Developed Countries

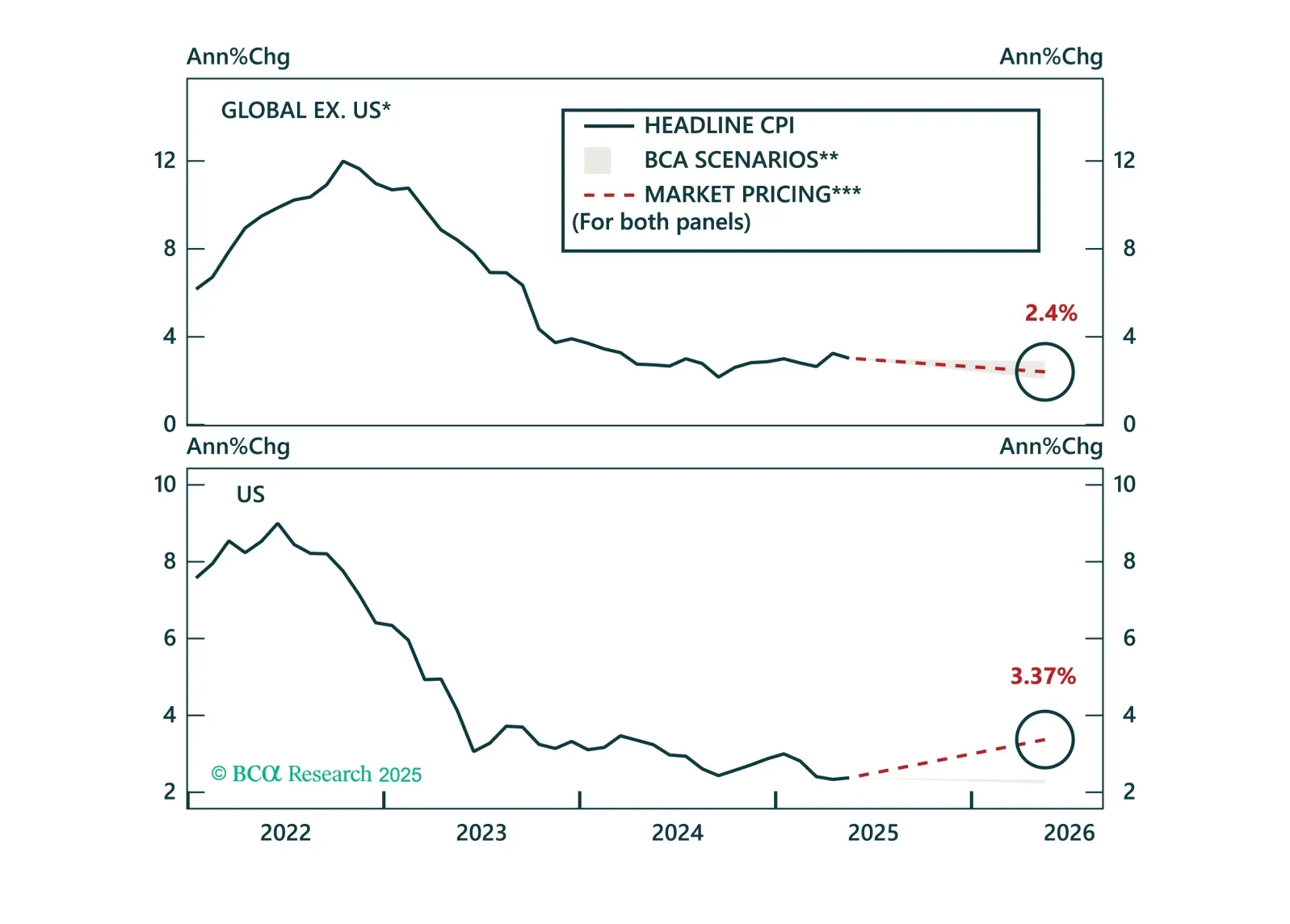

Disinflation continues to unfold globally, and markets are finally catching up. Inflation expectations have broadly realigned with fundamentals, prompting us to shift our global ILB allocation to neutral. While tariff risks are inflating US expectations, pricing in the UK, Japan, and Australia has adjusted sharply. Today’s Strategy Report reviews these developments and updates our country-level ILB positioning.

