Developed Countries

The ISM Services PMI largely surpassed expectations in May. The headline index grew by 4.4 ppt to 53.8, returning to expansion following April’s one-month contraction. Double-digit jumps in new export orders (13.9 ppt) and business activity (+10.3 ppts) drove…

The Bank of Canada reduced its policy rate by 25 basis points from 5% to 4.75% on Wednesday, in line with the market consensus. Headline inflation and the BoC’s preferred measures of core inflation are within the BoC’s target range of 1-3%, and shorter-term…

Utilities have had a stellar run since February with the MSCI ACW Utilities index outperforming the MSCI ACW by nearly nine percentage points. Despite being a defensive sector, Utilities’ performance this year has been comparable to that of top performing…

According to BCA Research’s US Bond Strategy service, Mortgage-Backed Securities are currently priced below fair value. Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 49 basis points in May, bringing year-to-date excess…

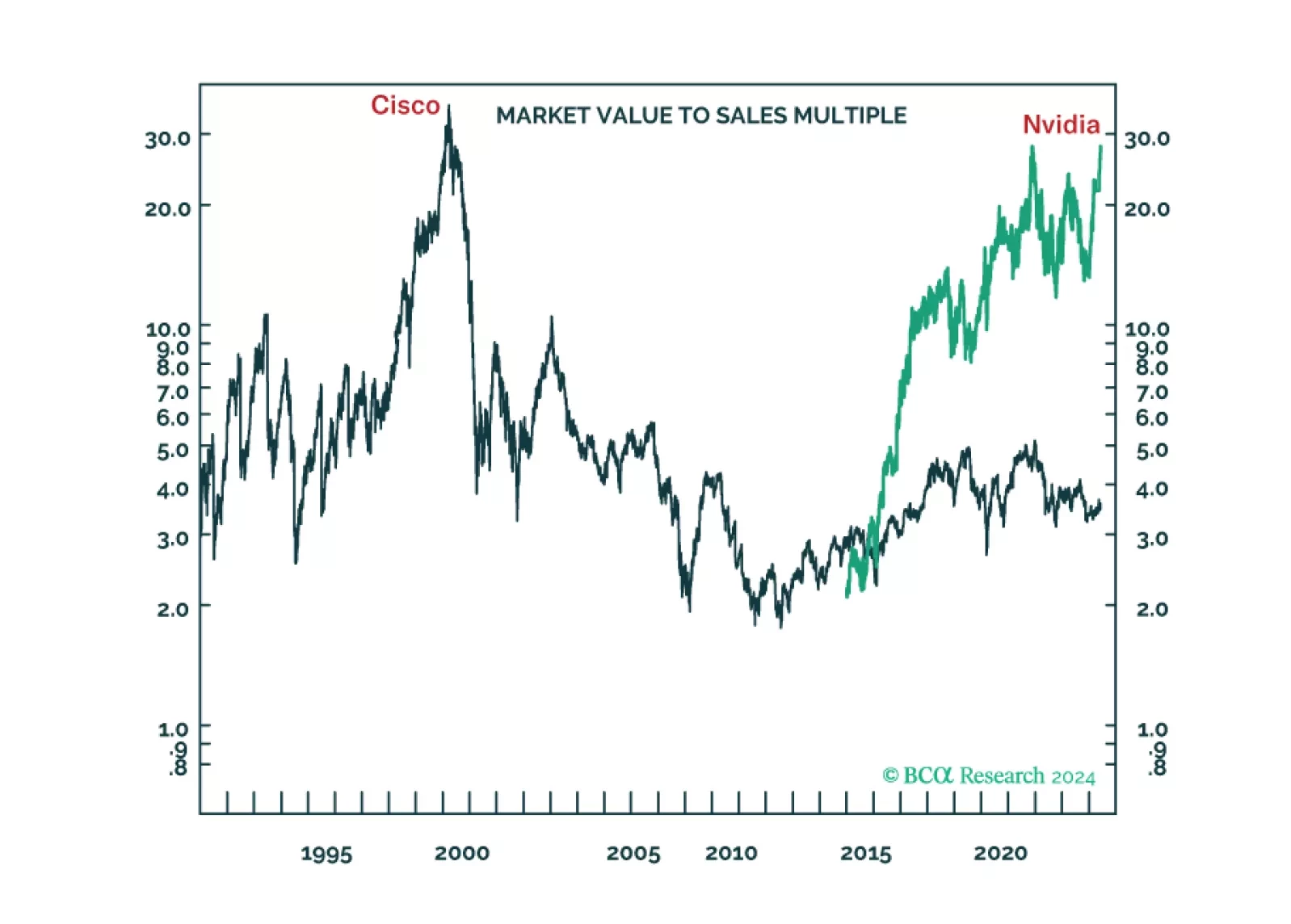

The long-term winners from the generative-AI gold rush are unlikely to be the ‘picks and shovels’ stock Nvidia or the overvalued US superstars of Web 2.0. We discuss the structural investment implications. Plus: time to go tactically overweight global consumer discretionary (RXI).

US job openings softened from 8.5 million in March to 8.1 million in April, below expectations of 8.4 million, and the lowest level in three years. Healthcare and social assistance, as well as leisure and hospitality, drove the decline while openings in the…

The moderation in core PCE in April was a step in the right direction towards a Fed easing. Our Global Investment Strategists also highlighted that outside of a few pandemic-related “catch-up” categories such as shelter, health care, and auto insurance, CPI…

Consumption accounts for two-thirds of the US economy, and our recession view relies heavily on the deteriorating outlook for US consumers. That said, dissecting US GDP into its components reveals that consumption tends to merely stabilize during…

Corporate and junk bonds are the fixed-income sectors that are most exposed to an economic downturn. We’ve highlighted that markets continue to price in a Goldilocks scenario, with spreads narrowing despite ongoing deterioration in the labor market. Spreads…

According to BCA Research’s Global Asset Allocation service, the economy has been in the “Overheating” phase of the cycle for a while, with signs of slowing growth but also stubbornly high inflation. The most likely next phase is “Recession,” though the…