Developed Countries

Over the last weeks, US semiconductor stocks have plunged by over 17%. In a way, this correction should be expected. Semiconductor stocks had skyrocketed this year. Even after the recent pullback, semi stocks are still up over 20%…

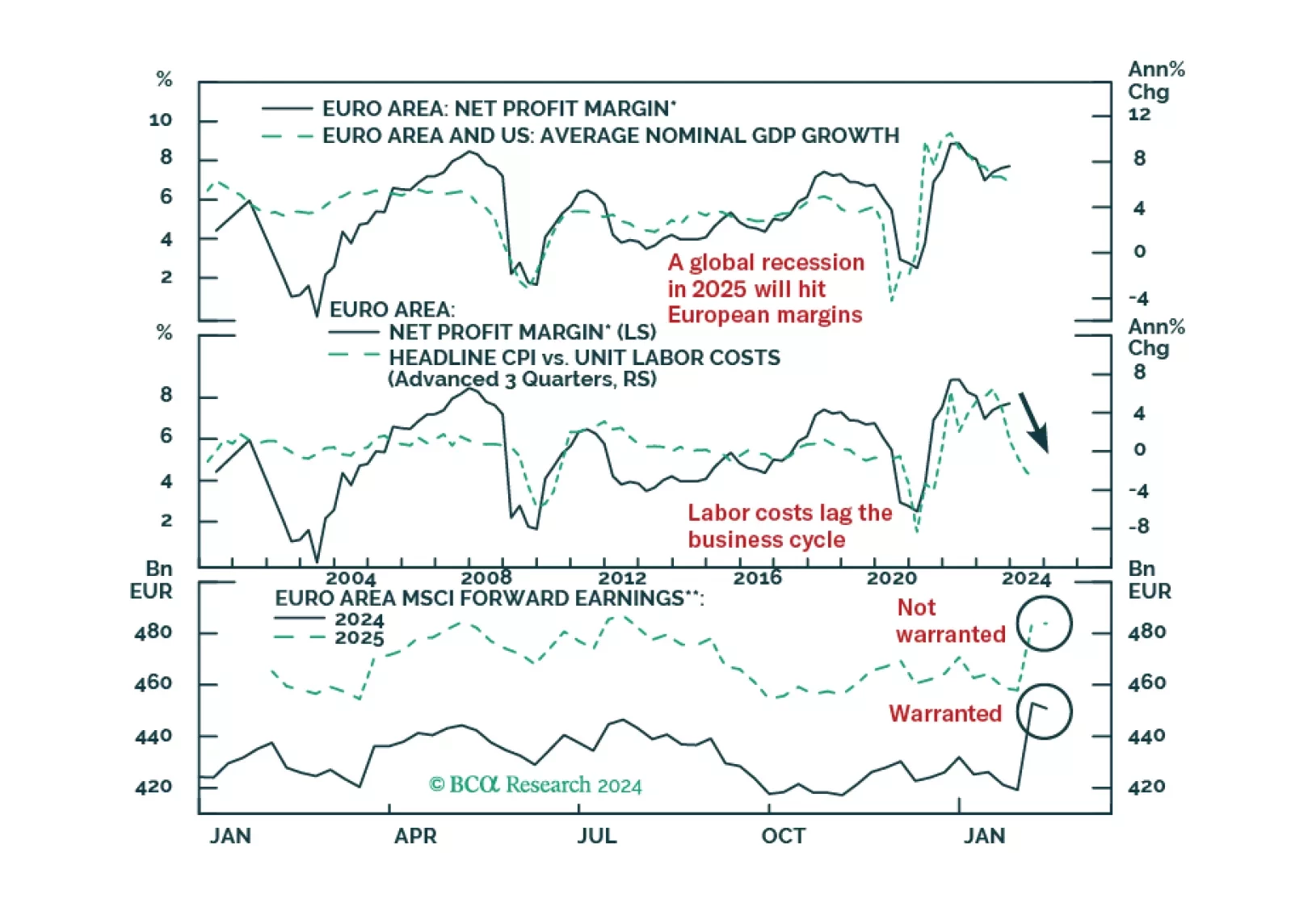

According to BCA Research's European Investment Strategy service, European profit margins have downside because they are both elevated and procyclical. European net margins stand at 7.7% above their long-term average of 5%. Analyst expectations…

European profits margins are elevated. Will a mild recession be enough to bring them down?

This Special Report introduces a framework for assessing the relative importance of slope change and initial yield in curve trade performance. The yield penalty for curve steepeners has fallen significantly since the beginning of the year, and we recommend shifting out of Treasury curve flatteners and into Treasury curve steepeners in US bond portfolios.

