Consumer

Emergency pandemic policies elongated the lag between Fed rate hikes and an observable slowdown in the economy. Notably, fiscal transfers and constrained consumption options endowed households with more than $2 trillion of savings they would not otherwise…

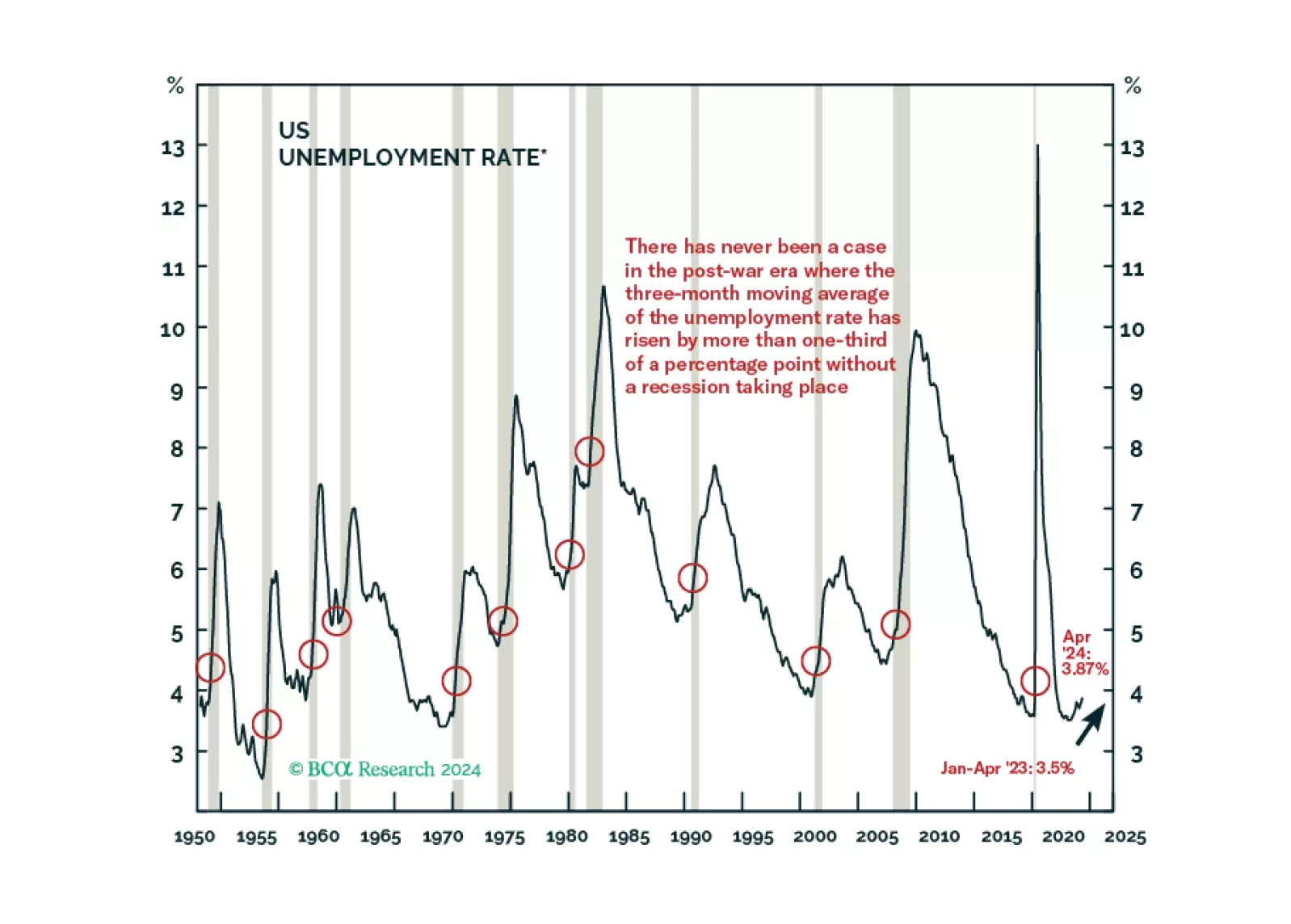

We marked the first X on our Equity Downgrade Checklist and the latest JOLTS, Employment Situation and SLOOS releases brought us closer to ticking some others. We remain tactically neutral on equities but expect that we will underweight them as excess savings are further depleted, leading labor market indicators continue to soften and consumer credit performance continues to fray.

