Developed Countries

Our Portfolio Allocation Summary for February 2024.

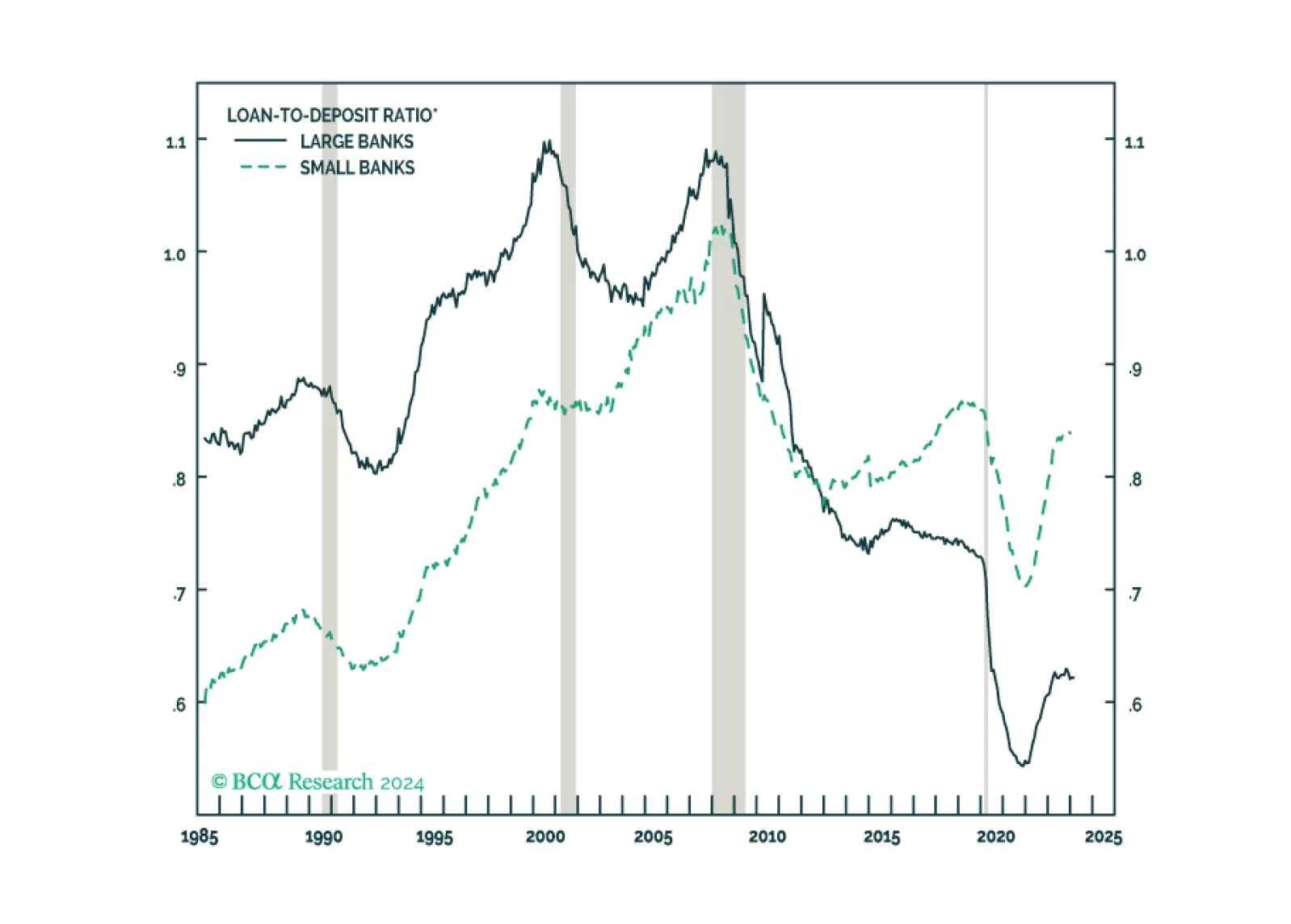

We do not believe that NYCB is a canary in the coal mine for a new round of bank distress. The MidCap 400 Regional Bank Index’s subsequent 10% decline looks to us like a juicy opportunity for stockpickers who can separate the wheat from the chaff. Our Special Report is meant to assist them with their initial winnowing.

