Consumer

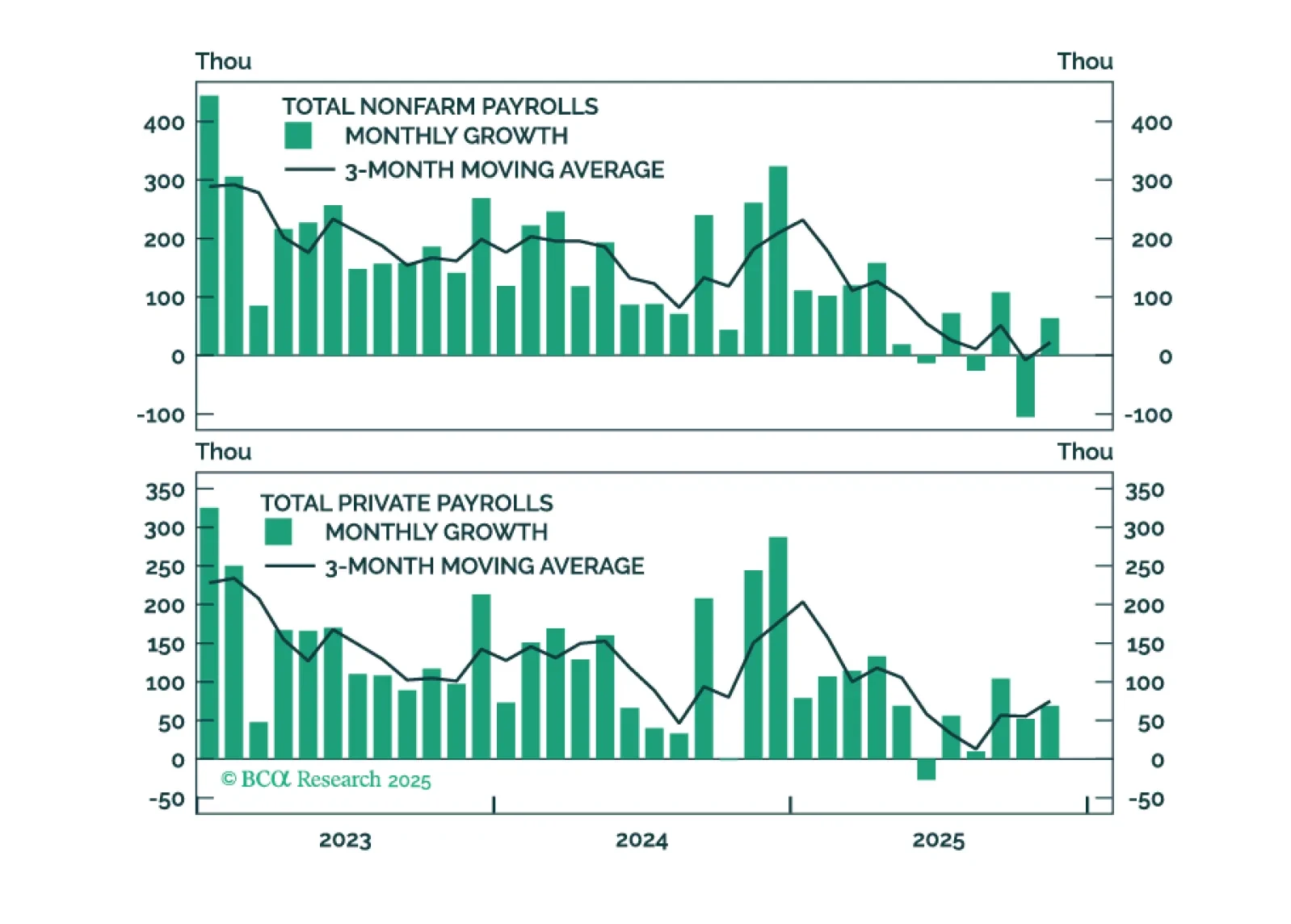

Employment Data Point To Dovish Policy Surprises In 2026

Weak, narrowly concentrated job growth in fields that pay poorly bodes ill for the economy, but we enter 2026 recommending benchmark allocations because we are wary of the potential for an AI-driven meltup. Investors should bide their time before turning defensive.

