Consumer

Canadian government bond yields jumped on Tuesday, with the 10-year yield rising by nearly 14 basis points. While most other major DM government bonds also sold off, the move in Canadian yields was relatively more pronounced. Both global and domestic forces…

Results of the ZEW survey sent a slightly positive signal on German investor sentiment. The economic expectations indicator rose to an 11-month high in January – beating consensus estimates of a decline. This increased optimism about the outlook reflects an…

China’s central bank unexpectedly held the medium-term policy rate unchanged at 2.5% on Monday, surprising expectations of a 10 basis point cut. Given that deflationary forces dominate China’s economy, the decision to stand pat underscores that policymakers…

On the surface, domestic economic data painted a mixed picture of conditions in China at the end of 2023. On the positive side, the December trade data beat expectations. The dollar value of Chinese imports expanded by 0.2% y/y, surprising anticipations…

The market’s pricing of a soft landing means that geopolitical risks are becoming more, not less, relevant in 2024. US domestic divisions will invite challenges as foreign powers rightly fear that US policy will turn more hawkish after the election.

Optimism among investors and economic agents continues to improve in the Eurozone. The Sentix Economic Index for the Eurozone rose from -16.8 to -15.8 in January – in line with consensus expectations and marking the third consecutive increase. The current…

Growth in US disposable income has outpaced inflation nearly every month since mid-2022. Consumption is principally driven by income, but in the US it has gotten a meaningful assist the last two years from the drawdown of excess savings accumulated over the…

According to BCA Research’s China Investment Strategy service, the structural landscape of China's property market today is, in many aspects, more challenging than the real estate markets in Japan and the US at the peak of their housing bubbles: The…

Despite the blah opening to the year, we do not think stocks have reached an inflection point. We expect that incoming data will continue to flatter the soft-landing narrative for another couple of months, helping the S&P 500 to establish a new all-time high before the rally runs out of steam.

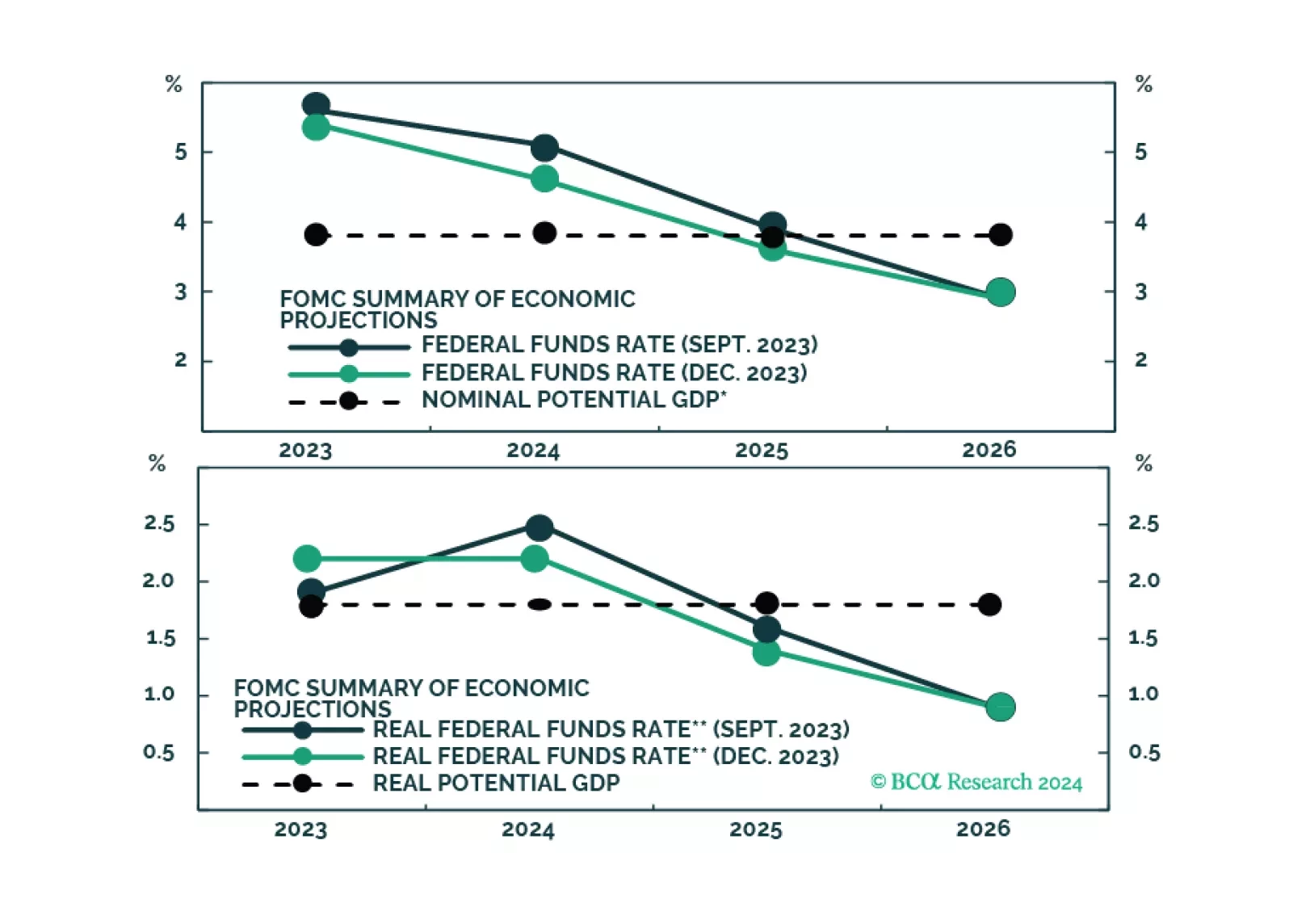

The market is excited by the idea that the Fed will cut rates early this year, even without a recession. But is that likely, with inflation still set to be around 2.8% mid-year?