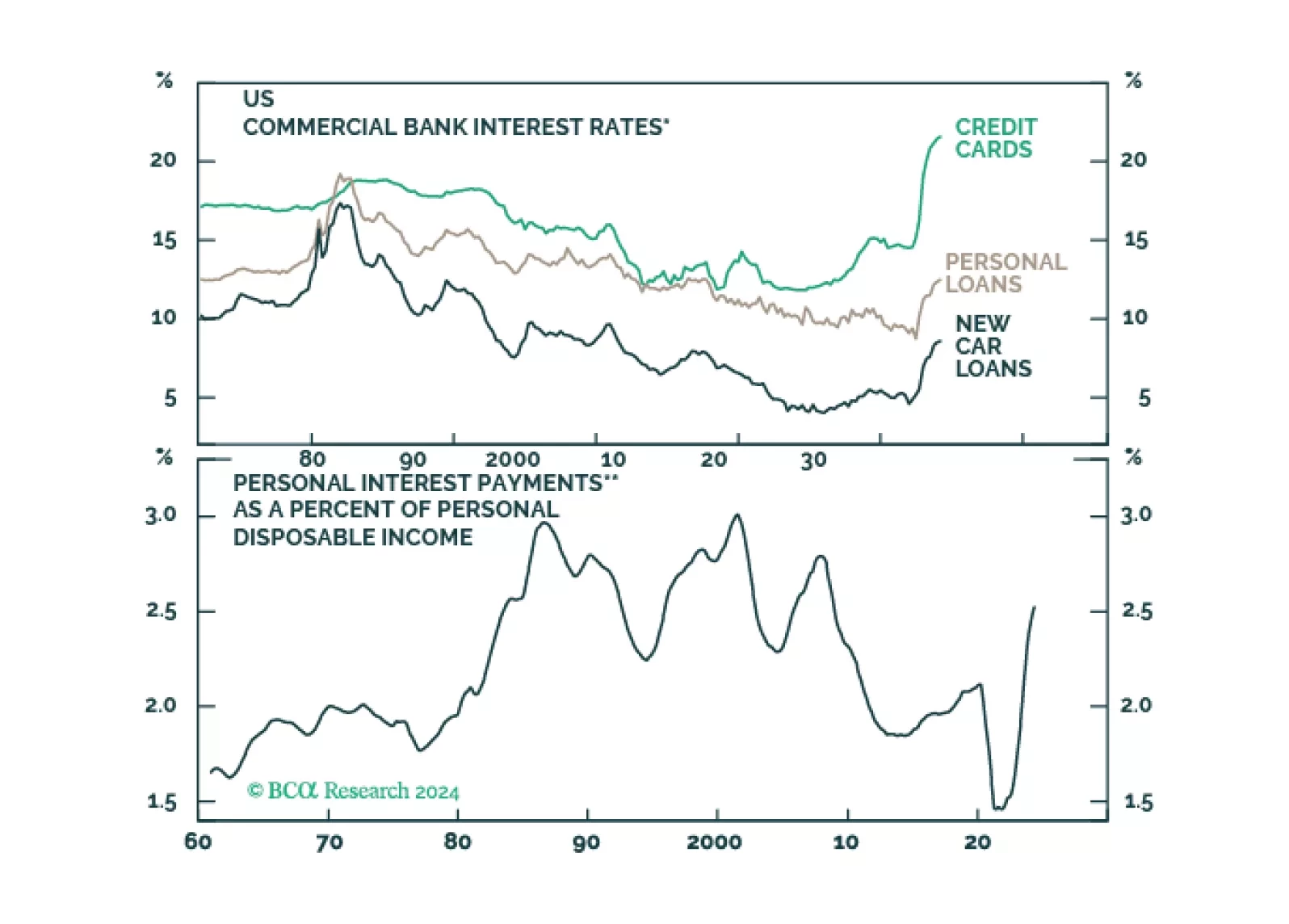

The preliminary University of Michigan gauge of consumer sentiment unexpectedly dropped in June to 65.6 from 69.1, against expectations of improving morale. Consumers’ assessments of current conditions declined by a larger margin than expectations for the…