Japan’s national CPI inflation unexpectedly cooled in March, falling to 2.7% y/y versus consensus estimates it would remain at 2.8% y/y. Notably, measures of underlying inflation such as core CPI (ex-fresh food) and “core-core” CPI (ex-fresh food and energy)…

The IMF’s latest fiscal monitor report highlighted the dangers that rising sovereign debt alongside rising deficits pose to advanced economies. The United States, in particular, is at risk. The IMF projects that fiscal deficits in the US will stay above 3% of…

BCA’s US Beige Book Monitor – an indicator we use to gauge changes in the language of the Fed’s Beige Book report and which historically tracks US GDP growth – has improved in April. Nevertheless — and despite March's hot retail sales and February's…

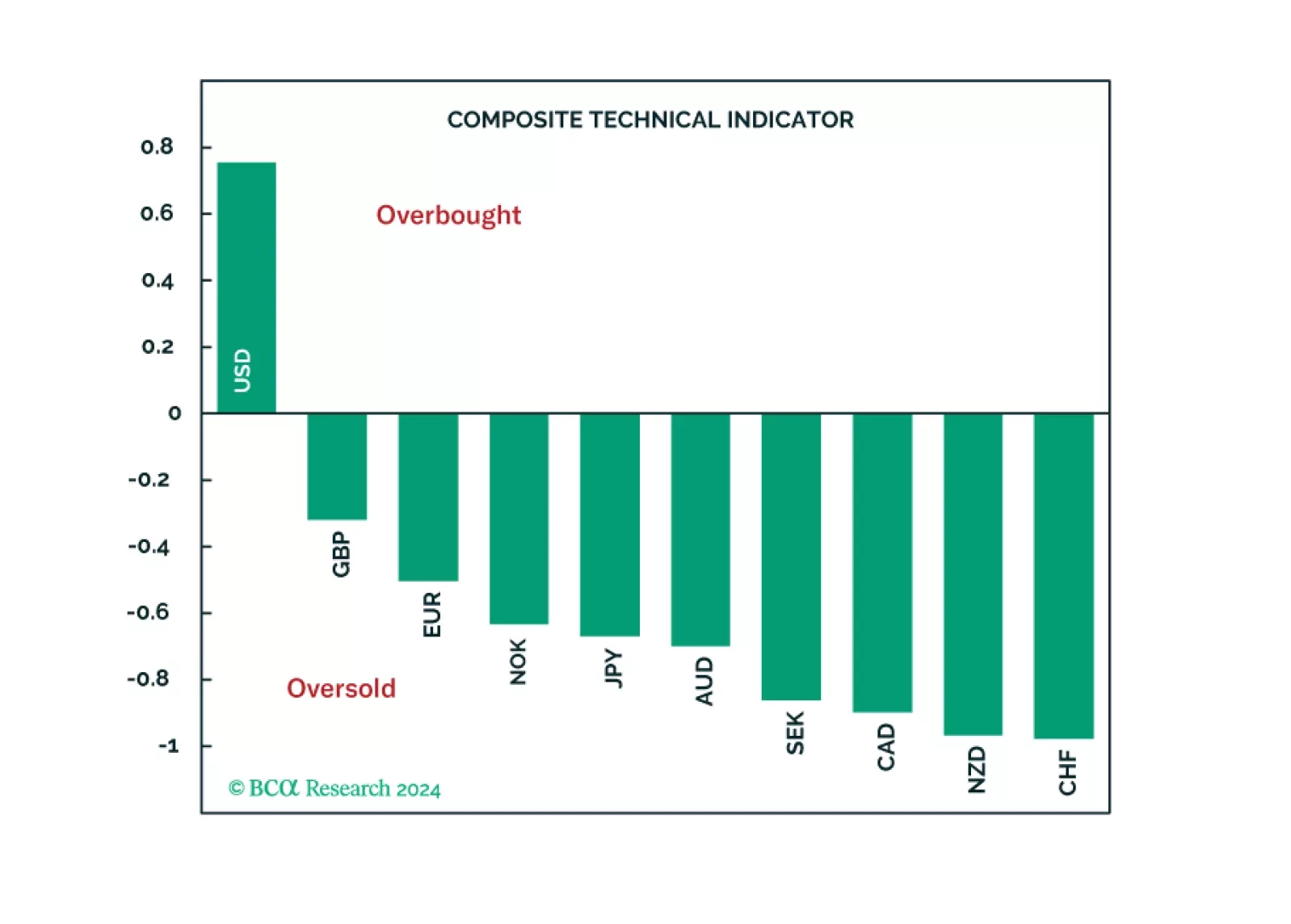

According to BCA Research’s Foreign Exchange Strategy service, an ensemble of technical indicators reveals that the dollar is overbought in the near term. The list of indicators they have compiled for this analysis is simple but potent: How are…

In this report, we review what our technical indicators are telling us about the G10 currencies.

Nvidia has amassed staggering sales from AI. Last year its data center revenues exploded, going from just over $4 billion in 2023 Q1, to over $18 billion in 2023 Q4. That said, its competitors have not done as well. In the same time frame that Nvidia added…