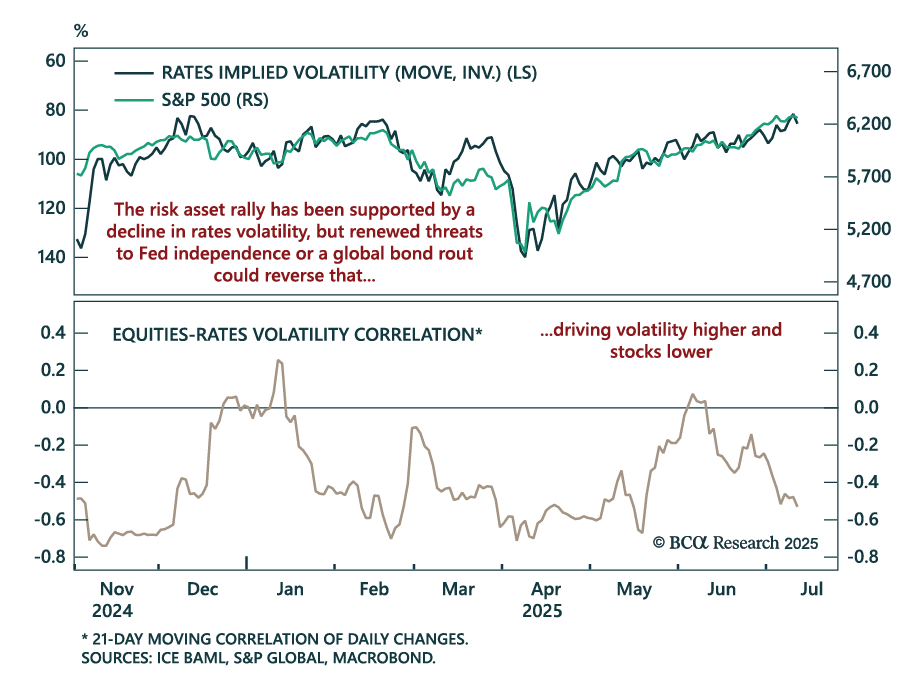

Equities have retraced sharply from Liberation Day lows, but renewed policy risk and mispriced volatility keep us tactically cautious. The Trump administration softened its trade stance as equities neared bear market territory in early April, but has now…