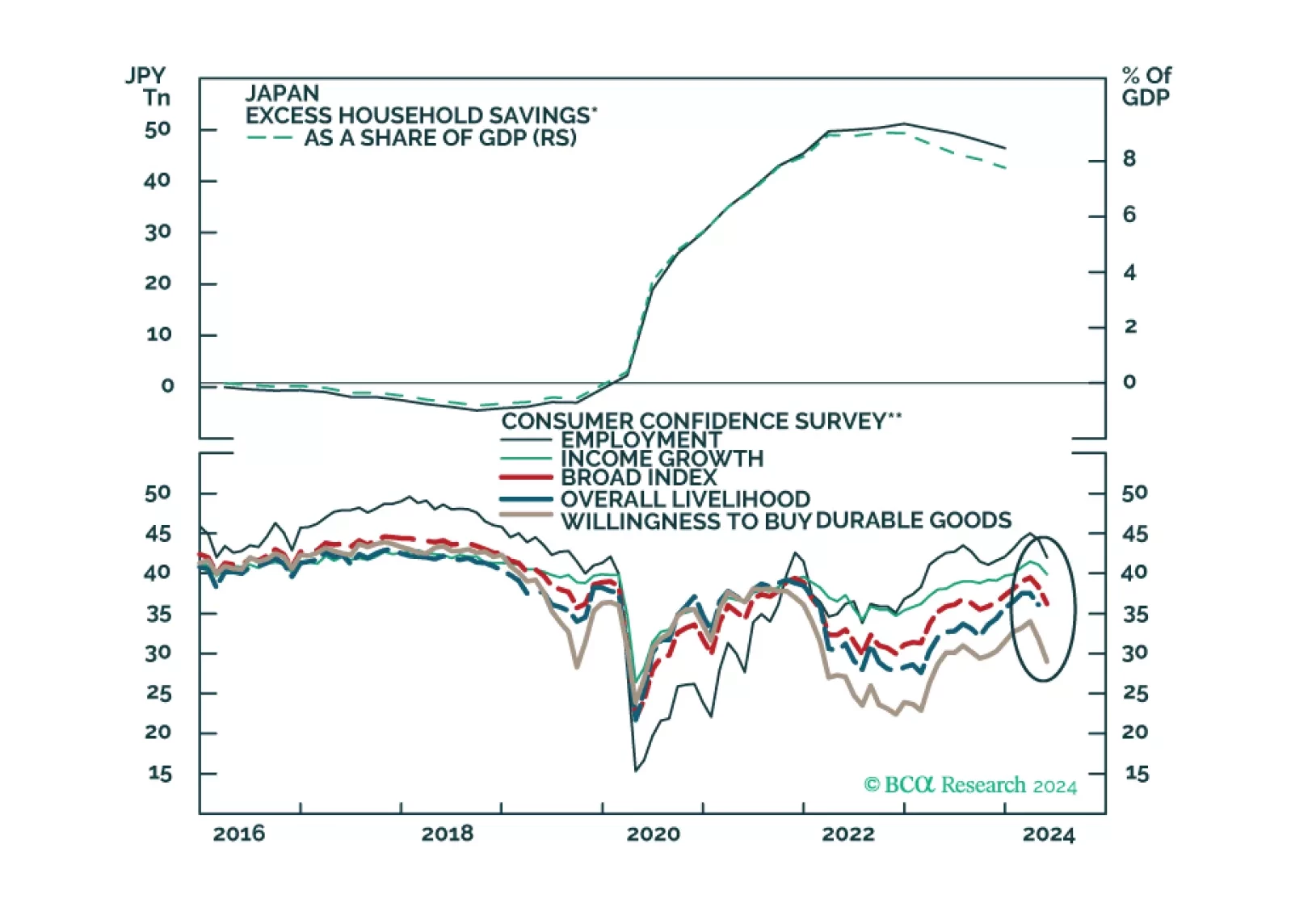

According to BCA Research’s Global Investment Strategy service, aggressive fiscal stimulus and labor market flexibility contributed to the relative strength of the US consumer. However, adverse region-specific effects also played a role. Most notably, the…

Global consumer spending is likely to slow over the coming quarters, culminating in a major economic downturn in late 2024 or early 2025. Investors should maintain benchmark exposure to equities for now but look to turn more defensive by the end of this summer.

The Eurozone Sentix Economic index improved from -3.6 to 0.3 in June, easily surpassing expectations of a more muted improvement to -1.7. Notably, the Expectation and Current Situation subindices rose to 28-month and 13-month highs of 10 and -9, respectively.…