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.

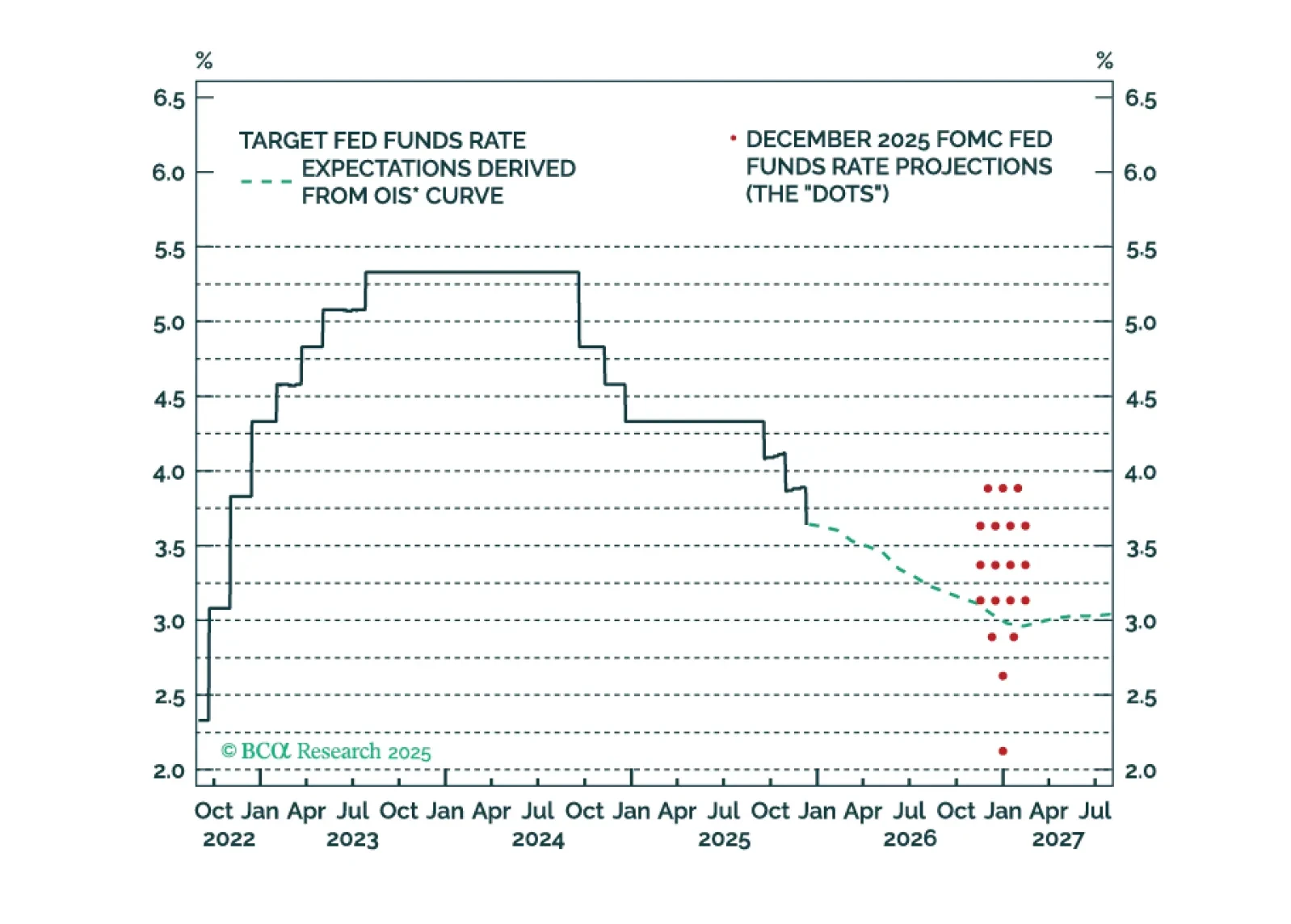

The Fed is on hold for now, but its 2026 economic projections are far too optimistic. The Fed will ease more next year than it currently anticipates.