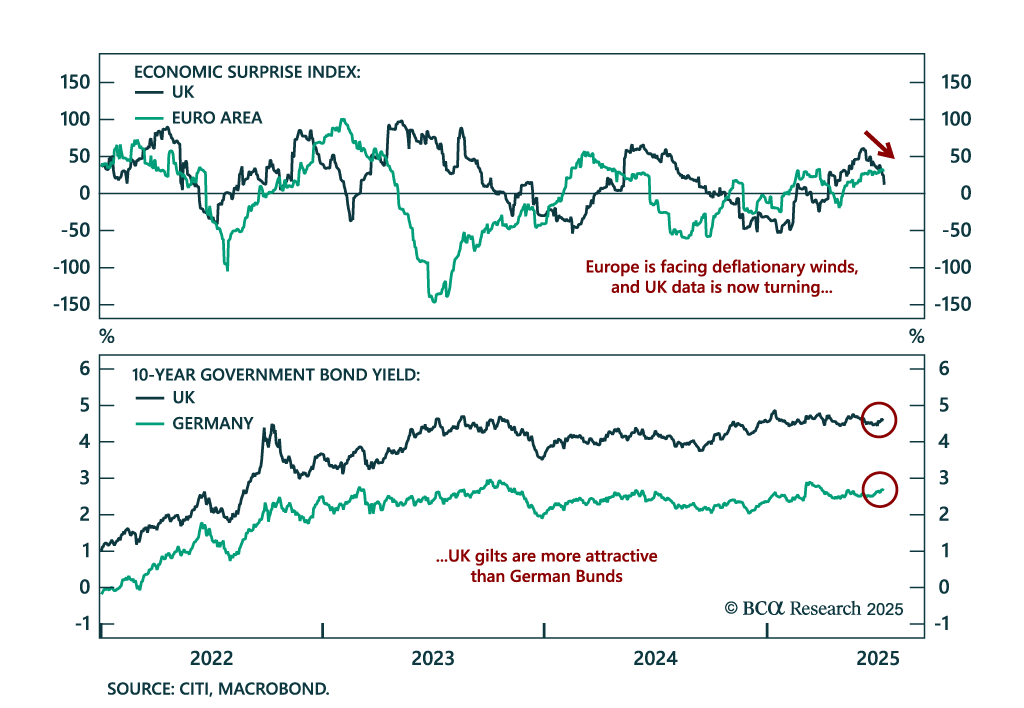

UK growth data continues to disappoint, making the case for a Gilts overweight and a dovish BoE. May GDP fell 0.1% m/m, missing estimates and marking a consecutive monthly contraction after April’s 0.3% decline. Industrial and manufacturing output both…

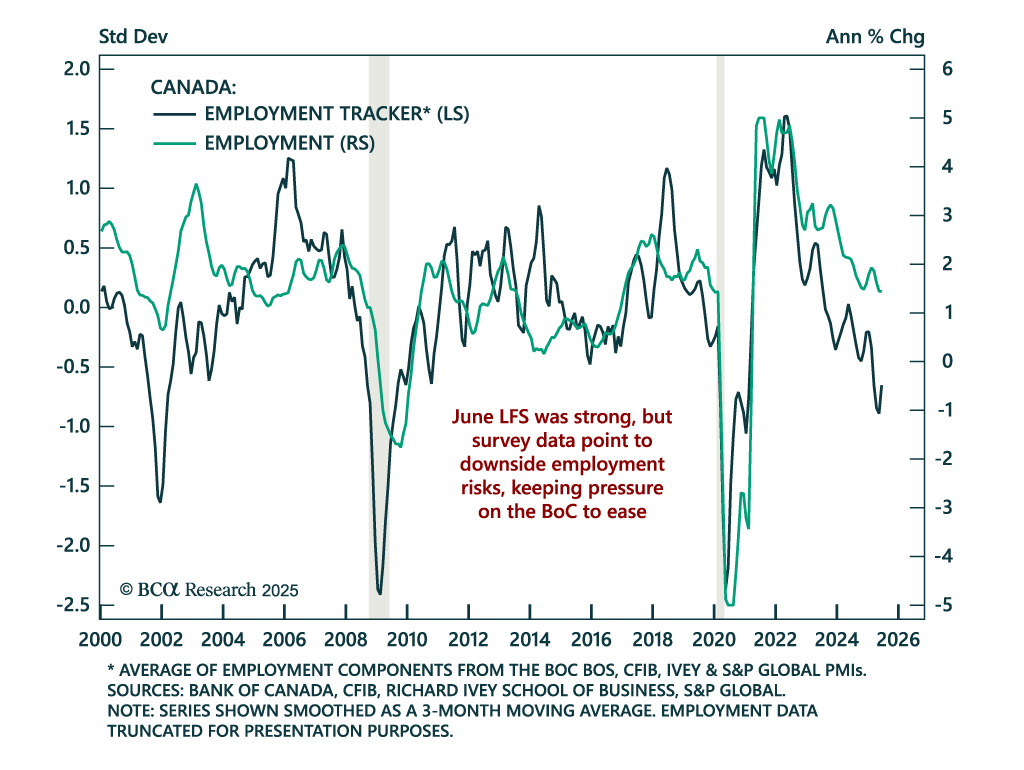

June’s strong Canadian jobs data does not argue against further easing and a CGBs overweight. Employment rose by 83.1k versus expectations for no growth, the first increase since January. The unemployment rate fell to 6.9% from 7.0%. However, gains were…

