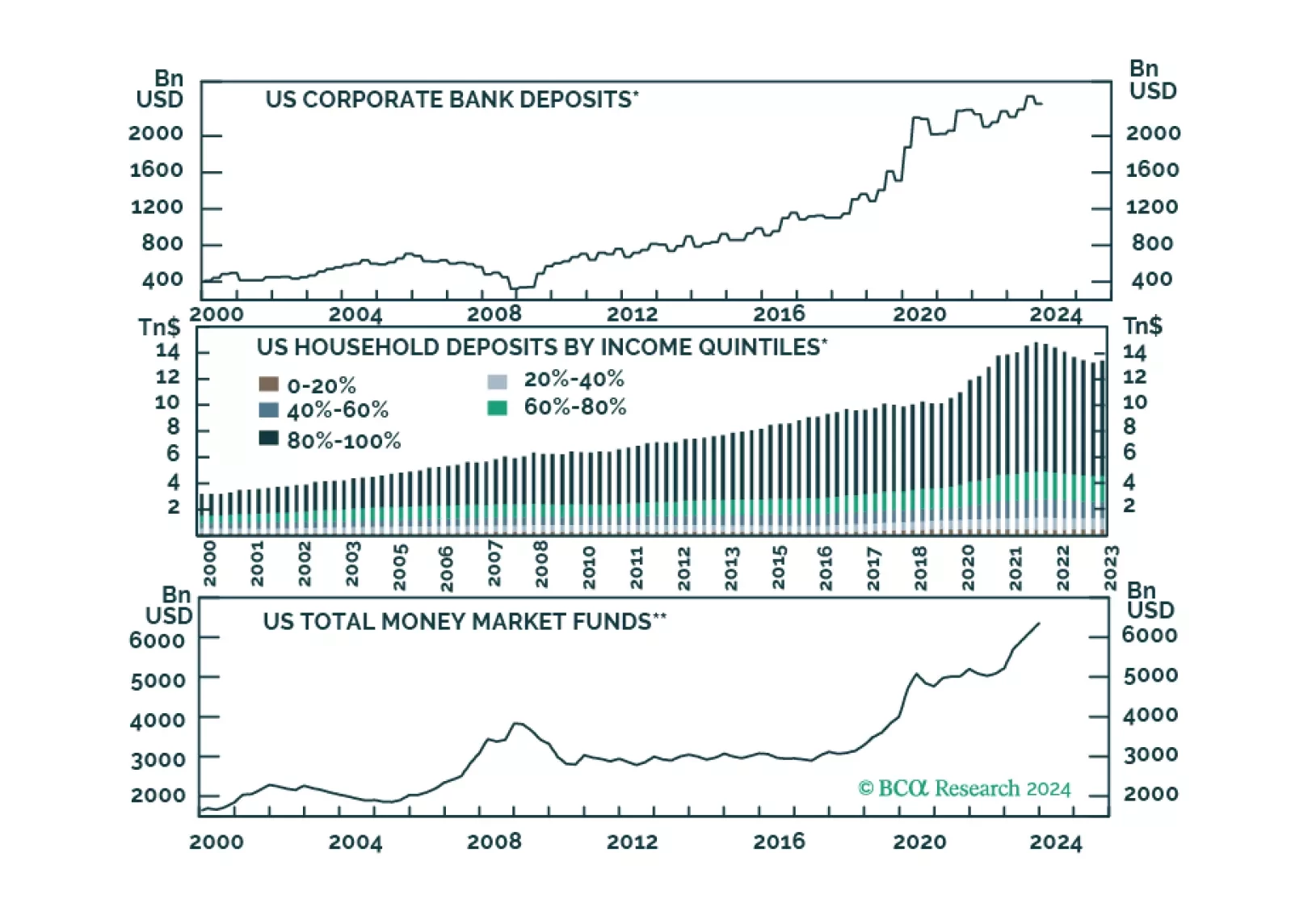

Developed Countries

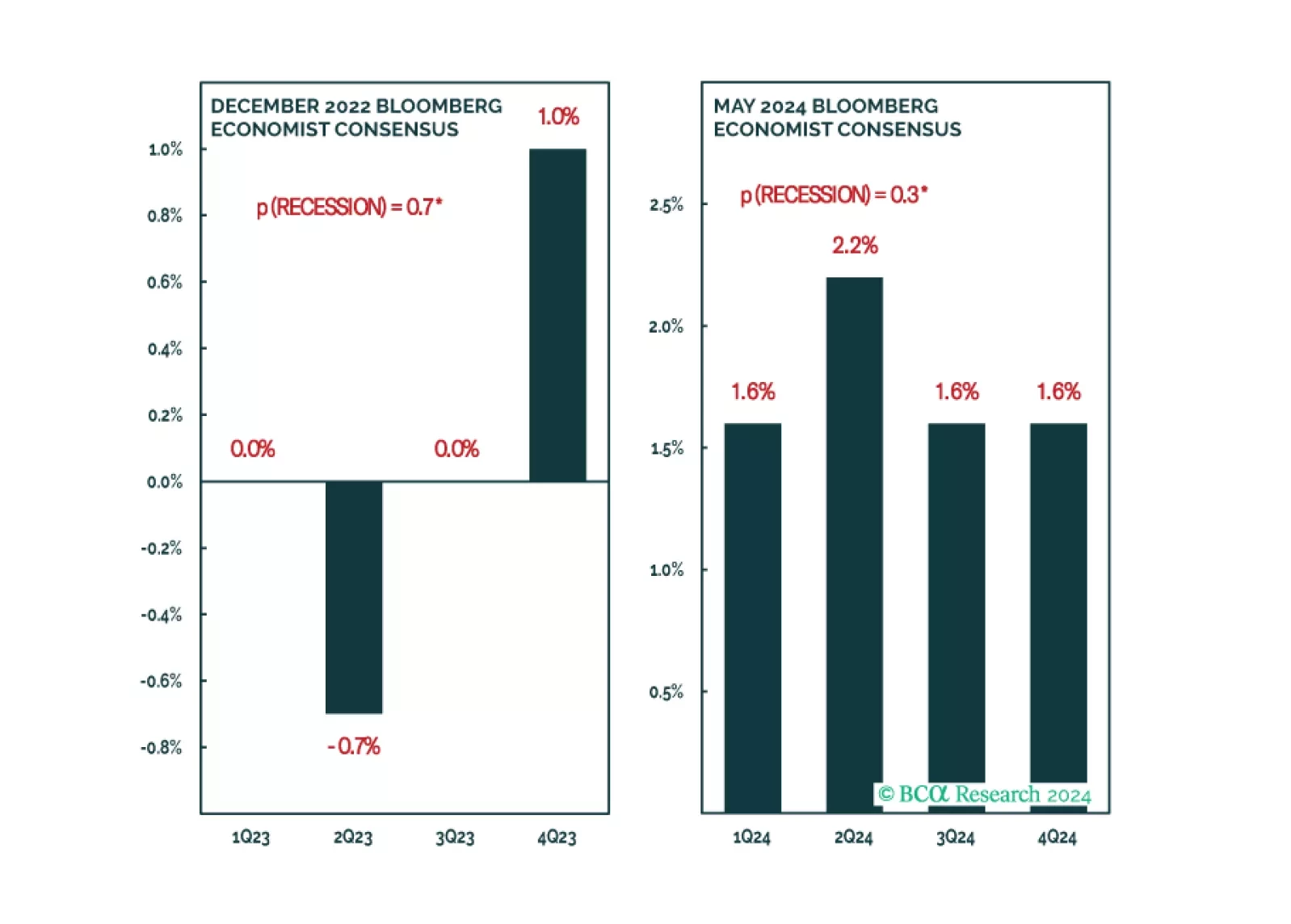

According to BCA Research’s Global Investment Strategy service, there is only a narrow path to a soft landing. Our colleagues estimate a mere 20% chance that the US will avoid a recession before the end of 2025. The US unemployment rate is a highly…

Looking at economic activity, global monetary policy seems restrictive, however, the behavior of financial markets tells a different story. What gives?

The signs of an approaching recession are starting to emerge. We will turn tactically defensive once they all fall into place.