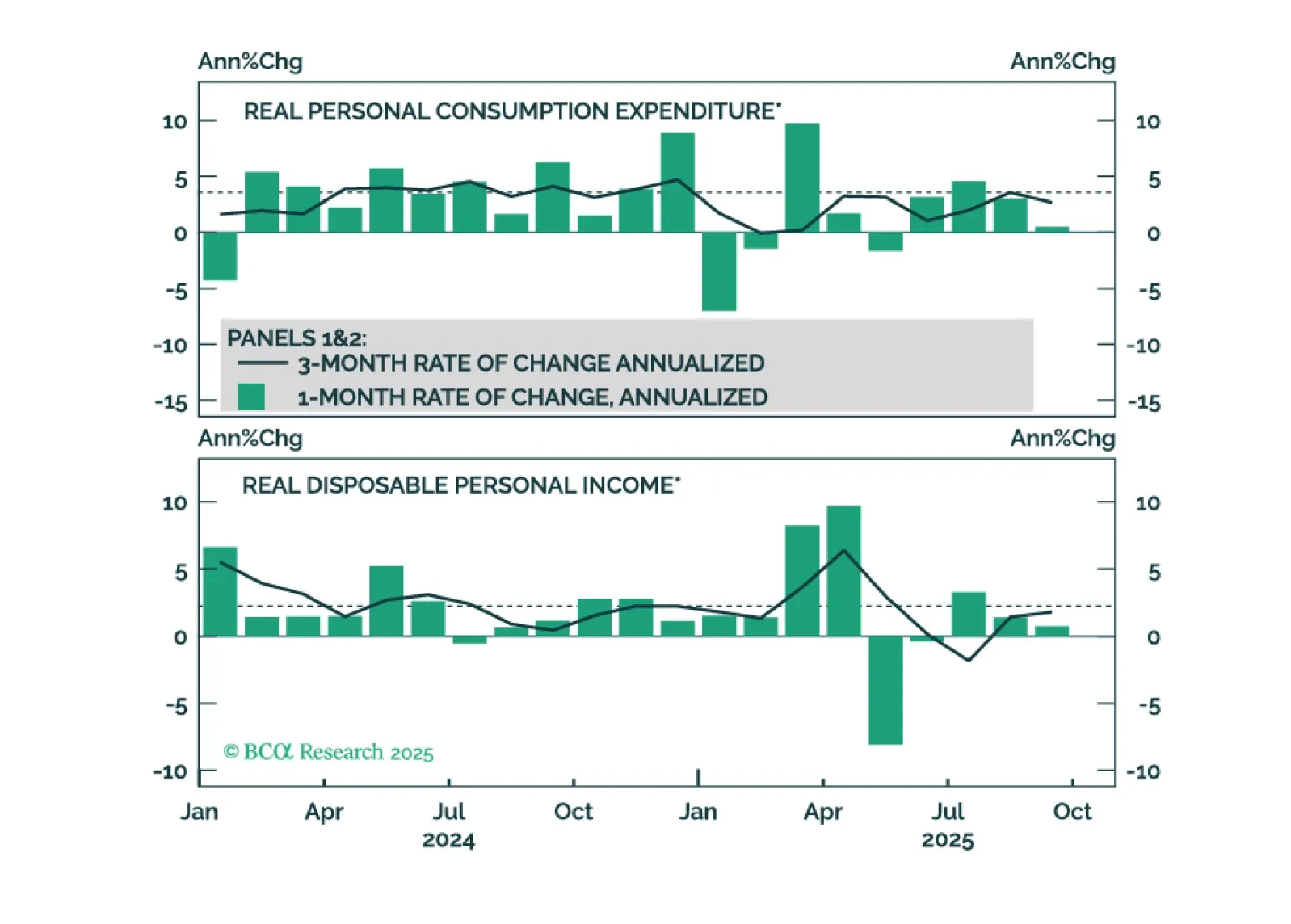

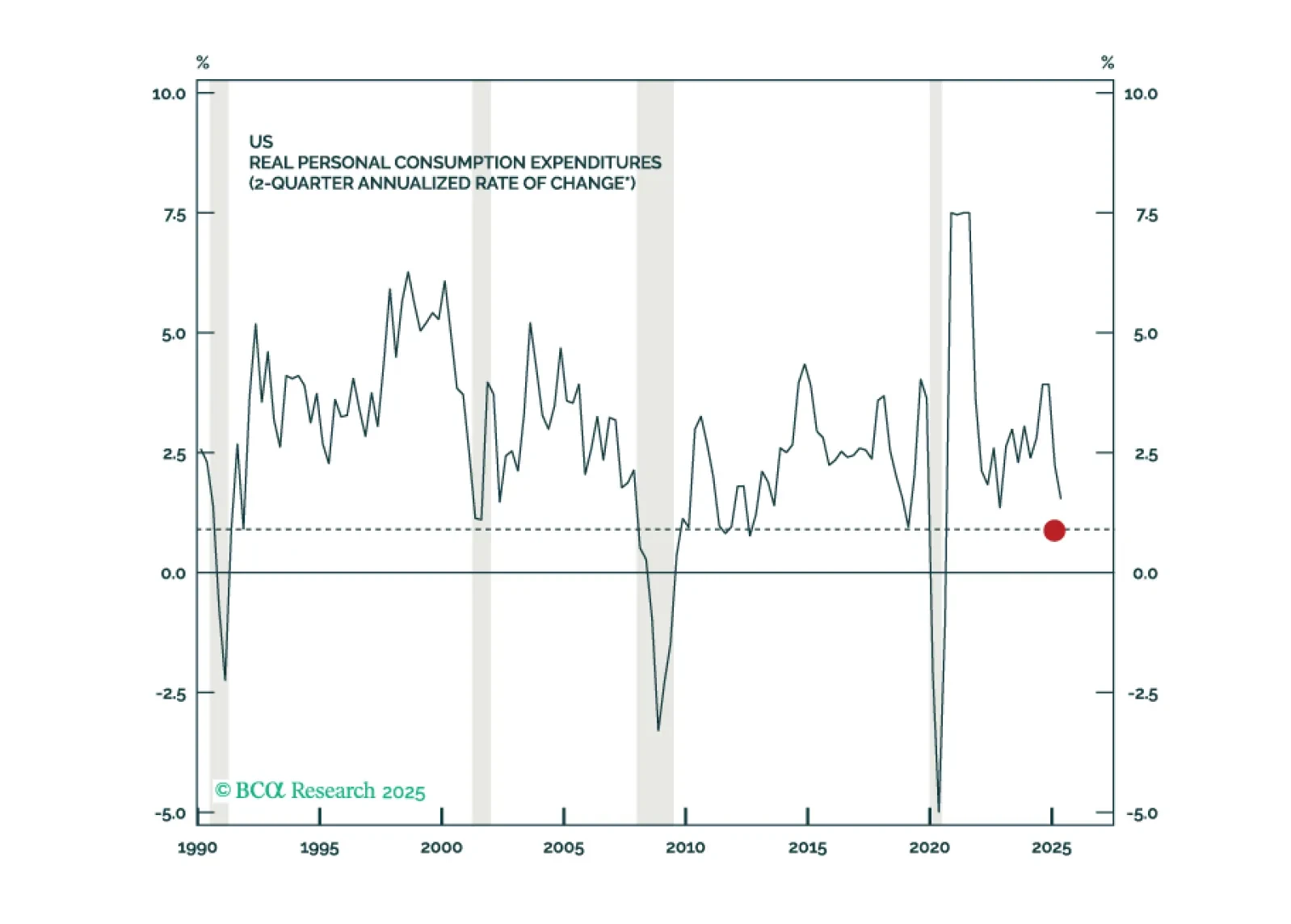

September’s weak consumer spending data challenge the K-shaped recovery narrative and suggest that spending will slow to match already-weak employment growth.

