Demographics

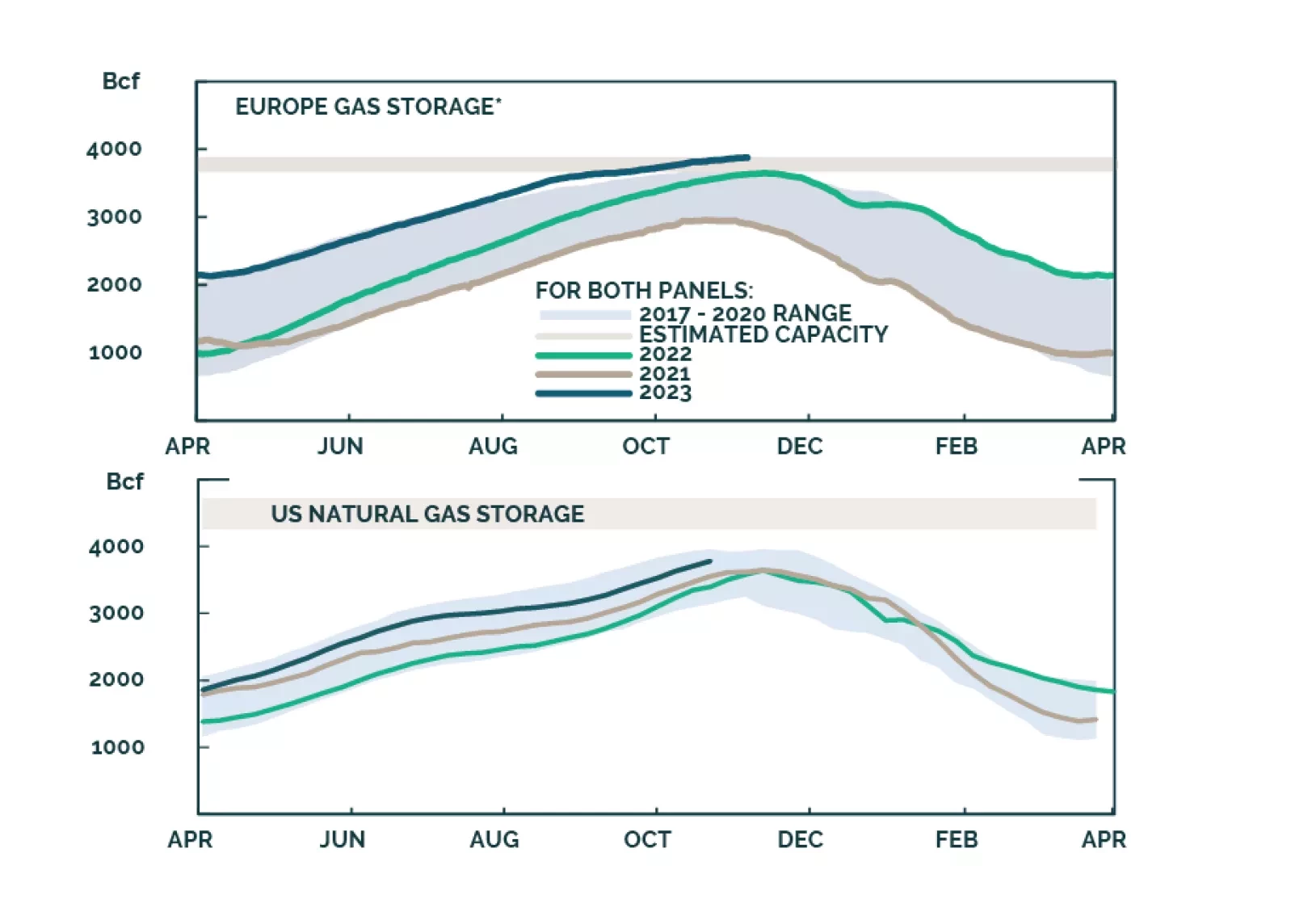

Natural gas storage levels in the US and EU are sufficient to balance flowing supply and demand this winter, assuming normal weather. China continues to invest in domestic production, and to diversify supply sources to compensate for a lack of storage. Longer-term Qatari contracts are giving higher weight to natgas trading hub prices. We remain long the XOP ETF to retain exposure to fossil-fuel producers supplying DM and EM economies with natgas beyond the 2050 net-zero-emissions goals advanced by the IEA.

We unveil the ‘Joshi rule’ real-time recession indicator as a much better version of the Federal Reserve’s own ‘Sahm rule’. And we identify what would trigger these recession indicators in this week’s and future US jobs reports. Plus: airlines, soybeans, and tin are all good rebound candidates based on their collapsed short-term complexities.

The ECB is done lifting interest rate for the cycle and its next move will be a cut next year. Yet, European rates will climb even higher in the second half of the decade.

In Part 2 of this series, we prescribe the treatment needed to produce a recovery for the ailing Chinese economy. Authorities will only panic and unleash “irrigation-style” stimulus if the unemployment rate rises sharply, or a financial crisis unravels in onshore markets. This is not yet the case.

A global portfolio is likely to return only 5.3% a year over the next decade, compared to 6.7% in the past. Investors either need to lower their return expectations, or take more risk. Our total return methodology remains consistent with previous editions, with changes limited to the Alternatives section.

The Supreme Court is a generator of certainty rather than uncertainty for US markets. In the event of a constitutional crisis, a court intervention will likely reduce volatility.

Collapsed complexity, plus the unwinding of favourable base effects and favourable seasonal adjustments to the inflation and jobs numbers, all pose a danger to the Goldilocks market.

The stratospheric valuation of this year’s AI mania is likely to deflate, just as it did after the Web 1.0 mania of the late 90s. We go through some long-term and short-term investment implications.

The market does not grasp the implied depths of recessions that will be needed to prevent inflation expectations from un-anchoring. Among the major economies, the most vulnerable to a deep recession is the UK. We explain why, and some investment implications. Plus: the yen is a rebound candidate, while Japanese equities are a reversal candidate.

Consumer discretionary shares have led European markets higher this year. While long-term drivers remain positive, can the same be said for the remainder of 2023?