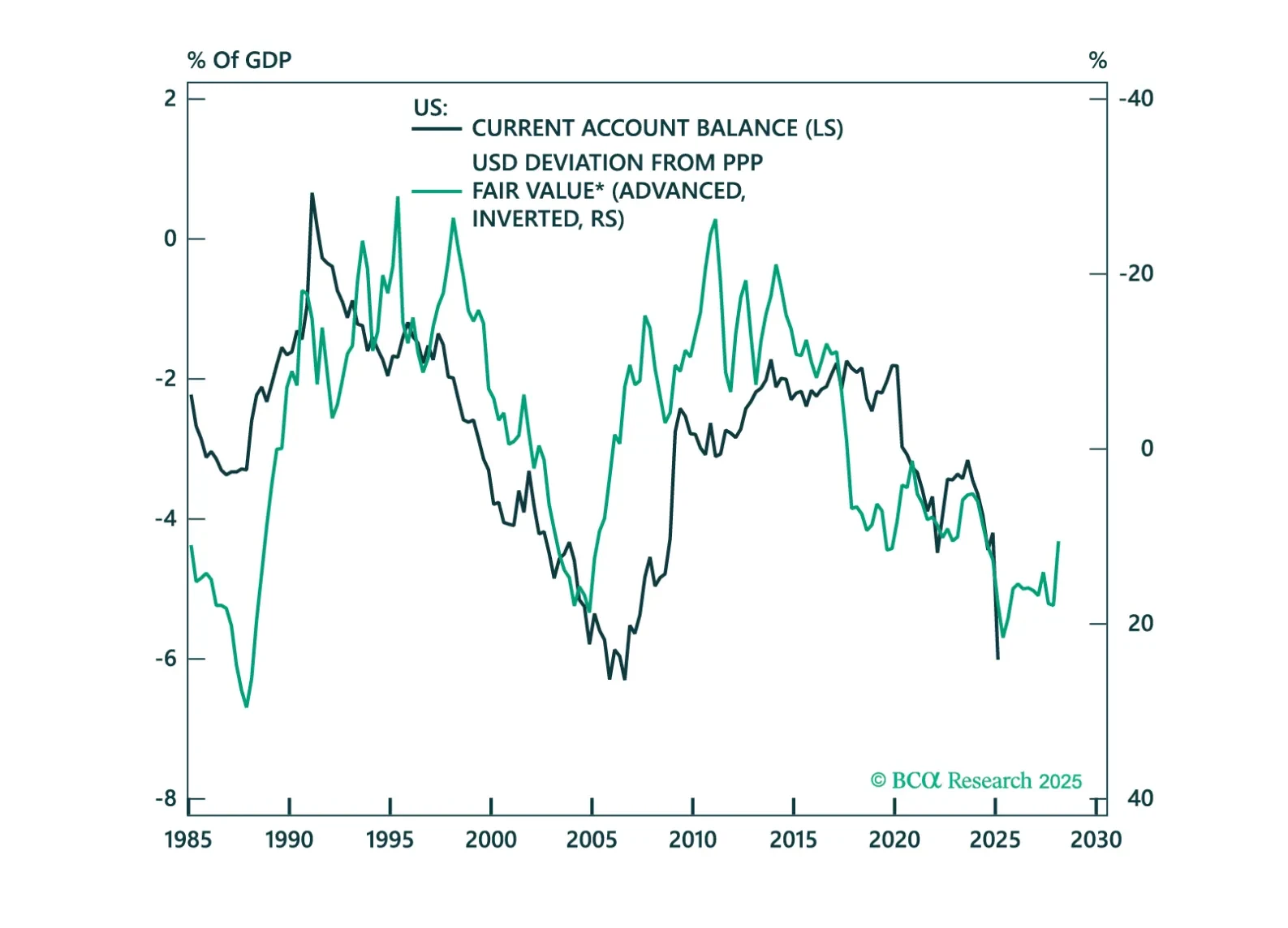

In this chartbook, we look at the balance of payments across DM and EM countries. The US does not fare well, but neither do a few other countries.

