Developed Countries

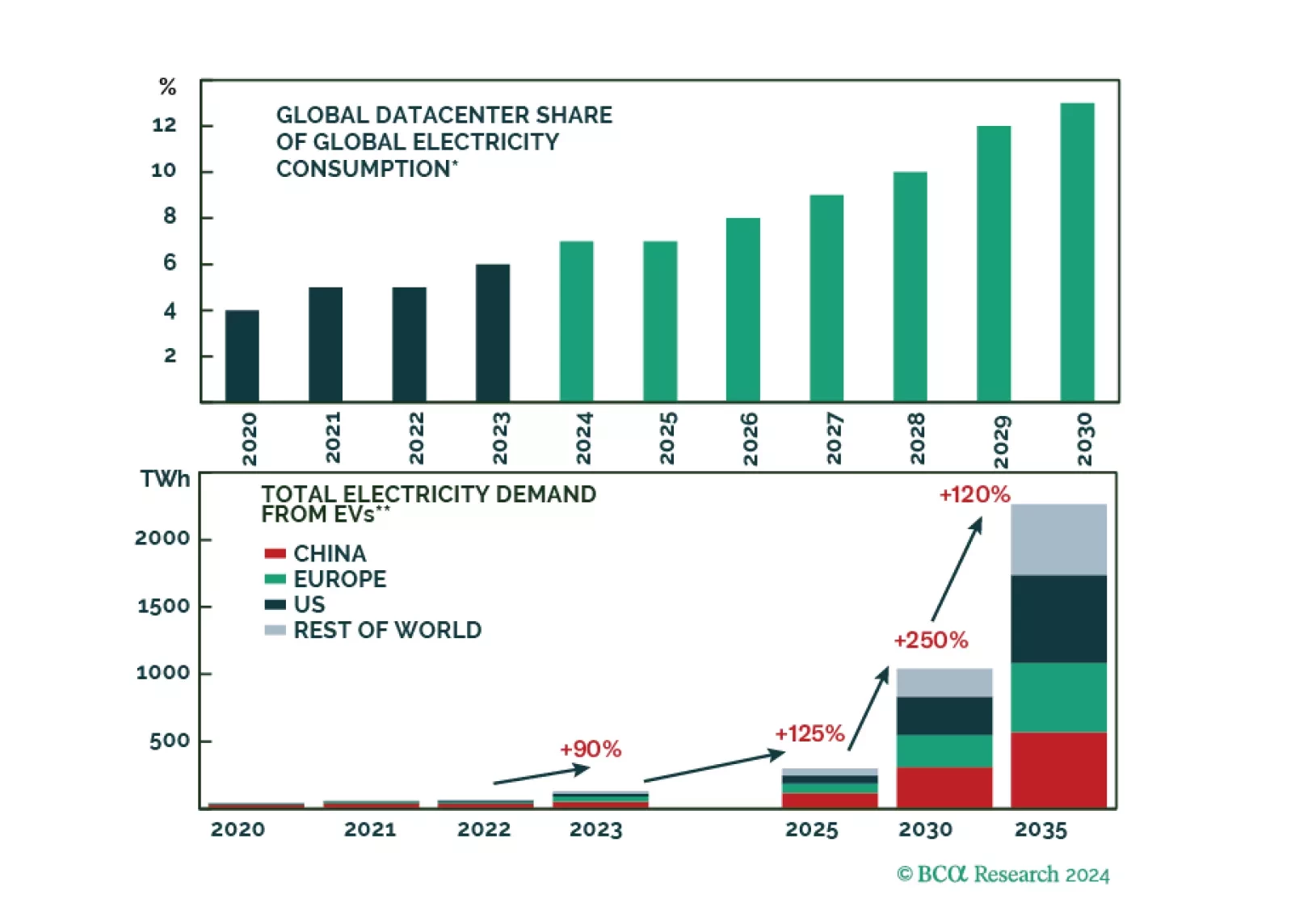

AI, EVs, and reshoring will lead to a massive surge in demand for electricity. Carbon-free, cheap, baseload nuclear energy stands to greatly benefit from these megatrends going forward.