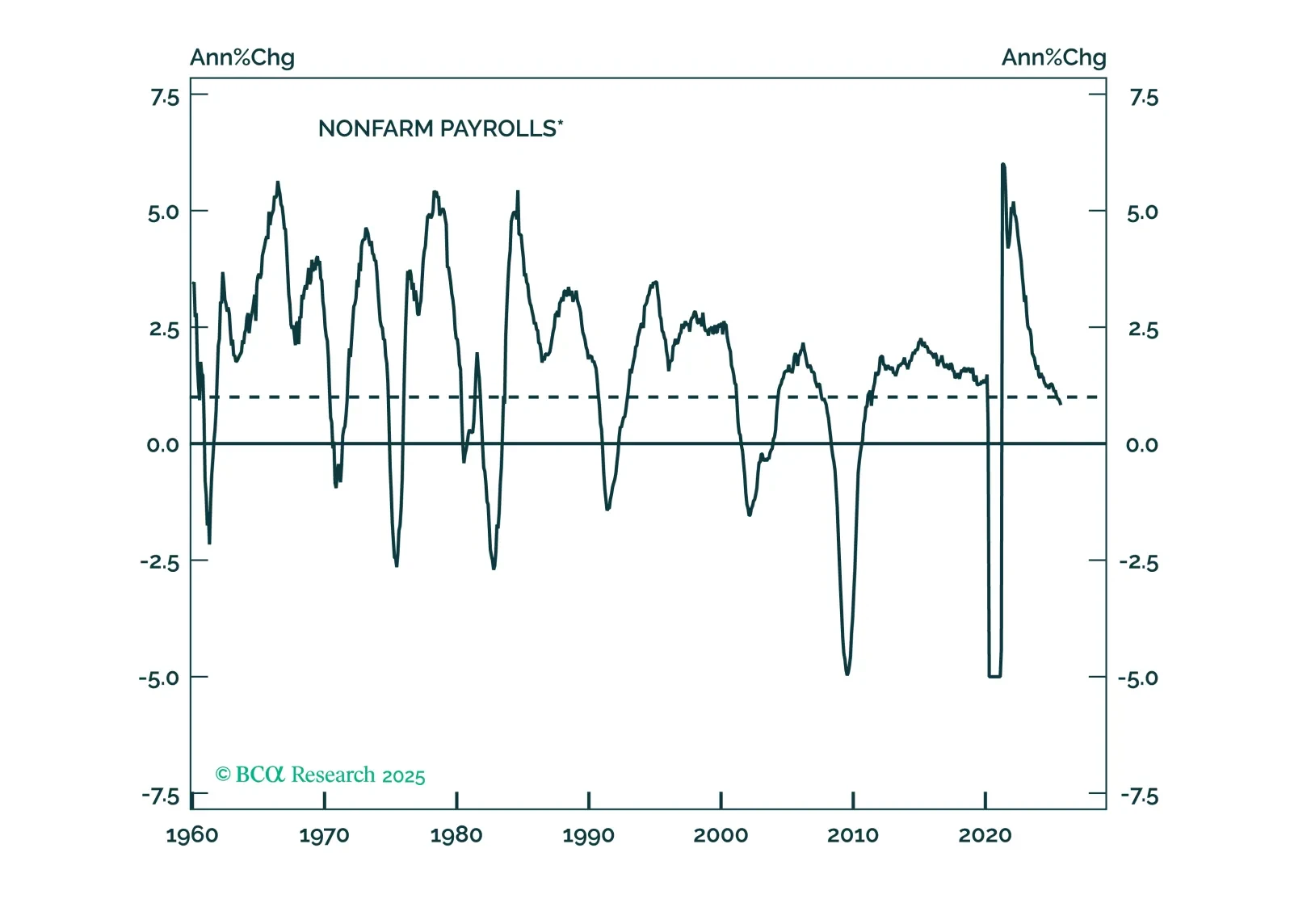

September job gains topped modest expectations, but year-over-year payrolls growth appears to have fallen below stall speed. We remain concerned about US activity.

