Developed Countries

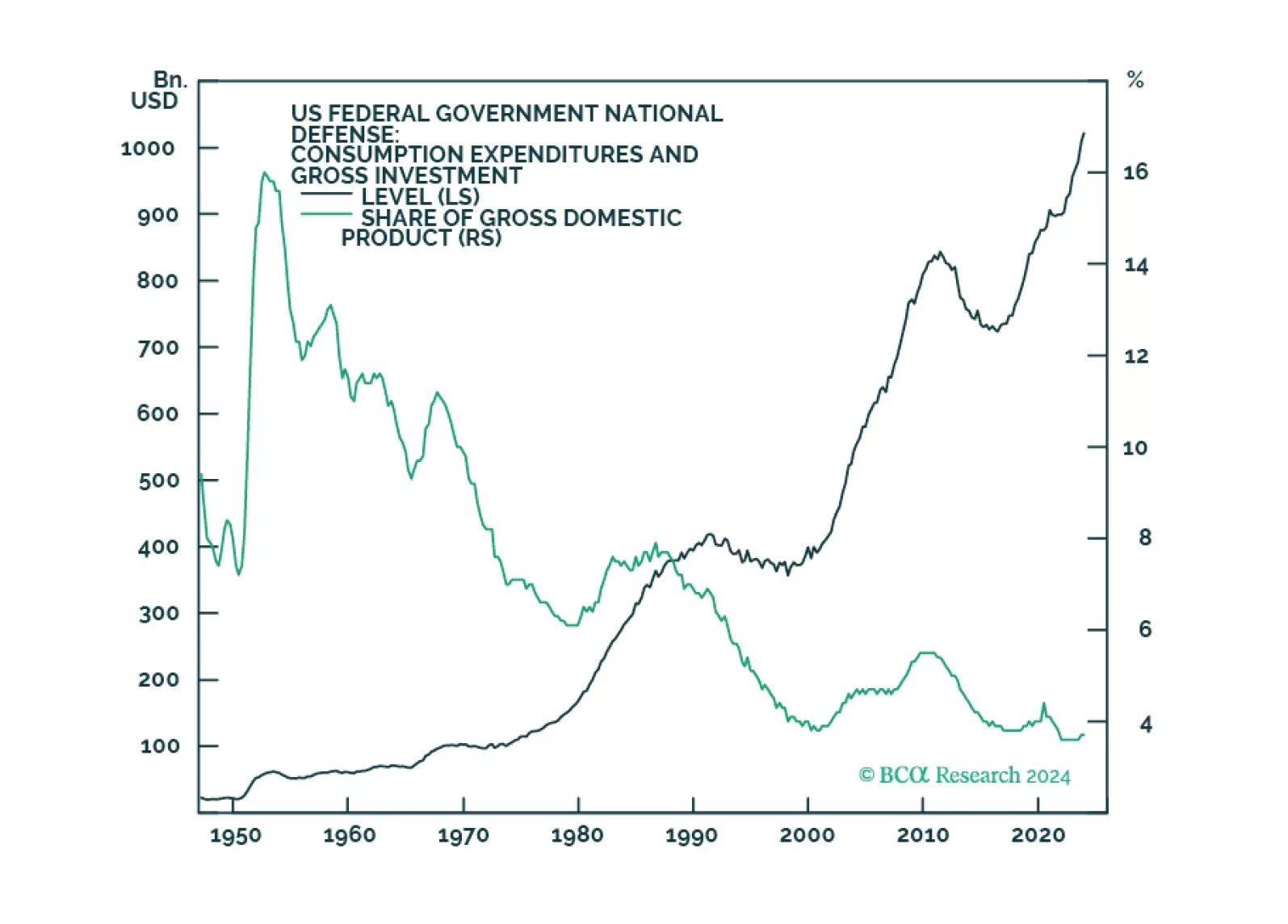

The US DoD rolled out its first-ever industrial policy designed to reverse decades of atrophy in its military-industrial complex. This left the US with diminished access to CMM commodities and supply chains, which are now dominated by China, and an industrial ecosystem to support its war-fighting mission that risks become uncompetitive. We remain long the XME and COMT ETFs to retain exposure to CMM producers and refiners. At tonight’s close, we will get long the Invesco Aerospace & Defense ETF (PPA), anticipating increased defense spending.