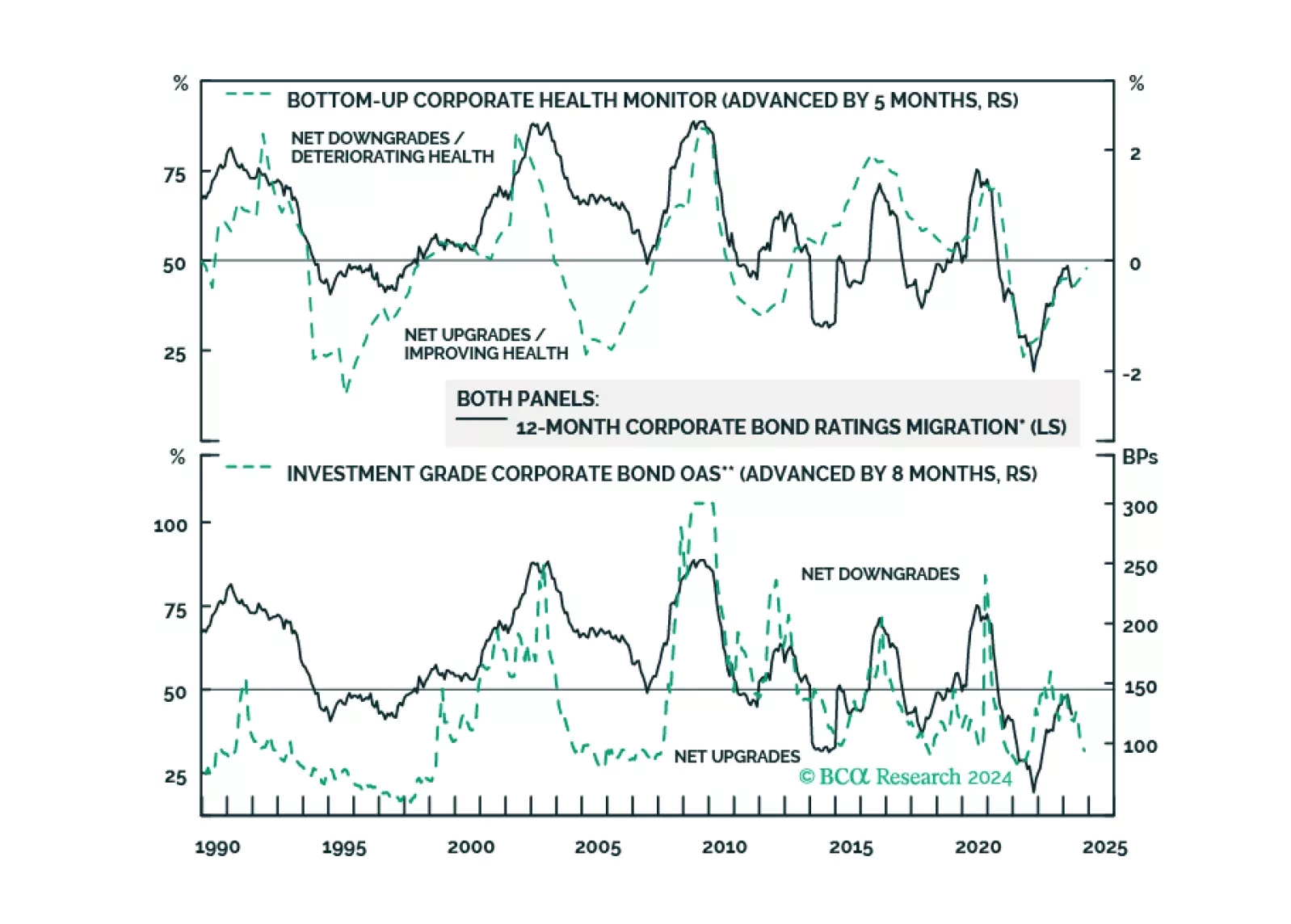

Nonfinancial corporate balance sheets are generally in good shape, but there are signs of deterioration at the bottom-end of the credit spectrum. We present evidence showing that credit deterioration at the bottom-end of the credit spectrum has a habit of migrating upwards.

The Reserve Bank of New Zealand (RBNZ) kept interest rates on hold at this week’s monetary policy meeting, in line with expectations. However, there were three new notes from its monetary policy statement that will likely affect how it approaches future…

US durable goods orders surprised to the upside in April, growing 0.7% m/m against expectations they would decline. The March growth rate was nevertheless revised significantly lower, from 2.6% m/m to 0.8% m/m. Core capital goods shipments (an input into…

Negotiated wages rose 4.7% y/y in Q1, from 4.5% y/y in Q4 in the Eurozone. Meanwhile, preliminary estimates for the Eurozone Composite PMI surprised to the upside in May. Although wage growth is the main driver of services inflation and Euro Area economic…

According to BCA Research’s Counterpoint service, the non-US developed economy is “demand-constrained” whereas the US economy is “supply-constrained”. This schism will continue but in reverse. The team has highlighted that following the surge in…

Minutes from the April 30 - May 1 FOMC meeting struck a hawkish tone on the latest discussions among Fed officials. Notably, the reference to “Various participants mention[ing] a willingness to tighten policy further should risks to inflation materialize in a…

The Conference Board measure of CEO Confidence improved slightly in Q2, from 53 to 54. A reading above 50 indicates that optimistic perceptions of business conditions outweigh pessimistic assessments. The Q2 survey result marks a second consecutive quarter of…