Developed Countries

The final UK S&P Global Services and Composite PMIs for March were both revised down slightly from their flash estimates. While the report indicates that activity is still expanding, there has been a clear loss in momentum since February. The Composite…

It is too early for the RBA to begin cutting rates. Inflation remains above target, with core CPI currently standing at 3.4%, one of the highest numbers amongst major economies. The labor market is also fundamentally strong. Australia’s unemployment rate…

As a small open economy, Sweden’s economic performance is a good barometer of global growth developments. Swedish PMIs for March were overall positive. The Manufacturing PMI rose to the 50 boom-bust line following 19 consecutive months of contraction and…

Flash estimates for Euro Area inflation in March surprised to the downside. Headline inflation slowed from 2.6% to 2.4% versus expectations of 2.5% and core inflation eased from 3.1% to 2.9% versus expectations of 3%. While the stickiness of services…

The US manufacturing sector appears to be enjoying a revival. As we highlighted yesterday, the ISM manufacturing PMI unexpectedly returned to growth in March and the S&P Global US manufacturing PMI remains in expansion territory. Yet, service sector…

The extraordinary performance of AI companies has pushed US growth stocks to new highs. So far, the MSCI US Growth Index has returned almost 11% since the start of the year, outperforming global stocks by over 3%. No growth index from the rest of the world…

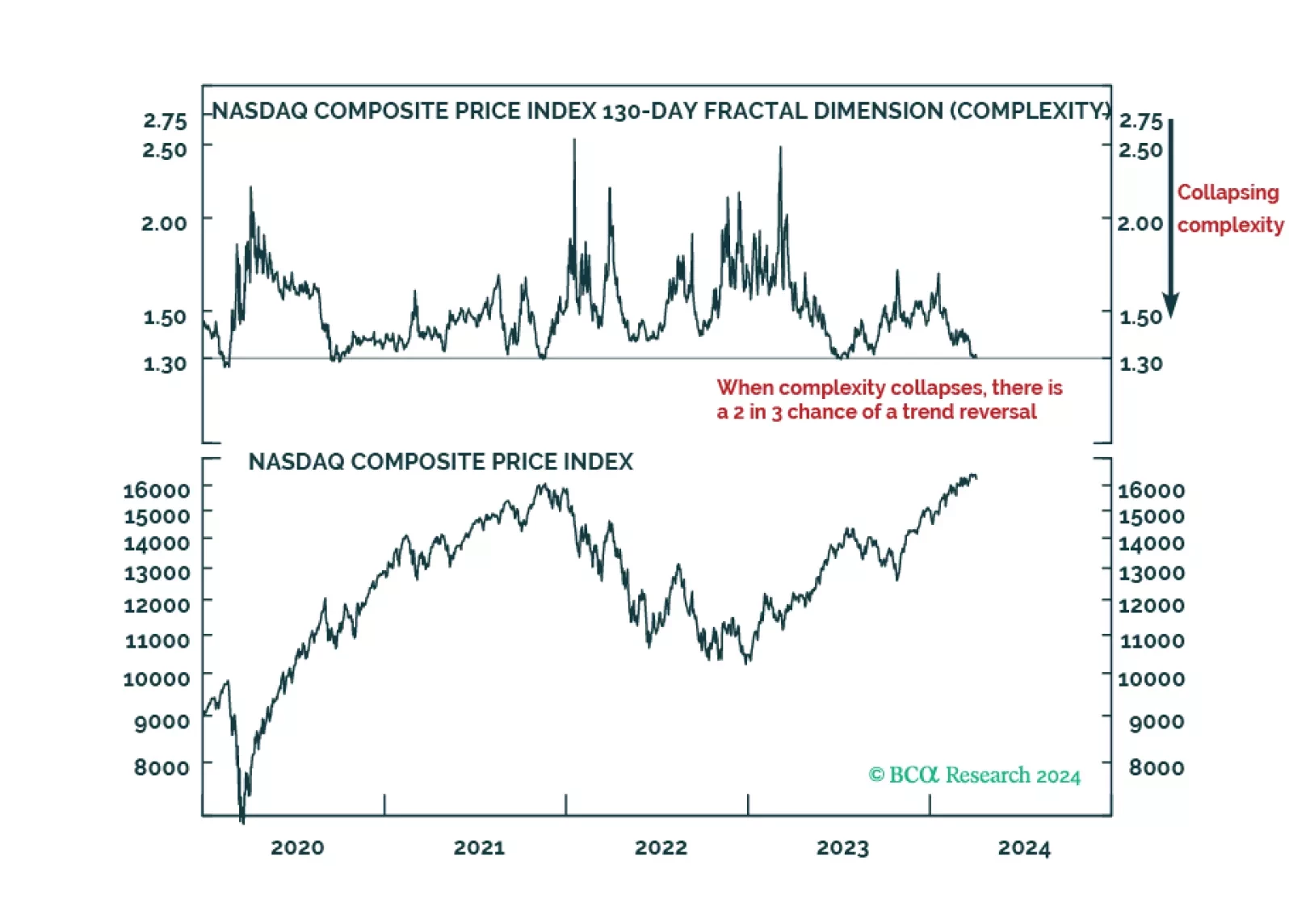

The analysis of complexity is a massive competitive advantage in investing, and from today, clients will be able to monitor the complexities of the world’s 17 major investments on our webpage in real-time.

The ISM Manufacturing PMI came in at 50.3 in March, better than expectations of 48.4 and breaking above the 50 boom-bust line for the first time since September 2022. Notably the new orders component rebounded to 51.4, marking the second expansionary reading…

The number of job openings in the US in February (8.76 million) was little changed from the downwardly revised 8.75 million in January, keeping the job openings rate stable at 5.3%. Similarly, the hiring rate was little changed at 3.7% in February, from 3.6%…

The Dallas Fed released its trimmed mean PCE inflation rate for February on Friday. The trimmed mean PCE is a measure of underlying inflation which excludes the top 31% and the bottom 25% of the PCE basket and then uses a weighted average of the remaining…