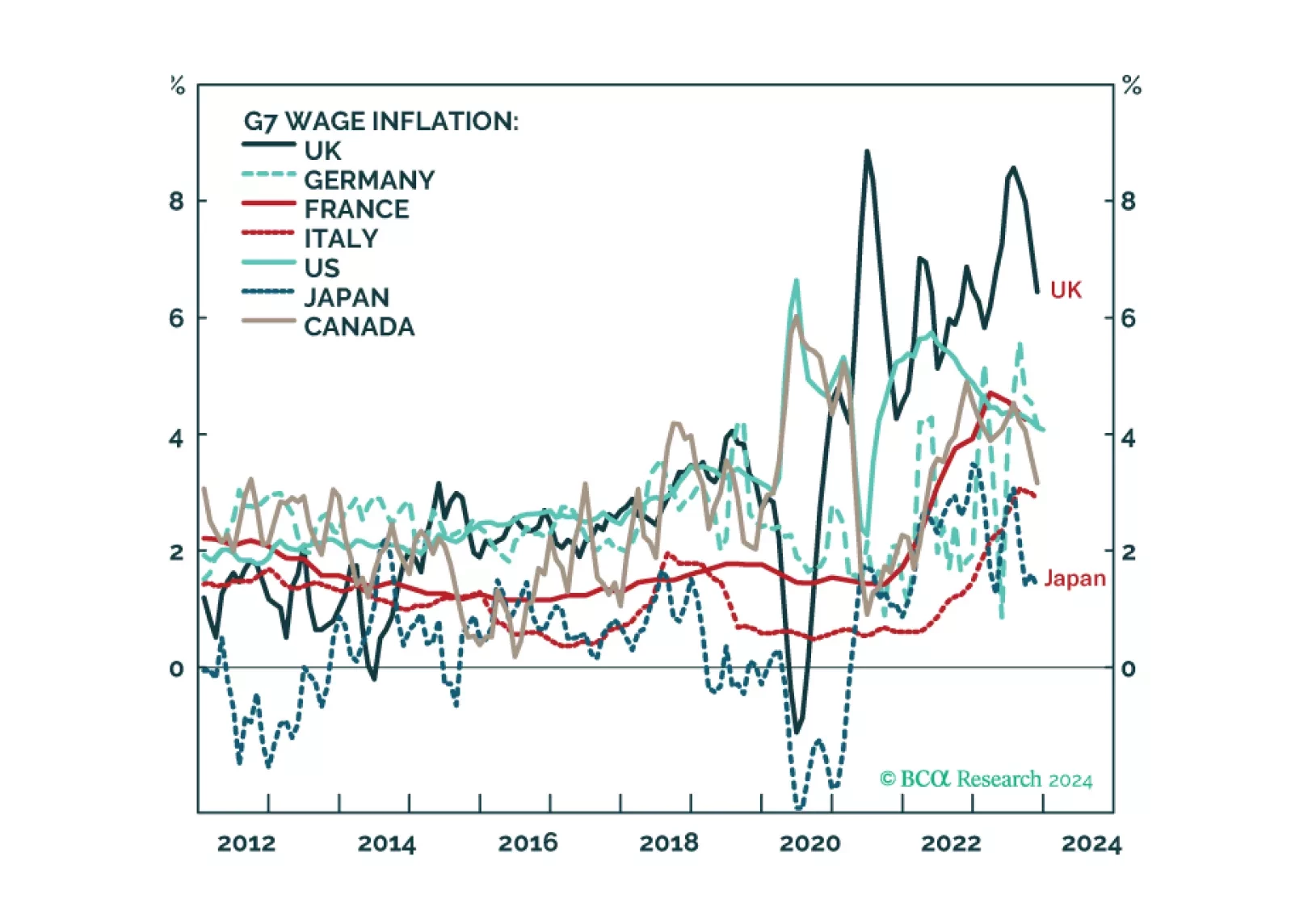

We describe and explain the wide disparity of wage inflation across G7 economies, and discuss what it means for the Fed, ECB, BoE, and BoJ policy moves in the coming year. Plus: we highlight two investments ripe for reversal, and two investments ripe for rebound.