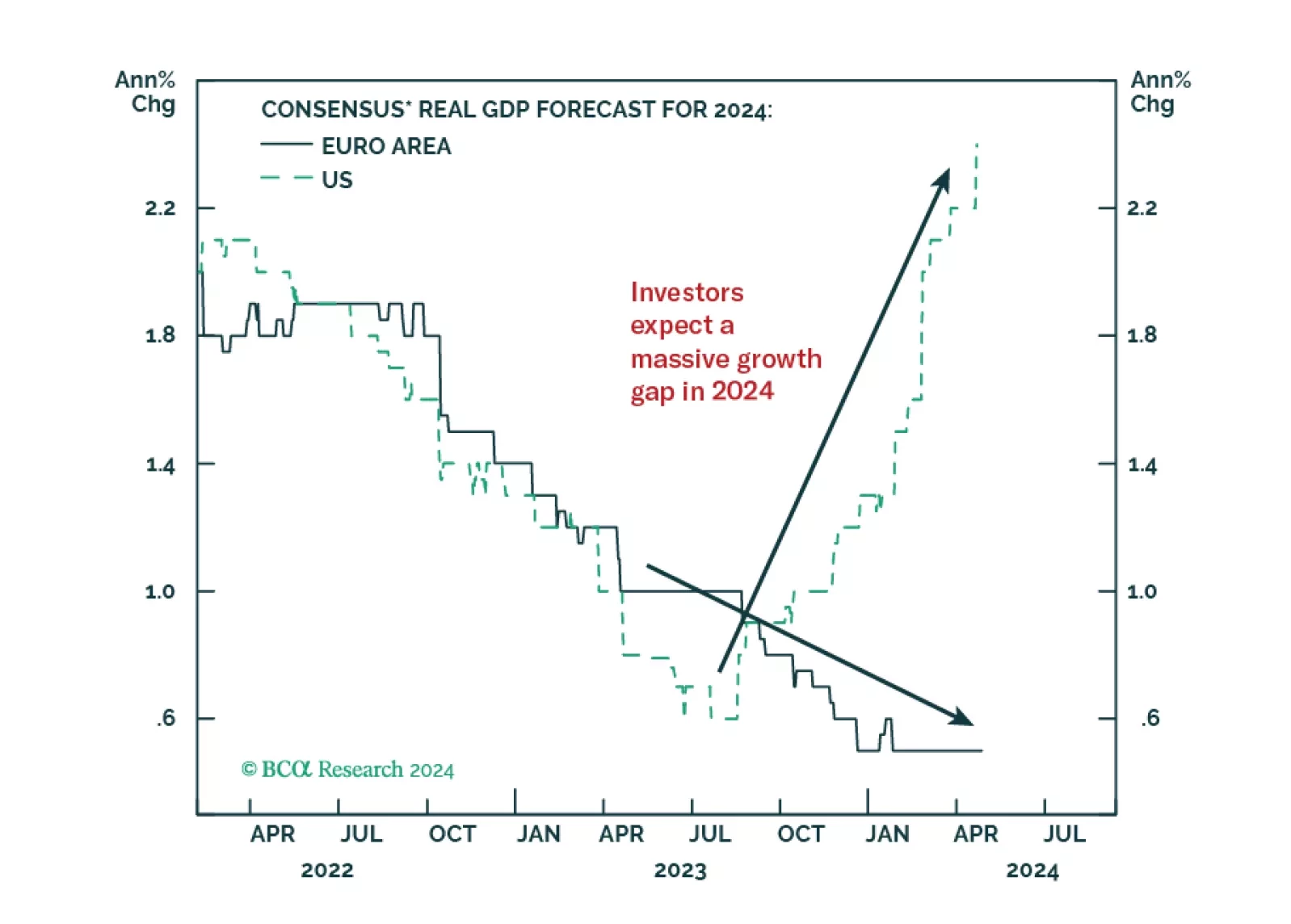

Investors anticipate a record growth gap between the US and the Eurozone in 2024. Does this skewed expectation create market opportunities?