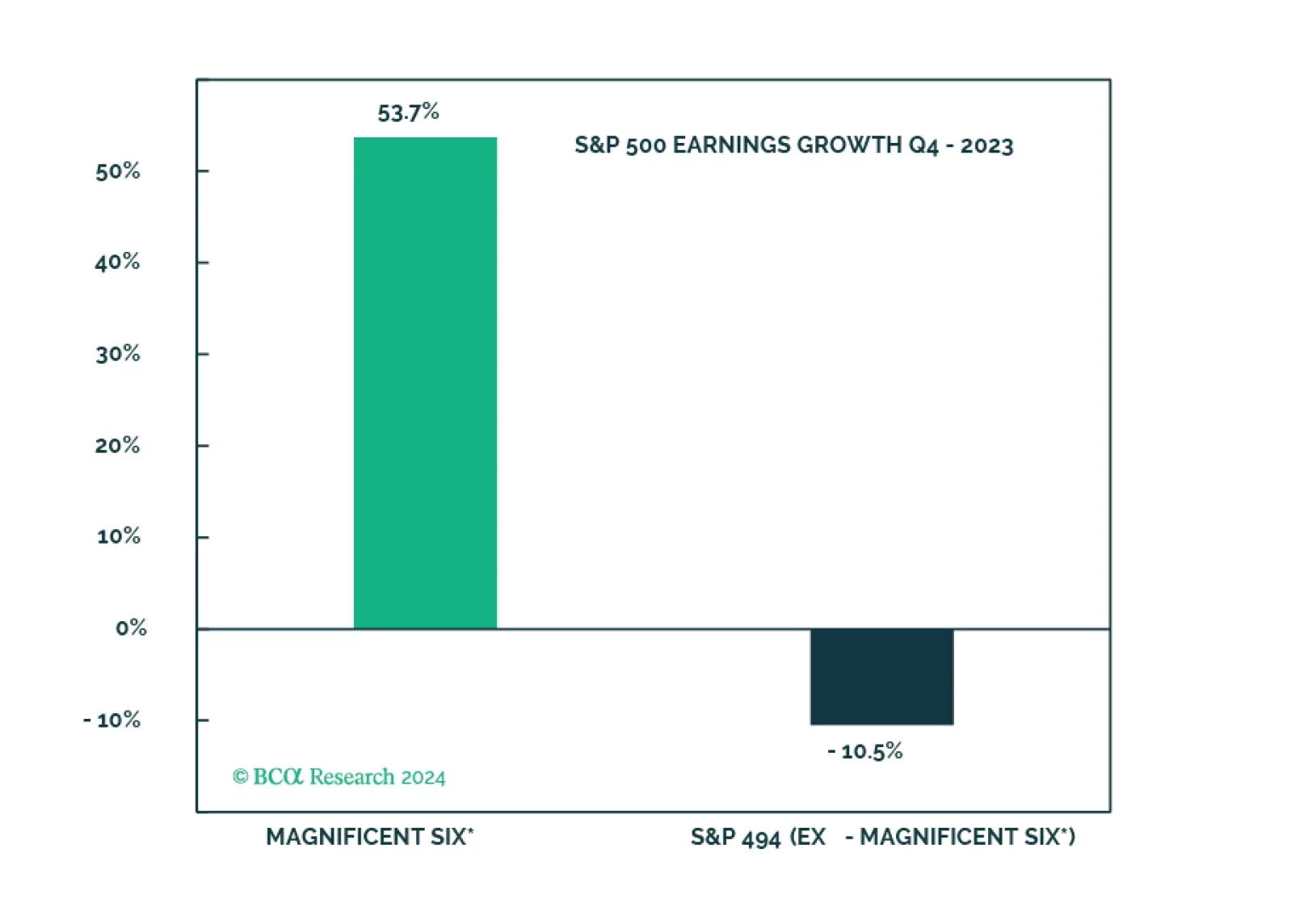

The soft landing and rate cuts narrative is being priced out, and the S&P 500 is overvalued and getting overbought. The Magnificent Seven are about to get a new moniker on the back of performance dispersion. However, without the cohort, S&P 500 earnings would have been even deeper in the red.