In a widely expected move, the Bank of England (BoE) maintained its policy rate at 5.25% in May. Nevertheless, two Committee Members voted in favor of cutting rates, one more than was anticipated. The tone of the report was overall dovish. The BoE…

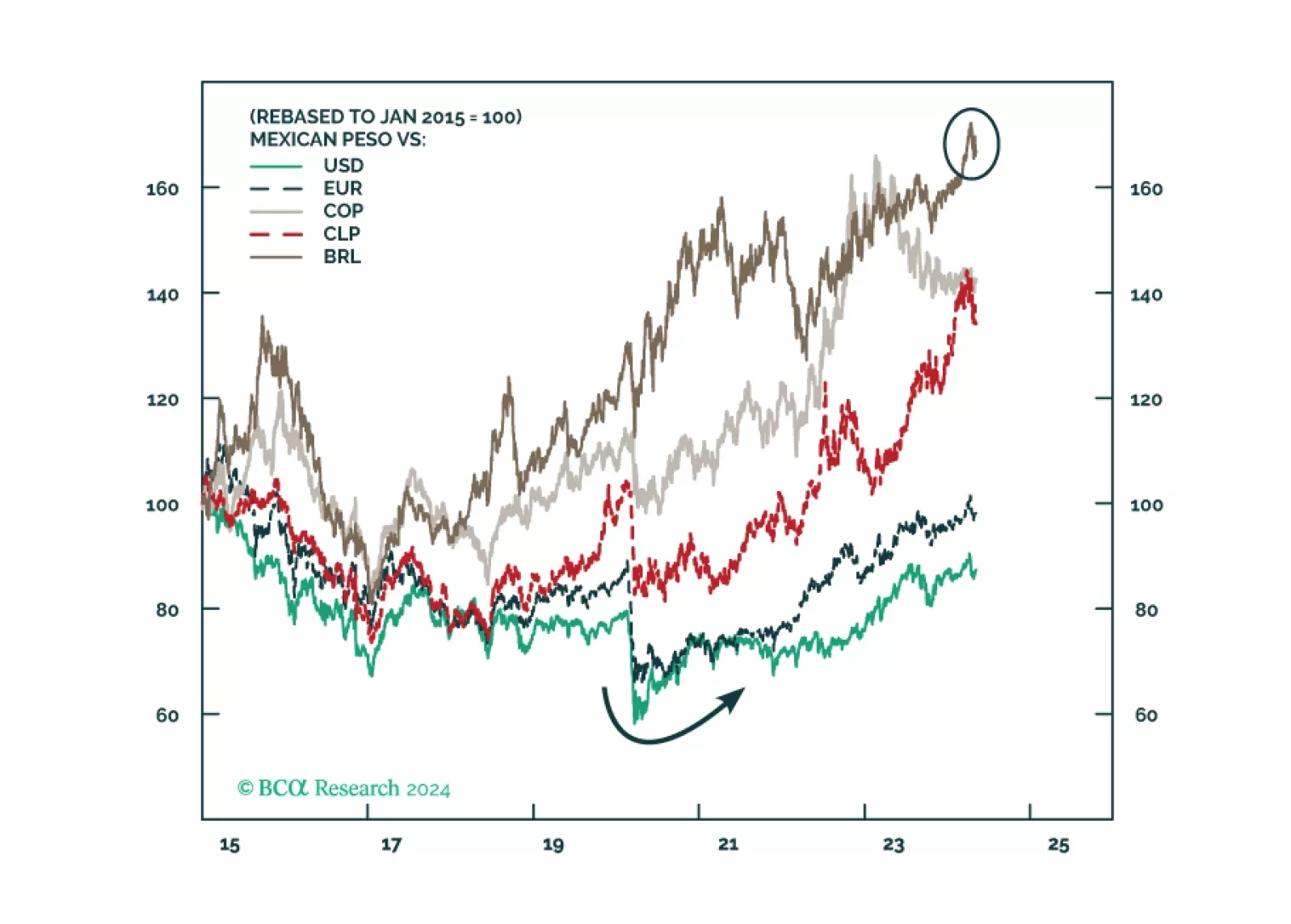

Mexico’s election and the US election pose short-term and potentially medium-term risks to Mexican financial assets. But unless the ruling party wins a double supermajority, we remain structurally overweight Mexico relative to global stocks excluding the United States.

European retail sales were stronger-than-expected in March. They grew by 0.7% y/y from an upwardly revised 0.5% contraction in February, upending expectations that they would continue to decline. Improved sales in food products were the main drivers,…

Lending standards continued to tighten for most loan categories in Q1 2024. US banks reported tightening lending standards for C&I and CRE. For real-estate-backed loans to households, lending standards tightened further for Home Equity Line of Credits…

According to BCA Research’s US Bond Strategy service, while US economic data clearly show that labor demand has slowed from its peak two years ago, it isn’t yet clear whether this slowing represents a re-normalization to pre-pandemic levels or the start of a…

The Caixin services and composite PMIs were broadly unchanged in April. The services PMI decreased from 52.7 to 52.5, in line with expectations, while the composite PMI increased from 52.7 to 52.8. Details underscored positive dynamics. New business growth…

The Federal Reserve has a target inflation of 2%. But what level of inflation does the American public actually prefer? A recent NBER paper titled “Inflation Preferences” by Afrouzi, Dietrich, Myrseth, Priftis, and Schoenle surveyed one thousand…

The ISM Services PMI largely disappointed in April. The headline index fell to 49.4 from 51.4, below expectations of a faster pace of growth. April’s contraction ends a streak of 15 consecutive months of services-sector expansion. Two alternative…