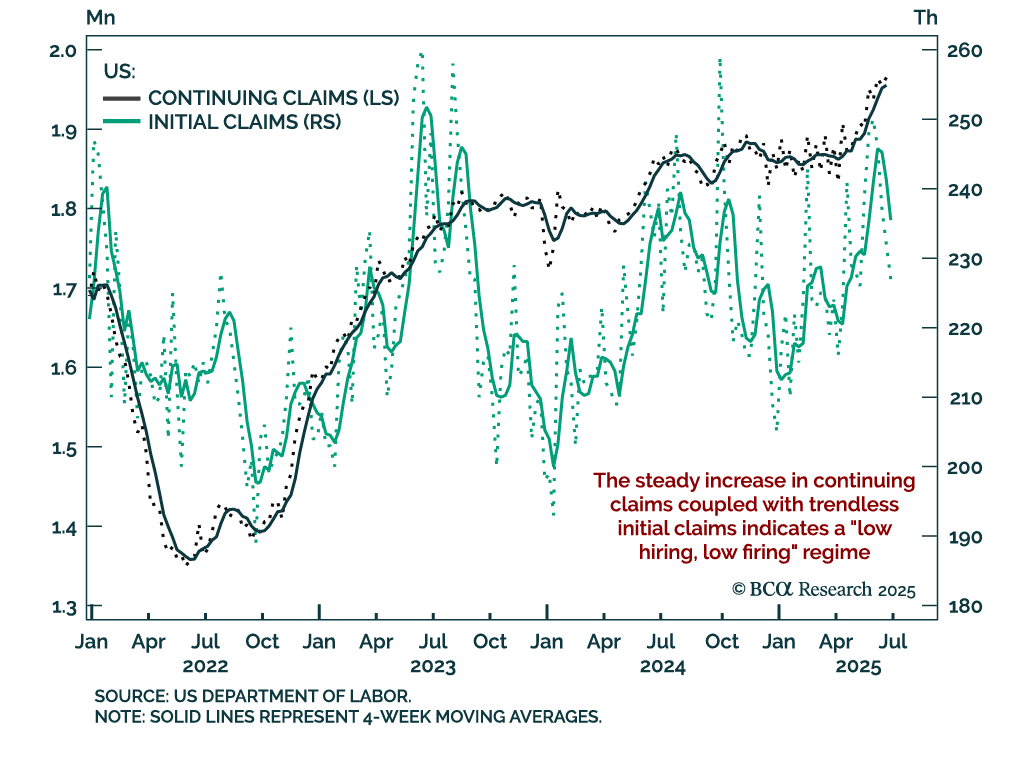

Rising continuing claims and slowing hiring momentum reinforce our defensive allocation stance. Continuing claims have reached a post-COVID high of 1.965m, while initial claims eased to 227k after peaking at 250k. The divergence between steadily rising…

Our Portfolio Allocation Summary for July 2025.