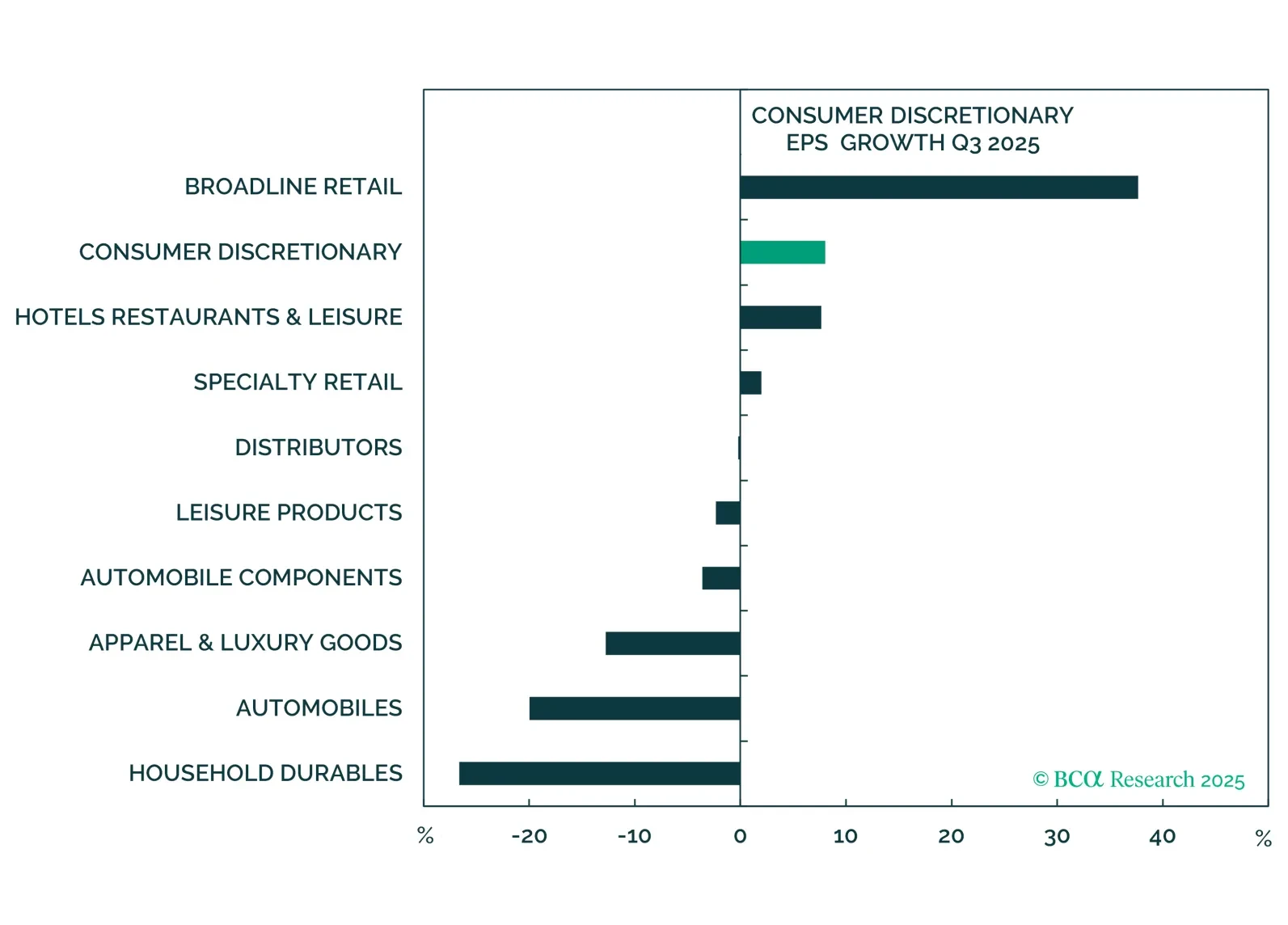

Q3 results were strong but failed to impress investors, and Q4 will likely prove more challenging. Beneath the surface, earnings diverged sharply: Firms catering to affluent consumers maintained solid momentum, while those reliant on the mass market lagged. We remain equal weight Consumer Services and underweight Consumer Staples.