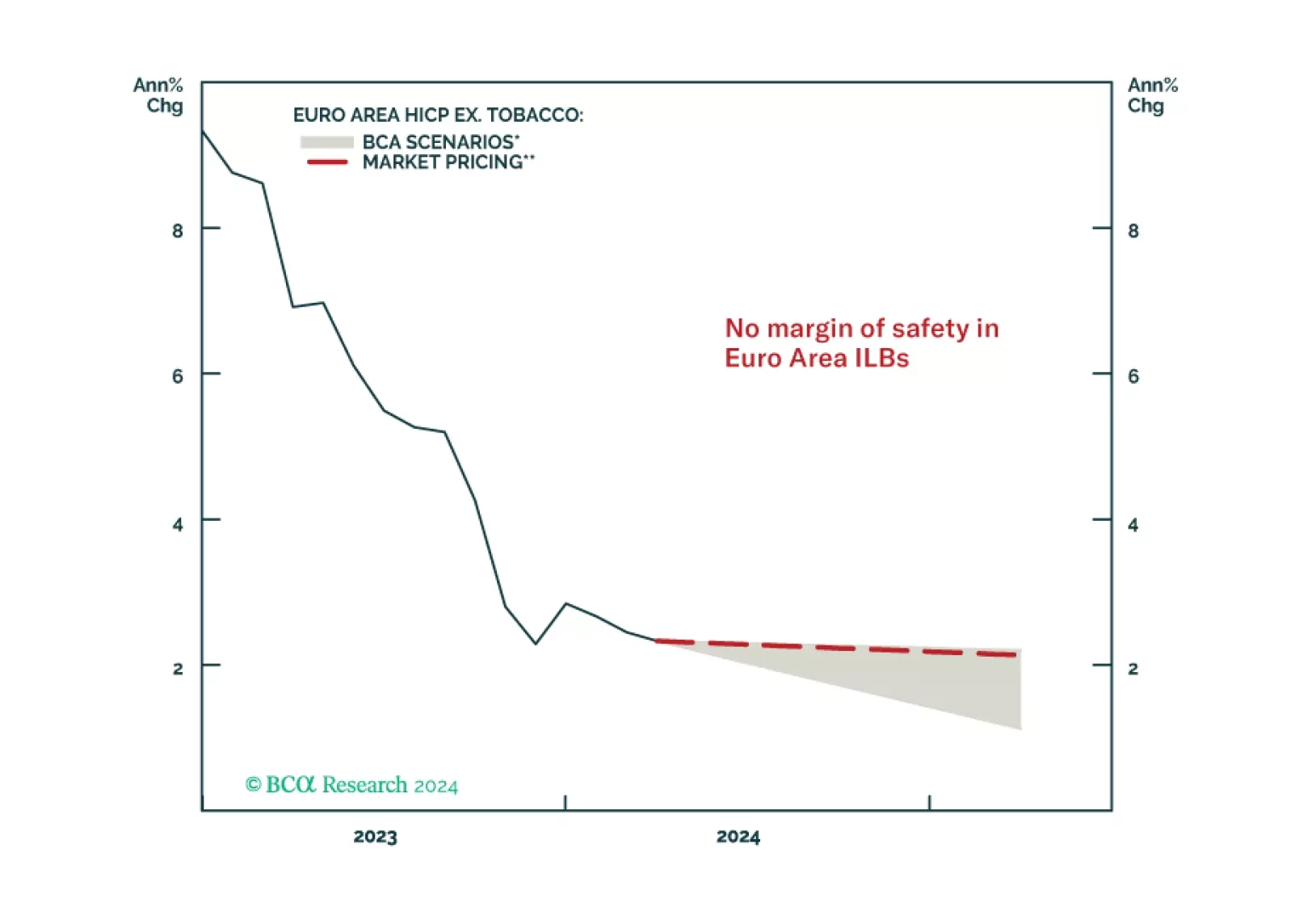

In this Special Report, we introduce our Euro Inflation-Linked Golden Rule – a framework to profitably trade and invest in Euro Area inflation-linked bonds versus nominals. The Rule is currently signaling that nominal government bonds should outperform inflation-linked bonds over the next year as disinflation in the Euro Area continues.

The latest edition of our Big Bank Beige Book suggests the expansion remains intact, though weakness in C’s private-label credit card portfolio could be a harbinger of distress among lower-income consumers. We remain tactically neutral with a bias to turn defensive once clearer signs of a recession emerge.