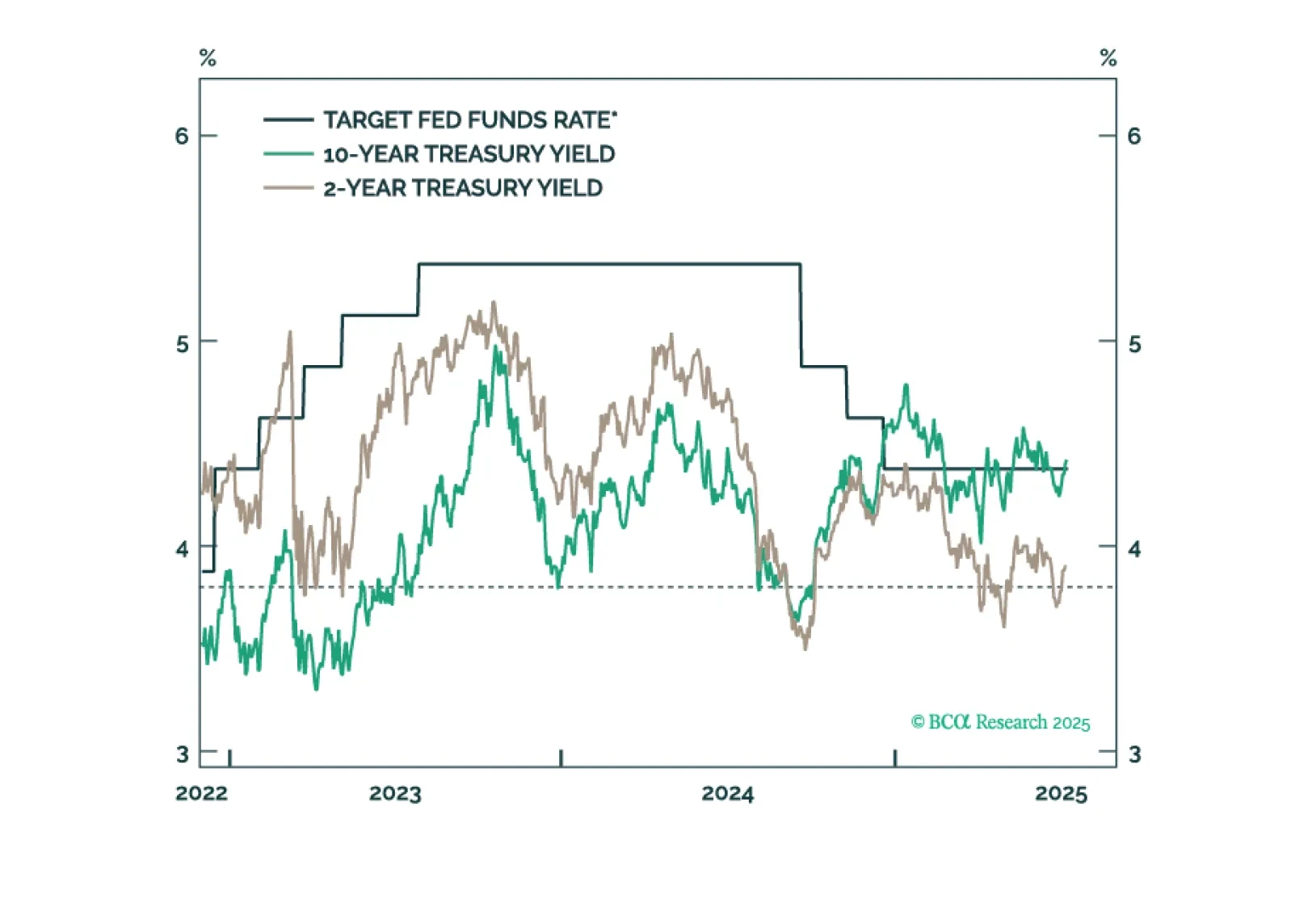

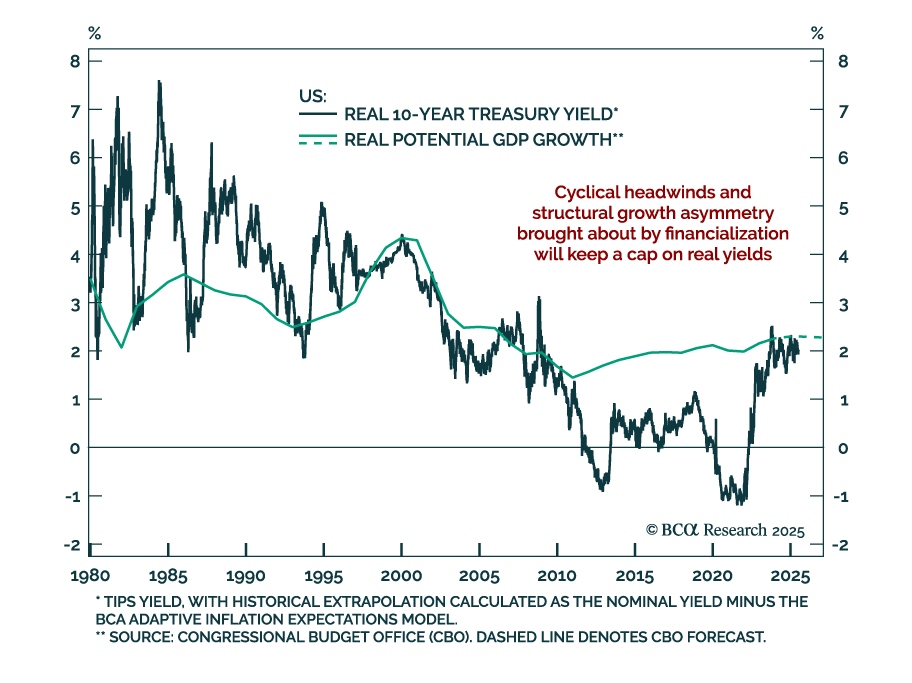

Real yields remain near 2%, but structural asymmetries justify a duration overweight as inflation expectations stay anchored. US 10-year yields have been volatile, testing 4.80% in January and dropping below 4.0% after April’s Liberation Day. Meanwhile,…

