Consumer

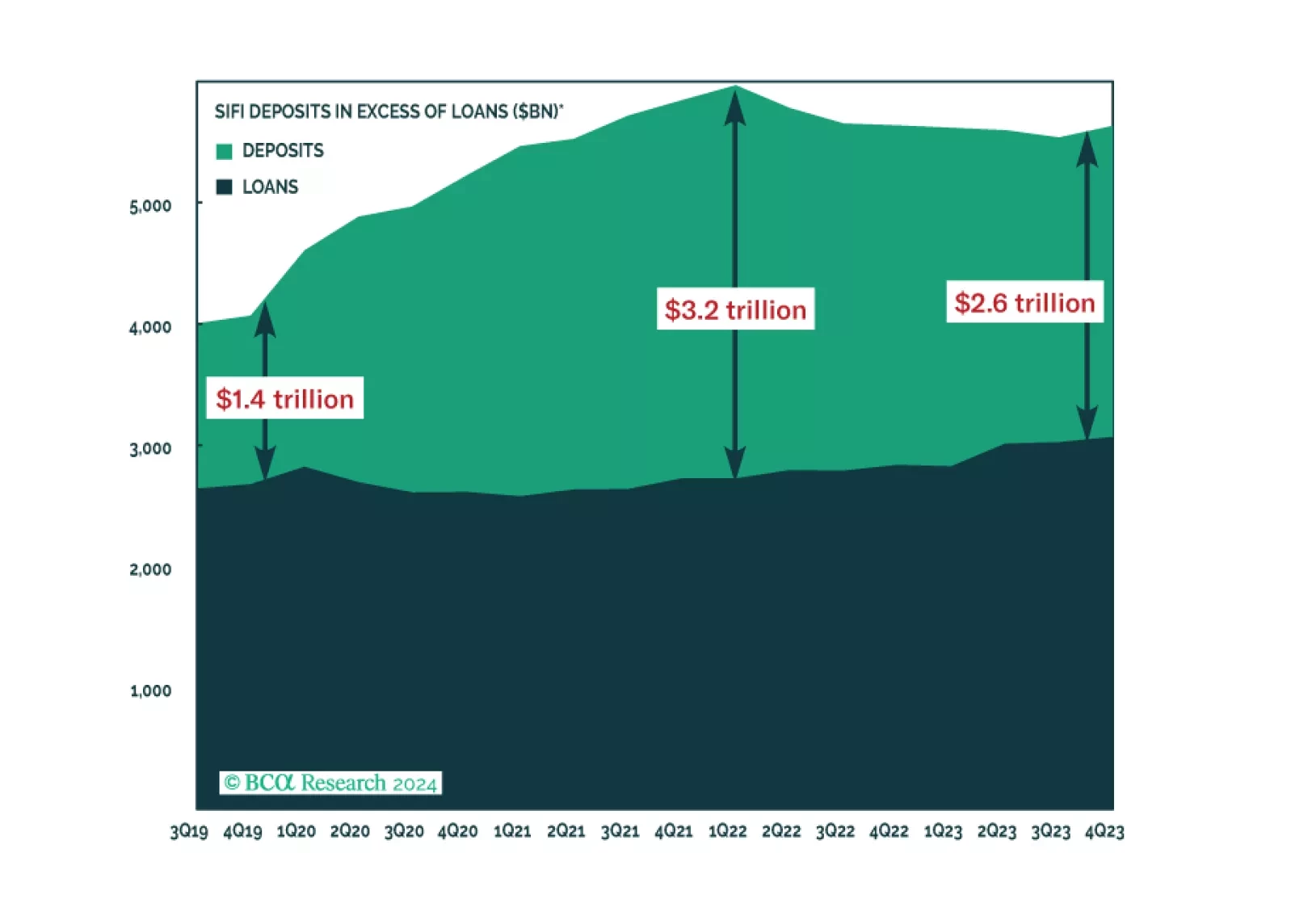

The SIFI banks expressed confidence in their credit outlook for 2024 and expect that credit losses will crest soon, given the reserves they’ve already set aside. Their implicit embrace of the soft-landing narrative suggests to us that the consensus is getting closer to being set up for disappointment. We remain tactically equal weight equities and fixed income but think conditions may soon favor turning defensive.

The preliminary release of the University of Michigan’s Survey of Consumers delivered a positive surprise on Friday. The headline index jumped from 69.7 to a 30-month high of 78.8, beating expectations of a slight increase to 70.1. The current conditions and…

After having traded sideways for the past month, US equities ended the week on a high note with the S&P 500 closing at fresh record high on Friday. Last year’s winners are once again driving the rally. Information Technology, Communication Services, and…

An update to our outlooks for the Fed’s interest rate and balance sheet policies following this week’s remarks from Fed Governor Waller.

According to BCA Research’s Emerging Markets Strategy service, Indian stocks, which benefitted immensely from foreign portfolio inflows and are now very expensive, remain vulnerable to any global risk-off sentiment. The new year marked a new high for…

The Fed’s latest Beige Book delivered a lukewarm message on the US economy. Growth, employment, and prices were all relatively stable since the previous release in late-November. Eight districts reported little or no change in activity, three districts…

Recent data suggest that the US housing market is resilient. In particular, a strong rebound in homebuilder sentiment is sending a positive signal. The NAHB Housing Market Index jumped from 37 to 44 in January – handily beating expectations of 39 on the back…

The 1mm b/d surge in US crude oil production last year was the result of a flood of low-cost drilled-but-uncompleted (DUCs) shale-oil wells coming online, mostly in 2H23 in the Permian Basin, which our colleagues in BCA's Commodity & Energy Strategy…

The US retail sales release delivered a positive signal about the US economy in December. The 0.6% m/m increase in overall retail sales beat expectations of a more muted acceleration from 0.3% m/m to 0.4% m/m. Importantly, the improvement was broad-based with…

Chinese data continues to send a pessimistic signal for domestic risk assets and China plays. Although at 5.2% in Q4, GDP growth stands above the official target, it underwhelmed anticipations of 5.3%. Moreover, other data releases reveal that the economy…