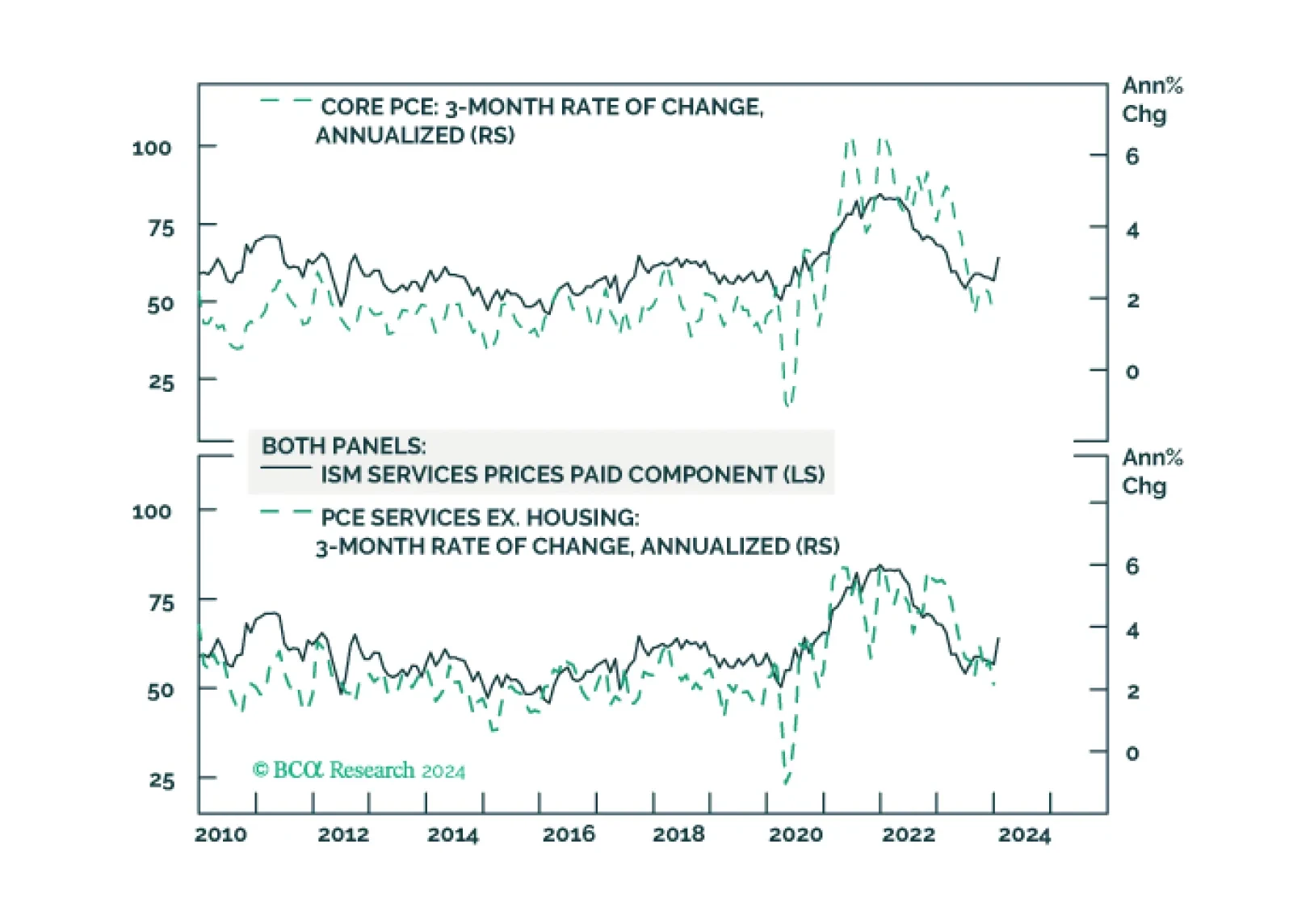

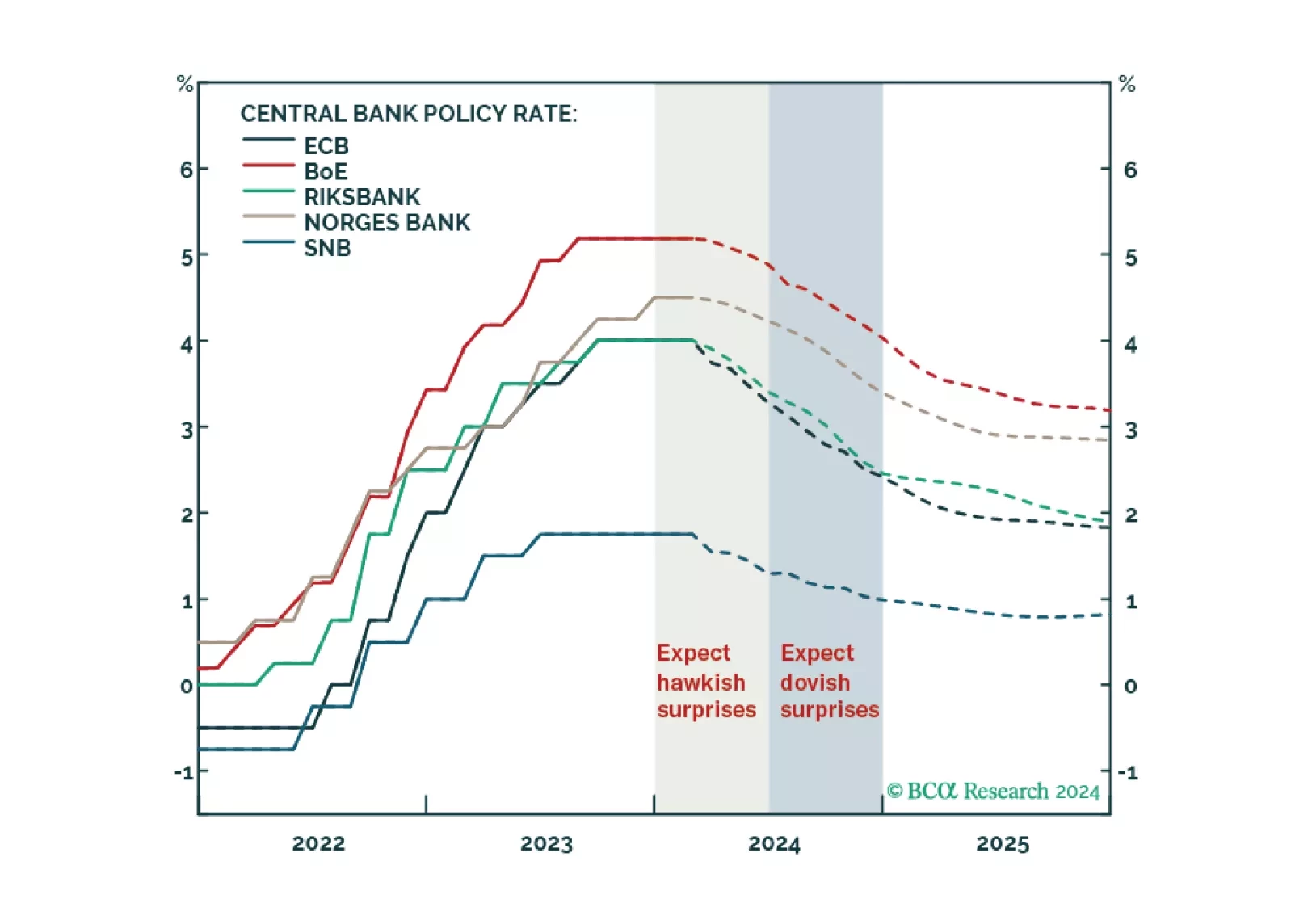

Our Central Bank Monitors support European central bankers’ decision to hold rates steady. Find out what it means for European fixed-income portfolio allocation.