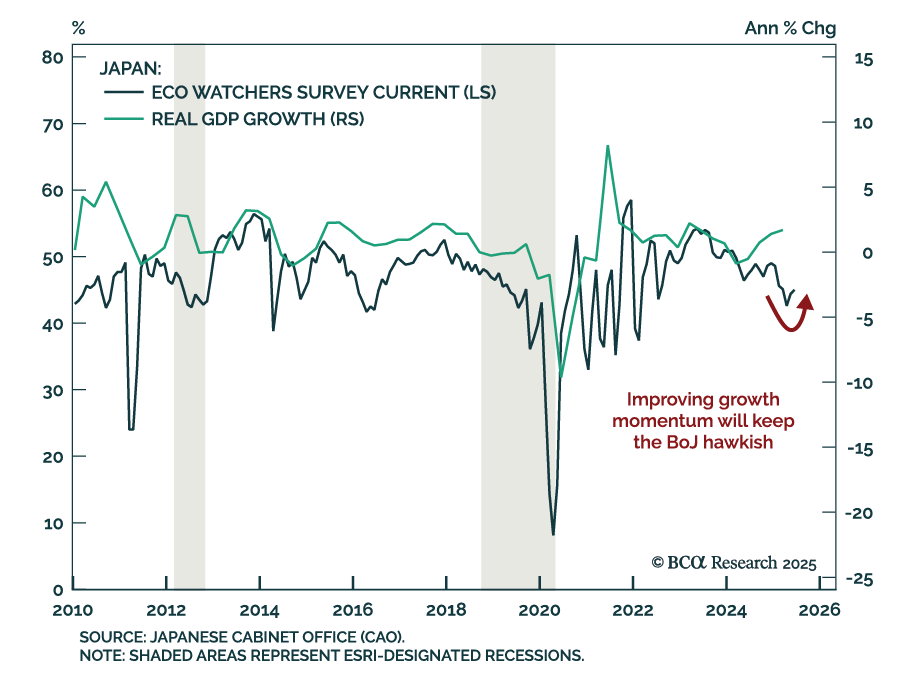

Japan’s improving growth momentum and structural inflation shift support an underweight in JGBs and long JPY positioning. The June Eco Watchers Survey was broadly in line with expectations, with current conditions ticking up to 45.0 and expectations modestly…

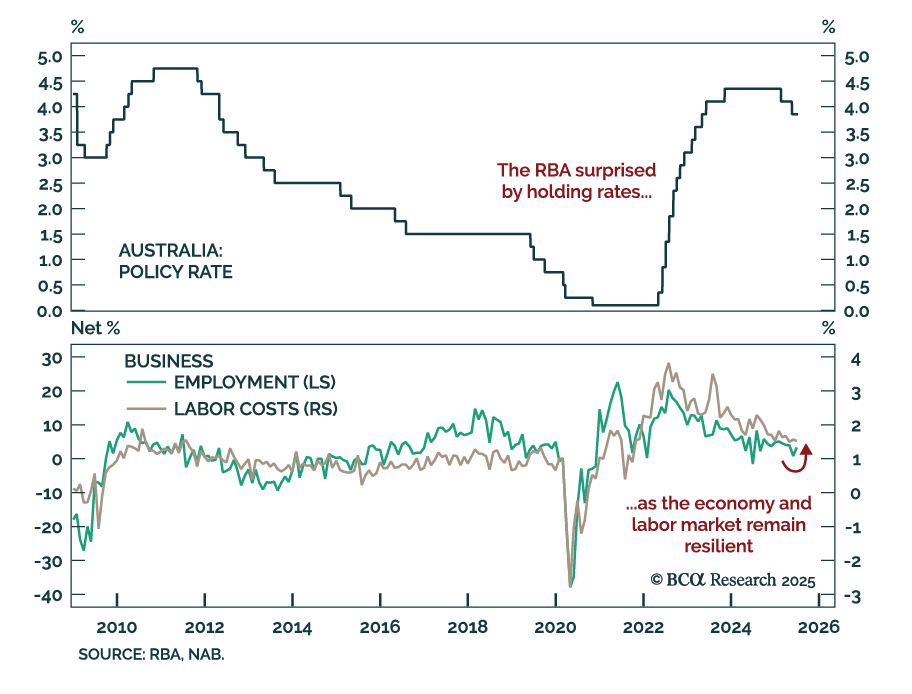

The RBA’s surprise hold reinforces a slower easing path, warranting an underweight on Australian bonds. Markets had priced in a 25 bps cut, but the central bank opted to keep rates at 3.85%. Governor Bullock characterized the decision as a matter of timing,…