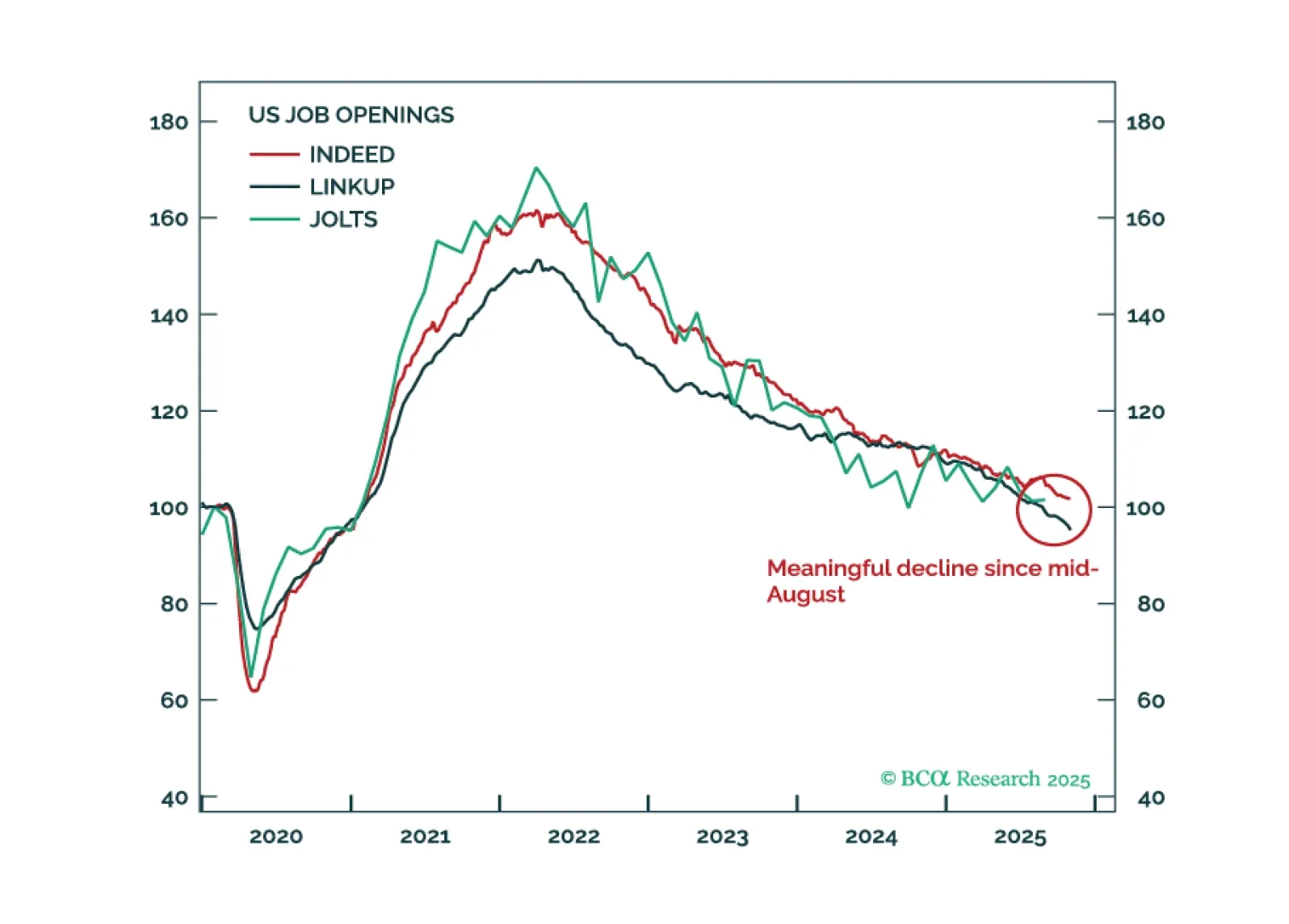

In the absence of official government data, investors are turning to alternative sources to gauge the direction of the US economy. Our analysis of this data suggests that the economy has continued to expand at a moderate pace over the past two months. If the Supreme Court were to strike down the tariffs, this would reduce the near-term odds of a recession while raising the odds of overheating.

In Section I, Doug explains how the sharp upward revision to second-quarter consumption in the final GDP estimate has reduced our recession conviction and could lead us to abandon our recession call altogether. The situation is fluid, though, as typified by the striking weakness of stocks in consumer-facing and cyclically exposed subindustries. In Section II, Doug and Global Investment Strategy’s Miroslav Aradski consider the implications of the AI investment boom.